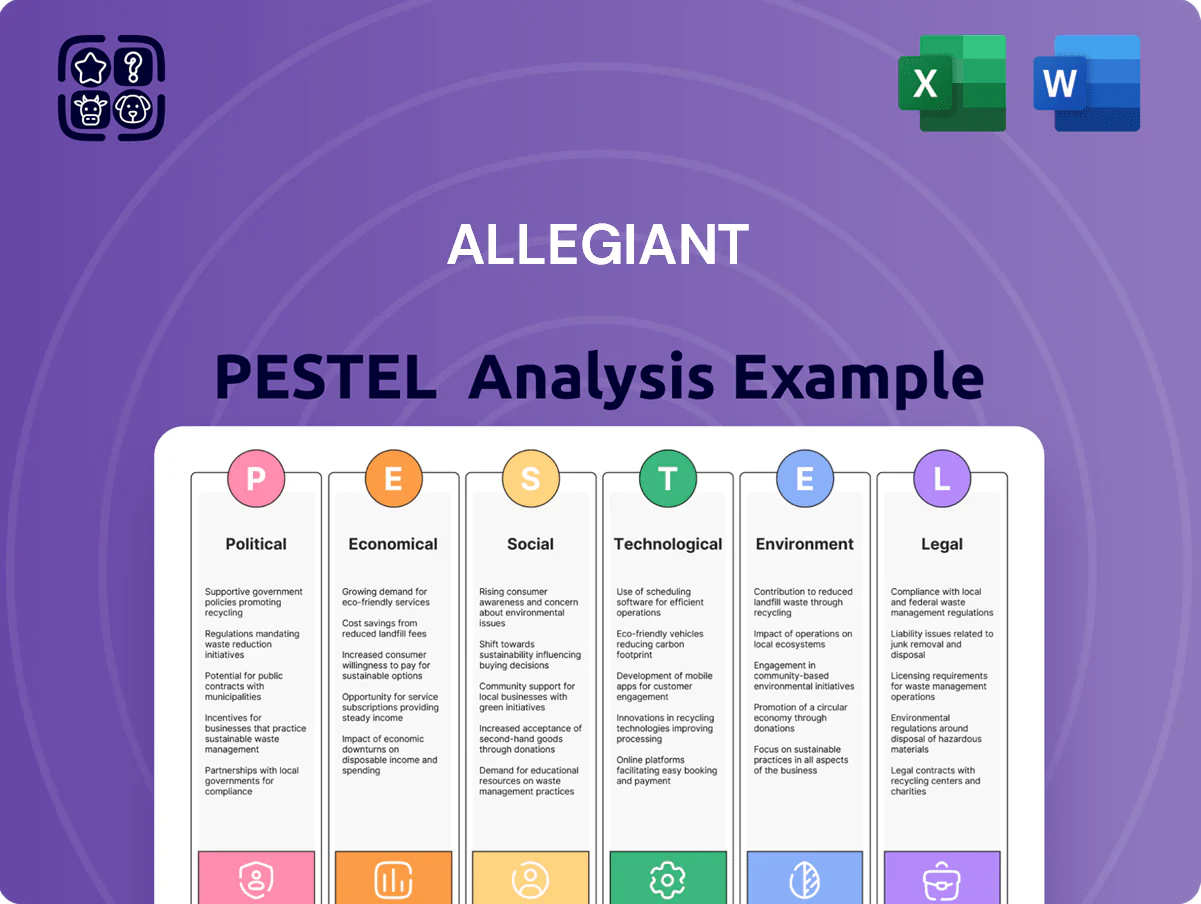

Allegiant PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis of Allegiant reveals how regulatory shifts, fuel price volatility, and evolving travel preferences are shaping growth and risk—insights tailored for investors and strategists seeking a competitive edge. Purchase the full report to access detailed drivers, quantified impacts, and actionable recommendations you can apply immediately.

Political factors

Federal Aviation Administration Reauthorization Implementation

The 2024 FAA Reauthorization Act, effective through late 2025, allocates $31.2 billion for airport improvements and expands FAA oversight, influencing Allegiant’s access to 420+ non-primary airports and ramp projects critical to its point-to-point model.

