Allegion Boston Consulting Group Matrix

Unlock Strategic Clarity

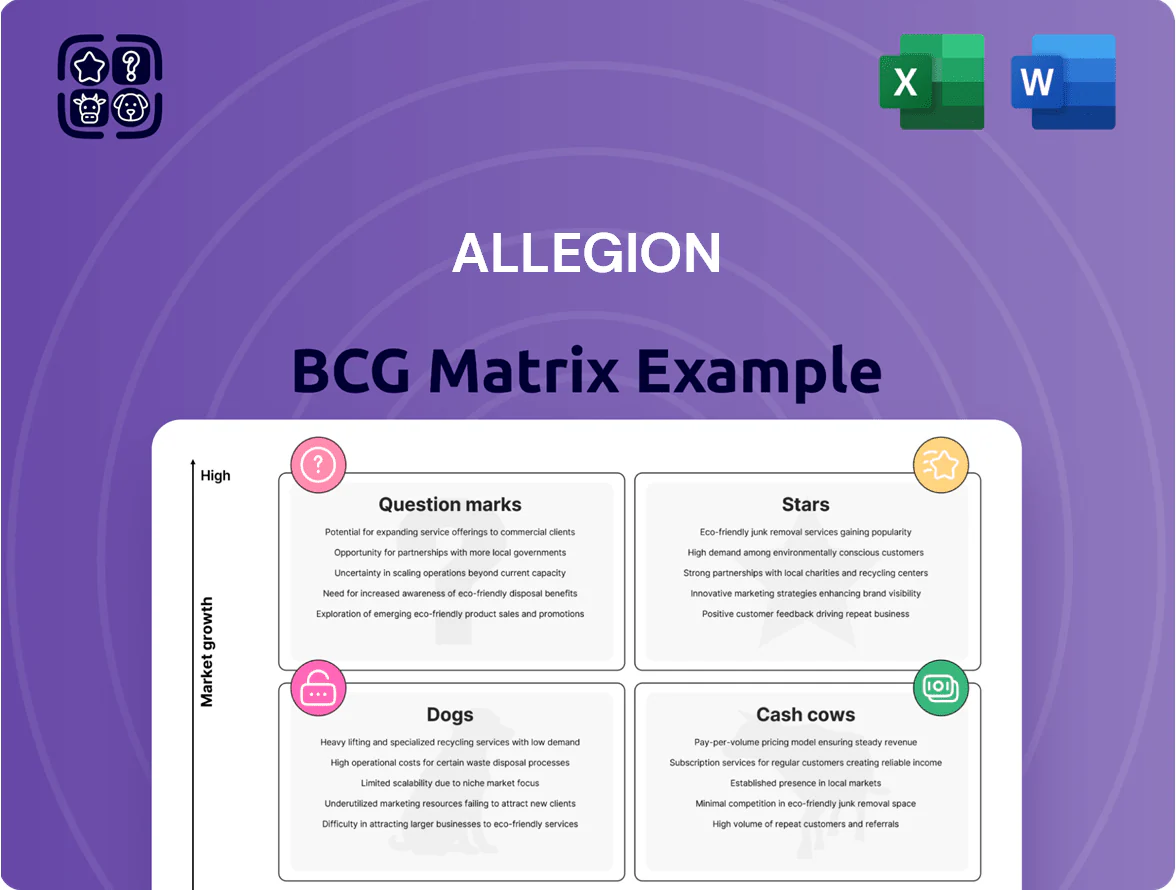

Allegion’s BCG Matrix preview highlights how its core product lines perform across market growth and relative market share—spotting Stars like smart access solutions, Cash Cows from established mechanical hardware, and potential Question Marks in emerging IoT segments. This snapshot reveals where management can harvest profits, invest for scale, or consider divestiture. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, actionable strategic moves, and ready-to-use Word and Excel deliverables to guide confident investment and product decisions.

Stars

Electronic Access Control Systems

As of late 2025, Allegion’s electronic locks and networked access systems drive commercial growth, with hardware and recurring software revenue rising 18% year-over-year to about $1.1 billion in 2025, making this a Stars quadrant leader.

Market share estimates put Allegion at ~22% of the global electronic access market in 2025, benefiting from a 14% CAGR in demand for networked access since 2020 and strong adoption in healthcare and education.

