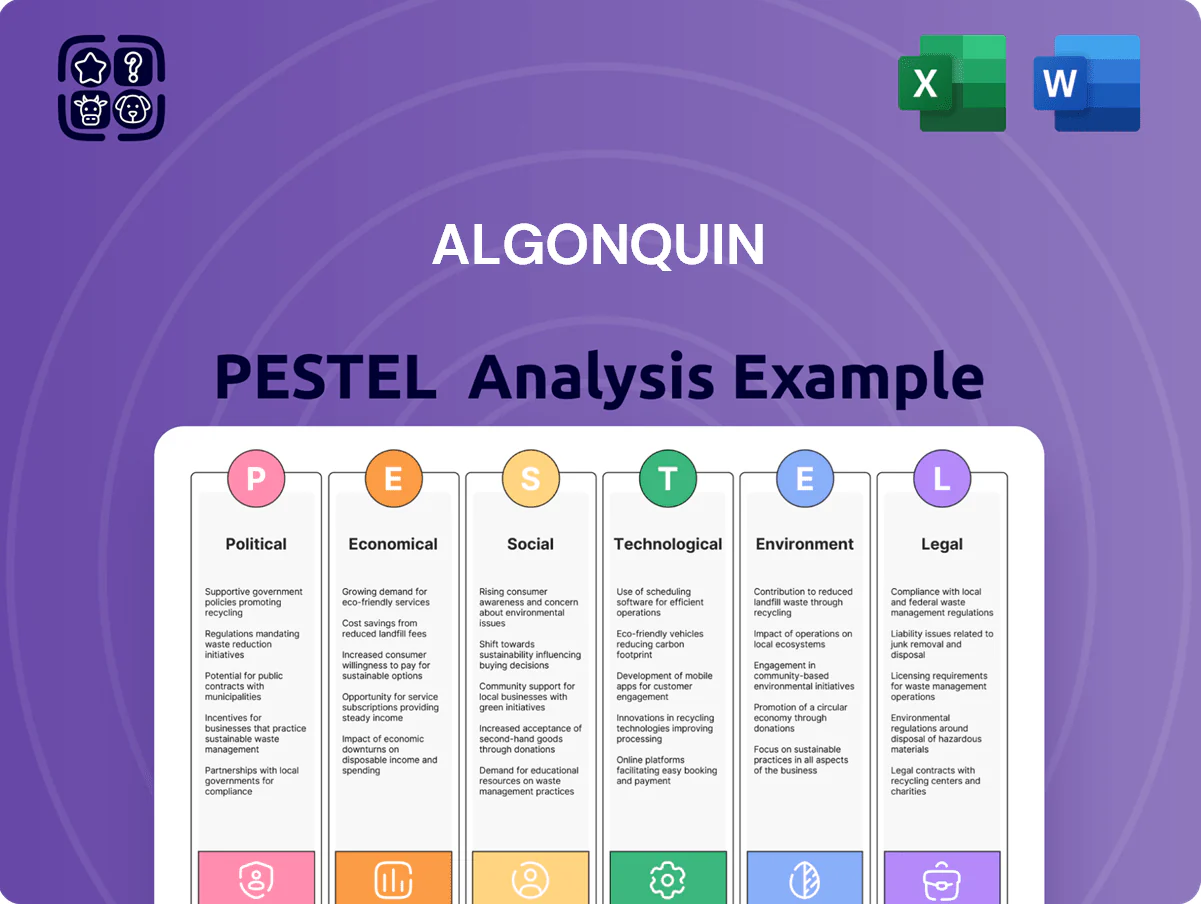

Algonquin PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, technological advances, legal developments, and environmental pressures collectively shape Algonquin’s strategic outlook; our concise PESTLE snapshot highlights the key external forces you need to know. Purchase the full analysis for a sector-by-sector deep dive, actionable risk mitigation strategies, and ready-to-use slides and tables to inform investments, board discussions, or strategic planning.

Political factors

Regulatory Oversight and Rate Case Approvals

Algonquin depends on state and provincial utility commissions to set consumer rates; favorable rate case approvals preserved a weighted average allowed ROE near 9.5% in recent 2024 decisions, and by end-2025 commissions’ political composition will directly shape allowed ROEs for capital recovery. Maintaining relationships with political appointees is essential across jurisdictions to protect cash flow for ~US$4.5bn regulated rate base and dividend coverage.