New mandates on pilot training and ATC modernization—$5.4 billion for NextGen upgrades—raise training and compliance costs; Allegiant reported $162 million in operating margin in 2024 and must balance these mandates to preserve low-cost operations.

Department of Transportation Consumer Protection Mandates

The U.S. Department of Transportation tightened passenger-rights and fee-transparency rules in 2025, mandating automatic refunds and clearer disclosure of ancillary fees for baggage and seating; DOT enforcement actions rose 28% in 2025 versus 2024, increasing regulatory risk for carriers. Allegiant, which generated roughly 28% of 2024 ancillary revenue from fees, must continually update booking UI, pricing disclosures, and marketing to avoid fines and potential consumer-remediation costs.

Regional Airport Subsidy and Grant Programs

Political support for the Essential Air Service and regional airport grants remains critical for Allegiant’s point-to-point model; in FY2024 the U.S. DOT disbursed about $200 million to EAS and small airport programs, directly shaping Allegiant’s access to 150+ secondary airports it serves.

Federal and state funding decisions influence route expansion into underserved markets—Allegiant added 18 new markets in 2024 where airports received state/local incentives averaging $1.2 million per new route.

Local political leadership changes can alter incentives for low-cost carriers: between 2023–2025 several municipalities revised or rescinded incentive packages, affecting Allegiant’s base decisions and expected ROI timelines.

Labor Relations and Federal Mediation

The post-2024 surge in airline union activity has made labor relations more complex for Allegiant, with pilots and flight attendants pushing for higher pay and job protections; by 2025 national airline union membership rose ~15% year-over-year, raising potential labor costs.

Federal mediation has been pivotal in recent negotiations—mediators shortened dispute durations by an average of 30% in 2023–25, affecting settlement timing and cash flow for carriers like Allegiant.

The administration’s pro-mediator stance can accelerate settlements but may increase wage outcomes; a 2024 industry sample showed negotiated labor expense rises of 4–7%, pressuring Allegiant’s unit cost structure and margins.

- Union membership +15% (2025 vs 2024)

- Mediation cut dispute duration ~30% (2023–25)

- Negotiated labor costs up 4–7% in 2024

Geopolitical Influence on Domestic Energy Policy

Global political instability raises U.S. federal energy policy responses that affect domestic jet fuel costs; in 2024 U.S. jet fuel averaged about $3.10/gal versus $2.70/gal in 2023, amplifying operational expense risk for Allegiant.

Decisions on the Strategic Petroleum Reserve releases and drilling permits—DOE SPR releases of ~180 million barrels since 2022 and O&G permitting increases in 2024—drive short-term fuel price volatility impacting Allegiant’s margins.

Allegiant’s sensitivity: fuel is ~25–30% of CASM-ex fuel expense variance, so politically induced price swings materially affect quarterly profitability and unit cost forecasts.

- 2024 jet fuel avg ~$3.10/gal; 2023 ~$2.70/gal

- SPR releases ~180M barrels since 2022

- Fuel-related CASM variance ~25–30%

Policy shifts, rising unions and fuel costs heighten Allegiant's compliance & labor risk

Political shifts—FAA funding ($31.2B through 2025), DOT rule-tightening (2025 fee/transparency mandates), EAS/state incentives (~$200M FY2024; ~$1.2M avg incentive per new route in 2024), rising unionization (+15% 2025 vs 2024) and fuel policy (2024 jet fuel ~$3.10/gal; SPR ~180M bbl releases since 2022)—collectively raise compliance, labor and fuel cost risk for Allegiant.

| Metric | Value |

|---|---|

| FAA airport funds | $31.2B (through 2025) |

| DOT EAS/small airport | $200M (FY2024) |

| Avg incentive/new route | $1.2M (2024) |

| Jet fuel avg | $3.10/gal (2024) |

| Union membership change | +15% (2025 vs 2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect Allegiant across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, actionable insights for executives and investors, specific sub-points tied to the low-cost leisure airline model, forward-looking scenario implications, and clean formatting ready for business plans, decks, or reports.

Summarizes Allegiant's PESTLE insights into a concise, shareable format ideal for slide decks or strategy sessions, enabling quick alignment across teams and effortless inclusion in client reports.

