Alibaba Group Boston Consulting Group Matrix

See the Bigger Picture

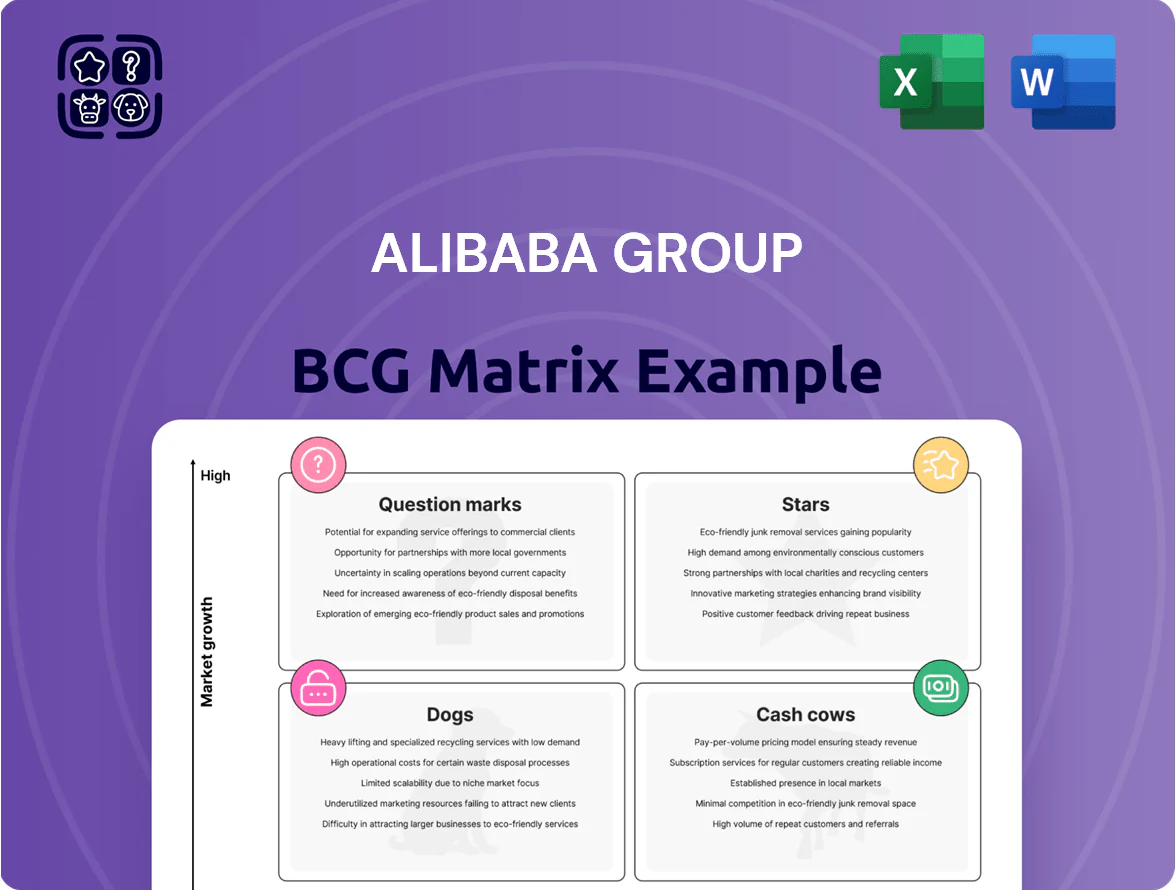

Alibaba’s BCG Matrix snapshot shows a diversified portfolio where core e-commerce and cloud services likely sit as Stars/Cash Cows while newer ventures may appear as Question Marks or Dogs, reflecting varied growth and market-share dynamics across China and international markets. This preview highlights strategic tensions—capital allocation, scaling cloud profitability, and pruning low-return bets—that shape Alibaba’s roadmap. Get the full BCG Matrix report for quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel files to inform investment and operational decisions.

Stars

Alibaba Cloud Intelligence

Alibaba Cloud Intelligence sits in the BCG Matrix as a Star: market leader in China and APAC by late 2025, holding ~40% China IaaS market share and growing revenue 28% YoY in FY2025 to RMB 125 billion driven by generative AI training and enterprise digitalization.

High demand keeps growth strong despite market maturity, but heavy capex remains—Alibaba earmarked RMB 60–80 billion for data-center buildout in 2025–26 to sustain performance and match global peers.

