Al Rajhi Bank Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

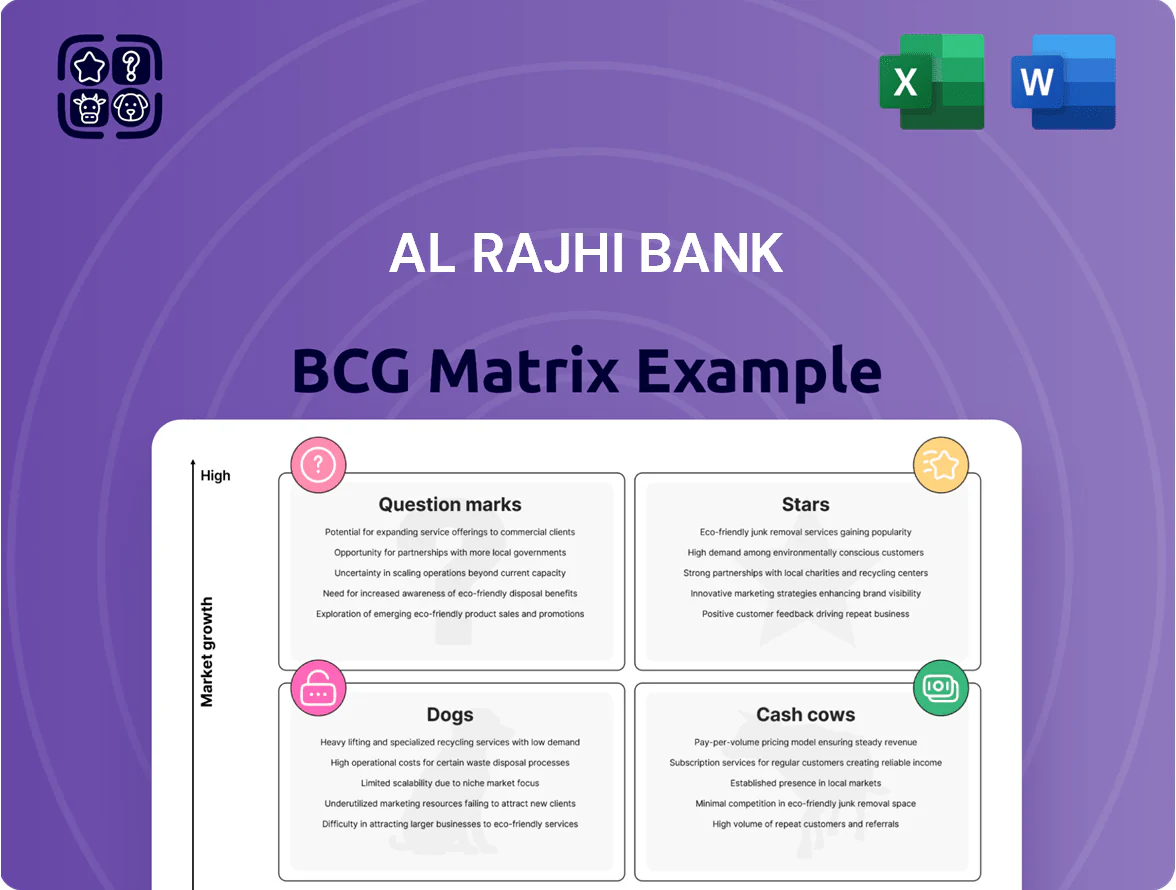

Al Rajhi Bank’s BCG Matrix preview highlights how its core retail and Islamic finance offerings perform across growth and market-share dimensions, hinting at potential Stars in consumer banking and Cash Cows in core deposit services while suggesting areas to watch for Question Marks amid digital disruption. This snapshot teases strategic priorities—resource allocation, divestment, or investment—to sharpen competitive advantage. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and ready-to-use Word and Excel deliverables to act with confidence.