Economic factors

Post Inflationary Consumer Spending Patterns

By end-2025 leisure travelers are more price-sensitive after multi-year inflation; consumer price index rose 3.4% in 2024 and CPI inflation averaged ~3.2% 2023–2025, pushing households toward lower-cost travel.

Allegiant’s ultra-low-cost model benefits as data show premium carrier domestic traffic down 4–6% in 2025 while LCC/ULCC routes grew ~5%, supporting Allegiant’s ticket and ancillary revenue mix.

However, stagnant real median weekly earnings—flat from 2023–2025 after adjusting for inflation—could restrain discretionary demand for bundled vacation packages and ancillary spending.

Fleet Transition Financing and Interest Rates

Allegiant’s shift to Boeing 737 MAX entails roughly $3.5–4.0 billion in aircraft CAPEX through 2028 based on announced orderbook; financing needs hinge on end-2025 rates—US 10-year Treasury at ~4.3% and average corporate borrowing costs near 6–7%—raising debt service costs if rates stay higher-for-longer.

Jet Fuel Price Volatility and Hedging

Fuel accounted for about 28% of Allegiant’s operating costs in 2024 and remains a key volatile expense into 2025; global oil supply shifts and U.S. refinery outages pushed jet fuel crack spreads up ~15% in late 2024, exposing Allegiant’s limited hedging versus larger carriers. With only modest fuel derivatives on the books, Allegiant must rapidly adjust fares and ancillary pricing to absorb sudden cost spikes while preserving appeal to price-sensitive leisure travelers.

Labor Market Competition and Wage Inflation

The aviation sector faces acute competition for pilots and A&P technicians in late 2025, with US pilot pay rising ~12% YoY and mechanic wages up ~9% per Bureau of Labor Statistics and airline reports, pressuring Allegiant’s low-cost model.

Allegiant reported 2024 CASM ex-fuel of roughly $0.08; upward wage pressure risks eroding this advantage unless offset by productivity gains or ancillary revenue growth.

- Pilot/technician wage inflation ~9–12% (2024–2025)

- Allegiant 2024 CASM ex-fuel ≈ $0.08

- Retention vs. cost trade-off critical for discount pricing

Ancillary Revenue Growth Trends

Ancillary revenue now accounts for roughly 35% of Allegiant’s 2024 total revenue, with baggage, seat selection and third-party commissions driving high-margin cash flow critical to unit economics.

In 2025 Allegiant’s model hinges on consumers buying add‑ons—hotel and car bookings contributed about $420 million in 2024—so lower hospitality demand cuts margins disproportionately.

A 2023–24 hospitality pullback saw RMS RevPAR declines of 2–4% in key markets, signaling downside risk to ancillary yields during economic contractions.

- Ancillaries ~35% of 2024 revenue

- Hotel/car commissions ≈ $420M in 2024

- RevPAR down 2–4% in 2023–24 markets—pressures yields

Price‑sensitive travel: LCCs surge +5% as CPI 3.4%, ancillaries 35% of revenue

Price-sensitive leisure demand after CPI ~3.4% in 2024; LCC/ULCC routes +5% in 2025 while premium domestic traffic -4–6%; real median weekly earnings flat 2023–2025; fuel ~28% of costs (2024) with jet crack spreads +15% late-2024; pilot/tech wages +9–12% (2024–25); ancillaries ~35% of revenue and hotel/car ≈$420M (2024).

| Metric | Value |

|---|---|

| CPI (2024) | 3.4% |

| LCC route growth (2025) | +5% |

| Fuel share (2024) | 28% |

| Ancillaries (2024) | 35%; $420M hotel/car |

Preview the Actual Deliverable

Allegiant PESTLE Analysis

The preview shown here is the exact Allegiant PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

What you see in the screenshot is the real file with complete content and layout; there are no placeholders or teasers.

After checkout you’ll instantly download this identical, final version for immediate use in analysis or presentations.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis of Allegiant reveals how regulatory shifts, fuel price volatility, and evolving travel preferences are shaping growth and risk—insights tailored for investors and strategists seeking a competitive edge. Purchase the full report to access detailed drivers, quantified impacts, and actionable recommendations you can apply immediately.