The unit is the group’s technological backbone and main innovation engine, powering cloud, AI products, and cross-group digital transformation initiatives that underpin future revenue streams.

Cainiao Smart Logistics

Cainiao Smart Logistics, part of Alibaba Group, became a global leader in end-to-end supply chains, operating 150+ automated warehouses and 60 global hubs and capturing an estimated 28% share of the smart logistics market by late 2025.

Cainiao drives substantial revenue—about RMB 42 billion in FY2024—but heavy capex for physical expansion consumed roughly 65% of operating cash flow, limiting free cash generation.

Despite high cash consumption, Cainiao remains strategic to Alibaba’s global e-commerce growth, supporting cross-border fulfillment and reducing average delivery times by 22% on core routes.

AliExpress Global

AliExpress Global, part of Alibaba Group, moved into a BCG Matrix star by late 2025 after Choice service and faster Europe/Latin America delivery drove GMV growth to about $32 billion in 2025, up ~18% year-over-year.

It dominates cross-border B2C for value-conscious shoppers, holding an estimated 28% share of global budget cross-border e-commerce in 2025, while Alibaba keeps heavy local marketing and logistics subsidies to defend share.

This high-growth segment is strategic: AliExpress contributed roughly 12% of Alibaba Group’s international revenue in FY2025, aiding diversification away from China.

DingTalk Enterprise Suite

DingTalk, Alibaba Group’s enterprise suite, remains China’s top internal collaboration platform with over 200 million monthly active enterprise users as of Dec 2025 and double‑digit ARR growth driven by AI assistants embedded in workflows.

Market share exceeds 45% for corporate internal tools; ongoing R&D spend (~RMB 3.2 billion in 2024) is needed to counter Tencent Meeting and niche rivals as DingTalk shifts from high‑growth star toward a stabilized, monetizing product.

- 200M monthly enterprise users (Dec 2025)

- 45%+ market share in internal tools

- Double‑digit ARR growth through 2025

- R&D spend ~RMB 3.2B in 2024

- Transitioning from star to stable monetized platform

Lazada Southeast Asia

Lazada Southeast Asia, part of Alibaba Group, is a Star in the BCG Matrix: a top-tier player in high-growth SEA e-commerce, especially Indonesia and Thailand, with estimated ~20–25% market share in key markets as of 2025 and GMV growth above 25% YoY.

It owns localized logistics and payments (Cainiao tie-ins, e-wallets) driving penetration; continued heavy cash burn for CAC and promos is required amid fierce competition from Shopee and Tokopedia.

Alibaba treats Lazada as a strategic pillar to capture ASEAN rising middle-class consumption; Alibaba allocated multibillion-dollar support rounds since 2021, keeping investment priority into 2025.

- 2025: ~20–25% share in Indonesia/Thailand

- GMV growth: >25% YoY

- High CAC; ongoing cash injections

- Key strategic pillar for ASEAN middle-class

Alibaba's Growth Engines: Cloud, Logistics, Retail & SaaS Powering 2025 Momentum

Alibaba Stars: Cloud (~40% China IaaS, RMB125B FY2025, +28% YoY; RMB60–80B capex 2025–26), Cainiao (150+ auto warehouses, RMB42B FY2024, 65% OCF capex), AliExpress (GMV $32B 2025, +18% YoY, 28% budget cross‑border share), DingTalk (200M MAU Dec2025, 45%+ share), Lazada (20–25% SEA share, >25% GMV growth).

| Unit | Key metric | 2025 |

|---|---|---|

| Cloud | Revenue/capex | RMB125B/RMB60–80B |

| Cainiao | Rev/warehouses | RMB42B/150+ |

| AliExpress | GMV/share | $32B/28% |

| DingTalk | MAU/share | 200M/45%+ |

| Lazada | Market share/GMV growth | 20–25%/>25% |

What is included in the product

BCG Matrix for Alibaba: assesses each business as Star, Cash Cow, Question Mark, or Dog with strategic investment, hold, or divest guidance.

One-page overview placing each Alibaba business unit in a quadrant, simplifying portfolio choices for executive decision-making.

Cash Cows

Taobao Marketplace

Taobao Marketplace remains Alibaba Group’s top cash generator, holding roughly 55% of China’s consumer-to-consumer (C2C) e-commerce GMV in 2025 and contributing about RMB 120 billion in operating profit in FY2024–25.

By end-2025 Taobao is mature: user growth is low-single-digits and GMV growth slowed to ~6% year-over-year, so it needs minimal capex versus new ventures.