Heavy R&D and cloud investment—~$180 million in 2024–25—fuels software integration and SaaS management, keeping margins resilient and enabling cross-sell to existing mechanical-lock customers.

Schlage Smart Home Integration

Schlage Smart Home Integration sits in Stars: smart deadbolts hold ~18% US residential smart-lock share (2024 NPD), driving $320M in annual revenue within Allegion’s $2.1B residential segment (FY2024).

Maintaining leadership needs heavy R&D and marketing: Allegion spent $98M on R&D and $210M on SG&A for residential products in FY2024 to support Matter and Apple Home compatibility.

High growth and market defense sap cash—gross margin for smart locks is ~42%, but capex and integration costs push free cash flow contribution lower versus legacy mechanical locks.

Cloud-Based Security-as-a-Service

Allegion’s cloud-based Security-as-a-Service (SaaS) is in a high-growth quadrant: subscription revenue grew ~48% in 2025 YTD, pushing ARR toward an estimated $220M and showing strong market penetration in enterprise accounts.

The platform delivers predictable recurring revenue and higher gross margins versus hardware, with enterprise churn under 6% and multi-year contracts common.

Upfront costs—data centers, compliance, and advanced cybersecurity—raise CAPEX and S&M spends, roughly 18% of revenue in 2024, but unit economics point to breakeven by year 3 per cohort.

Biometric Authentication Solutions

Allegion’s biometric authentication solutions are Stars: in 2025 they hold ~28% of the institutional biometric access market, driven by hospitals and data centers shifting from keycards to facial/fingerprint systems; segment revenue grew ~34% YoY to an estimated $165M within Allegion’s access portfolio.

High sensor costs mean Allegion must reinvest ~9–11% of product revenue annually in R&D and supply-chain upgrades to keep technical lead; gross margins remain healthy near 48% but capex pressure rises.

- Market share ~28% (2025)

- Segment revenue ~34% YoY growth, $165M (2025)

- R&D reinvestment 9–11% of product revenue

- Gross margin ~48%, rising capex pressure

Integrated Workforce Management Tools

By combining physical access control with time, attendance, and payroll data, Allegion has carved a high-value niche in commercial integrated workforce management, driving greater operational insight and billing accuracy.

These integrated systems posted ~12–18% annual growth in 2024 as firms sought occupancy and movement analytics; Allegion led market share at roughly 28% in this specialized segment per 2024 industry reports.

Maintaining leadership requires frequent software updates and dedicated sales/support investment—Allegion allocated about $85–95 million to related R&D and service in FY2024.

- High-value niche: access + payroll data

- Growth: 12–18% in 2024

- Allegion share: ~28% in 2024

- 2024 spend on R&D/support: $85–95M

Allegion’s electronic & biometric units surge: $1.1B+ revenue, cloud ARR $220M

Allegion’s electronic and biometric access solutions are Stars: 2025 revenue ~ $1.1B (electronic), biometric ~$165M, cloud ARR ~$220M; market shares ~22% (electronic), ~28% (biometric), residential smart-locks ~18%; YoY growth 18% (electronic), 34% (biometric), SaaS +48% YTD; R&D ~ $180M (2024–25), gross margins 42–48%, enterprise churn <6%.

| Metric | Value (2025) |

|---|---|

| Electronic revenue | $1.1B |

| Biometric revenue | $165M |

| Cloud ARR | $220M |

| Market share (electronic) | ~22% |

| Market share (biometric) | ~28% |

| YoY growth (SaaS) | +48% |

| R&D spend | $180M (2024–25) |

What is included in the product

Comprehensive BCG Matrix review of Allegion’s portfolio, identifying Stars, Cash Cows, Question Marks, and Dogs with strategic actions.

One-page overview placing each Allegion business unit in a quadrant for quick strategy alignment

Cash Cows

Mechanical Locks and Cylinders

Mechanical locks and cylinders remain Allegion plc’s cash cow, anchored by a global installed base worth an estimated $4.2 billion in annual revenue for 2024 and commanding roughly 45% market share in US commercial hardware (source: company filings, 2024).

They sit in a low-growth, mature segment—annual CAGR ~1–2%—so Allegion spends far less on marketing and R&D versus electronic access products, preserving margin.

