Allison PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological advances are reshaping Allison’s strategic outlook—our PESTLE Analysis translates these external forces into actionable insights you can deploy today; purchase the full report for a comprehensive, ready-to-use breakdown that saves research time and strengthens investment or strategic decisions.

Political factors

Defense spending and geopolitical tensions

Rising global defense budgets — up about 4.3% in 2024 and projected +3.8% in 2025 per SIPRI — have boosted demand for Allison’s tracked and wheeled defense transmissions, supporting roughly 12–18% revenue growth in its defense segment in 2024. Heightened Europe–Asia tensions have spurred multi-year procurement contracts, and government-funded programs now represent a more stable, less cyclical revenue stream, accounting for an estimated 20–25% of Allison’s order backlog.

Trade policies and international tariffs

As a major exporter with plants in the US, Mexico and Europe, Allison Transmission is exposed to trade shifts and tariffs; after 2023 US-Mexico-Canada trade flows, Mexico accounted for about 20–25% of North American light/medium vehicle parts trade, altering sourcing costs. Changes in US tariffs or renewed steel/semiconductor export controls could raise input costs and reduce margins on medium-/heavy-duty units sold internationally. Monitoring tariffs and trade agreements is vital to protect FY2024–25 margins amid intensifying global competition.

Government subsidies for electrification

U.S. policies like the 2022 Inflation Reduction Act provide tax credits and grants that lower total cost of ownership for EV drivetrains, accelerating fleet electrification and boosting demand for Allison eGen Power; federal EV incentives reached an estimated $7–10k per vehicle in 2024, lifting fleet EV orders by ~18% year-over-year.

Subsidies and infrastructure grants directly speed transition from automatic transmissions to e-axles, with EPA/DOE programs allocating $3.5B+ to heavy-duty electrification through 2025, improving near-term sales visibility for Allison.

Political shifts in 2025 affecting green energy budgets could change Allison’s R&D ROI: a 10% funding cut would extend payback on electrification R&D by an estimated 12–18%, while sustained funding growth of 15% would shorten ROI timelines and increase projected eGen revenue share to 25% by 2028.

Infrastructure investment legislation

Federal and state infrastructure packages — including the 2021 Bipartisan Infrastructure Law and 2024-25 regional allocations totaling over $300 billion for roads, bridges, and waste management — boost demand for vocational vehicles like dump trucks, concrete mixers, and refuse collectors, where Allison holds market-leading transmission share.

Sustained political commitment to domestic infrastructure modernization is a primary driver for Allison's North American segment, linking public capex to volume growth and supporting aftermarket revenue and parts sales.

- 2024 US federal infrastructure funding >$110B for roads/bridges

- Allison strong share in vocational transmissions — direct volume upside

- Municipal services capex drives recurring aftermarket parts

Regulatory pressure on internal combustion

Political mandates phasing out internal combustion in urban centers push Allison to pivot toward hybrid and zero-emission transmissions; EU city bans and US California rules aim for 2030–2040 timelines, shrinking ICE urban fleets by an estimated 20–40% by 2035.

Traditional transmissions still drive ~60% of Allison’s drivetrain revenue, but tightening municipal regs in Europe and parts of North America accelerate scaling of electric and hybrid portfolios, risking legacy sales decline while opening EV transmission market share opportunities.

- EU/CA urban ICE phase-out timelines: 2030–2040

- Projected urban ICE fleet decline: 20–40% by 2035

- Allison revenue from traditional transmissions: ~60%

- Opportunity: capture growing hybrid/EV commercial vehicle demand

Policy-Driven Defense & EV Tailwinds: Stable Contracts, Aftermarket Growth, and Margin Shifts

Political support for defense, infrastructure, and electrification (SIPRI: +4.3% defense spend 2024; EPA/DOE heavy-duty EV funding $3.5B+ to 2025) increases stable contract wins, aftermarket demand, and eGen adoption, while tariffs, export controls, and urban ICE phase-outs (2030–2040) create both margin risks and accelerated EV revenue opportunity.

