Alimak Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

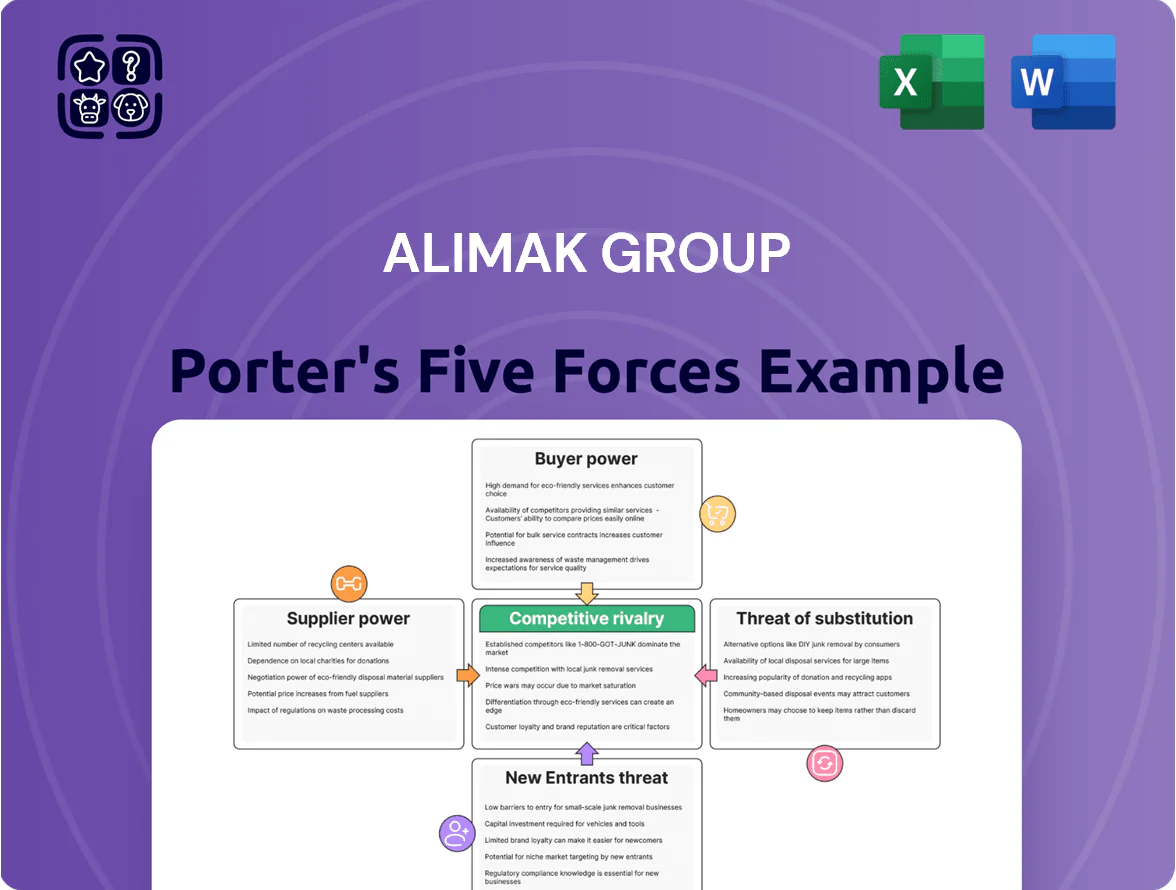

Suppliers Bargaining Power

Raw Material Price Volatility

Alimak depends on steel, aluminum and electronic components, so global commodity swings — steel up ~18% and aluminum up ~14% in 2021–2023 supply shocks — raise input-cost risk.

Multiple vendors lower single-supplier exposure, but the need for high-grade, certified materials keeps the pool of qualified suppliers small.

By late 2025, energy-driven inflation (EU industrial gas prices +60% vs 2021) has let suppliers continue passing costs to OEMs, squeezing margins.

Specialized Component Dependency

Integration of IoT sensors and automated controls forces Alimak to buy specialized electronic modules from a small set of global semiconductor suppliers, who in 2024 captured ~65% of the industrial IoT components market and can demand premiums of 10–25% on non-commodity parts.

Switching Costs for Technical Parts

Switching proprietary safety components and patented drive systems imposes high costs and months-long certification: recertifying a primary supplier can take 6–18 months and cost €200k–€1.2M per product line based on industry averages for vertical access equipment compliance.

