Alkami Boston Consulting Group Matrix

See the Bigger Picture

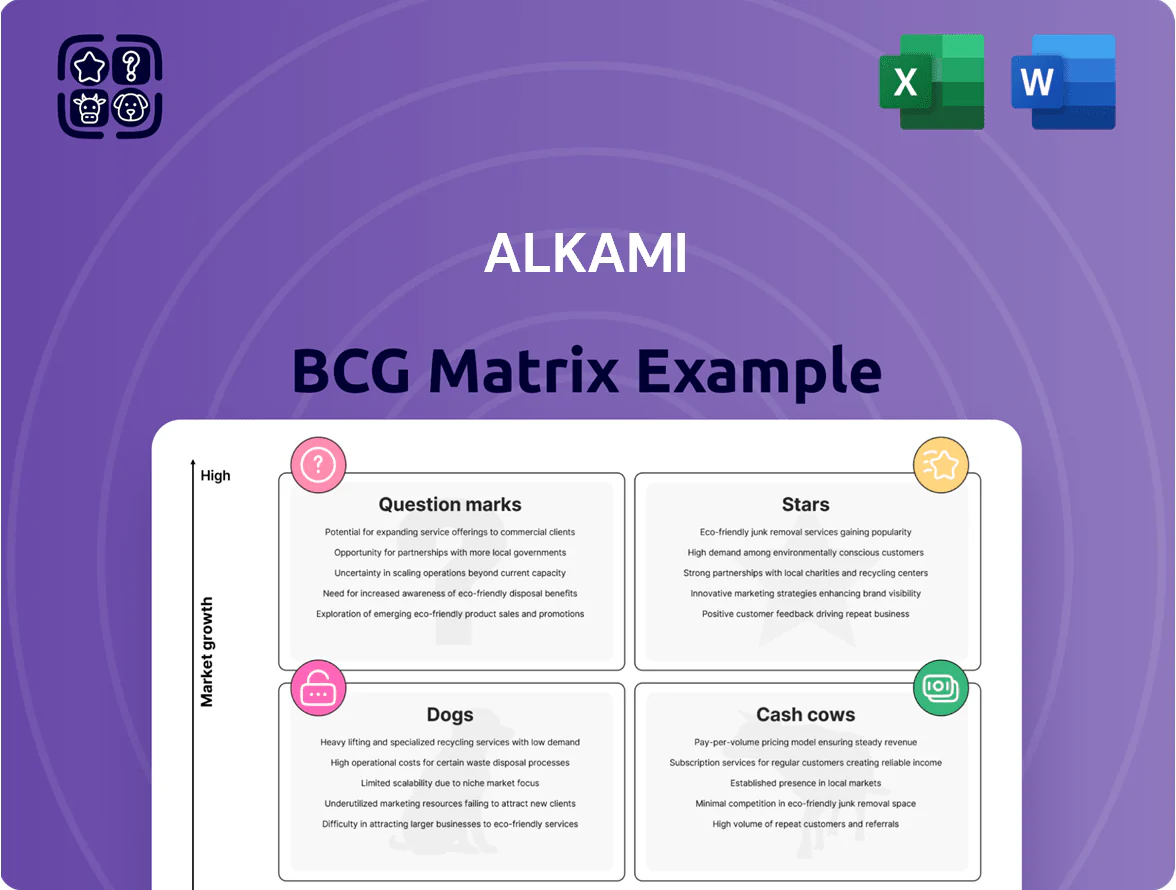

Alkami’s BCG Matrix snapshot highlights how its digital banking products map across market growth and share—revealing potential Stars in payments tech, Cash Cows in enterprise SaaS, and areas that may need retooling. This preview teases quadrant placement and strategic implications, but the full BCG Matrix delivers a complete, data-driven quadrant breakdown, actionable recommendations, and priority moves to optimize portfolio performance. Purchase the full report for Word and Excel deliverables to present, plan, and act with confidence.

Stars

MANTL Onboarding and Account Opening

Following Alkami’s acquisition of MANTL in January 2025, MANTL has become a core growth engine by removing friction in digital account opening, reducing time-to-open by ~60% and lifting conversion rates by 25% at pilot banks.