| Metric | Value |

|---|---|

| Defense spend growth 2024 | +4.3% |

| Heavy-duty EV funding | $3.5B+ |

| Allison legacy revenue | ~60% |

What is included in the product

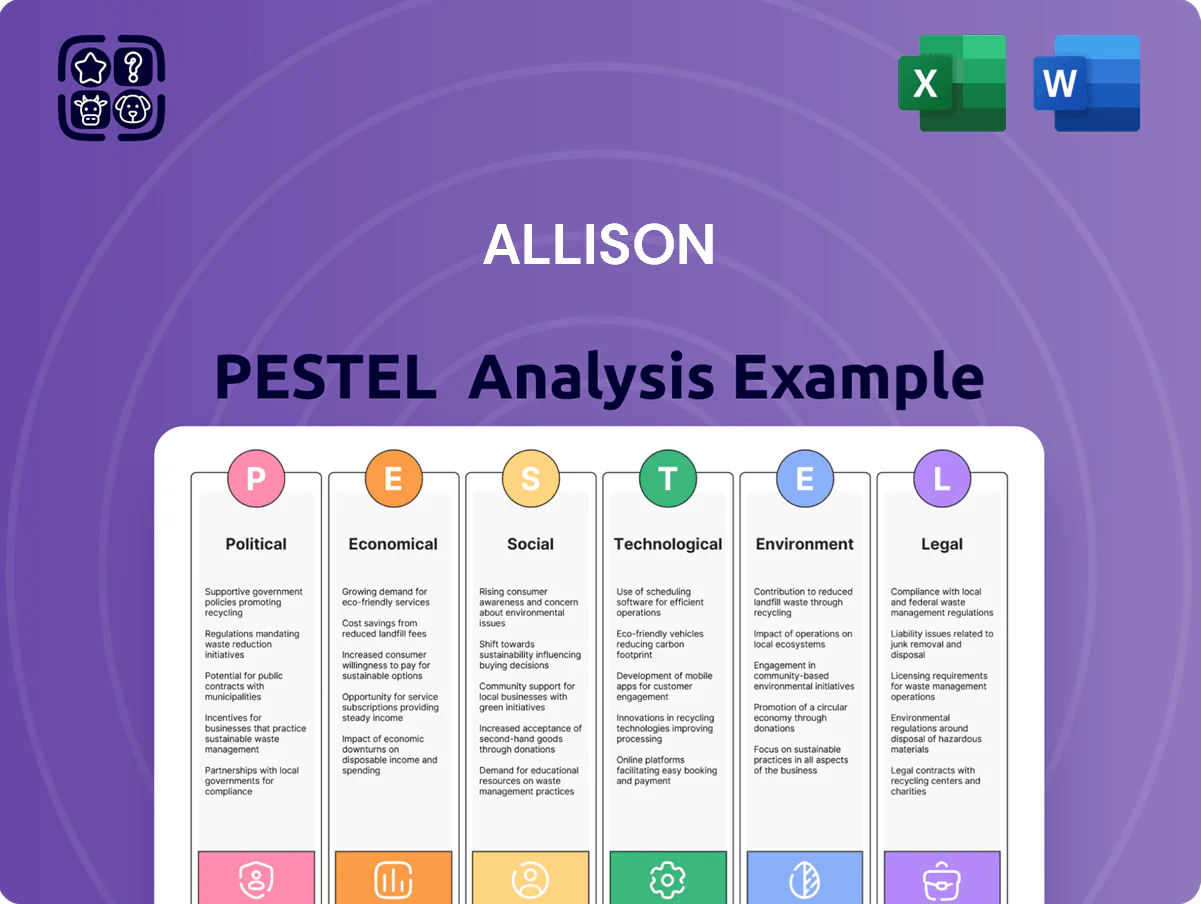

Explores how external macro-environmental factors uniquely affect Allison across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight threats and opportunities.

Provides a clean, visually segmented PESTLE summary that’s easily dropped into presentations or shared across teams, with editable notes for region- or business-specific context to streamline planning and risk discussions.

Economic factors

Global supply chain stability

The cost and availability of specialized components and raw materials like steel and aluminum drove Allison Transmission’s material costs up to about 8–12% in 2024 versus 2021 baseline; margins remain sensitive to commodity swings. By late 2025 global disruptions had largely eased, but 2024 Port of Los Angeles congestion spikes and regional semiconductor shortages still created localized bottlenecks affecting multi-week delivery timelines for large vehicle OEMs. Managing supplier relationships and maintaining higher inventory—Allison targeted ~10–15% buffer parts coverage in 2024—remains a critical economic priority to preserve its industry-leading lead times and protect margins.

