Alkermes Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

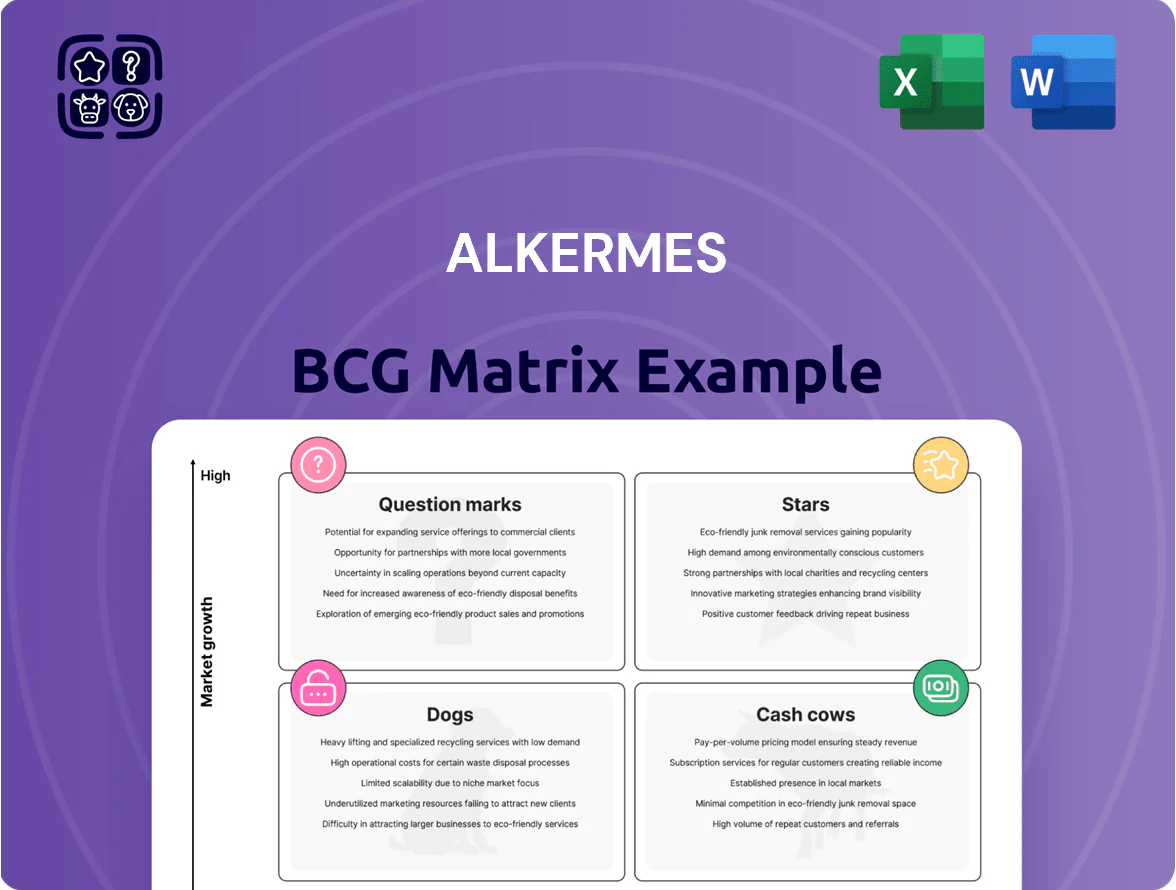

Alkermes' BCG Matrix preview highlights how its portfolio balances high-growth biologics with mature CNS franchises, revealing where R&D and commercialization fuel future Stars versus which assets act as Cash Cows or Dogs. This snapshot teases strategic tensions—resource allocation, divestiture opportunities, and pipeline prioritization—that investors and executives must resolve. The complete BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and editable Word/Excel files to guide confident capital and portfolio decisions; purchase the full report for instant, actionable clarity.

Stars

LYBALVI Growth Engine

LYBALVI is Alkermes' Star: Q3 2025 revenue rose 32% year-over-year to $98.2 million, driven by strong share in the oral atypical antipsychotic market for patients prioritizing lower weight gain.