MANTL leads a market growing at ~18% CAGR (2024–29) as banks prioritize front-door UX to capture deposits; Alkami reports MANTL drove a 19% ARPU lift and added $28M incremental revenue in FY2025.

MANTL sits in the BCG matrix as a high-market-share star: strong growth, top share, but requires continued investment—Alkami committed $40M capex in 2025 to integrate APIs, KYC, and product bundles.

Retail Digital Banking Platform

Alkami’s core retail digital banking platform is a Star: J.D. Power-certified for outstanding mobile experience through 2025 and serving nearly 21 million registered users by Q4 2025, anchoring a large share of community and regional banks amid mandatory digital transformation.

It produced substantial revenue—Alkami reported total platform revenue of $231 million in FY 2024 with retail client growth contributing a majority—and the sector’s high CAGR (~18% global digital banking through 2025) forces continuous R&D spend.

Ongoing investment in UX, APIs, and AI-driven personalization is required to defend share versus megabanks and fast-moving fintechs, keeping churn low and deal win rates high into 2026.

Data and Marketing Solutions (Segmint)

The data-driven marketing arm of Alkami, Segmint, is a Star in the BCG matrix as banks adopt Anticipatory Banking to boost cross-sell and loyalty; its transaction-driven personalization is driving Alkami’s 113% net dollar retention as of Q4 2025.

Business and Commercial Banking Solutions

Alkami has moved strongly into commercial banking, with 50% of 2025 new client wins coming from banks versus credit unions, signaling a clear shift in go-to-market traction.

The platform’s treasury and cash-management tools drive high growth—regional banks report average deal sizes 35% larger than retail-only contracts, helping Alkami win lucrative commercial relationships.

Demand for sophisticated, user-friendly business banking is expanding at ~12% CAGR industry-wide; Alkami is investing heavily to poach share from legacy providers and scale commercial revenue.

- 50% of 2025 new wins from banks

- Deal sizes ~35% larger on commercial deals

- Business banking market ~12% CAGR

- Aggressive investment to capture legacy share

Cloud-Native SaaS Infrastructure

Alkami’s cloud-native SaaS infrastructure is a clear star: its cloud-first delivery gives scalability and agility that on-prem rivals lack and drove a record 13 new client launches in one 2025 quarter, showing strong market demand for modern deployments.

The platform underpins roughly 30% revenue growth in 2025 but requires significant capital and ops spend—public filings show elevated cloud and R&D expenses representing a growing share of operating costs.

- 13 new client launches (one 2025 quarter)

- ~30% revenue growth (2025)

- High capex and ops spend on cloud/R&D

Alkami 2025: MANTL & Retail Drive High-Growth SaaS; $28M Lift, 21M Users, Heavy CapEx

Alkami’s Stars (2025): MANTL and core retail platform lead high-growth markets—MANTL cut time-to-open ~60%, +25% conversion, $28M incremental FY2025; retail platform: 21M users, $231M revenue FY2024; Segmint drove 113% NDR Q4 2025; cloud SaaS: ~30% revenue growth 2025, 13 new launches/Q. Continued heavy capex ($40M+ 2025) needed to defend share.

| Metric | Value (2025) |

|---|---|

| MANTL time-to-open | -60% |

| MANTL conv. lift | +25% |

| MANTL incremental rev | $28M |

| Retail users | 21M |

| Platform rev (FY2024) | $231M |

| Segmint NDR | 113% |

| Cloud revenue growth | ~30% |

| New launches (one quarter) | 13 |

| Alkami 2025 capex | $40M+ |

What is included in the product

Comprehensive BCG Matrix review of Alkami’s product portfolio with quadrant strategies, risks, and investment recommendations.

One-page Alkami BCG Matrix mapping products by growth and share to speed strategic decisions for executives

Cash Cows

SaaS Subscription Services

As of late 2025, SaaS subscriptions make up about 96% of Alkami Federal (Alkami Technology, Inc.) total revenue, delivering stable, predictable cash flow from long-term contracts and high switching costs.