Interest rate environment and capital costs

Fluctuating interest rates alter fleet owners' and construction firms' financing costs, with US 10-year Treasury yields falling from ~4.5% in mid-2023 to ~3.8% by end-2024, easing borrowing and supporting renewed vehicle purchases that can boost Allison's order book.

Higher borrowing costs historically delay fleet replacement—OEM demand elasticity rose after the 2022–23 rate spike—while the stabilizing/declining rate backdrop in 2025 is expected to encourage capex among fleet operators.

Allison's capital allocation—including its FY2024 $100–200m share repurchase authorization and targeted 5–7% revenue reinvestment into R&D—is sensitive to cost of capital; lower rates improve cash returns and funding for innovation.

Fuel price volatility

The operational cost of diesel—US average diesel retail price rose to about $4.00/gal in 2024 after peaking near $5.00/gal in 2022—boosts demand for Allison’s fuel-efficient automatics and hybrid systems by lowering fleet TCO. High fuel prices accelerate uptake of FuelSense 2.0 and electric propulsion as fleets seek 5–15% fuel savings reported in trials. Conversely, sustained low diesel prices can extend life of older vehicles, delaying retrofit or replacement cycles.

Emerging market growth rates

Economic expansion in India and Southeast Asia—GDP growth of 6–7% in India (2024 IMF) and 4–5% regional forecasts—boosts demand as fleets shift from manual to automatic transmissions, creating sizable addressable markets for Allison.

Infrastructure spending in ASEAN (est. $1.1 trillion 2024–2026 pipelines) and rising freight activity increase demand for high-performance commercial vehicles, favoring Allison’s transmission systems.

Market penetration hinges on localized economic stability and fleet purchasing power; average fleet CAPEX growth of ~8% in Asia Pacific (2023–24) signals opportunity but variance across markets affects rollout speed.

- India GDP ~6–7% (2024 IMF)

- ASEAN growth ~4–5% (2024 forecasts)

- ASEAN infrastructure pipeline ~$1.1T (2024–26)

- Asia Pacific fleet CAPEX +~8% (2023–24)

Currency exchange rate fluctuations

With roughly 60% of Allison Transmission’s 2024 revenue generated outside the United States, swings in the U.S. dollar create transaction and translation exposures that can compress reported sales and margins when the dollar strengthens and inflate them when it weakens.

Currency volatility also alters global price competitiveness versus European and Asian driveline manufacturers; a 10% USD appreciation versus EUR or CNY can materially erode export margins and market share.

Allison routinely uses hedging instruments and localized pricing adjustments—FX hedges covered about 45% of forecasted net exposure in 2024—to stabilize earnings and protect margins.

- ~60% 2024 revenue outside US

- 10% USD shift can impact margins/competitiveness materially

- ~45% of net FX exposure hedged in 2024

Allison weathers 8–12% commodity rise with 10–15% inventory, strong global revenue & hedges

Commodity-driven input costs rose ~8–12% (2021–24), Allison held ~10–15% buffer inventory in 2024; US 10y fell ~4.5% to ~3.8% (mid-2023 to end-2024) easing fleet financing; diesel averaged ~$4.00/gal in 2024 vs $5.00/gal peak 2022, supporting FuelSense uptake; ~60% revenue ex-US in 2024, ~45% FX hedge coverage.

| Metric | Value (2024) |

|---|---|

| Commodity cost change | +8–12% |

| Inventory buffer | 10–15% |

| US 10y yield | ~3.8% |

| Diesel retail | $4.00/gal |

| Revenue ex-US | ~60% |

| FX hedge coverage | ~45% |

What You See Is What You Get

Allison PESTLE Analysis

The preview shown here is the exact Allison PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or reporting.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological advances are reshaping Allison’s strategic outlook—our PESTLE Analysis translates these external forces into actionable insights you can deploy today; purchase the full report for a comprehensive, ready-to-use breakdown that saves research time and strengthens investment or strategic decisions.

