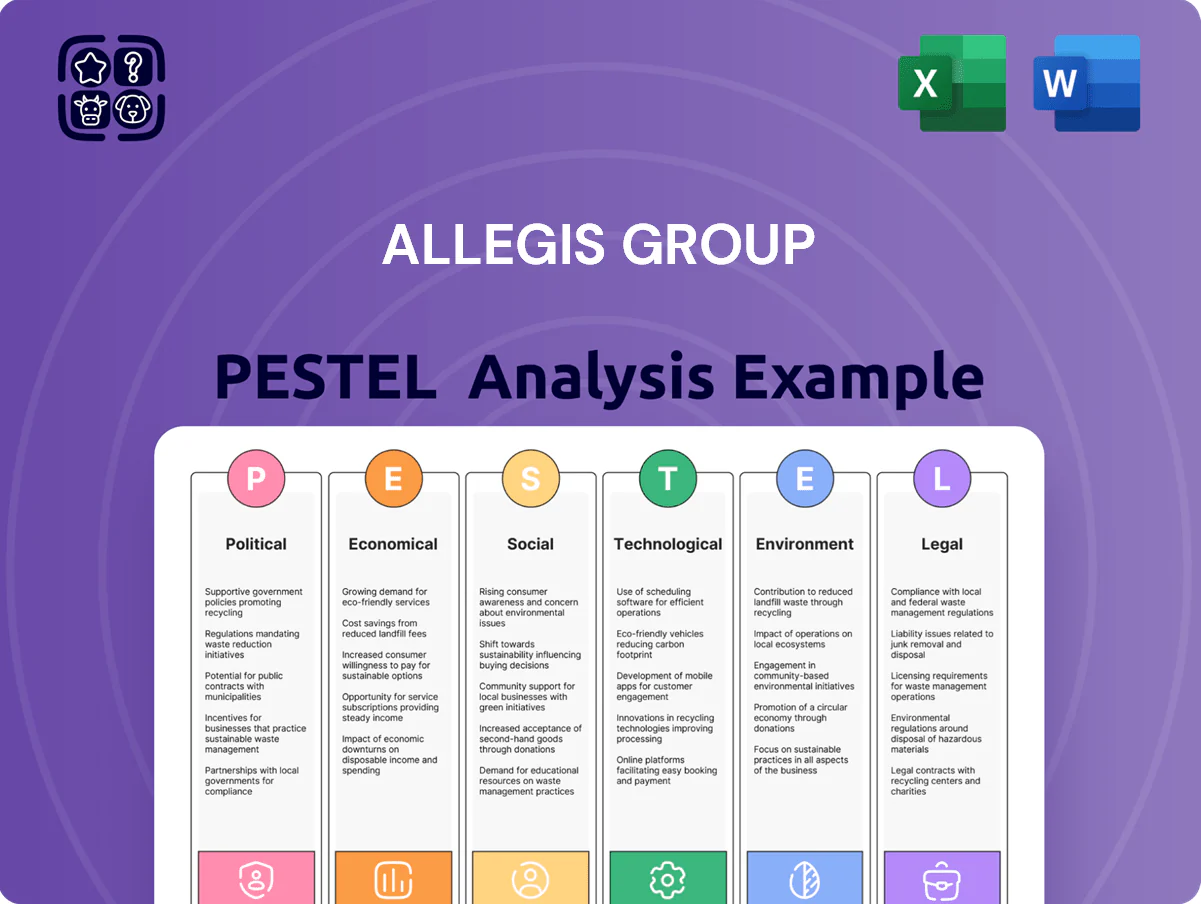

Allegis Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and tech disruption are reshaping Allegis Group’s staffing and talent solutions—our concise PESTLE highlights the external forces that matter most to investors and strategists. Purchase the full analysis to access actionable insights, risk forecasts, and customizable charts that accelerate decision-making and competitive planning.

Political factors

Changes in Global Immigration Policies

Immigration regulations in key markets like the US and EU directly affect mobility of high-skilled labor and availability of specialized talent, with H-1B, TN and EU Blue Card processes determining placement speed and costs.

As of late 2025, slower US visa processing—average adjudication delays up ~22% vs 2023—and tightened EU work-permit quotas force Allegis to keep agile global mobility programs to meet client staffing needs.

Political stability and cross-border labor agreements remain vital: bilateral pacts and streamlined visa corridors reduce administrative delays, enabling Allegis to deploy specialists where demand yields higher margin and utilization.