The product generates meaningful cash but Alkermes keeps investing heavily in promotion and sales-force expansion to defend growth versus entrenched competitors like Otsuka’s Abilify and others.

Alixorexton Breakthrough Potential

Alixorexton (formerly ALKS 2680) is a Star: FDA Breakthrough Therapy Designation for Narcolepsy Type 1 in Jan 2026 after positive Phase 2 data in Nov 2025; Phase 3 dosing began Q1 2026 with Alkermes guiding $150–200m incremental R&D spend through 2027.

As a potential first-in-class oral orexin 2 receptor agonist, alixorexton targets a >$2.5bn addressable market for central disorders of hypersomnolence by 2030 and could drive >30% of Alkermes product revenue in upside scenarios.

LUMRYZ Strategic Acquisition

The late 2025 Alkermes agreement to acquire Avadel Pharmaceuticals makes LUMRYZ a Star in the 2026 BCG matrix, joining Alkermes with a high-growth, high-share product.

As the only once-at-bedtime oxybate for narcolepsy, LUMRYZ addresses unmet need and posted projected 2025 revenue > $265 million, supporting strong market adoption.

It gives Alkermes immediate leadership in sleep medicine but will need sustained commercial investment—salesforce expansion, DTC spend, and manufacturing scale—to sustain growth.

Psychiatry Franchise Expansion

Alkermes treated its psychiatry franchise as a Star after a 2025 field expansion to support rapid uptake of proprietary brands, driving focus and resources to sustain growth.

By Q3 2025 proprietary product net sales rose 16% year-over-year, outpacing broader antipsychotic market growth and justifying prioritized capital allocation to capture share from generics and legacy branded therapies.

- 2025 field expansion made franchise a Star

- 16% YoY proprietary net sales growth by Q3 2025

- Capital redirected to high-growth psychiatry segment

- Strategy aims to displace generic/legacy antipsychotics

Alcohol Dependence Leadership

VIVITROL’s alcohol dependence sales rebounded; Alkermes raised 2025 guidance to $460–$470 million on robust demand and higher uptake in long-acting injectables for addiction.

As a Star in Alkermes’ BCG matrix, VIVITROL holds a leading share of the long-acting injectable addiction market and looks set to transition toward Cash Cow as growth moderates but margins improve.

Alkermes drives double-digit growth in high-need regions by tailoring to local payer systems and specialty-clinic channels; U.S. outpatient program expansions and state Medicaid policies boosted prescriptions in 2024–2025.

- 2025 guidance: $460–$470M

- High share: long-acting injectable addiction market

- Transitioning: Star → Cash Cow as margins rise

- Growth drivers: localized payers, specialty clinics, Medicaid expansions

High‑growth drug stars: LYBALVI, VIVITROL, LUMRYZ, Alixorexton—strong 2025 outlook

Stars: LYBALVI, alixorexton, LUMRYZ, VIVITROL—high growth and share; LYBALVI Q3 2025 revenue $98.2M (+32% YoY), VIVITROL 2025 guidance $460–470M, LUMRYZ projected 2025 revenue >$265M, alixorexton target market >$2.5B by 2030 with $150–200M incremental R&D to 2027.

| Product | 2025 ($M) | Notes |

|---|---|---|

| LYBALVI | 98.2 | Q3 2025 +32% YoY |

| VIVITROL | 460–470 (guidance) | Long‑acting injectables |

| LUMRYZ | >265 (proj) | Once‑at‑bedtime oxybate |

| Alixorexton | — | BTD Jan 2026; $150–200 R&D to 2027 |

What is included in the product

Comprehensive BCG Matrix analysis of Alkermes’ portfolio with quadrant-specific strategies, risks, and investment recommendations.

One-page Alkermes BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

VIVITROL Core Franchise

VIVITROL remains Alkermes’ primary Cash Cow, generating $121.1 million in Q3 2025 and providing steady liquidity for R&D and operations.

Growth has stabilized at ~7% year-over-year, while high market share in opioid and alcohol dependence delivers consistent margins and predictable cash flow.

Proceeds from VIVITROL fund pipeline Question Marks—supporting trials and commercialization to convert them into future Stars.