Transition to Pure-Play Utility Focus

The strategic pivot to divest Algonquin’s ~US$3.4bn renewables portfolio in 2024 was driven by shareholder pressure and political shifts favoring stable, regulated utility returns, with 2024 guidance emphasizing rate-regulated EBITDA to reach ~70% of total. This simplifies political risk by centering on local utility governance—state regulators, PUC decisions and tariff hearings—rather than volatile global energy policies. Management must manage political implications of asset sales, including approvals, tax treatments and potential pension/liability transfers affecting the 2025 balance sheet.

Government Incentives for Infrastructure Modernization

Federal programs in the US (Bipartisan Infrastructure Law allocations: roughly $65B for grid modernization through 2024) and Canada (2024 federal Investing in Canada Plan contributions) offer grants and tax credits for utility upgrades. Algonquin actively pursues these funds to offset capital spending on grid hardening and water-system projects, lowering its net investment needs. In 2024 Algonquin reported ~$120M in government funding that reduced ratepayer-funded capital by an estimated 8–10%.

Cross-Border Political Stability

Operating across Canada and the United States subjects Algonquin to two federal systems; in 2024 cross-border investments totaled roughly US$120bn in energy infrastructure, affecting permitting timelines and tariff frameworks impacting project returns.

Trade agreements like USMCA and evolving US-Canada clean energy policies shape capital flows and hydrogen/renewables trade; in 2025 proposed incentives could alter subsidy access for subsidiaries.

Algonquin’s planning assumes North American political stability, which supports a dividend payout ratio near 70% of FFO in 2024 and underpins long-term investment forecasts.

- Dual-jurisdiction regulatory risk affects permitting and tariffs

- USMCA and clean-energy incentives influence capital allocation

- 2024 FFO-based dividend payout ~70%

Impact of Federal Energy Policies

Federal carbon pricing and energy security measures raise Algonquin’s distribution costs; Canada’s federal carbon price was CAD 65/t in 2024 and rising to CAD 95/t by 2030, increasing fuel-switching and operational expense pressures on gas networks.

As federal mandates updated through 2025 push emissions targets and electrification incentives, Algonquin must revise long-term resource plans to stay compliant and avoid regulatory penalties that could affect cash flow.

A political tilt away from natural gas reduces valuation multiples for gas utility assets; market analysts in 2024 applied 20–30% lower enterprise value premiums to gas-heavy utilities versus diversified peers.

- 2024 carbon price CAD 65/t; CAD 95/t by 2030

- Mandates updated through 2025 require plan revisions

- Valuation discount 20–30% for gas-heavy utilities in 2024

Regulation, grants and carbon pricing reshape utility returns—9.5% ROE, $4.5B rate base

Regulatory politics drive allowed ROEs (~9.5% weighted in 2024) and shape recovery of a ~US$4.5bn rate base; 2024 divestiture refocused business to ~70% rate-regulated EBITDA. Federal grants (~US$120M to Algonquin in 2024) and US grid funding (~US$65B BIL) lower capex needs; Canada carbon price CAD65/t (2024) rising to CAD95/t (2030) increases operating costs and pressures gas-asset valuations (2024 discount 20–30%).

| Metric | 2024 | Outlook |

|---|---|---|

| Allowed ROE (Wtd) | ~9.5% | Commission composition to 2025 |

| Rate base | ~US$4.5bn | Stable |

| Govt funding | ~US$120M | Available |

| Carbon price (CA) | CAD65/t | CAD95/t by 2030 |

What is included in the product

Explores how macro-environmental factors uniquely affect the Algonquin across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends for reliable decision-making.

Condenses Algonquin's PESTLE into a clean, shareable summary for quick reference in meetings and presentations, visually segmented by category for immediate insight and easy drop‑in to slides or planning docs.

Economic factors

Interest Rate Volatility and Debt Servicing

As a capital-intensive utility, Algonquin is highly sensitive to central bank rate moves; Canada and the US policy rates hovering around 5% in late 2025 raise borrowing costs for the firm’s roughly CAD 34 billion consolidated debt stock. Analysts flag refinancing and new bond issuance for ongoing capex—Algonquin’s 2024–25 annual budget of ~USD 1.2–1.5 billion—as particularly exposed. Sustained high rates can compress EBITDA margins and restrict funding for growth projects.