Government Infrastructure and Tech Spending

Rising public sector digital transformation and infrastructure spending—US federal IT budget ~$98.5B in FY2025 and $153B+ in infrastructure allocations from the Bipartisan Infrastructure Law—boosts demand for Allegis’ engineering and IT staffing via TEKsystems and Aston Carter.

Large government contracts carry tight compliance and security-clearance hurdles, favoring established providers with institutional knowledge that Allegis has built across federal and state programs.

Aligning recruitment pipelines to state-funded initiatives lets Allegis capture long-term, high-value talent-management streams, with government spending acting as a key catalyst for growth in its public-sector-facing brands.

Geopolitical Trade Relations and Outsourcing

Trade tensions and a 28% rise in near-shoring deals since 2021 shift MNCs toward friend-shoring, pushing Allegis to realign talent hubs to Europe and Mexico to match client footprints.

Political moves discouraging offshoring to some APAC countries have forced Allegis to reconfigure delivery centers and sourcing strategies, impacting operating costs and margin mix.

Offering talent in politically stable markets—where demand for de-risked supply chains rose 22% in 2024—gives Allegis a measurable competitive edge for global clients.

Continuous monitoring of diplomatic shifts across EMEA and APAC is essential for Allegis’ long-term planning and client retention.

Public Sector Procurement and Compliance Rules

Governments now demand stricter social and ethical vendor standards; 2024 US federal procurement rules increased small business and veteran hiring preferences, affecting Allegis' access to ~$700B annual federal contracting spend.

Allegis must comply with local hiring quotas and supplier diversity programs across jurisdictions; noncompliance risks loss of government staffing contracts and removal from preferred vendor lists.

Robust internal governance and real-time reporting are required to meet transparency standards—failure could materially impact revenue from public-sector clients, which represented an estimated 12–15% of industry staffing billings in 2023–24.

- Must meet local hiring, veteran employment, small business sourcing

- Subject to evolving federal/state procurement rules (~$700B US market)

- Noncompliance risks contract loss and vendor delisting

- Requires strong governance, transparency, and reporting systems

National Security and Labor Restrictions

Rising political emphasis on national security—evidenced by US CHIPS and Science Act funding of $53B for semiconductors (2022) and tighter export controls—forces stricter labor restrictions in semiconductor and aerospace roles, requiring Allegis to enforce rigorous vetting and compliance for cleared positions.

These security filters reduce the eligible talent pool—estimated 10–20% fewer candidates for sensitive roles—heightening demand for Allegis’s specialized sourcing; staying compliant with evolving policies is crucial to retaining defense and tech clients and market share.

- CHIPS Act: $53B semiconductor funding

- Estimated 10–20% candidate pool reduction for cleared roles

- Rigorous vetting/compliance required for cleared placements

- Compliance key to retaining defense/tech market share

Federal IT boom vs talent squeeze: budgets up, visas slow, cleared pool down 10–20%

Political factors: visa/work-permit constraints (US visa delays +22% vs 2023) and tightened EU quotas affect skilled placement speed; increased US federal IT/infrastructure spend (~$98.5B FY2025 IT; $153B+ infrastructure) drives public-sector demand; procurement rules (~$700B US federal market) raise compliance/diversity requirements; CHIPS/security controls ($53B) shrink cleared candidate pools ~10–20%, raising sourcing costs.

| Factor | 2024–25 datapoint |

|---|---|

| US IT budget | $98.5B (FY2025) |

| Infrastructure funding | $153B+ |

| Federal contracting market | ~$700B |

| Visa delays | +22% adjudication time vs 2023 |

| Cleared talent impact | −10–20% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Allegis Group’s staffing and workforce-solutions operations, with data-driven trends and region-specific regulatory context to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary for Allegis Group that can be dropped into presentations or shared across teams to quickly align on external risks, market positioning, and strategic implications.

Economic factors

Global Interest Rate and Capital Expenditure Trends

At end-2025, global policy rates averaged about 4.5% (IMF World Economic Outlook 2025), directly constraining corporate CAPEX and reducing permanent hiring, which lowers clients’ demand for Allegis’s direct-hire services and raises contingent labor spend. High borrowing costs push firms toward flexible staffing to preserve liquidity, enabling Allegis to position staffing as a variable, off-balance-sheet expense. If central banks cut rates and global policy rates fall below 3% in 2026, firms may accelerate permanent recruitment, requiring Allegis to scale executive search and direct-hire capabilities to capture rising demand.