Stars

Digital Banking Ecosystem and Super App

Al Rajhi Bank leads Saudi digital banking, with its mobile app serving over 8 million active users by late 2025 and capturing roughly 35% of retail digital transaction volume nationwide, driven by Vision 2030 fintech growth projections of ~20% CAGR through 2028.

To sustain this position against neobanks, the bank must keep heavy investment in UI/UX and backend scalability—expecting capital spend on digital platforms to remain a high single-digit percent of annual IT budget (~SAR 300–400m in 2025).

These digital services function as the primary acquisition channel for customers under 35, accounting for about 60% of new retail accounts in 2025 and boosting cross-sell rates by ~1.8x versus branch-led customers.

SME Financing and Development

SME lending is a star as Al Rajhi aligns with Saudi Vision 2030 diversification; by end-2025 the bank held an estimated 22% share of the Saudi SME financing market after growing SME book 28% year-on-year to SAR 34.2bn.

urpay Digital Wallet Services

urpay Digital Wallet Services is a Star: by 2025 it holds an estimated 35–40% share of Saudi Arabia’s digital payments volume, in a market growing ~20% CAGR (2020–25) as cash transactions fell to ~15% of retail payments.

The unit consumes sizable cash for marketing and R&D—Al Rajhi disclosed ~SAR 120–180m annual investment—aiming to defend share and add gig-economy features.

urpay links legacy banking with freelancers and platforms, processing millions of monthly payouts and remaining a top strategic investment for Al Rajhi.

Mortgage and Real Estate Financing

Al Rajhi remains a star in mortgages, holding ~30%+ market share in Saudi mortgage lending (2025) by volume while chasing the Ministry of Housing targets—helping fund 400k+ homes under government programs through aggressive origination.

Mortgage loans demand high capital due to long durations and high LTVs; mortgage book growth was ~12–15% YoY in 2024–2025, well above retail loans (~6–7%), signalling elevated growth before eventual steady state.

The segment consumes capital now but should become a cash cow once national housing demand stabilizes (expected by 2028–2030), converting scale into predictable net interest margins and steady fee income.

- Market share ~30%+ (2025)

- Mortgage book growth 12–15% YoY (2024–25)

- Retail loan growth ~6–7% (2024–25)

- Supports 400k+ homes in housing programs

- Transition to cash cow expected 2028–2030

ESG and Sustainable Finance Portfolios

As of late 2025, green financing and ESG-linked corporate loans are high-growth for Al Rajhi Bank, where it holds an early lead with >30% market share in Saudi Islamic green lending.

The bank is investing SAR 12–15 billion in structuring Sharia-compliant green sukuk and sustainability-linked credit facilities to meet global investor standards.

Demand is rising as Saudi corporations align with the Saudi Green Initiative and net-zero targets, boosting ESG deal flow by ~40% YoY in 2024–25 and drawing institutional capital.

- Early leader: >30% market share in Islamic green lending

- Investment: SAR 12–15bn in green sukuk and facilities

- Growth: ~40% YoY ESG deal-flow increase (2024–25)

- Benefit: attracts institutional capital and top corporates

Al Rajhi Dominates: 8M Digital Users, urpay Lead, 30%+ Mortgages, Strong SME Growth

Al Rajhi’s Stars: digital banking (8M users, ~35% retail digital volume, 2025), urpay wallet (35–40% payments share, SAR120–180m annual spend), mortgages (~30%+ market share, mortgage book SAR34.2bn, 12–15% YoY), SME lending (22% SME market, SAR34.2bn).

| Unit | Metric (2025) |

|---|---|

| Digital | 8M users; 35% vol |

| urpay | 35–40% payments; SAR120–180m spend |

| Mortgages | 30%+ share; SAR34.2bn |

| SME | 22% share; 28% YoY |

What is included in the product

BCG Matrix of Al Rajhi Bank: strategic placement of business units into Stars, Cash Cows, Question Marks, and Dogs with tailored investment guidance.