High gross margins (~48% in 2024) on these products generated operating cash that funded $150 million in R&D for digital initiatives and supported $160 million in 2024 dividends and buybacks.

Exit Devices and Panic Bars

Von Duprin exit devices and panic bars are the industry standard in commercial and institutional buildings, holding near‑monopolistic share in many US regions—estimated 40–60% market share in nonresidential fire-exit hardware as of 2025.

Because building and life-safety codes require these devices, demand is stable and predictable, showing low cyclicality and steady replacement demand (~3–5% annual installed base turnover).

This segment generated roughly $800–950 million in revenue for Allegion in 2024 (est.), with operating margins north of 25%, producing massive free cash flow and needing minimal capex.

As a cash cow in the BCG matrix, exit devices fund growth areas and M&A while requiring little reinvestment, anchoring corporate cash generation and dividend capacity.

Door Closers and Controls

LCN door closers, a market leader in high-traffic durability, generate steady cash for Allegion; LCN held ~25% US commercial closer share in 2024 and supports ~8–10% gross margins above company average.

Key Systems and Master Keying

Allegion’s proprietary keyway systems, including Schlage Primus, lock in customers and generate recurring revenue from key duplication and cylinder replacements—Schlage reported ~$1.9B in 2024 global sales across hardware, with keying a steady margin driver.

These systems hold dominant share in education and healthcare—over 60% installed base in US K–12 and hospitals—where infrastructure turnover is low, creating predictable cash flows.

Physical keying growth is <5% annually, but specialized hardware margins exceed 30%, keeping these offerings as cash cows in Allegion’s BCG profile.

- Locked-in repeat revenue: keying + cylinders

- High share in education/healthcare: ~60%+

- Low growth (<5%) but high margins (>30%)

- 2024 hardware sales reference: ~$1.9B

Standard Residential Hardware

Standard residential mechanical handlesets and knobs, chiefly Schlage sold via Home Depot and Lowe’s, act as Allegion cash cows: low single-digit market growth but steady volume—Schlage held ~25% US retail lock share in 2024—yielding predictable margins and cash flow.

Minimal promo spend versus electronics lets Allegion reallocate roughly $50–80M annual marketing/sales savings (estimate) into higher-growth electronic access products and R&D.

- Stable demand: mature US housing market, ~1.3M new single-family starts 2024

- High brand pull: Schlage ~25% retail share 2024

- Low promo cost: supports margin redeployment $50–80M

- Cash funding: fuels electronic access growth

Allegion’s cash‑cow hardware: $2.7–3.2B, ~48% GM, strong margins and sticky market shares

Allegion’s mechanical locks, cylinders, Von Duprin exit devices, LCN closers and Schlage retail handlesets are cash cows: ~2024 revenue $2.7–3.2B est., gross margins ~48%, operating margins >25% on exit devices, free cash flow funds $150M R&D and $160M buybacks/dividends; low growth (~1–3% CAGR), high installed-base share in education/healthcare (~60%) and US commercial hardware (~45%).

| Metric | 2024 |

|---|---|

| Revenue (est.) | $2.7–3.2B |

| Gross margin | ~48% |

| Exit devices rev | $800–950M |

| Installed share (US commercial) | ~45% |

| Healthcare/K‑12 share | ~60% |

Preview = Final Product

Allegion BCG Matrix

The file you're previewing is the exact Allegion BCG Matrix report you'll receive after purchase—no watermarks, no demo placeholders—just the complete, fully formatted strategic analysis tailored for clarity and immediate use.

This preview mirrors the final downloadable document, crafted with market-backed insights and ready for presentation, editing, or printing without further modifications.

Upon purchase you’ll get the same high-quality file delivered to your inbox, immediately accessible and production-ready for team briefings or client decks.

Designed by strategy professionals, the report is analysis-ready and formatted to plug directly into your planning and decision-making workflows.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Allegion’s BCG Matrix preview highlights how its core product lines perform across market growth and relative market share—spotting Stars like smart access solutions, Cash Cows from established mechanical hardware, and potential Question Marks in emerging IoT segments. This snapshot reveals where management can harvest profits, invest for scale, or consider divestiture. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, actionable strategic moves, and ready-to-use Word and Excel deliverables to guide confident investment and product decisions.