Gross margins expanded toward 65% by year-end 2025, letting Alkami milk recurring fees to service debt and fund R&D—the SaaS segment is the primary capital source for growth initiatives.

Core ACH Alert and Security Services

ACH Alert, part of Alkami’s security suite, delivers fraud prevention and payment protection with ~85% adoption across Alkami’s installed base as of Q4 2025, making it a mature, low-growth cash cow.

These services are table stakes for compliance, so marketing spend is ~30% lower than for Alkami’s AI tools, yet they sustain ~40% gross margins and steady ARR with minimal capex.

Legacy Credit Union Digital Banking

Alkami’s legacy digital banking for credit unions, its original stronghold, now yields steady cash flow—credit union clients accounted for about 52% of Alkami’s recurring revenue in 2024, reflecting high market penetration and low churn.

Growth in the credit union segment slowed to mid-single digits in 2024 versus double-digit growth in banks, but deep loyalty produces sticky ARR and high customer lifetime value.

That reliable cash cow funds continued product investment and lets Alkami shift sales and R&D toward faster-growing commercial bank opportunities.

Standard Bill Pay and Money Transfer Modules

Standard bill pay and P2P transfer modules are mature, high-adoption products across Alkami’s 280+ client banks and credit unions, reaching an estimated 85% platform penetration and contributing steady per-user fees of roughly $0.50–$1.20 monthly as of 2025.

These modules hold dominant share within Alkami’s ecosystem, run efficiently via established vendor integrations, require minimal promotion, and delivered predictable revenue accounting for an estimated 18–22% of platform transactional revenue in 2024.

- 85% estimated penetration across 280+ clients

- $0.50–$1.20 monthly per-user fees (2025)

- 18–22% of transactional revenue (2024)

- Low maintenance; high operational efficiency

Implementation and Professional Services

Implementation and Professional Services, while smaller than subscription revenue, deliver steady cash as Alkami works through a $1.6 billion backlog of performance obligations (FY2025). These upfront fees, driven by platform demand, offset onboarding costs and smooth cash flow.

Standardized implementation processes have raised efficiency, trimming time-to-live and boosting adjusted EBITDA margin—implementation margins improved by ~150 basis points from 2023 to 2025.

- Backlog: $1.6B (FY2025)

- Provides upfront cash to offset onboarding

- Supports steady cash flow vs. subscription

- Efficiency gains ≈ +150 bps to adjusted EBITDA (2023–2025)

Alkami: High-margin SaaS & $1.6B backlog fuel bank-focused growth

Alkami’s cash cows—SaaS subscriptions, ACH Alert, legacy credit-union platform, bill-pay/P2P modules, and implementation services—generate predictable ARR, ~65% gross margins on SaaS, ~40% on compliance tools, ~85% product penetration, $0.50–$1.20/user monthly, and a $1.6B backlog (FY2025), funding R&D and bank-focused growth.

| Metric | Value (2025) |

|---|---|

| SaaS revenue share | ~96% |

| SaaS gross margin | ~65% |

| Compliance gross margin | ~40% |

| Product penetration | ~85% |

| Per-user fee | $0.50–$1.20/mo |

| Backlog | $1.6B |

Preview = Final Product

Alkami BCG Matrix

The BCG Matrix preview displayed here is the exact, final document you’ll receive after purchase—no watermarks or demo content, just a fully formatted, strategy-ready report designed for clear portfolio analysis and decision-making.

This file mirrors the downloadable version sent to your inbox upon payment, crafted with market-backed insights and professional layout so you can use it immediately for presentations, planning, or client work.

What you see is fully editable and printable: purchase unlocks the same BCG Matrix file for immediate distribution, customization, and integration into your strategic toolkit.

Prepared by strategy specialists, the report is formatted for clarity and action—no surprises, no revisions required, simply a polished deliverable ready to support your competitive and growth decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Alkami’s BCG Matrix snapshot highlights how its digital banking products map across market growth and share—revealing potential Stars in payments tech, Cash Cows in enterprise SaaS, and areas that may need retooling. This preview teases quadrant placement and strategic implications, but the full BCG Matrix delivers a complete, data-driven quadrant breakdown, actionable recommendations, and priority moves to optimize portfolio performance. Purchase the full report for Word and Excel deliverables to present, plan, and act with confidence.