Inflationary Pressures on Global Wage Demands

Persistent inflation—U.S. CPI ~3.4% in 2024 and Eurozone HICP ~2.9%—has driven skilled professional wage demands up 4–6% year-over-year, complicating talent acquisition for Allegis clients.

Allegis must supply data-driven market benchmarks and pay bands so clients can balance competitive offers with target margins amid average staffing gross margin compression of ~100–200 basis points in 2023–24.

Wage-price spirals risk further margin squeeze if contract rates lag rising labor costs, requiring Allegis to adjust pricing and contract terms dynamically.

As intermediary, Allegis needs real-time economic monitoring and advanced negotiation capabilities to align employer budgets with candidate expectations and preserve placement volumes.

The Expansion of the Contingent Labor Market

Economic uncertainty has accelerated gigification: by 2024 the US contingent workforce reached ~27% of workers (Upwork/Oxford), and corporate use of contract talent rose 15% YoY, driving demand for Allegis’s contingent workforce management expertise.

Allegis benefits as firms shift from full-time hires to contract-based expertise, with MSP and RPO spend projected to grow at ~6–8% CAGR through 2026, supporting higher service revenues.

As companies go asset-light, client outsourcing to MSP/RPO increases; Allegis’s scale positions it to capture market share and recurring fee streams amid this structural, multi-year tailwind.

Currency Exchange Volatility and Global Revenue

As a global staffing leader, Allegis faces currency exchange volatility that can sway reported international revenues and raise cross-border service costs; e.g., a 10% depreciation in a major currency can cut converted revenue materially—recent FX swings in 2024 saw emerging-market currencies fall 5–15% vs USD.

Regional economic instability can devalue local earnings when converted to the dollar, reducing subsidiary profitability; Allegis mitigates this with hedging, localized pricing, and contract clauses.

- Exposure: multi-currency revenue streams; 2024 FX moves ±5–15%

- Impact: lower converted margins, higher cross-border costs

- Mitigation: hedging, localized pricing, FX clauses

- Priority: monitor macro shifts to protect subsidiary financials

Unemployment Rates and Labor Market Tightness

Low unemployment in specialties like cybersecurity (US job vacancy rate ~3.2% for cybersecurity roles in 2024) and renewable energy (global clean energy jobs 65 million in 2023, growing ~6%/yr) intensifies the war for talent, raising demand and fees for Allegis’s sourcing services.

Tight labor markets push clients to pay recruitment premiums; Allegis’s specialized expertise captures higher margins, while a downturn could reduce job volume and shift demand to reorganization and outplacement.

Allegis must stay versatile—combining contingent staffing, executive search, and outplacement—to monetize both hiring booms and economic cooling.

- Cybersecurity vacancy rate ~3.2% (US, 2024) increases recruiter leverage

- Clean energy jobs ~65M globally (2023), ~6% annual growth

- Tight markets → higher premiums; downturns → focus on outplacement

- Versatility across staffing, search, outplacement preserves revenue

Higher rates reshape staffing: contingent work rises, margins squeezed—hiring may rebound 2026

Higher global rates (~4.5% end‑2025) push firms to flexible staffing; potential cuts <3% in 2026 could revive permanent hires. 2024 wage inflation (US CPI 3.4%, Euro HICP 2.9%) raised skilled wages 4–6% YoY, compressing staffing margins ~100–200 bps. Contingent work ~27% US workforce (2024); MSP/RPO CAGR ~6–8% to 2026. FX moves ±5–15% (2024) threaten converted revenues; mitigation: hedging, local pricing.

| Metric | Value |

|---|---|

| Global policy rate (end‑2025) | ~4.5% |

| US CPI (2024) | 3.4% |

| Contingent workforce (US, 2024) | ~27% |

| MSP/RPO CAGR | ~6–8% to 2026 |

| FX moves (2024) | ±5–15% |

Preview the Actual Deliverable

Allegis Group PESTLE Analysis

The preview shown here is the exact Allegis Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy, risk assessment, or investor briefing.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and tech disruption are reshaping Allegis Group’s staffing and talent solutions—our concise PESTLE highlights the external forces that matter most to investors and strategists. Purchase the full analysis to access actionable insights, risk forecasts, and customizable charts that accelerate decision-making and competitive planning.

Political factors

Changes in Global Immigration Policies

Immigration regulations in key markets like the US and EU directly affect mobility of high-skilled labor and availability of specialized talent, with H-1B, TN and EU Blue Card processes determining placement speed and costs.