Political factors

Federal Aviation Administration Reauthorization Implementation

The 2024 FAA Reauthorization Act, effective through late 2025, allocates $31.2 billion for airport improvements and expands FAA oversight, influencing Allegiant’s access to 420+ non-primary airports and ramp projects critical to its point-to-point model.

New mandates on pilot training and ATC modernization—$5.4 billion for NextGen upgrades—raise training and compliance costs; Allegiant reported $162 million in operating margin in 2024 and must balance these mandates to preserve low-cost operations.

Department of Transportation Consumer Protection Mandates

The U.S. Department of Transportation tightened passenger-rights and fee-transparency rules in 2025, mandating automatic refunds and clearer disclosure of ancillary fees for baggage and seating; DOT enforcement actions rose 28% in 2025 versus 2024, increasing regulatory risk for carriers. Allegiant, which generated roughly 28% of 2024 ancillary revenue from fees, must continually update booking UI, pricing disclosures, and marketing to avoid fines and potential consumer-remediation costs.

Regional Airport Subsidy and Grant Programs

Political support for the Essential Air Service and regional airport grants remains critical for Allegiant’s point-to-point model; in FY2024 the U.S. DOT disbursed about $200 million to EAS and small airport programs, directly shaping Allegiant’s access to 150+ secondary airports it serves.

Federal and state funding decisions influence route expansion into underserved markets—Allegiant added 18 new markets in 2024 where airports received state/local incentives averaging $1.2 million per new route.

Local political leadership changes can alter incentives for low-cost carriers: between 2023–2025 several municipalities revised or rescinded incentive packages, affecting Allegiant’s base decisions and expected ROI timelines.

Labor Relations and Federal Mediation

The post-2024 surge in airline union activity has made labor relations more complex for Allegiant, with pilots and flight attendants pushing for higher pay and job protections; by 2025 national airline union membership rose ~15% year-over-year, raising potential labor costs.

Federal mediation has been pivotal in recent negotiations—mediators shortened dispute durations by an average of 30% in 2023–25, affecting settlement timing and cash flow for carriers like Allegiant.

The administration’s pro-mediator stance can accelerate settlements but may increase wage outcomes; a 2024 industry sample showed negotiated labor expense rises of 4–7%, pressuring Allegiant’s unit cost structure and margins.

- Union membership +15% (2025 vs 2024)

- Mediation cut dispute duration ~30% (2023–25)

- Negotiated labor costs up 4–7% in 2024

Geopolitical Influence on Domestic Energy Policy

Global political instability raises U.S. federal energy policy responses that affect domestic jet fuel costs; in 2024 U.S. jet fuel averaged about $3.10/gal versus $2.70/gal in 2023, amplifying operational expense risk for Allegiant.

Decisions on the Strategic Petroleum Reserve releases and drilling permits—DOE SPR releases of ~180 million barrels since 2022 and O&G permitting increases in 2024—drive short-term fuel price volatility impacting Allegiant’s margins.

Allegiant’s sensitivity: fuel is ~25–30% of CASM-ex fuel expense variance, so politically induced price swings materially affect quarterly profitability and unit cost forecasts.

- 2024 jet fuel avg ~$3.10/gal; 2023 ~$2.70/gal

- SPR releases ~180M barrels since 2022

- Fuel-related CASM variance ~25–30%

Policy shifts, rising unions and fuel costs heighten Allegiant's compliance & labor risk

Political shifts—FAA funding ($31.2B through 2025), DOT rule-tightening (2025 fee/transparency mandates), EAS/state incentives (~$200M FY2024; ~$1.2M avg incentive per new route in 2024), rising unionization (+15% 2025 vs 2024) and fuel policy (2024 jet fuel ~$3.10/gal; SPR ~180M bbl releases since 2022)—collectively raise compliance, labor and fuel cost risk for Allegiant.

| Metric | Value |

|---|---|

| FAA airport funds | $31.2B (through 2025) |

| DOT EAS/small airport | $200M (FY2024) |

| Avg incentive/new route | $1.2M (2024) |

| Jet fuel avg | $3.10/gal (2024) |

| Union membership change | +15% (2025 vs 2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect Allegiant across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, actionable insights for executives and investors, specific sub-points tied to the low-cost leisure airline model, forward-looking scenario implications, and clean formatting ready for business plans, decks, or reports.