Supplier Consolidation Trends

The global industrial supply chain saw M&A activity concentrate suppliers: between 2018–2024 the top 10 global elevator/machinery parts suppliers’ combined market share rose from ~36% to ~49%, tightening supplier leverage.

Large consolidated suppliers now push longer lead times (+15–30 days) and higher minimum order quantities (up to 40% increase), raising procurement costs for mid-sized OEMs.

Alimak offsets some pressure by centralizing purchasing across 50+ country operations and $420m FY2024 revenue scale, but mega-conglomerates’ pricing power still compresses margins.

- Top-10 supplier share: ~49% (2024)

- Lead-time increase: +15–30 days

- MOQ rise: up to +40%

- Alimak FY2024 revenue: $420m

- Global purchasing across 50+ countries

Labor Market Constraints

Suppliers of specialized engineering services and fabricated sub-assemblies face chronic shortages of skilled labor in European and Asian hubs, raising outsourced production costs by an estimated 8–12% in 2024 versus 2021 benchmarks.

This scarcity forces suppliers to hike contract prices to preserve margins, increasing Alimak Group’s regional project COGS and pressuring gross margins if Alimak cannot pass costs to customers.

- Skilled-labor shortfall drives 8–12% cost rise (2021–24)

- Higher supplier contract prices raise Alimak COGS

- Margin pressure unless Alimak raises prices or onshores work

Supplier power fuels margin squeeze: commodities, modules & recert costs bite

Suppliers hold moderate-to-high power: concentrated parts/electronics markets (top-10 share ~49% in 2024), commodity swings (steel +18%, aluminum +14% 2021–23) and energy-driven input inflation (EU gas +60% vs 2021 by late 2025) let vendors pass costs; specialized modules add 10–25% premiums and recertification costs €200k–€1.2M (6–18 months). Alimak’s $420m FY2024 scale and centralized buying mitigate but don’t eliminate margin squeeze.

| Metric | Value |

|---|---|

| Top-10 supplier share (2024) | ~49% |

| Steel price change (2021–23) | +18% |

| Aluminum price change (2021–23) | +14% |

| EU industrial gas vs 2021 (late 2025) | +60% |

| IoT component premium | +10–25% |

| Recertification cost per line | €200k–€1.2M |

| Alimak FY2024 revenue | $420m |

What is included in the product

Tailored Porter's Five Forces analysis for Alimak Group, uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes, and emerging disruptive threats to assess pricing power and strategic vulnerabilities.

Clear, one-sheet Porter's Five Forces for Alimak Group—visualize supplier, buyer, entrant, substitute, and rivalry pressures at a glance to streamline strategic decisions and risk mitigation.

Customers Bargaining Power

Consolidation of Rental Companies

A significant share of Alimak Group’s 2024 rental-related sales—about 28% of total revenue (SEK 1.9bn of SEK 6.8bn)—comes from a handful of global rental firms, giving buyers strong leverage.

These high-volume customers press for price cuts up to 10–15%, longer payment terms averaging 60–90 days, and multi-year service contracts that compress margins.

Industry consolidation raised the top-5 global rental firms’ market share to roughly 45% by end-2025, concentrating bargaining power and increasing Alimak’s dependency on a few dominant buyers.

Project-Based Procurement Cycles

Large infrastructure procurements use competitive bids where price often wins; 2024 World Bank data shows 60% of contracts award to lowest bidder, raising buyer leverage against Alimak.

Construction clients pit manufacturers to cut unit price for vertical access systems, squeezing margins and shortening sales cycles.

Alimak counters by stressing total cost of ownership—25% lower lifecycle cost in a 2023 independent study—and a safety record with 0.4 incidents per 1,000 units, to defend premium pricing.

Low Switching Costs in Standard Segments

In standard mast climbing platforms and construction hoists, switching costs are low, so buyers can easily move to regional alternatives; this gives customers negotiation leverage against Alimak despite its premium reliability.

Industry reports show basic hoist segments grew 3.2% in 2024 while Alimak’s premium segment price premiums averaged ~18%, making cost and availability decisive for short projects.

Procurement teams prioritize lead time and upfront price — projects under 6 months often choose the cheapest available unit over brand prestige.

Information Symmetry and Transparency

Modern procurement teams access pricing databases and trade platforms showing ±10–15% price spreads for vertical-transport equipment; that transparency lets buyers use real-time benchmarks to push margins down and demand service-level guarantees.

Alimak must boost digital services—predictive maintenance, uptime SLAs, remote diagnostics—to command a 5–8% premium versus peers and fend off commoditization as buyers compare global suppliers.

