Alm. Brand Business Model Canvas

Alm. Brand Business Model Canvas: Plug-and-Play Strategic Blueprint

Unlock the full strategic blueprint behind Alm. Brand’s business model — this concise Business Model Canvas exposes how the firm creates value, manages risk, and monetizes customer relationships; perfect for investors, consultants, and founders seeking actionable, plug-and-play insights. Download the complete Word/Excel files for a section-by-section breakdown, ready for benchmarking, presentations, or strategic planning.

Partnerships

Sydbank Strategic Alliance

The Sydbank alliance remains a cornerstone of Alm. Brand’s distribution after the 2020 banking divestment, driving ~22% of new motor and home insurance sales in 2024 and accessing 1.1m bank customers via 120 branches and Sydbank’s digital channels.

Reinsurance Providers

Engagement with global reinsurance firms like Munich Re and Swiss Re lets Alm. Brand cede portions of catastrophe and large-loss exposure, keeping solvency ratio targets (Solvency II SCR) above regulatory minimums—Alm. Brand reported a 2024 solvency ratio near 200%, aided by reinsurance placements covering peak risks. These partners cap single-event losses, smoothing claims volatility in Denmark and protecting the company’s ~DKK 12.5bn capital base.

Automotive and Repair Networks

Collaborations with car dealerships and certified repair shops are central to Alm. Brand’s motor insurance, cutting average repair cycle time by ~25% and reducing claim costs—Alm. Brand reported a 12% lower cost-per-claim in motor lines in 2024 versus market peers. These partners also generate referrals: dealer-originated policies accounted for about 18% of new motor business in 2024, speeding customer acquisition and ensuring quality, trackable repairs.

Independent Insurance Brokers

Independent brokers are vital intermediaries for Alm. Brand in large corporate and specialized commercial lines, tailoring complex solutions and driving 28% of corporate new business in 2024, helping secure higher-margin contracts.

Maintaining broker relationships reduced acquisition cost by 12% in 2024 and is key to competing for accounts >DKK 5m.

- Brokers drive 28% of corporate new business (2024)

- Broker-led deals often exceed DKK 5m

- Strong broker ties cut acquisition costs by ~12% (2024)

IT and Fintech Vendors

Strategic alliances with IT and fintech vendors drive Alm. Brand’s digital overhaul, replacing legacy systems and cutting platform costs—Alm. Brand reported a 22% rise in digital policy sales in 2024 after platform upgrades.

Vendors deliver cloud infrastructure, advanced analytics, and mobile UIs to speed claims handling and personalization; partnering with insurtechs reduced claim cycle time by ~30% in 2024.

- 22% increase in digital policy sales (2024)

- ~30% faster claim cycles post-integration (2024)

- Cloud migration lowers ops cost, boosts scalability

Partnerships drive growth: Sydbank 22% sales, reinsurance protects DKK12.5bn capital

Sydbank partnership drove ~22% of new motor/home sales in 2024, accessing 1.1m customers; reinsurance (Munich Re, Swiss Re) kept Solvency II ratio near 200% protecting a ~DKK 12.5bn capital base; brokers and dealers supplied 28% of corporate and 18% of motor new business, cutting acquisition costs ~12% and reducing repair/claim cycles 25–30%.