Stars

MANTL Onboarding and Account Opening

Following Alkami’s acquisition of MANTL in January 2025, MANTL has become a core growth engine by removing friction in digital account opening, reducing time-to-open by ~60% and lifting conversion rates by 25% at pilot banks.

MANTL leads a market growing at ~18% CAGR (2024–29) as banks prioritize front-door UX to capture deposits; Alkami reports MANTL drove a 19% ARPU lift and added $28M incremental revenue in FY2025.

MANTL sits in the BCG matrix as a high-market-share star: strong growth, top share, but requires continued investment—Alkami committed $40M capex in 2025 to integrate APIs, KYC, and product bundles.

Retail Digital Banking Platform

Alkami’s core retail digital banking platform is a Star: J.D. Power-certified for outstanding mobile experience through 2025 and serving nearly 21 million registered users by Q4 2025, anchoring a large share of community and regional banks amid mandatory digital transformation.

It produced substantial revenue—Alkami reported total platform revenue of $231 million in FY 2024 with retail client growth contributing a majority—and the sector’s high CAGR (~18% global digital banking through 2025) forces continuous R&D spend.

Ongoing investment in UX, APIs, and AI-driven personalization is required to defend share versus megabanks and fast-moving fintechs, keeping churn low and deal win rates high into 2026.

Data and Marketing Solutions (Segmint)

The data-driven marketing arm of Alkami, Segmint, is a Star in the BCG matrix as banks adopt Anticipatory Banking to boost cross-sell and loyalty; its transaction-driven personalization is driving Alkami’s 113% net dollar retention as of Q4 2025.

Business and Commercial Banking Solutions

Alkami has moved strongly into commercial banking, with 50% of 2025 new client wins coming from banks versus credit unions, signaling a clear shift in go-to-market traction.

The platform’s treasury and cash-management tools drive high growth—regional banks report average deal sizes 35% larger than retail-only contracts, helping Alkami win lucrative commercial relationships.

Demand for sophisticated, user-friendly business banking is expanding at ~12% CAGR industry-wide; Alkami is investing heavily to poach share from legacy providers and scale commercial revenue.

- 50% of 2025 new wins from banks

- Deal sizes ~35% larger on commercial deals

- Business banking market ~12% CAGR

- Aggressive investment to capture legacy share

Cloud-Native SaaS Infrastructure

Alkami’s cloud-native SaaS infrastructure is a clear star: its cloud-first delivery gives scalability and agility that on-prem rivals lack and drove a record 13 new client launches in one 2025 quarter, showing strong market demand for modern deployments.

The platform underpins roughly 30% revenue growth in 2025 but requires significant capital and ops spend—public filings show elevated cloud and R&D expenses representing a growing share of operating costs.

- 13 new client launches (one 2025 quarter)

- ~30% revenue growth (2025)

- High capex and ops spend on cloud/R&D

Alkami 2025: MANTL & Retail Drive High-Growth SaaS; $28M Lift, 21M Users, Heavy CapEx

Alkami’s Stars (2025): MANTL and core retail platform lead high-growth markets—MANTL cut time-to-open ~60%, +25% conversion, $28M incremental FY2025; retail platform: 21M users, $231M revenue FY2024; Segmint drove 113% NDR Q4 2025; cloud SaaS: ~30% revenue growth 2025, 13 new launches/Q. Continued heavy capex ($40M+ 2025) needed to defend share.

| Metric | Value (2025) |

|---|---|

| MANTL time-to-open | -60% |

| MANTL conv. lift | +25% |

| MANTL incremental rev | $28M |

| Retail users | 21M |

| Platform rev (FY2024) | $231M |

| Segmint NDR | 113% |

| Cloud revenue growth | ~30% |

| New launches (one quarter) | 13 |

| Alkami 2025 capex | $40M+ |

What is included in the product

Comprehensive BCG Matrix review of Alkami’s product portfolio with quadrant strategies, risks, and investment recommendations.