As of late 2025, slower US visa processing—average adjudication delays up ~22% vs 2023—and tightened EU work-permit quotas force Allegis to keep agile global mobility programs to meet client staffing needs.

Political stability and cross-border labor agreements remain vital: bilateral pacts and streamlined visa corridors reduce administrative delays, enabling Allegis to deploy specialists where demand yields higher margin and utilization.

Government Infrastructure and Tech Spending

Rising public sector digital transformation and infrastructure spending—US federal IT budget ~$98.5B in FY2025 and $153B+ in infrastructure allocations from the Bipartisan Infrastructure Law—boosts demand for Allegis’ engineering and IT staffing via TEKsystems and Aston Carter.

Large government contracts carry tight compliance and security-clearance hurdles, favoring established providers with institutional knowledge that Allegis has built across federal and state programs.

Aligning recruitment pipelines to state-funded initiatives lets Allegis capture long-term, high-value talent-management streams, with government spending acting as a key catalyst for growth in its public-sector-facing brands.

Geopolitical Trade Relations and Outsourcing

Trade tensions and a 28% rise in near-shoring deals since 2021 shift MNCs toward friend-shoring, pushing Allegis to realign talent hubs to Europe and Mexico to match client footprints.

Political moves discouraging offshoring to some APAC countries have forced Allegis to reconfigure delivery centers and sourcing strategies, impacting operating costs and margin mix.

Offering talent in politically stable markets—where demand for de-risked supply chains rose 22% in 2024—gives Allegis a measurable competitive edge for global clients.

Continuous monitoring of diplomatic shifts across EMEA and APAC is essential for Allegis’ long-term planning and client retention.

Public Sector Procurement and Compliance Rules

Governments now demand stricter social and ethical vendor standards; 2024 US federal procurement rules increased small business and veteran hiring preferences, affecting Allegis' access to ~$700B annual federal contracting spend.

Allegis must comply with local hiring quotas and supplier diversity programs across jurisdictions; noncompliance risks loss of government staffing contracts and removal from preferred vendor lists.

Robust internal governance and real-time reporting are required to meet transparency standards—failure could materially impact revenue from public-sector clients, which represented an estimated 12–15% of industry staffing billings in 2023–24.

- Must meet local hiring, veteran employment, small business sourcing

- Subject to evolving federal/state procurement rules (~$700B US market)

- Noncompliance risks contract loss and vendor delisting

- Requires strong governance, transparency, and reporting systems

National Security and Labor Restrictions

Rising political emphasis on national security—evidenced by US CHIPS and Science Act funding of $53B for semiconductors (2022) and tighter export controls—forces stricter labor restrictions in semiconductor and aerospace roles, requiring Allegis to enforce rigorous vetting and compliance for cleared positions.

These security filters reduce the eligible talent pool—estimated 10–20% fewer candidates for sensitive roles—heightening demand for Allegis’s specialized sourcing; staying compliant with evolving policies is crucial to retaining defense and tech clients and market share.

- CHIPS Act: $53B semiconductor funding

- Estimated 10–20% candidate pool reduction for cleared roles

- Rigorous vetting/compliance required for cleared placements

- Compliance key to retaining defense/tech market share

Federal IT boom vs talent squeeze: budgets up, visas slow, cleared pool down 10–20%

Political factors: visa/work-permit constraints (US visa delays +22% vs 2023) and tightened EU quotas affect skilled placement speed; increased US federal IT/infrastructure spend (~$98.5B FY2025 IT; $153B+ infrastructure) drives public-sector demand; procurement rules (~$700B US federal market) raise compliance/diversity requirements; CHIPS/security controls ($53B) shrink cleared candidate pools ~10–20%, raising sourcing costs.

| Factor | 2024–25 datapoint |

|---|---|

| US IT budget | $98.5B (FY2025) |

| Infrastructure funding | $153B+ |

| Federal contracting market | ~$700B |

| Visa delays | +22% adjudication time vs 2023 |

| Cleared talent impact | −10–20% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Allegis Group’s staffing and workforce-solutions operations, with data-driven trends and region-specific regulatory context to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary for Allegis Group that can be dropped into presentations or shared across teams to quickly align on external risks, market positioning, and strategic implications.