ARISTADA Schizophrenia Treatment

ARISTADA, Alkermes’s long-acting injectable schizophrenia therapy, is a Cash Cow with 2025 net sales forecast at $360–$370 million and strong prescriber breadth, giving steady revenue and low incremental marketing spend.

Despite competition, its margin profile and recurring injections materially supported Alkermes’ GAAP net income, which was $82.8 million in Q3 2025, reinforcing free-cash generation for R&D and dividends.

VUMERITY Royalty Stream

The VUMERITY royalty and manufacturing stream, commercialized by Biogen, functions as a high-margin Cash Cow for Alkermes with minimal overhead. In Q3 2025 it delivered $35.6 million of pure cash flow to Alkermes' topline, requiring no direct sales spend. Alkermes redirects these funds to the alixorexton (orexin antagonist) clinical program and to service debt from the Avadel acquisition. This predictable revenue lowers funding dilution risk and funds R&D runway.

Legacy Long-Acting Royalties

Alkermes continues to milk royalties from partner-marketed products XEPLION and INVEGA TRINZA, which contributed $30.2 million in Q3 2025, fitting the Cash Cow quadrant of the BCG matrix.

These products sit in a mature market where Alkermes holds protected IP but no longer invests in active development, yielding steady, low-growth cash flows.

The royalties provide a predictable financial floor, helping maintain a strong cash balance of $1.14 billion at year-end and fund other initiatives.

- Q3 2025 royalties: $30.2M

- Year-end cash balance: $1.14B

- Mature market, protected IP, no active development

Proprietary Manufacturing Services

Alkermes’ proprietary manufacturing services for long-acting injectables act as a secondary Cash Cow, delivering steady service revenue—about $220M in 2024—from global partners and contract work.

After divesting non-core assets in 2023–24, the firm runs high-efficiency facilities focused on high-margin proprietary and partner neuro-medicines, pushing facility utilization to ~85% and gross margins above 35%.

This segment free cash flow funds R&D and the shift to a pure-play neuroscience company, having contributed roughly $90M of operating cash flow in 2024 toward strategic M&A and pipeline investment.

- 2024 service revenue ~$220M

- Facility utilization ~85%

- Gross margins >35%

- 2024 operating cash from segment ~$90M

Alkermes’ cash cows: VIVITROL, ARISTADA, VUMERITY, royalties & manufacturing fuel stability

VIVITROL, ARISTADA, VUMERITY royalties, partner royalties (XEPLION/INVEGA TRINZA), and manufacturing services are Alkermes’ Cash Cows, delivering predictable cash flow (VIVITROL $121.1M Q3 2025; ARISTADA $360–$370M 2025; VUMERITY $35.6M Q3 2025; partner royalties $30.2M Q3 2025; manufacturing ~$220M 2024) supporting R&D, debt service, and dividends.

| Asset | Key 2024/2025 |

|---|---|

| VIVITROL | $121.1M Q3 2025 |

| ARISTADA | $360–$370M 2025 |

| VUMERITY | $35.6M Q3 2025 |

| Partner royalties | $30.2M Q3 2025 |

| Manufacturing | $220M 2024, util ~85% |

What You See Is What You Get

Alkermes BCG Matrix

The Alkermes BCG Matrix you're previewing on this page is the exact, final document you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready-to-use strategic report crafted for clarity and decision-making.

This preview mirrors the downloadable file delivered to your inbox: comprehensive market-backed analysis, clean visuals, and editable elements so you can present or adapt it immediately without further revisions.

What you see is the real product—professionally designed by strategy experts to slot seamlessly into planning, investor decks, or portfolio reviews.

Upon purchase you’ll unlock the same complete file for instant downloading, printing, or sharing with stakeholders—no surprises, only actionable insight.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Alkermes' BCG Matrix preview highlights how its portfolio balances high-growth biologics with mature CNS franchises, revealing where R&D and commercialization fuel future Stars versus which assets act as Cash Cows or Dogs. This snapshot teases strategic tensions—resource allocation, divestiture opportunities, and pipeline prioritization—that investors and executives must resolve. The complete BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and editable Word/Excel files to guide confident capital and portfolio decisions; purchase the full report for instant, actionable clarity.