| Partner | 2024 KPI | Impact |

|---|---|---|

| Sydbank | 22% new sales; 1.1m customers | Distribution reach |

| Reinsurers | Solvency ~200%; DKK 12.5bn capital | Risk transfer |

| Brokers/Dealers | 28% corporate; 18% motor | Acq cost −12% |

| IT/Insurtech | Digital sales +22%; claim cycles −30% | Efficiency |

What is included in the product

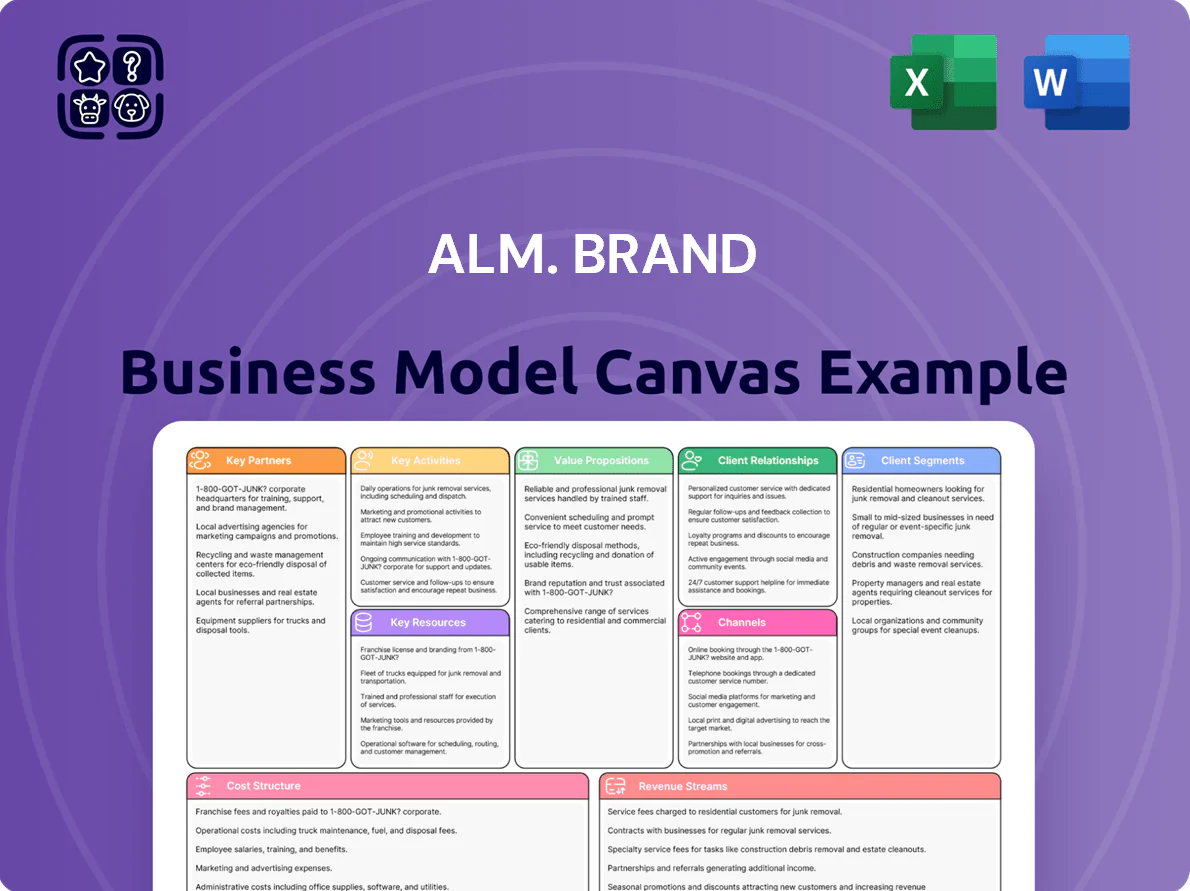

A concise, pre-written Business Model Canvas for Alm. Brand outlining customer segments, channels, value propositions, revenue streams, key resources and partners, cost structure, and customer relationships aligned with the company’s insurance and financial-services operations.

High-level view of Alm. Brand’s business model with editable cells to quickly map insurance products, distribution channels, and risk management—ideal for boardrooms or teams needing a concise, shareable snapshot.

Activities

Risk Underwriting and Pricing

Risk underwriting and pricing centers on assessing retail and commercial risks and setting premiums to keep Alm. Brand profitable and competitive; in 2024 the group reported a combined ratio of ~92.5%, underscoring disciplined pricing. Using actuarial models fed by claims, telematics, and commercial exposure data, underwriters target loss ratios near 70–75% for P&C lines to sustain the 2024 return on equity of ~10.8%.

Claims Processing and Settlement

Efficient claims handling is central: Alm. Brand automates ~60% of non-complex claims (2024), cuts average settlement time to 4.2 days, and deploys specialist teams for complex losses, improving NPS and lowering loss adjustment expense to 8.1% of incurred claims in 2024; fast, fair settlements are marketed as a core differentiator in the Danish non-life market.

Product Innovation and Development

Alm. Brand continuously refines its product portfolio to match shifting customer needs and rising risks like cyber threats, launching specialized packages for households, SMEs and large industry; in 2024 Alm. Brand reported a 12% growth in commercial cyber premiums and a 4.5% rise in household policies, keeping its value proposition aligned with tech and economic changes.

Multi-channel Distribution Management

Managing Alm. Brand’s multi-channel distribution—digital portals, call centers, brokers, and in-person advisors—keeps acquisition efficient and consistency high; in 2024 Alm. Brand reported 42% of new retail policies sold online and a 28% rise in commercial advisory revenues from hybrid sales models.

- Balance online efficiency vs. advisor-led complexity

- Coordinate channels to protect NPS and brand consistency

- Use hybrid sales: 42% online retail, +28% commercial advisory revenue (2024)

Asset and Capital Management

Managing Alm. Brand’s ~DKK 33.5bn investment portfolio (2024 year-end) turns premium inflows into secondary revenue while targeting risk-adjusted returns within Danish and EU rules.