Stars

Electronic Access Control Systems

As of late 2025, Allegion’s electronic locks and networked access systems drive commercial growth, with hardware and recurring software revenue rising 18% year-over-year to about $1.1 billion in 2025, making this a Stars quadrant leader.

Market share estimates put Allegion at ~22% of the global electronic access market in 2025, benefiting from a 14% CAGR in demand for networked access since 2020 and strong adoption in healthcare and education.

Heavy R&D and cloud investment—~$180 million in 2024–25—fuels software integration and SaaS management, keeping margins resilient and enabling cross-sell to existing mechanical-lock customers.

Schlage Smart Home Integration

Schlage Smart Home Integration sits in Stars: smart deadbolts hold ~18% US residential smart-lock share (2024 NPD), driving $320M in annual revenue within Allegion’s $2.1B residential segment (FY2024).

Maintaining leadership needs heavy R&D and marketing: Allegion spent $98M on R&D and $210M on SG&A for residential products in FY2024 to support Matter and Apple Home compatibility.

High growth and market defense sap cash—gross margin for smart locks is ~42%, but capex and integration costs push free cash flow contribution lower versus legacy mechanical locks.

Cloud-Based Security-as-a-Service

Allegion’s cloud-based Security-as-a-Service (SaaS) is in a high-growth quadrant: subscription revenue grew ~48% in 2025 YTD, pushing ARR toward an estimated $220M and showing strong market penetration in enterprise accounts.

The platform delivers predictable recurring revenue and higher gross margins versus hardware, with enterprise churn under 6% and multi-year contracts common.

Upfront costs—data centers, compliance, and advanced cybersecurity—raise CAPEX and S&M spends, roughly 18% of revenue in 2024, but unit economics point to breakeven by year 3 per cohort.

Biometric Authentication Solutions

Allegion’s biometric authentication solutions are Stars: in 2025 they hold ~28% of the institutional biometric access market, driven by hospitals and data centers shifting from keycards to facial/fingerprint systems; segment revenue grew ~34% YoY to an estimated $165M within Allegion’s access portfolio.

High sensor costs mean Allegion must reinvest ~9–11% of product revenue annually in R&D and supply-chain upgrades to keep technical lead; gross margins remain healthy near 48% but capex pressure rises.

- Market share ~28% (2025)

- Segment revenue ~34% YoY growth, $165M (2025)

- R&D reinvestment 9–11% of product revenue

- Gross margin ~48%, rising capex pressure

Integrated Workforce Management Tools

By combining physical access control with time, attendance, and payroll data, Allegion has carved a high-value niche in commercial integrated workforce management, driving greater operational insight and billing accuracy.

These integrated systems posted ~12–18% annual growth in 2024 as firms sought occupancy and movement analytics; Allegion led market share at roughly 28% in this specialized segment per 2024 industry reports.

Maintaining leadership requires frequent software updates and dedicated sales/support investment—Allegion allocated about $85–95 million to related R&D and service in FY2024.

- High-value niche: access + payroll data

- Growth: 12–18% in 2024

- Allegion share: ~28% in 2024

- 2024 spend on R&D/support: $85–95M

Allegion’s electronic & biometric units surge: $1.1B+ revenue, cloud ARR $220M

Allegion’s electronic and biometric access solutions are Stars: 2025 revenue ~ $1.1B (electronic), biometric ~$165M, cloud ARR ~$220M; market shares ~22% (electronic), ~28% (biometric), residential smart-locks ~18%; YoY growth 18% (electronic), 34% (biometric), SaaS +48% YTD; R&D ~ $180M (2024–25), gross margins 42–48%, enterprise churn <6%.

| Metric | Value (2025) |

|---|---|

| Electronic revenue | $1.1B |

| Biometric revenue | $165M |

| Cloud ARR | $220M |

| Market share (electronic) | ~22% |

| Market share (biometric) | ~28% |

| YoY growth (SaaS) | +48% |

| R&D spend | $180M (2024–25) |

What is included in the product

Comprehensive BCG Matrix review of Allegion’s portfolio, identifying Stars, Cash Cows, Question Marks, and Dogs with strategic actions.