Political factors

Defense spending and geopolitical tensions

Rising global defense budgets — up about 4.3% in 2024 and projected +3.8% in 2025 per SIPRI — have boosted demand for Allison’s tracked and wheeled defense transmissions, supporting roughly 12–18% revenue growth in its defense segment in 2024. Heightened Europe–Asia tensions have spurred multi-year procurement contracts, and government-funded programs now represent a more stable, less cyclical revenue stream, accounting for an estimated 20–25% of Allison’s order backlog.

Trade policies and international tariffs

As a major exporter with plants in the US, Mexico and Europe, Allison Transmission is exposed to trade shifts and tariffs; after 2023 US-Mexico-Canada trade flows, Mexico accounted for about 20–25% of North American light/medium vehicle parts trade, altering sourcing costs. Changes in US tariffs or renewed steel/semiconductor export controls could raise input costs and reduce margins on medium-/heavy-duty units sold internationally. Monitoring tariffs and trade agreements is vital to protect FY2024–25 margins amid intensifying global competition.

Government subsidies for electrification

U.S. policies like the 2022 Inflation Reduction Act provide tax credits and grants that lower total cost of ownership for EV drivetrains, accelerating fleet electrification and boosting demand for Allison eGen Power; federal EV incentives reached an estimated $7–10k per vehicle in 2024, lifting fleet EV orders by ~18% year-over-year.

Subsidies and infrastructure grants directly speed transition from automatic transmissions to e-axles, with EPA/DOE programs allocating $3.5B+ to heavy-duty electrification through 2025, improving near-term sales visibility for Allison.

Political shifts in 2025 affecting green energy budgets could change Allison’s R&D ROI: a 10% funding cut would extend payback on electrification R&D by an estimated 12–18%, while sustained funding growth of 15% would shorten ROI timelines and increase projected eGen revenue share to 25% by 2028.

Infrastructure investment legislation

Federal and state infrastructure packages — including the 2021 Bipartisan Infrastructure Law and 2024-25 regional allocations totaling over $300 billion for roads, bridges, and waste management — boost demand for vocational vehicles like dump trucks, concrete mixers, and refuse collectors, where Allison holds market-leading transmission share.

Sustained political commitment to domestic infrastructure modernization is a primary driver for Allison's North American segment, linking public capex to volume growth and supporting aftermarket revenue and parts sales.

- 2024 US federal infrastructure funding >$110B for roads/bridges

- Allison strong share in vocational transmissions — direct volume upside

- Municipal services capex drives recurring aftermarket parts

Regulatory pressure on internal combustion

Political mandates phasing out internal combustion in urban centers push Allison to pivot toward hybrid and zero-emission transmissions; EU city bans and US California rules aim for 2030–2040 timelines, shrinking ICE urban fleets by an estimated 20–40% by 2035.

Traditional transmissions still drive ~60% of Allison’s drivetrain revenue, but tightening municipal regs in Europe and parts of North America accelerate scaling of electric and hybrid portfolios, risking legacy sales decline while opening EV transmission market share opportunities.

- EU/CA urban ICE phase-out timelines: 2030–2040

- Projected urban ICE fleet decline: 20–40% by 2035

- Allison revenue from traditional transmissions: ~60%

- Opportunity: capture growing hybrid/EV commercial vehicle demand

Policy-Driven Defense & EV Tailwinds: Stable Contracts, Aftermarket Growth, and Margin Shifts

Political support for defense, infrastructure, and electrification (SIPRI: +4.3% defense spend 2024; EPA/DOE heavy-duty EV funding $3.5B+ to 2025) increases stable contract wins, aftermarket demand, and eGen adoption, while tariffs, export controls, and urban ICE phase-outs (2030–2040) create both margin risks and accelerated EV revenue opportunity.

| Metric | Value |

|---|---|

| Defense spend growth 2024 | +4.3% |

| Heavy-duty EV funding | $3.5B+ |

| Allison legacy revenue | ~60% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Allison across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight threats and opportunities.

Provides a clean, visually segmented PESTLE summary that’s easily dropped into presentations or shared across teams, with editable notes for region- or business-specific context to streamline planning and risk discussions.