High margins and low incremental investment let Taobao fund R&D and experimental units, making it the quintessential cash cow that supplies group liquidity for strategic bets.

Tmall Premium Retail

Tmall Premium Retail anchors Alibaba’s B2C dominance, hosting 60%+ of China’s online premium brand storefronts and capturing roughly 35% of national B2C GMV in 2024, making it a high-market-share cash cow.

It delivers steady commission and marketing income—about RMB 110 billion in service revenue in FY2024—prioritizing margin efficiency and retention over aggressive user growth.

With premium online goods maturing, Tmall emphasizes cost-per-order cuts and loyalty programs; its predictable cash flow supports Alibaba’s net interest costs and funds R&D investments, including RMB 30–40 billion annually.

Alibaba.com B2B

Alibaba.com, the group’s original B2B unit, still leads global wholesale trade in 2025, handling over $150 billion in annual GMV and connecting ~20 million suppliers with 200+ markets.

Operating in a mature, low-growth B2B market, it holds a very high market share in China–export manufacturing and needs far less marketing spend than newer consumer platforms.

With ~30% adjusted EBITDA margin in 2024 and steady revenue, it reliably funds Alibaba Group’s core operations and strategic bets.

Ant Group Stake

Alibaba holds a material stake in Ant Group, owner of Alipay, giving Alibaba steady investment income and strategic payment synergies; Ant reported GMV of ~155 trillion RMB in 2024 and processed payments for 1.3 billion users by end-2024.

Alipay dominates China’s mature mobile-payments market (market share ~55% in 2024), serving as a daily utility for hundreds of millions; domestic payment growth was modest at ~6% CAGR 2022–2025.

Regulation stabilized by 2025, so Ant is a reliable cash cow: predictable dividends and fee income support Alibaba’s cash flow and keep its e-commerce ecosystem tightly integrated with secure payments.

- Stake provides steady investment income and strategic integration

- Alipay: ~1.3B users, ~155T RMB GMV (2024)

- Market share ~55%, domestic payments growth ~6% CAGR (2022–25)

- Regulatory risks eased by 2025; asset is cash-generating

Freshippo Hema

Freshippo Hema, Alibaba Group’s grocery chain, reached maturity in Tier 1–2 Chinese cities by end-2025, holding a leading share in New Retail with ~18–22% segment share and >200 stores in metro areas.

After heavy capex 2016–2023, unit economics improved: gross margin rose to ~27% and same-store sales growth stabilized ~4–6% in 2025, boosting operating profit contribution to Alibaba’s local retail revenue.

It now generates steady cash flow from a loyal, high-spend customer base—average basket size ~¥180 and online delivery fulfillment under 30 minutes—serving as a Cash Cow in Alibaba’s BCG matrix.

- Market share: ~18–22% New Retail

- Stores: >200 metro stores (end-2025)

- Gross margin: ~27% (2025)

- SSS growth: 4–6% (2025)

- Avg basket: ~¥180; delivery <30 min

Alibaba’s Cash Cows: Taobao, Tmall, Alibaba.com, Ant & Freshippo Powering Strong Profits

Taobao, Tmall, Alibaba.com, Ant (Alipay) and Freshippo are cash cows: Taobao ~RMB120bn OP (FY24–25), Tmall service revenue ~RMB110bn (FY24), Alibaba.com GMV >$150bn (2025), Ant GMV ~155T RMB/1.3B users (2024), Freshippo gross margin ~27%/SSS 4–6% (2025).

| Unit | Key 2024–25 |

|---|---|

| Taobao | RMB120bn OP; GMV share 55% |

| Tmall | RMB110bn service rev; 35% B2C GMV |

| Alibaba.com | $150bn GMV; 30% EBITDA |

| Ant/Alipay | 155T RMB GMV; 1.3B users |

| Freshippo | 27% GM; SSS 4–6% |

Full Transparency, Always

Alibaba Group BCG Matrix

The file you're previewing is the final Alibaba Group BCG Matrix you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analyst-ready report designed for strategic clarity and presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Alibaba’s BCG Matrix snapshot shows a diversified portfolio where core e-commerce and cloud services likely sit as Stars/Cash Cows while newer ventures may appear as Question Marks or Dogs, reflecting varied growth and market-share dynamics across China and international markets. This preview highlights strategic tensions—capital allocation, scaling cloud profitability, and pruning low-return bets—that shape Alibaba’s roadmap. Get the full BCG Matrix report for quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel files to inform investment and operational decisions.