Summarizes Allegiant's PESTLE insights into a concise, shareable format ideal for slide decks or strategy sessions, enabling quick alignment across teams and effortless inclusion in client reports.

Economic factors

Post Inflationary Consumer Spending Patterns

By end-2025 leisure travelers are more price-sensitive after multi-year inflation; consumer price index rose 3.4% in 2024 and CPI inflation averaged ~3.2% 2023–2025, pushing households toward lower-cost travel.

Allegiant’s ultra-low-cost model benefits as data show premium carrier domestic traffic down 4–6% in 2025 while LCC/ULCC routes grew ~5%, supporting Allegiant’s ticket and ancillary revenue mix.

However, stagnant real median weekly earnings—flat from 2023–2025 after adjusting for inflation—could restrain discretionary demand for bundled vacation packages and ancillary spending.

Fleet Transition Financing and Interest Rates

Allegiant’s shift to Boeing 737 MAX entails roughly $3.5–4.0 billion in aircraft CAPEX through 2028 based on announced orderbook; financing needs hinge on end-2025 rates—US 10-year Treasury at ~4.3% and average corporate borrowing costs near 6–7%—raising debt service costs if rates stay higher-for-longer.

Jet Fuel Price Volatility and Hedging

Fuel accounted for about 28% of Allegiant’s operating costs in 2024 and remains a key volatile expense into 2025; global oil supply shifts and U.S. refinery outages pushed jet fuel crack spreads up ~15% in late 2024, exposing Allegiant’s limited hedging versus larger carriers. With only modest fuel derivatives on the books, Allegiant must rapidly adjust fares and ancillary pricing to absorb sudden cost spikes while preserving appeal to price-sensitive leisure travelers.

Labor Market Competition and Wage Inflation

The aviation sector faces acute competition for pilots and A&P technicians in late 2025, with US pilot pay rising ~12% YoY and mechanic wages up ~9% per Bureau of Labor Statistics and airline reports, pressuring Allegiant’s low-cost model.

Allegiant reported 2024 CASM ex-fuel of roughly $0.08; upward wage pressure risks eroding this advantage unless offset by productivity gains or ancillary revenue growth.

- Pilot/technician wage inflation ~9–12% (2024–2025)

- Allegiant 2024 CASM ex-fuel ≈ $0.08

- Retention vs. cost trade-off critical for discount pricing

Ancillary Revenue Growth Trends

Ancillary revenue now accounts for roughly 35% of Allegiant’s 2024 total revenue, with baggage, seat selection and third-party commissions driving high-margin cash flow critical to unit economics.

In 2025 Allegiant’s model hinges on consumers buying add‑ons—hotel and car bookings contributed about $420 million in 2024—so lower hospitality demand cuts margins disproportionately.

A 2023–24 hospitality pullback saw RMS RevPAR declines of 2–4% in key markets, signaling downside risk to ancillary yields during economic contractions.

- Ancillaries ~35% of 2024 revenue

- Hotel/car commissions ≈ $420M in 2024

- RevPAR down 2–4% in 2023–24 markets—pressures yields

Price‑sensitive travel: LCCs surge +5% as CPI 3.4%, ancillaries 35% of revenue

Price-sensitive leisure demand after CPI ~3.4% in 2024; LCC/ULCC routes +5% in 2025 while premium domestic traffic -4–6%; real median weekly earnings flat 2023–2025; fuel ~28% of costs (2024) with jet crack spreads +15% late-2024; pilot/tech wages +9–12% (2024–25); ancillaries ~35% of revenue and hotel/car ≈$420M (2024).

| Metric | Value |

|---|---|

| CPI (2024) | 3.4% |

| LCC route growth (2025) | +5% |

| Fuel share (2024) | 28% |

| Ancillaries (2024) | 35%; $420M hotel/car |

Preview the Actual Deliverable

Allegiant PESTLE Analysis

The preview shown here is the exact Allegiant PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

What you see in the screenshot is the real file with complete content and layout; there are no placeholders or teasers.

After checkout you’ll instantly download this identical, final version for immediate use in analysis or presentations.