Stars

LYBALVI Growth Engine

LYBALVI is Alkermes' Star: Q3 2025 revenue rose 32% year-over-year to $98.2 million, driven by strong share in the oral atypical antipsychotic market for patients prioritizing lower weight gain.

The product generates meaningful cash but Alkermes keeps investing heavily in promotion and sales-force expansion to defend growth versus entrenched competitors like Otsuka’s Abilify and others.

Alixorexton Breakthrough Potential

Alixorexton (formerly ALKS 2680) is a Star: FDA Breakthrough Therapy Designation for Narcolepsy Type 1 in Jan 2026 after positive Phase 2 data in Nov 2025; Phase 3 dosing began Q1 2026 with Alkermes guiding $150–200m incremental R&D spend through 2027.

As a potential first-in-class oral orexin 2 receptor agonist, alixorexton targets a >$2.5bn addressable market for central disorders of hypersomnolence by 2030 and could drive >30% of Alkermes product revenue in upside scenarios.

LUMRYZ Strategic Acquisition

The late 2025 Alkermes agreement to acquire Avadel Pharmaceuticals makes LUMRYZ a Star in the 2026 BCG matrix, joining Alkermes with a high-growth, high-share product.

As the only once-at-bedtime oxybate for narcolepsy, LUMRYZ addresses unmet need and posted projected 2025 revenue > $265 million, supporting strong market adoption.

It gives Alkermes immediate leadership in sleep medicine but will need sustained commercial investment—salesforce expansion, DTC spend, and manufacturing scale—to sustain growth.

Psychiatry Franchise Expansion

Alkermes treated its psychiatry franchise as a Star after a 2025 field expansion to support rapid uptake of proprietary brands, driving focus and resources to sustain growth.

By Q3 2025 proprietary product net sales rose 16% year-over-year, outpacing broader antipsychotic market growth and justifying prioritized capital allocation to capture share from generics and legacy branded therapies.

- 2025 field expansion made franchise a Star

- 16% YoY proprietary net sales growth by Q3 2025

- Capital redirected to high-growth psychiatry segment

- Strategy aims to displace generic/legacy antipsychotics

Alcohol Dependence Leadership

VIVITROL’s alcohol dependence sales rebounded; Alkermes raised 2025 guidance to $460–$470 million on robust demand and higher uptake in long-acting injectables for addiction.

As a Star in Alkermes’ BCG matrix, VIVITROL holds a leading share of the long-acting injectable addiction market and looks set to transition toward Cash Cow as growth moderates but margins improve.

Alkermes drives double-digit growth in high-need regions by tailoring to local payer systems and specialty-clinic channels; U.S. outpatient program expansions and state Medicaid policies boosted prescriptions in 2024–2025.

- 2025 guidance: $460–$470M

- High share: long-acting injectable addiction market

- Transitioning: Star → Cash Cow as margins rise

- Growth drivers: localized payers, specialty clinics, Medicaid expansions

High‑growth drug stars: LYBALVI, VIVITROL, LUMRYZ, Alixorexton—strong 2025 outlook

Stars: LYBALVI, alixorexton, LUMRYZ, VIVITROL—high growth and share; LYBALVI Q3 2025 revenue $98.2M (+32% YoY), VIVITROL 2025 guidance $460–470M, LUMRYZ projected 2025 revenue >$265M, alixorexton target market >$2.5B by 2030 with $150–200M incremental R&D to 2027.

| Product | 2025 ($M) | Notes |

|---|---|---|

| LYBALVI | 98.2 | Q3 2025 +32% YoY |

| VIVITROL | 460–470 (guidance) | Long‑acting injectables |

| LUMRYZ | >265 (proj) | Once‑at‑bedtime oxybate |

| Alixorexton | — | BTD Jan 2026; $150–200 R&D to 2027 |

What is included in the product

Comprehensive BCG Matrix analysis of Alkermes’ portfolio with quadrant-specific strategies, risks, and investment recommendations.