Stars

Alibaba Cloud Intelligence

Alibaba Cloud Intelligence sits in the BCG Matrix as a Star: market leader in China and APAC by late 2025, holding ~40% China IaaS market share and growing revenue 28% YoY in FY2025 to RMB 125 billion driven by generative AI training and enterprise digitalization.

High demand keeps growth strong despite market maturity, but heavy capex remains—Alibaba earmarked RMB 60–80 billion for data-center buildout in 2025–26 to sustain performance and match global peers.

The unit is the group’s technological backbone and main innovation engine, powering cloud, AI products, and cross-group digital transformation initiatives that underpin future revenue streams.

Cainiao Smart Logistics

Cainiao Smart Logistics, part of Alibaba Group, became a global leader in end-to-end supply chains, operating 150+ automated warehouses and 60 global hubs and capturing an estimated 28% share of the smart logistics market by late 2025.

Cainiao drives substantial revenue—about RMB 42 billion in FY2024—but heavy capex for physical expansion consumed roughly 65% of operating cash flow, limiting free cash generation.

Despite high cash consumption, Cainiao remains strategic to Alibaba’s global e-commerce growth, supporting cross-border fulfillment and reducing average delivery times by 22% on core routes.

AliExpress Global

AliExpress Global, part of Alibaba Group, moved into a BCG Matrix star by late 2025 after Choice service and faster Europe/Latin America delivery drove GMV growth to about $32 billion in 2025, up ~18% year-over-year.

It dominates cross-border B2C for value-conscious shoppers, holding an estimated 28% share of global budget cross-border e-commerce in 2025, while Alibaba keeps heavy local marketing and logistics subsidies to defend share.

This high-growth segment is strategic: AliExpress contributed roughly 12% of Alibaba Group’s international revenue in FY2025, aiding diversification away from China.

DingTalk Enterprise Suite

DingTalk, Alibaba Group’s enterprise suite, remains China’s top internal collaboration platform with over 200 million monthly active enterprise users as of Dec 2025 and double‑digit ARR growth driven by AI assistants embedded in workflows.

Market share exceeds 45% for corporate internal tools; ongoing R&D spend (~RMB 3.2 billion in 2024) is needed to counter Tencent Meeting and niche rivals as DingTalk shifts from high‑growth star toward a stabilized, monetizing product.

- 200M monthly enterprise users (Dec 2025)

- 45%+ market share in internal tools

- Double‑digit ARR growth through 2025

- R&D spend ~RMB 3.2B in 2024

- Transitioning from star to stable monetized platform

Lazada Southeast Asia

Lazada Southeast Asia, part of Alibaba Group, is a Star in the BCG Matrix: a top-tier player in high-growth SEA e-commerce, especially Indonesia and Thailand, with estimated ~20–25% market share in key markets as of 2025 and GMV growth above 25% YoY.

It owns localized logistics and payments (Cainiao tie-ins, e-wallets) driving penetration; continued heavy cash burn for CAC and promos is required amid fierce competition from Shopee and Tokopedia.

Alibaba treats Lazada as a strategic pillar to capture ASEAN rising middle-class consumption; Alibaba allocated multibillion-dollar support rounds since 2021, keeping investment priority into 2025.

- 2025: ~20–25% share in Indonesia/Thailand

- GMV growth: >25% YoY

- High CAC; ongoing cash injections

- Key strategic pillar for ASEAN middle-class

Alibaba's Growth Engines: Cloud, Logistics, Retail & SaaS Powering 2025 Momentum

Alibaba Stars: Cloud (~40% China IaaS, RMB125B FY2025, +28% YoY; RMB60–80B capex 2025–26), Cainiao (150+ auto warehouses, RMB42B FY2024, 65% OCF capex), AliExpress (GMV $32B 2025, +18% YoY, 28% budget cross‑border share), DingTalk (200M MAU Dec2025, 45%+ share), Lazada (20–25% SEA share, >25% GMV growth).

| Unit | Key metric | 2025 |

|---|---|---|

| Cloud | Revenue/capex | RMB125B/RMB60–80B |

| Cainiao | Rev/warehouses | RMB42B/150+ |

| AliExpress | GMV/share | $32B/28% |

| DingTalk | MAU/share | 200M/45%+ |

| Lazada | Market share/GMV growth | 20–25%/>25% |

What is included in the product

BCG Matrix for Alibaba: assesses each business as Star, Cash Cow, Question Mark, or Dog with strategic investment, hold, or divest guidance.

One-page overview placing each Alibaba business unit in a quadrant, simplifying portfolio choices for executive decision-making.