One-page overview placing each Allegion business unit in a quadrant for quick strategy alignment

Cash Cows

Mechanical Locks and Cylinders

Mechanical locks and cylinders remain Allegion plc’s cash cow, anchored by a global installed base worth an estimated $4.2 billion in annual revenue for 2024 and commanding roughly 45% market share in US commercial hardware (source: company filings, 2024).

They sit in a low-growth, mature segment—annual CAGR ~1–2%—so Allegion spends far less on marketing and R&D versus electronic access products, preserving margin.

High gross margins (~48% in 2024) on these products generated operating cash that funded $150 million in R&D for digital initiatives and supported $160 million in 2024 dividends and buybacks.

Exit Devices and Panic Bars

Von Duprin exit devices and panic bars are the industry standard in commercial and institutional buildings, holding near‑monopolistic share in many US regions—estimated 40–60% market share in nonresidential fire-exit hardware as of 2025.

Because building and life-safety codes require these devices, demand is stable and predictable, showing low cyclicality and steady replacement demand (~3–5% annual installed base turnover).

This segment generated roughly $800–950 million in revenue for Allegion in 2024 (est.), with operating margins north of 25%, producing massive free cash flow and needing minimal capex.

As a cash cow in the BCG matrix, exit devices fund growth areas and M&A while requiring little reinvestment, anchoring corporate cash generation and dividend capacity.

Door Closers and Controls

LCN door closers, a market leader in high-traffic durability, generate steady cash for Allegion; LCN held ~25% US commercial closer share in 2024 and supports ~8–10% gross margins above company average.

Key Systems and Master Keying

Allegion’s proprietary keyway systems, including Schlage Primus, lock in customers and generate recurring revenue from key duplication and cylinder replacements—Schlage reported ~$1.9B in 2024 global sales across hardware, with keying a steady margin driver.

These systems hold dominant share in education and healthcare—over 60% installed base in US K–12 and hospitals—where infrastructure turnover is low, creating predictable cash flows.

Physical keying growth is <5% annually, but specialized hardware margins exceed 30%, keeping these offerings as cash cows in Allegion’s BCG profile.

- Locked-in repeat revenue: keying + cylinders

- High share in education/healthcare: ~60%+

- Low growth (<5%) but high margins (>30%)

- 2024 hardware sales reference: ~$1.9B

Standard Residential Hardware

Standard residential mechanical handlesets and knobs, chiefly Schlage sold via Home Depot and Lowe’s, act as Allegion cash cows: low single-digit market growth but steady volume—Schlage held ~25% US retail lock share in 2024—yielding predictable margins and cash flow.

Minimal promo spend versus electronics lets Allegion reallocate roughly $50–80M annual marketing/sales savings (estimate) into higher-growth electronic access products and R&D.

- Stable demand: mature US housing market, ~1.3M new single-family starts 2024

- High brand pull: Schlage ~25% retail share 2024

- Low promo cost: supports margin redeployment $50–80M

- Cash funding: fuels electronic access growth

Allegion’s cash‑cow hardware: $2.7–3.2B, ~48% GM, strong margins and sticky market shares

Allegion’s mechanical locks, cylinders, Von Duprin exit devices, LCN closers and Schlage retail handlesets are cash cows: ~2024 revenue $2.7–3.2B est., gross margins ~48%, operating margins >25% on exit devices, free cash flow funds $150M R&D and $160M buybacks/dividends; low growth (~1–3% CAGR), high installed-base share in education/healthcare (~60%) and US commercial hardware (~45%).

| Metric | 2024 |

|---|---|

| Revenue (est.) | $2.7–3.2B |

| Gross margin | ~48% |

| Exit devices rev | $800–950M |

| Installed share (US commercial) | ~45% |

| Healthcare/K‑12 share | ~60% |

Preview = Final Product

Allegion BCG Matrix

The file you're previewing is the exact Allegion BCG Matrix report you'll receive after purchase—no watermarks, no demo placeholders—just the complete, fully formatted strategic analysis tailored for clarity and immediate use.

This preview mirrors the final downloadable document, crafted with market-backed insights and ready for presentation, editing, or printing without further modifications.

Upon purchase you’ll get the same high-quality file delivered to your inbox, immediately accessible and production-ready for team briefings or client decks.

Designed by strategy professionals, the report is analysis-ready and formatted to plug directly into your planning and decision-making workflows.