- Buyers see 10–15% price spreads

- Real-time benchmarks enable tougher negotiations

- Digital services can justify 5–8% price premium

- Continuous innovation reduces churn

Economic Sensitivity of Industrial Buyers

Customers in oil, gas and mining tie capex to commodity cycles; Brent fell from $86 in Jan 2024 to ~$75 avg in 2025, squeezing budgets and raising buyer leverage.

In downturns buyers defer projects or demand double-digit discounts; Alimak’s 2024 revenue mix—~30% mining, ~25% oil & gas—partially cushions but cyclicality still boosts buyer power.

- Commodity-linked capex

- Deferral/discount pressure

- Diverse end-markets mitigate

Rental giants boost buyer leverage; Alimak touts 25% lifecycle edge, 5–8% premium

Buyers hold strong leverage: top rental firms account for ~28% of 2024 revenue (SEK 1.9bn/SEK 6.8bn) and top-5 rental share rose to ~45% by end-2025, driving 10–15% price concessions, 60–90 day terms, and multi-year service demands; procurement awards 60% of infrastructure contracts to lowest bidder (World Bank 2024). Alimak defends a ~25% lower lifecycle cost and 0.4 incidents/1,000 units to sustain a 5–8% premium.

| Metric | Value |

|---|---|

| Rental revenue share 2024 | 28% (SEK 1.9bn) |

| Top-5 rental market share 2025 | ~45% |

| Lowest-bid awards (World Bank 2024) | 60% |

| Price concessions | 10–15% |

| Lifecycle cost advantage | 25% |

| Safety incidents | 0.4/1,000 units |

Preview Before You Purchase

Alimak Group Porter's Five Forces Analysis

This preview shows the exact Alimak Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted, comprehensive, and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Suppliers Bargaining Power

Raw Material Price Volatility

Alimak depends on steel, aluminum and electronic components, so global commodity swings — steel up ~18% and aluminum up ~14% in 2021–2023 supply shocks — raise input-cost risk.

Multiple vendors lower single-supplier exposure, but the need for high-grade, certified materials keeps the pool of qualified suppliers small.

By late 2025, energy-driven inflation (EU industrial gas prices +60% vs 2021) has let suppliers continue passing costs to OEMs, squeezing margins.

Specialized Component Dependency

Integration of IoT sensors and automated controls forces Alimak to buy specialized electronic modules from a small set of global semiconductor suppliers, who in 2024 captured ~65% of the industrial IoT components market and can demand premiums of 10–25% on non-commodity parts.

Switching Costs for Technical Parts

Switching proprietary safety components and patented drive systems imposes high costs and months-long certification: recertifying a primary supplier can take 6–18 months and cost €200k–€1.2M per product line based on industry averages for vertical access equipment compliance.

Supplier Consolidation Trends

The global industrial supply chain saw M&A activity concentrate suppliers: between 2018–2024 the top 10 global elevator/machinery parts suppliers’ combined market share rose from ~36% to ~49%, tightening supplier leverage.

Large consolidated suppliers now push longer lead times (+15–30 days) and higher minimum order quantities (up to 40% increase), raising procurement costs for mid-sized OEMs.

Alimak offsets some pressure by centralizing purchasing across 50+ country operations and $420m FY2024 revenue scale, but mega-conglomerates’ pricing power still compresses margins.

- Top-10 supplier share: ~49% (2024)

- Lead-time increase: +15–30 days

- MOQ rise: up to +40%

- Alimak FY2024 revenue: $420m

- Global purchasing across 50+ countries

Labor Market Constraints

Suppliers of specialized engineering services and fabricated sub-assemblies face chronic shortages of skilled labor in European and Asian hubs, raising outsourced production costs by an estimated 8–12% in 2024 versus 2021 benchmarks.

This scarcity forces suppliers to hike contract prices to preserve margins, increasing Alimak Group’s regional project COGS and pressuring gross margins if Alimak cannot pass costs to customers.