Capital Allocation Post-Renewables Divestiture

The sale of Algonquin’s renewables unit closed in 2024, netting roughly US$3.5 billion in proceeds; investors expect swift redeployment toward debt reduction, with management targeting a debt/EBITDA reduction from 4.2x to ~3.5x, share buybacks, or capex in regulated utilities where returns average 7–9% ROIC. Efficient allocation is key to restore investment-grade metrics and improve the BBB- credit outlook cited by rating agencies in 2025.

Inflationary Pressures on Operational Costs

Persistent inflation through 2025 raised Algonquin's input costs—wages up ~4.5% YoY and material indexes up ~6% in 2024—pushing annual O&M expense growth above historical norms. Regulated frameworks allow cost recovery, but average lag of 12–24 months between expenditure and approved rate adjustments strains short-term liquidity. Higher equipment and contractor prices increased near-term capex by an estimated 5–8% versus 2023 budgets, making active cash management critical.

Currency Exchange Rate Fluctuations

Algonquin reports in USD while running major operations in Canada; CAD/USD moved from ~0.74 in Jan 2024 to ~0.73 in Dec 2024 and averaged 0.74–0.76 in 2025, creating reported-earnings volatility and altering USD dividend value for CAD-based cash flows.

The company uses forward contracts and natural hedges; disclosed hedging reduced FX sensitivity by an estimated 30–40% in 2024, but persistent CAD strength/weakness trends still affect long-term EPS and dividend purchasing power.

- Reported currency: USD; significant costs/revenue in CAD

- CAD/USD ~0.74 (2024 avg); 2025 range 0.73–0.76

- Hedging cut FX exposure ~30–40% in 2024

- Long-term currency trends continue to influence EPS and dividend value

Economic Growth in Service Jurisdictions

Economic growth in Algonquin’s service jurisdictions directly affects demand for electricity, water, and gas; U.S. metro GDP growth of ~2.5% in 2024 and population gains of 0.6%–1.2% in key states supported higher residential and commercial consumption.

Localized downturns—e.g., a 2023 manufacturing decline of 3% in parts of the Midwest—increase industrial demand risk and delinquency rates, while robust regional expansion drives new connections and capital projects that boost organic revenue.

- 2024 U.S. GDP ~2.5%

- Population growth 0.6%–1.2% in core states

- 2023 regional manufacturing drop ~3% in affected areas

- New connections and infrastructure expansion fuel organic revenue

Higher rates, CAD34bn debt and US$3.5bn relief reshape Algonquin’s 2024–25 capex risks

Higher policy rates (~5% in late 2025) raise borrowing costs for Algonquin’s ~CAD 34bn debt; 2024–25 capex budget ~USD 1.2–1.5bn faces refinancing risk. Sale of renewables in 2024 netted ~US$3.5bn to reduce debt (target debt/EBITDA ~3.5x) or fund regulated returns (7–9% ROIC). Inflation lifted wages ~4.5% and materials ~6% in 2024, increasing O&M and near-term capex 5–8%; CAD/USD ~0.74–0.76 (2024–25) adds FX volatility.

| Metric | Value |

|---|---|

| Consolidated debt | ~CAD 34bn |

| Capex 2024–25 | ~USD 1.2–1.5bn |

| Renewables sale | ~US$3.5bn (2024) |

| Debt/EBITDA target | ~3.5x |

| Policy rates (CA/US) | ~5% (late 2025) |

| Wage inflation (2024) | ~4.5% YoY |

| Materials inflation (2024) | ~6% YoY |

| Capex rise vs 2023 | ~5–8% |

| CAD/USD | ~0.74–0.76 (2024–25) |

Preview the Actual Deliverable

Algonquin PESTLE Analysis

The preview shown here is the exact Algonquin PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, technological advances, legal developments, and environmental pressures collectively shape Algonquin’s strategic outlook; our concise PESTLE snapshot highlights the key external forces you need to know. Purchase the full analysis for a sector-by-sector deep dive, actionable risk mitigation strategies, and ready-to-use slides and tables to inform investments, board discussions, or strategic planning.