One-page Alkami BCG Matrix mapping products by growth and share to speed strategic decisions for executives

Cash Cows

SaaS Subscription Services

As of late 2025, SaaS subscriptions make up about 96% of Alkami Federal (Alkami Technology, Inc.) total revenue, delivering stable, predictable cash flow from long-term contracts and high switching costs.

Gross margins expanded toward 65% by year-end 2025, letting Alkami milk recurring fees to service debt and fund R&D—the SaaS segment is the primary capital source for growth initiatives.

Core ACH Alert and Security Services

ACH Alert, part of Alkami’s security suite, delivers fraud prevention and payment protection with ~85% adoption across Alkami’s installed base as of Q4 2025, making it a mature, low-growth cash cow.

These services are table stakes for compliance, so marketing spend is ~30% lower than for Alkami’s AI tools, yet they sustain ~40% gross margins and steady ARR with minimal capex.

Legacy Credit Union Digital Banking

Alkami’s legacy digital banking for credit unions, its original stronghold, now yields steady cash flow—credit union clients accounted for about 52% of Alkami’s recurring revenue in 2024, reflecting high market penetration and low churn.

Growth in the credit union segment slowed to mid-single digits in 2024 versus double-digit growth in banks, but deep loyalty produces sticky ARR and high customer lifetime value.

That reliable cash cow funds continued product investment and lets Alkami shift sales and R&D toward faster-growing commercial bank opportunities.

Standard Bill Pay and Money Transfer Modules

Standard bill pay and P2P transfer modules are mature, high-adoption products across Alkami’s 280+ client banks and credit unions, reaching an estimated 85% platform penetration and contributing steady per-user fees of roughly $0.50–$1.20 monthly as of 2025.

These modules hold dominant share within Alkami’s ecosystem, run efficiently via established vendor integrations, require minimal promotion, and delivered predictable revenue accounting for an estimated 18–22% of platform transactional revenue in 2024.

- 85% estimated penetration across 280+ clients

- $0.50–$1.20 monthly per-user fees (2025)

- 18–22% of transactional revenue (2024)

- Low maintenance; high operational efficiency

Implementation and Professional Services

Implementation and Professional Services, while smaller than subscription revenue, deliver steady cash as Alkami works through a $1.6 billion backlog of performance obligations (FY2025). These upfront fees, driven by platform demand, offset onboarding costs and smooth cash flow.

Standardized implementation processes have raised efficiency, trimming time-to-live and boosting adjusted EBITDA margin—implementation margins improved by ~150 basis points from 2023 to 2025.

- Backlog: $1.6B (FY2025)

- Provides upfront cash to offset onboarding

- Supports steady cash flow vs. subscription

- Efficiency gains ≈ +150 bps to adjusted EBITDA (2023–2025)

Alkami: High-margin SaaS & $1.6B backlog fuel bank-focused growth

Alkami’s cash cows—SaaS subscriptions, ACH Alert, legacy credit-union platform, bill-pay/P2P modules, and implementation services—generate predictable ARR, ~65% gross margins on SaaS, ~40% on compliance tools, ~85% product penetration, $0.50–$1.20/user monthly, and a $1.6B backlog (FY2025), funding R&D and bank-focused growth.

| Metric | Value (2025) |

|---|---|

| SaaS revenue share | ~96% |

| SaaS gross margin | ~65% |

| Compliance gross margin | ~40% |

| Product penetration | ~85% |

| Per-user fee | $0.50–$1.20/mo |

| Backlog | $1.6B |

Preview = Final Product

Alkami BCG Matrix

The BCG Matrix preview displayed here is the exact, final document you’ll receive after purchase—no watermarks or demo content, just a fully formatted, strategy-ready report designed for clear portfolio analysis and decision-making.

This file mirrors the downloadable version sent to your inbox upon payment, crafted with market-backed insights and professional layout so you can use it immediately for presentations, planning, or client work.

What you see is fully editable and printable: purchase unlocks the same BCG Matrix file for immediate distribution, customization, and integration into your strategic toolkit.

Prepared by strategy specialists, the report is formatted for clarity and action—no surprises, no revisions required, simply a polished deliverable ready to support your competitive and growth decisions.