Alliar Boston Consulting Group Matrix

Download Your Competitive Advantage

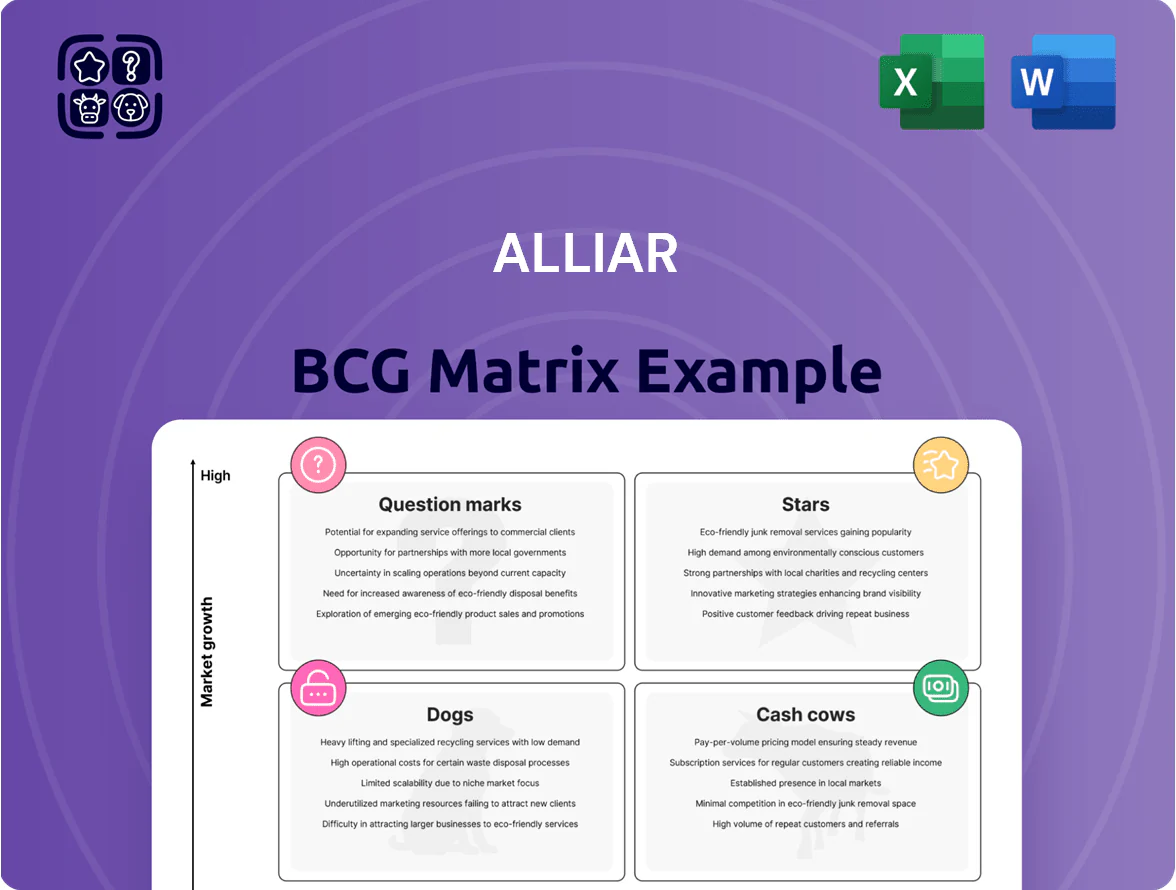

Alliar’s BCG Matrix preview highlights which service lines could be Stars driving growth and which may be Cash Cows funding operations, while flagging lower-growth Dogs and ambivalent Question Marks—offering a quick strategic snapshot of competitive positioning and resource allocation. This glimpse is useful, but the full BCG Matrix delivers quadrant-by-quadrant data, tactical recommendations, and ready-to-use visuals to guide investment and portfolio decisions. Purchase the complete report for an editable Word analysis plus an Excel summary—instantly actionable insights to prioritize capital and sharpen strategy.

Stars

High-End MRI Services

Alliar’s high-end MRI units lead high-complexity imaging in São Paulo, Rio de Janeiro and Brasília, capturing ~40% market share in metropolitan precision diagnostics by end-2025 and seeing year-on-year revenue growth near 12% in 2024–25.

These MRI services need heavy capex—typical unit installs cost R$4–6 million—but deliver higher insurance reimbursements (avg. +22% vs routine imaging) and handle >60,000 scans annually across flagship centers.