One-page overview placing each Al Rajhi Bank business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

Retail Deposit Base

Al Rajhi Bank holds the largest retail deposit base in Saudi Arabia—SAR 428 billion in customer deposits as of FY 2024—providing a low‑cost funding source typical of a cash cow.

With dominant market share in basic savings and low sector growth, these deposits produce strong net interest margin cash flow with minimal marketing spend.

The resulting liquidity funds stars and question marks across the portfolio and underpins dividend capacity and balance‑sheet stability.

Personal Islamic Financing

Personal Islamic financing is a mature, low-growth cash cow for Al Rajhi Bank; as of FY2024 the bank held about 30–35% domestic market share in retail Sharia loans while segment growth slowed to ~3–4% year-on-year, signaling market saturation.

Profit margins remain strong—net finance income contribution from retail Sharia products stayed around 28% of total operating income in 2024—thanks to efficient servicing, brand loyalty, and limited incremental capex needs versus digital offerings.

These loans need minimal new infrastructure or marketing spend; steady monthly repayments generated roughly SAR 12–15 billion in free cash flow in FY2024, funding operations and supporting dividends and buybacks.

Corporate Banking Services

Al Rajhi Bank’s corporate banking services—traditional lending and cash management for large enterprises—remain a cash cow, holding high market share in Saudi Arabia’s corporate credit market (about 18% market share in 2024 corporate loans to large corporates, SAMA data). The segment grows modestly (~3–5% annual loan book expansion) but delivers predictable net interest income and stable fees. Deep ties with Saudi conglomerates drive low churn and strong deposit stickiness. It reliably funds the bank’s higher-risk innovation and investment activities.

Treasury and Liquidity Management

Treasury and Liquidity Management holds a large portfolio of high-quality liquid assets and Sharia-compliant sukuk yielding steady returns; as of 2025 Al Rajhi reported SAR 200+ billion in liquid assets, supporting net interest income stability. The unit operates in a mature Saudi market where Al Rajhi’s scale secures dominant market liquidity, so growth is low but cash generation is high. It stabilizes the balance sheet during interest-rate swings and funds lending needs.

- SAR 200+ billion liquid assets (2025)

- High-quality sukuk and cash equivalents

- Low growth, surplus cash generator

- Key stabilizer vs. rate volatility

Brokerage and Asset Management

Al Rajhi Capital leads Saudi equity brokerage with ~28% market share in 2024 and average daily trading volumes >SAR 6.5bn, generating fee income that exceeded SAR 420m in 2024; steady Tadawul growth (~6% CAGR 2020–24) limits rapid top-line expansion but sustains high margins.

Brokerage/AM needs low capex versus lending; operating cash flow funded SAR 200–300m of digital wealth tech investments in 2024, recycling fees into product digitization and platform scale-up.

- ~28% local equity market share (2024)

- Avg daily trading volume >SAR 6.5bn (2024)

- Fee income ~SAR 420m (2024)

- Reinvested SAR 200–300m into digital wealth (2024)

Al Rajhi’s cash cows: deposits, Islamic retail loans, corporate lending & SAR200bn+ treasuries

Al Rajhi’s cash cows—retail deposits (SAR 428bn FY2024), personal Islamic financing (30–35% market share, ~SAR 12–15bn FCF FY2024), corporate lending (≈18% market share, 3–5% growth) and treasury/liquid assets (SAR 200+bn 2025)—generate steady net interest income and fees, fund dividends, buybacks, and invest in digital growth.

| Segment | Key metric | 2024/25 |

|---|---|---|

| Deposits | Customer deposits | SAR 428bn |

| Retail financing | FCF / mkt share | SAR 12–15bn / 30–35% |

| Corporate | Market share / growth | ≈18% / 3–5% |

| Treasury | Liquid assets | SAR 200+bn |

Delivered as Shown

Al Rajhi Bank BCG Matrix

The file you're previewing is the exact Al Rajhi Bank BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document built for strategic decision-making and presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Al Rajhi Bank’s BCG Matrix preview highlights how its core retail and Islamic finance offerings perform across growth and market-share dimensions, hinting at potential Stars in consumer banking and Cash Cows in core deposit services while suggesting areas to watch for Question Marks amid digital disruption. This snapshot teases strategic priorities—resource allocation, divestment, or investment—to sharpen competitive advantage. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and ready-to-use Word and Excel deliverables to act with confidence.