Capital management focuses on optimizing reserves, meeting Solvency II capital requirements (SCR coverage >100%) and preserving liquidity for claims and growth.

- DKK 33.5bn portfolio (YE 2024)

- Target risk-adjusted returns vs. Solvency II

- Maintain SCR coverage above 100%

Well‑rounded insurer: 92.5% combined ratio, 10.8% ROE, 60% automated claims, DKK33.5bn

Key activities: risk underwriting/pricing (combined ratio ~92.5%, target P&C loss ratio 70–75%, ROE 10.8% in 2024), claims handling (60% automated, avg settlement 4.2 days, LAE 8.1%), product development (commercial cyber +12%, household +4.5% in 2024), multi-channel distribution (42% online new retail, +28% commercial advisory), investment & capital mgmt (DKK 33.5bn portfolio, SCR >100%).

| Metric | 2024 |

|---|---|

| Combined ratio | ~92.5% |

| Target P&C loss ratio | 70–75% |

| ROE | 10.8% |

| Claims automated | ~60% |

| Avg settlement | 4.2 days |

| LAE | 8.1% |

| Cyber premium growth | +12% |

| Household growth | +4.5% |

| Online new retail | 42% |

| Commercial advisory rev | +28% |

| Investment portfolio | DKK 33.5bn |

| SCR coverage | >100% |

Full Version Awaits

Business Model Canvas

The Alm. Brand Business Model Canvas shown here is the exact document you’ll receive after purchase—not a mockup or sample—and it’s fully ready for use in your analyses and presentations.

Upon completing your order you’ll get this same file, with all sections and content included, instantly downloadable and editable in the provided formats.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Alm. Brand Business Model Canvas: Plug-and-Play Strategic Blueprint

Unlock the full strategic blueprint behind Alm. Brand’s business model — this concise Business Model Canvas exposes how the firm creates value, manages risk, and monetizes customer relationships; perfect for investors, consultants, and founders seeking actionable, plug-and-play insights. Download the complete Word/Excel files for a section-by-section breakdown, ready for benchmarking, presentations, or strategic planning.

Partnerships

Sydbank Strategic Alliance

The Sydbank alliance remains a cornerstone of Alm. Brand’s distribution after the 2020 banking divestment, driving ~22% of new motor and home insurance sales in 2024 and accessing 1.1m bank customers via 120 branches and Sydbank’s digital channels.

Reinsurance Providers

Engagement with global reinsurance firms like Munich Re and Swiss Re lets Alm. Brand cede portions of catastrophe and large-loss exposure, keeping solvency ratio targets (Solvency II SCR) above regulatory minimums—Alm. Brand reported a 2024 solvency ratio near 200%, aided by reinsurance placements covering peak risks. These partners cap single-event losses, smoothing claims volatility in Denmark and protecting the company’s ~DKK 12.5bn capital base.

Automotive and Repair Networks

Collaborations with car dealerships and certified repair shops are central to Alm. Brand’s motor insurance, cutting average repair cycle time by ~25% and reducing claim costs—Alm. Brand reported a 12% lower cost-per-claim in motor lines in 2024 versus market peers. These partners also generate referrals: dealer-originated policies accounted for about 18% of new motor business in 2024, speeding customer acquisition and ensuring quality, trackable repairs.

Independent Insurance Brokers

Independent brokers are vital intermediaries for Alm. Brand in large corporate and specialized commercial lines, tailoring complex solutions and driving 28% of corporate new business in 2024, helping secure higher-margin contracts.

Maintaining broker relationships reduced acquisition cost by 12% in 2024 and is key to competing for accounts >DKK 5m.

- Brokers drive 28% of corporate new business (2024)

- Broker-led deals often exceed DKK 5m

- Strong broker ties cut acquisition costs by ~12% (2024)

IT and Fintech Vendors

Strategic alliances with IT and fintech vendors drive Alm. Brand’s digital overhaul, replacing legacy systems and cutting platform costs—Alm. Brand reported a 22% rise in digital policy sales in 2024 after platform upgrades.

Vendors deliver cloud infrastructure, advanced analytics, and mobile UIs to speed claims handling and personalization; partnering with insurtechs reduced claim cycle time by ~30% in 2024.