Cash Cows

Taobao Marketplace

Taobao Marketplace remains Alibaba Group’s top cash generator, holding roughly 55% of China’s consumer-to-consumer (C2C) e-commerce GMV in 2025 and contributing about RMB 120 billion in operating profit in FY2024–25.

By end-2025 Taobao is mature: user growth is low-single-digits and GMV growth slowed to ~6% year-over-year, so it needs minimal capex versus new ventures.

High margins and low incremental investment let Taobao fund R&D and experimental units, making it the quintessential cash cow that supplies group liquidity for strategic bets.

Tmall Premium Retail

Tmall Premium Retail anchors Alibaba’s B2C dominance, hosting 60%+ of China’s online premium brand storefronts and capturing roughly 35% of national B2C GMV in 2024, making it a high-market-share cash cow.

It delivers steady commission and marketing income—about RMB 110 billion in service revenue in FY2024—prioritizing margin efficiency and retention over aggressive user growth.

With premium online goods maturing, Tmall emphasizes cost-per-order cuts and loyalty programs; its predictable cash flow supports Alibaba’s net interest costs and funds R&D investments, including RMB 30–40 billion annually.

Alibaba.com B2B

Alibaba.com, the group’s original B2B unit, still leads global wholesale trade in 2025, handling over $150 billion in annual GMV and connecting ~20 million suppliers with 200+ markets.

Operating in a mature, low-growth B2B market, it holds a very high market share in China–export manufacturing and needs far less marketing spend than newer consumer platforms.

With ~30% adjusted EBITDA margin in 2024 and steady revenue, it reliably funds Alibaba Group’s core operations and strategic bets.

Ant Group Stake

Alibaba holds a material stake in Ant Group, owner of Alipay, giving Alibaba steady investment income and strategic payment synergies; Ant reported GMV of ~155 trillion RMB in 2024 and processed payments for 1.3 billion users by end-2024.

Alipay dominates China’s mature mobile-payments market (market share ~55% in 2024), serving as a daily utility for hundreds of millions; domestic payment growth was modest at ~6% CAGR 2022–2025.

Regulation stabilized by 2025, so Ant is a reliable cash cow: predictable dividends and fee income support Alibaba’s cash flow and keep its e-commerce ecosystem tightly integrated with secure payments.

- Stake provides steady investment income and strategic integration

- Alipay: ~1.3B users, ~155T RMB GMV (2024)

- Market share ~55%, domestic payments growth ~6% CAGR (2022–25)

- Regulatory risks eased by 2025; asset is cash-generating

Freshippo Hema

Freshippo Hema, Alibaba Group’s grocery chain, reached maturity in Tier 1–2 Chinese cities by end-2025, holding a leading share in New Retail with ~18–22% segment share and >200 stores in metro areas.

After heavy capex 2016–2023, unit economics improved: gross margin rose to ~27% and same-store sales growth stabilized ~4–6% in 2025, boosting operating profit contribution to Alibaba’s local retail revenue.

It now generates steady cash flow from a loyal, high-spend customer base—average basket size ~¥180 and online delivery fulfillment under 30 minutes—serving as a Cash Cow in Alibaba’s BCG matrix.

- Market share: ~18–22% New Retail

- Stores: >200 metro stores (end-2025)

- Gross margin: ~27% (2025)

- SSS growth: 4–6% (2025)

- Avg basket: ~¥180; delivery <30 min

Alibaba’s Cash Cows: Taobao, Tmall, Alibaba.com, Ant & Freshippo Powering Strong Profits

Taobao, Tmall, Alibaba.com, Ant (Alipay) and Freshippo are cash cows: Taobao ~RMB120bn OP (FY24–25), Tmall service revenue ~RMB110bn (FY24), Alibaba.com GMV >$150bn (2025), Ant GMV ~155T RMB/1.3B users (2024), Freshippo gross margin ~27%/SSS 4–6% (2025).

| Unit | Key 2024–25 |

|---|---|

| Taobao | RMB120bn OP; GMV share 55% |

| Tmall | RMB110bn service rev; 35% B2C GMV |

| Alibaba.com | $150bn GMV; 30% EBITDA |

| Ant/Alipay | 155T RMB GMV; 1.3B users |

| Freshippo | 27% GM; SSS 4–6% |

Full Transparency, Always

Alibaba Group BCG Matrix

The file you're previewing is the final Alibaba Group BCG Matrix you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analyst-ready report designed for strategic clarity and presentation.