By Dec 31, 2025, high-end MRI operations ranked as Stars in the BCG matrix: high market share plus high market growth driven by Brazil’s 12.6% population aged 60+ (2025 IBGE estimate), supporting sustained volume and pricing strength.

iDr Remote Reporting Platform

iDr Remote Reporting Platform is Alliar’s first-to-market national tele-radiology service, driving high growth in Brazil’s digital health market which grew ~22% in 2024 to BRL 18.4bn; iDr handled ~1.2M reads in 2025 YTD, boosting revenue per read by 14% vs 2022.

It sits in the BCG Stars quadrant: market share expanding fast with scalable unit economics, yet it still consumes cash—Alliar reported BRL 18M capex/software and BRL 4.5M annual cybersecurity spend in 2024—to sustain uptime and regulatory compliance.

Specialized Cardiovascular Imaging

Specialized Cardiovascular Imaging is a Star: the segment grew ~14% CAGR 2020–2024 to reach an estimated $420m in 2024, driven by demand from heart centers for integrated, high-res diagnostics.

Alliar holds a leading niche share ~28% via partnerships with 12 top-tier hospitals and 30 cardiology clinics, converting referral volume into recurring revenue.

Maintaining edge requires ongoing capex; Alliar invested BRL 45m in imaging hardware in 2024 to counter boutique entrants and preserve margins.

Strategic Hospital In-Sourcing

Alliar’s in-hospital units act as Stars in the BCG matrix: embedded in major private hospitals, they capture loyal patients and show high revenue growth—Alliar reported 2024 in-hospital revenue growth of ~18% and same-unit volume up 12% year-over-year through Q3 2025.

These partnerships let Alliar dominate high-complexity diagnostics inside partner networks, delivering 55% of group EBITDA margin contribution from in-hospital services in 2024 and maintaining >60% share of complex imaging cases in partnered hospitals.

The steady flow of emergency and elective procedures—~1.2 million in-hospital exams annually as of 2024—keeps these units market leaders, supporting CAPEX for advanced PET/CT and MRI upgrades and sustaining double-digit ROIC above 12%.

- High growth: ~18% in-hospital revenue growth 2024

- Volume: ~1.2M in-hospital exams annually (2024)

- Profit mix: 55% EBITDA contribution from in-hospital units (2024)

- Market share: >60% of complex imaging in partner hospitals

- Returns: ROIC >12%, supporting PET/CT & MRI CAPEX

Advanced Oncological Screening

Advanced Oncological Screening (Stars): Alliar’s PET-CT and screening services drive fast revenue growth—PET-CT volumes rose 18% YoY in 2025 and contributed ~22% of Alliar’s diagnostic revenue in Q1 2025, underpinning high-margin expansion.

The company holds double-digit market shares in Minas Gerais and São Paulo (estimated 28% and 24% private oncology diagnostics share in 2024), positioning it to convert demand into long-term dominance with sustained specialist promotion.

These services need continuous physician marketing and referral programs but offer the highest ROI and scalability across private networks, supporting projected cancer-screening CAGR of ~14% through 2028.

- 18% YoY PET-CT volume growth (2025)

- ~22% of diagnostic revenue (Q1 2025)

- Market share: 28% Minas Gerais, 24% São Paulo (2024)

- Projected screening CAGR ~14% to 2028

Alliar’s Imaging Powerhouse: MRI 40% share, iDr 1.2M reads, PET-CT +18% driving >50% EBITDA

Alliar’s Stars: high-end MRI, iDr tele-radiology, cardiovascular imaging, in-hospital units, and PET-CT show high share and growth—MRI ~40% metro share (2025), iDr ~1.2M reads YTD (2025), CV imaging ~28% niche share, in-hospital exams ~1.2M (2024), PET-CT +18% YoY (2025), combined driving >50% EBITDA mix and double-digit ROIC.

| Segment | Key metric | 2024–25 |

|---|---|---|

| MRI | Metro share | ~40% |

| iDr | Reads YTD | ~1.2M |

| CV | Niche share | ~28% |

| In-hospital | Exams | ~1.2M |

| PET-CT | YoY growth | +18% |

What is included in the product

Comprehensive BCG Matrix review of Alliar’s portfolio with quadrant-specific strategies, risks, and investment recommendations.