- 22% increase in digital policy sales (2024)

- ~30% faster claim cycles post-integration (2024)

- Cloud migration lowers ops cost, boosts scalability

Partnerships drive growth: Sydbank 22% sales, reinsurance protects DKK12.5bn capital

Sydbank partnership drove ~22% of new motor/home sales in 2024, accessing 1.1m customers; reinsurance (Munich Re, Swiss Re) kept Solvency II ratio near 200% protecting a ~DKK 12.5bn capital base; brokers and dealers supplied 28% of corporate and 18% of motor new business, cutting acquisition costs ~12% and reducing repair/claim cycles 25–30%.

| Partner | 2024 KPI | Impact |

|---|---|---|

| Sydbank | 22% new sales; 1.1m customers | Distribution reach |

| Reinsurers | Solvency ~200%; DKK 12.5bn capital | Risk transfer |

| Brokers/Dealers | 28% corporate; 18% motor | Acq cost −12% |

| IT/Insurtech | Digital sales +22%; claim cycles −30% | Efficiency |

What is included in the product

A concise, pre-written Business Model Canvas for Alm. Brand outlining customer segments, channels, value propositions, revenue streams, key resources and partners, cost structure, and customer relationships aligned with the company’s insurance and financial-services operations.

High-level view of Alm. Brand’s business model with editable cells to quickly map insurance products, distribution channels, and risk management—ideal for boardrooms or teams needing a concise, shareable snapshot.

Activities

Risk Underwriting and Pricing

Risk underwriting and pricing centers on assessing retail and commercial risks and setting premiums to keep Alm. Brand profitable and competitive; in 2024 the group reported a combined ratio of ~92.5%, underscoring disciplined pricing. Using actuarial models fed by claims, telematics, and commercial exposure data, underwriters target loss ratios near 70–75% for P&C lines to sustain the 2024 return on equity of ~10.8%.

Claims Processing and Settlement

Efficient claims handling is central: Alm. Brand automates ~60% of non-complex claims (2024), cuts average settlement time to 4.2 days, and deploys specialist teams for complex losses, improving NPS and lowering loss adjustment expense to 8.1% of incurred claims in 2024; fast, fair settlements are marketed as a core differentiator in the Danish non-life market.

Product Innovation and Development

Alm. Brand continuously refines its product portfolio to match shifting customer needs and rising risks like cyber threats, launching specialized packages for households, SMEs and large industry; in 2024 Alm. Brand reported a 12% growth in commercial cyber premiums and a 4.5% rise in household policies, keeping its value proposition aligned with tech and economic changes.

Multi-channel Distribution Management

Managing Alm. Brand’s multi-channel distribution—digital portals, call centers, brokers, and in-person advisors—keeps acquisition efficient and consistency high; in 2024 Alm. Brand reported 42% of new retail policies sold online and a 28% rise in commercial advisory revenues from hybrid sales models.

- Balance online efficiency vs. advisor-led complexity

- Coordinate channels to protect NPS and brand consistency

- Use hybrid sales: 42% online retail, +28% commercial advisory revenue (2024)

Asset and Capital Management

Managing Alm. Brand’s ~DKK 33.5bn investment portfolio (2024 year-end) turns premium inflows into secondary revenue while targeting risk-adjusted returns within Danish and EU rules.

Capital management focuses on optimizing reserves, meeting Solvency II capital requirements (SCR coverage >100%) and preserving liquidity for claims and growth.

- DKK 33.5bn portfolio (YE 2024)

- Target risk-adjusted returns vs. Solvency II

- Maintain SCR coverage above 100%

Well‑rounded insurer: 92.5% combined ratio, 10.8% ROE, 60% automated claims, DKK33.5bn

Key activities: risk underwriting/pricing (combined ratio ~92.5%, target P&C loss ratio 70–75%, ROE 10.8% in 2024), claims handling (60% automated, avg settlement 4.2 days, LAE 8.1%), product development (commercial cyber +12%, household +4.5% in 2024), multi-channel distribution (42% online new retail, +28% commercial advisory), investment & capital mgmt (DKK 33.5bn portfolio, SCR >100%).

| Metric | 2024 |

|---|---|

| Combined ratio | ~92.5% |

| Target P&C loss ratio | 70–75% |

| ROE | 10.8% |

| Claims automated | ~60% |

| Avg settlement | 4.2 days |

| LAE | 8.1% |

| Cyber premium growth | +12% |

| Household growth | +4.5% |

| Online new retail | 42% |

| Commercial advisory rev | +28% |

| Investment portfolio | DKK 33.5bn |

| SCR coverage | >100% |

Full Version Awaits

Business Model Canvas

The Alm. Brand Business Model Canvas shown here is the exact document you’ll receive after purchase—not a mockup or sample—and it’s fully ready for use in your analyses and presentations.

Upon completing your order you’ll get this same file, with all sections and content included, instantly downloadable and editable in the provided formats.