Stars

Digital Banking Ecosystem and Super App

Al Rajhi Bank leads Saudi digital banking, with its mobile app serving over 8 million active users by late 2025 and capturing roughly 35% of retail digital transaction volume nationwide, driven by Vision 2030 fintech growth projections of ~20% CAGR through 2028.

To sustain this position against neobanks, the bank must keep heavy investment in UI/UX and backend scalability—expecting capital spend on digital platforms to remain a high single-digit percent of annual IT budget (~SAR 300–400m in 2025).

These digital services function as the primary acquisition channel for customers under 35, accounting for about 60% of new retail accounts in 2025 and boosting cross-sell rates by ~1.8x versus branch-led customers.

SME Financing and Development

SME lending is a star as Al Rajhi aligns with Saudi Vision 2030 diversification; by end-2025 the bank held an estimated 22% share of the Saudi SME financing market after growing SME book 28% year-on-year to SAR 34.2bn.

urpay Digital Wallet Services

urpay Digital Wallet Services is a Star: by 2025 it holds an estimated 35–40% share of Saudi Arabia’s digital payments volume, in a market growing ~20% CAGR (2020–25) as cash transactions fell to ~15% of retail payments.

The unit consumes sizable cash for marketing and R&D—Al Rajhi disclosed ~SAR 120–180m annual investment—aiming to defend share and add gig-economy features.

urpay links legacy banking with freelancers and platforms, processing millions of monthly payouts and remaining a top strategic investment for Al Rajhi.

Mortgage and Real Estate Financing

Al Rajhi remains a star in mortgages, holding ~30%+ market share in Saudi mortgage lending (2025) by volume while chasing the Ministry of Housing targets—helping fund 400k+ homes under government programs through aggressive origination.

Mortgage loans demand high capital due to long durations and high LTVs; mortgage book growth was ~12–15% YoY in 2024–2025, well above retail loans (~6–7%), signalling elevated growth before eventual steady state.

The segment consumes capital now but should become a cash cow once national housing demand stabilizes (expected by 2028–2030), converting scale into predictable net interest margins and steady fee income.

- Market share ~30%+ (2025)

- Mortgage book growth 12–15% YoY (2024–25)

- Retail loan growth ~6–7% (2024–25)

- Supports 400k+ homes in housing programs

- Transition to cash cow expected 2028–2030

ESG and Sustainable Finance Portfolios

As of late 2025, green financing and ESG-linked corporate loans are high-growth for Al Rajhi Bank, where it holds an early lead with >30% market share in Saudi Islamic green lending.

The bank is investing SAR 12–15 billion in structuring Sharia-compliant green sukuk and sustainability-linked credit facilities to meet global investor standards.

Demand is rising as Saudi corporations align with the Saudi Green Initiative and net-zero targets, boosting ESG deal flow by ~40% YoY in 2024–25 and drawing institutional capital.

- Early leader: >30% market share in Islamic green lending

- Investment: SAR 12–15bn in green sukuk and facilities

- Growth: ~40% YoY ESG deal-flow increase (2024–25)

- Benefit: attracts institutional capital and top corporates

Al Rajhi Dominates: 8M Digital Users, urpay Lead, 30%+ Mortgages, Strong SME Growth

Al Rajhi’s Stars: digital banking (8M users, ~35% retail digital volume, 2025), urpay wallet (35–40% payments share, SAR120–180m annual spend), mortgages (~30%+ market share, mortgage book SAR34.2bn, 12–15% YoY), SME lending (22% SME market, SAR34.2bn).

| Unit | Metric (2025) |

|---|---|

| Digital | 8M users; 35% vol |

| urpay | 35–40% payments; SAR120–180m spend |

| Mortgages | 30%+ share; SAR34.2bn |

| SME | 22% share; 28% YoY |

What is included in the product

BCG Matrix of Al Rajhi Bank: strategic placement of business units into Stars, Cash Cows, Question Marks, and Dogs with tailored investment guidance.