Political factors

Regulatory Oversight and Rate Case Approvals

Algonquin depends on state and provincial utility commissions to set consumer rates; favorable rate case approvals preserved a weighted average allowed ROE near 9.5% in recent 2024 decisions, and by end-2025 commissions’ political composition will directly shape allowed ROEs for capital recovery. Maintaining relationships with political appointees is essential across jurisdictions to protect cash flow for ~US$4.5bn regulated rate base and dividend coverage.

Transition to Pure-Play Utility Focus

The strategic pivot to divest Algonquin’s ~US$3.4bn renewables portfolio in 2024 was driven by shareholder pressure and political shifts favoring stable, regulated utility returns, with 2024 guidance emphasizing rate-regulated EBITDA to reach ~70% of total. This simplifies political risk by centering on local utility governance—state regulators, PUC decisions and tariff hearings—rather than volatile global energy policies. Management must manage political implications of asset sales, including approvals, tax treatments and potential pension/liability transfers affecting the 2025 balance sheet.

Government Incentives for Infrastructure Modernization

Federal programs in the US (Bipartisan Infrastructure Law allocations: roughly $65B for grid modernization through 2024) and Canada (2024 federal Investing in Canada Plan contributions) offer grants and tax credits for utility upgrades. Algonquin actively pursues these funds to offset capital spending on grid hardening and water-system projects, lowering its net investment needs. In 2024 Algonquin reported ~$120M in government funding that reduced ratepayer-funded capital by an estimated 8–10%.

Cross-Border Political Stability

Operating across Canada and the United States subjects Algonquin to two federal systems; in 2024 cross-border investments totaled roughly US$120bn in energy infrastructure, affecting permitting timelines and tariff frameworks impacting project returns.

Trade agreements like USMCA and evolving US-Canada clean energy policies shape capital flows and hydrogen/renewables trade; in 2025 proposed incentives could alter subsidy access for subsidiaries.

Algonquin’s planning assumes North American political stability, which supports a dividend payout ratio near 70% of FFO in 2024 and underpins long-term investment forecasts.

- Dual-jurisdiction regulatory risk affects permitting and tariffs

- USMCA and clean-energy incentives influence capital allocation

- 2024 FFO-based dividend payout ~70%

Impact of Federal Energy Policies

Federal carbon pricing and energy security measures raise Algonquin’s distribution costs; Canada’s federal carbon price was CAD 65/t in 2024 and rising to CAD 95/t by 2030, increasing fuel-switching and operational expense pressures on gas networks.

As federal mandates updated through 2025 push emissions targets and electrification incentives, Algonquin must revise long-term resource plans to stay compliant and avoid regulatory penalties that could affect cash flow.

A political tilt away from natural gas reduces valuation multiples for gas utility assets; market analysts in 2024 applied 20–30% lower enterprise value premiums to gas-heavy utilities versus diversified peers.

- 2024 carbon price CAD 65/t; CAD 95/t by 2030

- Mandates updated through 2025 require plan revisions

- Valuation discount 20–30% for gas-heavy utilities in 2024

Regulation, grants and carbon pricing reshape utility returns—9.5% ROE, $4.5B rate base

Regulatory politics drive allowed ROEs (~9.5% weighted in 2024) and shape recovery of a ~US$4.5bn rate base; 2024 divestiture refocused business to ~70% rate-regulated EBITDA. Federal grants (~US$120M to Algonquin in 2024) and US grid funding (~US$65B BIL) lower capex needs; Canada carbon price CAD65/t (2024) rising to CAD95/t (2030) increases operating costs and pressures gas-asset valuations (2024 discount 20–30%).

| Metric | 2024 | Outlook |

|---|---|---|

| Allowed ROE (Wtd) | ~9.5% | Commission composition to 2025 |

| Rate base | ~US$4.5bn | Stable |

| Govt funding | ~US$120M | Available |

| Carbon price (CA) | CAD65/t | CAD95/t by 2030 |

What is included in the product

Explores how macro-environmental factors uniquely affect the Algonquin across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends for reliable decision-making.

Condenses Algonquin's PESTLE into a clean, shareable summary for quick reference in meetings and presentations, visually segmented by category for immediate insight and easy drop‑in to slides or planning docs.