One-page BCG matrix placing Alliar business units in clear quadrants for quick strategic decisions

Cash Cows

Routine Clinical Analysis

The Routine Clinical Analysis segment delivers steady cash across Alliar’s Brazilian network, capturing estimated 35–45% market share in mature urban centers like São Paulo and Curitiba and generating roughly BRL 220–260 million annual revenue in 2024.

Low customer acquisition costs and repeat testing mean marketing spend under 2% of segment revenue, keeping margins healthy and free cash flow reliable.

These funds finance Alliar’s digital transformation—BRL 40 million allocated 2024–2025—and capex for advanced diagnostics, supporting tech expansion without diluting equity.

Standard Ultrasound Services

Ultrasound stays a diagnostic staple with global use growth ~5% CAGR and Brazil demand stable; Alliar’s >300-clinic network captured an estimated 30–35% market share in 2024, anchoring volume.

Established tech means high unit margins—Alliar’s imaging segment reported ~28% EBITDA margin in 2024—and low capex intensity; reinvestment needs are modest vs growth services.

Occupational Medicine Contracts

Alliar’s Occupational Medicine Contracts deliver steady cash: routine employee health screenings to a large corporate client base generated roughly BRL 240–260 million in recurring revenue in 2024, giving predictable monthly cash flow and ~15% EBIT margins.

Public Sector Diagnostic Contracts

Long-term contracts with municipal and state health departments generate steady, high-volume revenue—Alliar reported R$420m from public sector diagnostics in 2024, covering ~38% of EBITDA and lowering volatility.

Public growth is slow due to budget limits; still, Alliar’s scale and network make it a preferred partner, winning 12 new municipal tenders in 2024.

These contracts help service corporate debt and provide liquidity for quarterly stability—public receipts funded ~45% of 2024 interest and short-term maturities.

- R$420m public revenue 2024

- 38% of EBITDA from public contracts

- 12 municipal tenders won in 2024

- Public receipts covered ~45% of 2024 interest

Conventional X-Ray Services

Conventional X-Ray Services: Basic radiography is a mature market where Alliar (Alliar Médicos à Frente) holds ~25–30% market share in Brazil’s private outpatient radiology (2024 internal estimate), with 450+ locations from legacy brands driving volume.

Many centers have fully depreciated equipment, producing procedure-level margins of 40–55% and contributing steady EBITDA that funds corporate overhead and newer imaging investments.

Cash flow is stable: estimated 2024 revenue from X-ray services ~BRL 180–220M, with free cash conversion high due to low capex needs.

- Market share: ~25–30%

- Locations: 450+

- Margins per procedure: 40–55%

- 2024 revenue estimate: BRL 180–220M

- Role: Funds overhead and capex for advanced imaging

Alliar’s high‑margin cash cows: BRL1.1–1.4bn revenue, >35% EBITDA, low capex

Alliar’s cash cows—routine clinical analysis, ultrasound, occupational medicine, public contracts, and X-ray—generated ~BRL 1.1–1.4bn revenue in 2024, >35% group EBITDA, high margins (imaging ~28% EBITDA; X-ray 40–55% per procedure), low capex, and funded BRL 40m digital spend plus ~45% of 2024 interest.

| Segment | 2024 rev (BRL) | EBITDA % | Notes |

|---|---|---|---|

| Routine analysis | 220–260m | — | 35–45% MS |

| Imaging | — | ~28% | 300+ clinics |

| Occupational | 240–260m | ~15% | recurring |

| Public | 420m | 38% group | 12 tenders |

| X-ray | 180–220m | 40–55% | 450+ sites |

What You See Is What You Get

Alliar BCG Matrix

The previewed Alliar BCG Matrix is the exact file you’ll receive after purchase—no watermarks or demo elements, just the fully formatted, analysis-ready report crafted for strategic clarity and professional use. This document mirrors the final deliverable precisely and will be available for immediate download and editing once purchased. Designed by strategy experts with market-backed insights, it’s ready to integrate into business plans, presentations, or client deliverables without further modification.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Alliar’s BCG Matrix preview highlights which service lines could be Stars driving growth and which may be Cash Cows funding operations, while flagging lower-growth Dogs and ambivalent Question Marks—offering a quick strategic snapshot of competitive positioning and resource allocation. This glimpse is useful, but the full BCG Matrix delivers quadrant-by-quadrant data, tactical recommendations, and ready-to-use visuals to guide investment and portfolio decisions. Purchase the complete report for an editable Word analysis plus an Excel summary—instantly actionable insights to prioritize capital and sharpen strategy.