Economic factors

Global Interest Rate and Capital Expenditure Trends

At end-2025, global policy rates averaged about 4.5% (IMF World Economic Outlook 2025), directly constraining corporate CAPEX and reducing permanent hiring, which lowers clients’ demand for Allegis’s direct-hire services and raises contingent labor spend. High borrowing costs push firms toward flexible staffing to preserve liquidity, enabling Allegis to position staffing as a variable, off-balance-sheet expense. If central banks cut rates and global policy rates fall below 3% in 2026, firms may accelerate permanent recruitment, requiring Allegis to scale executive search and direct-hire capabilities to capture rising demand.

Inflationary Pressures on Global Wage Demands

Persistent inflation—U.S. CPI ~3.4% in 2024 and Eurozone HICP ~2.9%—has driven skilled professional wage demands up 4–6% year-over-year, complicating talent acquisition for Allegis clients.

Allegis must supply data-driven market benchmarks and pay bands so clients can balance competitive offers with target margins amid average staffing gross margin compression of ~100–200 basis points in 2023–24.

Wage-price spirals risk further margin squeeze if contract rates lag rising labor costs, requiring Allegis to adjust pricing and contract terms dynamically.

As intermediary, Allegis needs real-time economic monitoring and advanced negotiation capabilities to align employer budgets with candidate expectations and preserve placement volumes.

The Expansion of the Contingent Labor Market

Economic uncertainty has accelerated gigification: by 2024 the US contingent workforce reached ~27% of workers (Upwork/Oxford), and corporate use of contract talent rose 15% YoY, driving demand for Allegis’s contingent workforce management expertise.

Allegis benefits as firms shift from full-time hires to contract-based expertise, with MSP and RPO spend projected to grow at ~6–8% CAGR through 2026, supporting higher service revenues.

As companies go asset-light, client outsourcing to MSP/RPO increases; Allegis’s scale positions it to capture market share and recurring fee streams amid this structural, multi-year tailwind.

Currency Exchange Volatility and Global Revenue

As a global staffing leader, Allegis faces currency exchange volatility that can sway reported international revenues and raise cross-border service costs; e.g., a 10% depreciation in a major currency can cut converted revenue materially—recent FX swings in 2024 saw emerging-market currencies fall 5–15% vs USD.

Regional economic instability can devalue local earnings when converted to the dollar, reducing subsidiary profitability; Allegis mitigates this with hedging, localized pricing, and contract clauses.

- Exposure: multi-currency revenue streams; 2024 FX moves ±5–15%

- Impact: lower converted margins, higher cross-border costs

- Mitigation: hedging, localized pricing, FX clauses

- Priority: monitor macro shifts to protect subsidiary financials

Unemployment Rates and Labor Market Tightness

Low unemployment in specialties like cybersecurity (US job vacancy rate ~3.2% for cybersecurity roles in 2024) and renewable energy (global clean energy jobs 65 million in 2023, growing ~6%/yr) intensifies the war for talent, raising demand and fees for Allegis’s sourcing services.

Tight labor markets push clients to pay recruitment premiums; Allegis’s specialized expertise captures higher margins, while a downturn could reduce job volume and shift demand to reorganization and outplacement.

Allegis must stay versatile—combining contingent staffing, executive search, and outplacement—to monetize both hiring booms and economic cooling.

- Cybersecurity vacancy rate ~3.2% (US, 2024) increases recruiter leverage

- Clean energy jobs ~65M globally (2023), ~6% annual growth

- Tight markets → higher premiums; downturns → focus on outplacement

- Versatility across staffing, search, outplacement preserves revenue

Higher rates reshape staffing: contingent work rises, margins squeezed—hiring may rebound 2026

Higher global rates (~4.5% end‑2025) push firms to flexible staffing; potential cuts <3% in 2026 could revive permanent hires. 2024 wage inflation (US CPI 3.4%, Euro HICP 2.9%) raised skilled wages 4–6% YoY, compressing staffing margins ~100–200 bps. Contingent work ~27% US workforce (2024); MSP/RPO CAGR ~6–8% to 2026. FX moves ±5–15% (2024) threaten converted revenues; mitigation: hedging, local pricing.

| Metric | Value |

|---|---|

| Global policy rate (end‑2025) | ~4.5% |

| US CPI (2024) | 3.4% |

| Contingent workforce (US, 2024) | ~27% |

| MSP/RPO CAGR | ~6–8% to 2026 |

| FX moves (2024) | ±5–15% |

Preview the Actual Deliverable

Allegis Group PESTLE Analysis

The preview shown here is the exact Allegis Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy, risk assessment, or investor briefing.