One-page Alkermes BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

VIVITROL Core Franchise

VIVITROL remains Alkermes’ primary Cash Cow, generating $121.1 million in Q3 2025 and providing steady liquidity for R&D and operations.

Growth has stabilized at ~7% year-over-year, while high market share in opioid and alcohol dependence delivers consistent margins and predictable cash flow.

Proceeds from VIVITROL fund pipeline Question Marks—supporting trials and commercialization to convert them into future Stars.

ARISTADA Schizophrenia Treatment

ARISTADA, Alkermes’s long-acting injectable schizophrenia therapy, is a Cash Cow with 2025 net sales forecast at $360–$370 million and strong prescriber breadth, giving steady revenue and low incremental marketing spend.

Despite competition, its margin profile and recurring injections materially supported Alkermes’ GAAP net income, which was $82.8 million in Q3 2025, reinforcing free-cash generation for R&D and dividends.

VUMERITY Royalty Stream

The VUMERITY royalty and manufacturing stream, commercialized by Biogen, functions as a high-margin Cash Cow for Alkermes with minimal overhead. In Q3 2025 it delivered $35.6 million of pure cash flow to Alkermes' topline, requiring no direct sales spend. Alkermes redirects these funds to the alixorexton (orexin antagonist) clinical program and to service debt from the Avadel acquisition. This predictable revenue lowers funding dilution risk and funds R&D runway.

Legacy Long-Acting Royalties

Alkermes continues to milk royalties from partner-marketed products XEPLION and INVEGA TRINZA, which contributed $30.2 million in Q3 2025, fitting the Cash Cow quadrant of the BCG matrix.

These products sit in a mature market where Alkermes holds protected IP but no longer invests in active development, yielding steady, low-growth cash flows.

The royalties provide a predictable financial floor, helping maintain a strong cash balance of $1.14 billion at year-end and fund other initiatives.

- Q3 2025 royalties: $30.2M

- Year-end cash balance: $1.14B

- Mature market, protected IP, no active development

Proprietary Manufacturing Services

Alkermes’ proprietary manufacturing services for long-acting injectables act as a secondary Cash Cow, delivering steady service revenue—about $220M in 2024—from global partners and contract work.

After divesting non-core assets in 2023–24, the firm runs high-efficiency facilities focused on high-margin proprietary and partner neuro-medicines, pushing facility utilization to ~85% and gross margins above 35%.

This segment free cash flow funds R&D and the shift to a pure-play neuroscience company, having contributed roughly $90M of operating cash flow in 2024 toward strategic M&A and pipeline investment.

- 2024 service revenue ~$220M

- Facility utilization ~85%

- Gross margins >35%

- 2024 operating cash from segment ~$90M

Alkermes’ cash cows: VIVITROL, ARISTADA, VUMERITY, royalties & manufacturing fuel stability

VIVITROL, ARISTADA, VUMERITY royalties, partner royalties (XEPLION/INVEGA TRINZA), and manufacturing services are Alkermes’ Cash Cows, delivering predictable cash flow (VIVITROL $121.1M Q3 2025; ARISTADA $360–$370M 2025; VUMERITY $35.6M Q3 2025; partner royalties $30.2M Q3 2025; manufacturing ~$220M 2024) supporting R&D, debt service, and dividends.

| Asset | Key 2024/2025 |

|---|---|

| VIVITROL | $121.1M Q3 2025 |

| ARISTADA | $360–$370M 2025 |

| VUMERITY | $35.6M Q3 2025 |

| Partner royalties | $30.2M Q3 2025 |

| Manufacturing | $220M 2024, util ~85% |

What You See Is What You Get

Alkermes BCG Matrix

The Alkermes BCG Matrix you're previewing on this page is the exact, final document you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready-to-use strategic report crafted for clarity and decision-making.

This preview mirrors the downloadable file delivered to your inbox: comprehensive market-backed analysis, clean visuals, and editable elements so you can present or adapt it immediately without further revisions.

What you see is the real product—professionally designed by strategy experts to slot seamlessly into planning, investor decks, or portfolio reviews.

Upon purchase you’ll unlock the same complete file for instant downloading, printing, or sharing with stakeholders—no surprises, only actionable insight.