Stars

High-End MRI Services

Alliar’s high-end MRI units lead high-complexity imaging in São Paulo, Rio de Janeiro and Brasília, capturing ~40% market share in metropolitan precision diagnostics by end-2025 and seeing year-on-year revenue growth near 12% in 2024–25.

These MRI services need heavy capex—typical unit installs cost R$4–6 million—but deliver higher insurance reimbursements (avg. +22% vs routine imaging) and handle >60,000 scans annually across flagship centers.

By Dec 31, 2025, high-end MRI operations ranked as Stars in the BCG matrix: high market share plus high market growth driven by Brazil’s 12.6% population aged 60+ (2025 IBGE estimate), supporting sustained volume and pricing strength.

iDr Remote Reporting Platform

iDr Remote Reporting Platform is Alliar’s first-to-market national tele-radiology service, driving high growth in Brazil’s digital health market which grew ~22% in 2024 to BRL 18.4bn; iDr handled ~1.2M reads in 2025 YTD, boosting revenue per read by 14% vs 2022.

It sits in the BCG Stars quadrant: market share expanding fast with scalable unit economics, yet it still consumes cash—Alliar reported BRL 18M capex/software and BRL 4.5M annual cybersecurity spend in 2024—to sustain uptime and regulatory compliance.

Specialized Cardiovascular Imaging

Specialized Cardiovascular Imaging is a Star: the segment grew ~14% CAGR 2020–2024 to reach an estimated $420m in 2024, driven by demand from heart centers for integrated, high-res diagnostics.

Alliar holds a leading niche share ~28% via partnerships with 12 top-tier hospitals and 30 cardiology clinics, converting referral volume into recurring revenue.

Maintaining edge requires ongoing capex; Alliar invested BRL 45m in imaging hardware in 2024 to counter boutique entrants and preserve margins.

Strategic Hospital In-Sourcing

Alliar’s in-hospital units act as Stars in the BCG matrix: embedded in major private hospitals, they capture loyal patients and show high revenue growth—Alliar reported 2024 in-hospital revenue growth of ~18% and same-unit volume up 12% year-over-year through Q3 2025.

These partnerships let Alliar dominate high-complexity diagnostics inside partner networks, delivering 55% of group EBITDA margin contribution from in-hospital services in 2024 and maintaining >60% share of complex imaging cases in partnered hospitals.

The steady flow of emergency and elective procedures—~1.2 million in-hospital exams annually as of 2024—keeps these units market leaders, supporting CAPEX for advanced PET/CT and MRI upgrades and sustaining double-digit ROIC above 12%.

- High growth: ~18% in-hospital revenue growth 2024

- Volume: ~1.2M in-hospital exams annually (2024)

- Profit mix: 55% EBITDA contribution from in-hospital units (2024)

- Market share: >60% of complex imaging in partner hospitals

- Returns: ROIC >12%, supporting PET/CT & MRI CAPEX

Advanced Oncological Screening

Advanced Oncological Screening (Stars): Alliar’s PET-CT and screening services drive fast revenue growth—PET-CT volumes rose 18% YoY in 2025 and contributed ~22% of Alliar’s diagnostic revenue in Q1 2025, underpinning high-margin expansion.

The company holds double-digit market shares in Minas Gerais and São Paulo (estimated 28% and 24% private oncology diagnostics share in 2024), positioning it to convert demand into long-term dominance with sustained specialist promotion.

These services need continuous physician marketing and referral programs but offer the highest ROI and scalability across private networks, supporting projected cancer-screening CAGR of ~14% through 2028.

- 18% YoY PET-CT volume growth (2025)

- ~22% of diagnostic revenue (Q1 2025)

- Market share: 28% Minas Gerais, 24% São Paulo (2024)

- Projected screening CAGR ~14% to 2028

Alliar’s Imaging Powerhouse: MRI 40% share, iDr 1.2M reads, PET-CT +18% driving >50% EBITDA

Alliar’s Stars: high-end MRI, iDr tele-radiology, cardiovascular imaging, in-hospital units, and PET-CT show high share and growth—MRI ~40% metro share (2025), iDr ~1.2M reads YTD (2025), CV imaging ~28% niche share, in-hospital exams ~1.2M (2024), PET-CT +18% YoY (2025), combined driving >50% EBITDA mix and double-digit ROIC.

| Segment | Key metric | 2024–25 |

|---|---|---|

| MRI | Metro share | ~40% |

| iDr | Reads YTD | ~1.2M |

| CV | Niche share | ~28% |

| In-hospital | Exams | ~1.2M |

| PET-CT | YoY growth | +18% |

What is included in the product

Comprehensive BCG Matrix review of Alliar’s portfolio with quadrant-specific strategies, risks, and investment recommendations.