Economic factors

Interest Rate Volatility and Debt Servicing

As a capital-intensive utility, Algonquin is highly sensitive to central bank rate moves; Canada and the US policy rates hovering around 5% in late 2025 raise borrowing costs for the firm’s roughly CAD 34 billion consolidated debt stock. Analysts flag refinancing and new bond issuance for ongoing capex—Algonquin’s 2024–25 annual budget of ~USD 1.2–1.5 billion—as particularly exposed. Sustained high rates can compress EBITDA margins and restrict funding for growth projects.

Capital Allocation Post-Renewables Divestiture

The sale of Algonquin’s renewables unit closed in 2024, netting roughly US$3.5 billion in proceeds; investors expect swift redeployment toward debt reduction, with management targeting a debt/EBITDA reduction from 4.2x to ~3.5x, share buybacks, or capex in regulated utilities where returns average 7–9% ROIC. Efficient allocation is key to restore investment-grade metrics and improve the BBB- credit outlook cited by rating agencies in 2025.

Inflationary Pressures on Operational Costs

Persistent inflation through 2025 raised Algonquin's input costs—wages up ~4.5% YoY and material indexes up ~6% in 2024—pushing annual O&M expense growth above historical norms. Regulated frameworks allow cost recovery, but average lag of 12–24 months between expenditure and approved rate adjustments strains short-term liquidity. Higher equipment and contractor prices increased near-term capex by an estimated 5–8% versus 2023 budgets, making active cash management critical.

Currency Exchange Rate Fluctuations

Algonquin reports in USD while running major operations in Canada; CAD/USD moved from ~0.74 in Jan 2024 to ~0.73 in Dec 2024 and averaged 0.74–0.76 in 2025, creating reported-earnings volatility and altering USD dividend value for CAD-based cash flows.

The company uses forward contracts and natural hedges; disclosed hedging reduced FX sensitivity by an estimated 30–40% in 2024, but persistent CAD strength/weakness trends still affect long-term EPS and dividend purchasing power.

- Reported currency: USD; significant costs/revenue in CAD

- CAD/USD ~0.74 (2024 avg); 2025 range 0.73–0.76

- Hedging cut FX exposure ~30–40% in 2024

- Long-term currency trends continue to influence EPS and dividend value

Economic Growth in Service Jurisdictions

Economic growth in Algonquin’s service jurisdictions directly affects demand for electricity, water, and gas; U.S. metro GDP growth of ~2.5% in 2024 and population gains of 0.6%–1.2% in key states supported higher residential and commercial consumption.

Localized downturns—e.g., a 2023 manufacturing decline of 3% in parts of the Midwest—increase industrial demand risk and delinquency rates, while robust regional expansion drives new connections and capital projects that boost organic revenue.

- 2024 U.S. GDP ~2.5%

- Population growth 0.6%–1.2% in core states

- 2023 regional manufacturing drop ~3% in affected areas

- New connections and infrastructure expansion fuel organic revenue

Higher rates, CAD34bn debt and US$3.5bn relief reshape Algonquin’s 2024–25 capex risks

Higher policy rates (~5% in late 2025) raise borrowing costs for Algonquin’s ~CAD 34bn debt; 2024–25 capex budget ~USD 1.2–1.5bn faces refinancing risk. Sale of renewables in 2024 netted ~US$3.5bn to reduce debt (target debt/EBITDA ~3.5x) or fund regulated returns (7–9% ROIC). Inflation lifted wages ~4.5% and materials ~6% in 2024, increasing O&M and near-term capex 5–8%; CAD/USD ~0.74–0.76 (2024–25) adds FX volatility.

| Metric | Value |

|---|---|

| Consolidated debt | ~CAD 34bn |

| Capex 2024–25 | ~USD 1.2–1.5bn |

| Renewables sale | ~US$3.5bn (2024) |

| Debt/EBITDA target | ~3.5x |

| Policy rates (CA/US) | ~5% (late 2025) |

| Wage inflation (2024) | ~4.5% YoY |

| Materials inflation (2024) | ~6% YoY |

| Capex rise vs 2023 | ~5–8% |

| CAD/USD | ~0.74–0.76 (2024–25) |

Preview the Actual Deliverable

Algonquin PESTLE Analysis

The preview shown here is the exact Algonquin PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.