Economic factors

Global supply chain stability

The cost and availability of specialized components and raw materials like steel and aluminum drove Allison Transmission’s material costs up to about 8–12% in 2024 versus 2021 baseline; margins remain sensitive to commodity swings. By late 2025 global disruptions had largely eased, but 2024 Port of Los Angeles congestion spikes and regional semiconductor shortages still created localized bottlenecks affecting multi-week delivery timelines for large vehicle OEMs. Managing supplier relationships and maintaining higher inventory—Allison targeted ~10–15% buffer parts coverage in 2024—remains a critical economic priority to preserve its industry-leading lead times and protect margins.

Interest rate environment and capital costs

Fluctuating interest rates alter fleet owners' and construction firms' financing costs, with US 10-year Treasury yields falling from ~4.5% in mid-2023 to ~3.8% by end-2024, easing borrowing and supporting renewed vehicle purchases that can boost Allison's order book.

Higher borrowing costs historically delay fleet replacement—OEM demand elasticity rose after the 2022–23 rate spike—while the stabilizing/declining rate backdrop in 2025 is expected to encourage capex among fleet operators.

Allison's capital allocation—including its FY2024 $100–200m share repurchase authorization and targeted 5–7% revenue reinvestment into R&D—is sensitive to cost of capital; lower rates improve cash returns and funding for innovation.

Fuel price volatility

The operational cost of diesel—US average diesel retail price rose to about $4.00/gal in 2024 after peaking near $5.00/gal in 2022—boosts demand for Allison’s fuel-efficient automatics and hybrid systems by lowering fleet TCO. High fuel prices accelerate uptake of FuelSense 2.0 and electric propulsion as fleets seek 5–15% fuel savings reported in trials. Conversely, sustained low diesel prices can extend life of older vehicles, delaying retrofit or replacement cycles.

Emerging market growth rates

Economic expansion in India and Southeast Asia—GDP growth of 6–7% in India (2024 IMF) and 4–5% regional forecasts—boosts demand as fleets shift from manual to automatic transmissions, creating sizable addressable markets for Allison.

Infrastructure spending in ASEAN (est. $1.1 trillion 2024–2026 pipelines) and rising freight activity increase demand for high-performance commercial vehicles, favoring Allison’s transmission systems.

Market penetration hinges on localized economic stability and fleet purchasing power; average fleet CAPEX growth of ~8% in Asia Pacific (2023–24) signals opportunity but variance across markets affects rollout speed.

- India GDP ~6–7% (2024 IMF)

- ASEAN growth ~4–5% (2024 forecasts)

- ASEAN infrastructure pipeline ~$1.1T (2024–26)

- Asia Pacific fleet CAPEX +~8% (2023–24)

Currency exchange rate fluctuations

With roughly 60% of Allison Transmission’s 2024 revenue generated outside the United States, swings in the U.S. dollar create transaction and translation exposures that can compress reported sales and margins when the dollar strengthens and inflate them when it weakens.

Currency volatility also alters global price competitiveness versus European and Asian driveline manufacturers; a 10% USD appreciation versus EUR or CNY can materially erode export margins and market share.

Allison routinely uses hedging instruments and localized pricing adjustments—FX hedges covered about 45% of forecasted net exposure in 2024—to stabilize earnings and protect margins.

- ~60% 2024 revenue outside US

- 10% USD shift can impact margins/competitiveness materially

- ~45% of net FX exposure hedged in 2024

Allison weathers 8–12% commodity rise with 10–15% inventory, strong global revenue & hedges

Commodity-driven input costs rose ~8–12% (2021–24), Allison held ~10–15% buffer inventory in 2024; US 10y fell ~4.5% to ~3.8% (mid-2023 to end-2024) easing fleet financing; diesel averaged ~$4.00/gal in 2024 vs $5.00/gal peak 2022, supporting FuelSense uptake; ~60% revenue ex-US in 2024, ~45% FX hedge coverage.

| Metric | Value (2024) |

|---|---|

| Commodity cost change | +8–12% |

| Inventory buffer | 10–15% |

| US 10y yield | ~3.8% |

| Diesel retail | $4.00/gal |

| Revenue ex-US | ~60% |

| FX hedge coverage | ~45% |

What You See Is What You Get

Allison PESTLE Analysis

The preview shown here is the exact Allison PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or reporting.