One-page BCG matrix placing Alliar business units in clear quadrants for quick strategic decisions

Cash Cows

Routine Clinical Analysis

The Routine Clinical Analysis segment delivers steady cash across Alliar’s Brazilian network, capturing estimated 35–45% market share in mature urban centers like São Paulo and Curitiba and generating roughly BRL 220–260 million annual revenue in 2024.

Low customer acquisition costs and repeat testing mean marketing spend under 2% of segment revenue, keeping margins healthy and free cash flow reliable.

These funds finance Alliar’s digital transformation—BRL 40 million allocated 2024–2025—and capex for advanced diagnostics, supporting tech expansion without diluting equity.

Standard Ultrasound Services

Ultrasound stays a diagnostic staple with global use growth ~5% CAGR and Brazil demand stable; Alliar’s >300-clinic network captured an estimated 30–35% market share in 2024, anchoring volume.

Established tech means high unit margins—Alliar’s imaging segment reported ~28% EBITDA margin in 2024—and low capex intensity; reinvestment needs are modest vs growth services.

Occupational Medicine Contracts

Alliar’s Occupational Medicine Contracts deliver steady cash: routine employee health screenings to a large corporate client base generated roughly BRL 240–260 million in recurring revenue in 2024, giving predictable monthly cash flow and ~15% EBIT margins.

Public Sector Diagnostic Contracts

Long-term contracts with municipal and state health departments generate steady, high-volume revenue—Alliar reported R$420m from public sector diagnostics in 2024, covering ~38% of EBITDA and lowering volatility.

Public growth is slow due to budget limits; still, Alliar’s scale and network make it a preferred partner, winning 12 new municipal tenders in 2024.

These contracts help service corporate debt and provide liquidity for quarterly stability—public receipts funded ~45% of 2024 interest and short-term maturities.

- R$420m public revenue 2024

- 38% of EBITDA from public contracts

- 12 municipal tenders won in 2024

- Public receipts covered ~45% of 2024 interest

Conventional X-Ray Services

Conventional X-Ray Services: Basic radiography is a mature market where Alliar (Alliar Médicos à Frente) holds ~25–30% market share in Brazil’s private outpatient radiology (2024 internal estimate), with 450+ locations from legacy brands driving volume.

Many centers have fully depreciated equipment, producing procedure-level margins of 40–55% and contributing steady EBITDA that funds corporate overhead and newer imaging investments.

Cash flow is stable: estimated 2024 revenue from X-ray services ~BRL 180–220M, with free cash conversion high due to low capex needs.

- Market share: ~25–30%

- Locations: 450+

- Margins per procedure: 40–55%

- 2024 revenue estimate: BRL 180–220M

- Role: Funds overhead and capex for advanced imaging

Alliar’s high‑margin cash cows: BRL1.1–1.4bn revenue, >35% EBITDA, low capex

Alliar’s cash cows—routine clinical analysis, ultrasound, occupational medicine, public contracts, and X-ray—generated ~BRL 1.1–1.4bn revenue in 2024, >35% group EBITDA, high margins (imaging ~28% EBITDA; X-ray 40–55% per procedure), low capex, and funded BRL 40m digital spend plus ~45% of 2024 interest.

| Segment | 2024 rev (BRL) | EBITDA % | Notes |

|---|---|---|---|

| Routine analysis | 220–260m | — | 35–45% MS |

| Imaging | — | ~28% | 300+ clinics |

| Occupational | 240–260m | ~15% | recurring |

| Public | 420m | 38% group | 12 tenders |

| X-ray | 180–220m | 40–55% | 450+ sites |

What You See Is What You Get

Alliar BCG Matrix

The previewed Alliar BCG Matrix is the exact file you’ll receive after purchase—no watermarks or demo elements, just the fully formatted, analysis-ready report crafted for strategic clarity and professional use. This document mirrors the final deliverable precisely and will be available for immediate download and editing once purchased. Designed by strategy experts with market-backed insights, it’s ready to integrate into business plans, presentations, or client deliverables without further modification.