- Skilled-labor shortfall drives 8–12% cost rise (2021–24)

- Higher supplier contract prices raise Alimak COGS

- Margin pressure unless Alimak raises prices or onshores work

Supplier power fuels margin squeeze: commodities, modules & recert costs bite

Suppliers hold moderate-to-high power: concentrated parts/electronics markets (top-10 share ~49% in 2024), commodity swings (steel +18%, aluminum +14% 2021–23) and energy-driven input inflation (EU gas +60% vs 2021 by late 2025) let vendors pass costs; specialized modules add 10–25% premiums and recertification costs €200k–€1.2M (6–18 months). Alimak’s $420m FY2024 scale and centralized buying mitigate but don’t eliminate margin squeeze.

| Metric | Value |

|---|---|

| Top-10 supplier share (2024) | ~49% |

| Steel price change (2021–23) | +18% |

| Aluminum price change (2021–23) | +14% |

| EU industrial gas vs 2021 (late 2025) | +60% |

| IoT component premium | +10–25% |

| Recertification cost per line | €200k–€1.2M |

| Alimak FY2024 revenue | $420m |

What is included in the product

Tailored Porter's Five Forces analysis for Alimak Group, uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes, and emerging disruptive threats to assess pricing power and strategic vulnerabilities.

Clear, one-sheet Porter's Five Forces for Alimak Group—visualize supplier, buyer, entrant, substitute, and rivalry pressures at a glance to streamline strategic decisions and risk mitigation.

Customers Bargaining Power

Consolidation of Rental Companies

A significant share of Alimak Group’s 2024 rental-related sales—about 28% of total revenue (SEK 1.9bn of SEK 6.8bn)—comes from a handful of global rental firms, giving buyers strong leverage.

These high-volume customers press for price cuts up to 10–15%, longer payment terms averaging 60–90 days, and multi-year service contracts that compress margins.

Industry consolidation raised the top-5 global rental firms’ market share to roughly 45% by end-2025, concentrating bargaining power and increasing Alimak’s dependency on a few dominant buyers.

Project-Based Procurement Cycles

Large infrastructure procurements use competitive bids where price often wins; 2024 World Bank data shows 60% of contracts award to lowest bidder, raising buyer leverage against Alimak.

Construction clients pit manufacturers to cut unit price for vertical access systems, squeezing margins and shortening sales cycles.

Alimak counters by stressing total cost of ownership—25% lower lifecycle cost in a 2023 independent study—and a safety record with 0.4 incidents per 1,000 units, to defend premium pricing.

Low Switching Costs in Standard Segments

In standard mast climbing platforms and construction hoists, switching costs are low, so buyers can easily move to regional alternatives; this gives customers negotiation leverage against Alimak despite its premium reliability.

Industry reports show basic hoist segments grew 3.2% in 2024 while Alimak’s premium segment price premiums averaged ~18%, making cost and availability decisive for short projects.

Procurement teams prioritize lead time and upfront price — projects under 6 months often choose the cheapest available unit over brand prestige.

Information Symmetry and Transparency

Modern procurement teams access pricing databases and trade platforms showing ±10–15% price spreads for vertical-transport equipment; that transparency lets buyers use real-time benchmarks to push margins down and demand service-level guarantees.

Alimak must boost digital services—predictive maintenance, uptime SLAs, remote diagnostics—to command a 5–8% premium versus peers and fend off commoditization as buyers compare global suppliers.

- Buyers see 10–15% price spreads

- Real-time benchmarks enable tougher negotiations

- Digital services can justify 5–8% price premium

- Continuous innovation reduces churn

Economic Sensitivity of Industrial Buyers

Customers in oil, gas and mining tie capex to commodity cycles; Brent fell from $86 in Jan 2024 to ~$75 avg in 2025, squeezing budgets and raising buyer leverage.

In downturns buyers defer projects or demand double-digit discounts; Alimak’s 2024 revenue mix—~30% mining, ~25% oil & gas—partially cushions but cyclicality still boosts buyer power.

- Commodity-linked capex

- Deferral/discount pressure

- Diverse end-markets mitigate

Rental giants boost buyer leverage; Alimak touts 25% lifecycle edge, 5–8% premium

Buyers hold strong leverage: top rental firms account for ~28% of 2024 revenue (SEK 1.9bn/SEK 6.8bn) and top-5 rental share rose to ~45% by end-2025, driving 10–15% price concessions, 60–90 day terms, and multi-year service demands; procurement awards 60% of infrastructure contracts to lowest bidder (World Bank 2024). Alimak defends a ~25% lower lifecycle cost and 0.4 incidents/1,000 units to sustain a 5–8% premium.

| Metric | Value |

|---|---|

| Rental revenue share 2024 | 28% (SEK 1.9bn) |

| Top-5 rental market share 2025 | ~45% |

| Lowest-bid awards (World Bank 2024) | 60% |

| Price concessions | 10–15% |

| Lifecycle cost advantage | 25% |

| Safety incidents | 0.4/1,000 units |

Preview Before You Purchase

Alimak Group Porter's Five Forces Analysis

This preview shows the exact Alimak Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted, comprehensive, and ready for use.