One-page overview placing each Al Rajhi Bank business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

Retail Deposit Base

Al Rajhi Bank holds the largest retail deposit base in Saudi Arabia—SAR 428 billion in customer deposits as of FY 2024—providing a low‑cost funding source typical of a cash cow.

With dominant market share in basic savings and low sector growth, these deposits produce strong net interest margin cash flow with minimal marketing spend.

The resulting liquidity funds stars and question marks across the portfolio and underpins dividend capacity and balance‑sheet stability.

Personal Islamic Financing

Personal Islamic financing is a mature, low-growth cash cow for Al Rajhi Bank; as of FY2024 the bank held about 30–35% domestic market share in retail Sharia loans while segment growth slowed to ~3–4% year-on-year, signaling market saturation.

Profit margins remain strong—net finance income contribution from retail Sharia products stayed around 28% of total operating income in 2024—thanks to efficient servicing, brand loyalty, and limited incremental capex needs versus digital offerings.

These loans need minimal new infrastructure or marketing spend; steady monthly repayments generated roughly SAR 12–15 billion in free cash flow in FY2024, funding operations and supporting dividends and buybacks.

Corporate Banking Services

Al Rajhi Bank’s corporate banking services—traditional lending and cash management for large enterprises—remain a cash cow, holding high market share in Saudi Arabia’s corporate credit market (about 18% market share in 2024 corporate loans to large corporates, SAMA data). The segment grows modestly (~3–5% annual loan book expansion) but delivers predictable net interest income and stable fees. Deep ties with Saudi conglomerates drive low churn and strong deposit stickiness. It reliably funds the bank’s higher-risk innovation and investment activities.

Treasury and Liquidity Management

Treasury and Liquidity Management holds a large portfolio of high-quality liquid assets and Sharia-compliant sukuk yielding steady returns; as of 2025 Al Rajhi reported SAR 200+ billion in liquid assets, supporting net interest income stability. The unit operates in a mature Saudi market where Al Rajhi’s scale secures dominant market liquidity, so growth is low but cash generation is high. It stabilizes the balance sheet during interest-rate swings and funds lending needs.

- SAR 200+ billion liquid assets (2025)

- High-quality sukuk and cash equivalents

- Low growth, surplus cash generator

- Key stabilizer vs. rate volatility

Brokerage and Asset Management

Al Rajhi Capital leads Saudi equity brokerage with ~28% market share in 2024 and average daily trading volumes >SAR 6.5bn, generating fee income that exceeded SAR 420m in 2024; steady Tadawul growth (~6% CAGR 2020–24) limits rapid top-line expansion but sustains high margins.

Brokerage/AM needs low capex versus lending; operating cash flow funded SAR 200–300m of digital wealth tech investments in 2024, recycling fees into product digitization and platform scale-up.

- ~28% local equity market share (2024)

- Avg daily trading volume >SAR 6.5bn (2024)

- Fee income ~SAR 420m (2024)

- Reinvested SAR 200–300m into digital wealth (2024)

Al Rajhi’s cash cows: deposits, Islamic retail loans, corporate lending & SAR200bn+ treasuries

Al Rajhi’s cash cows—retail deposits (SAR 428bn FY2024), personal Islamic financing (30–35% market share, ~SAR 12–15bn FCF FY2024), corporate lending (≈18% market share, 3–5% growth) and treasury/liquid assets (SAR 200+bn 2025)—generate steady net interest income and fees, fund dividends, buybacks, and invest in digital growth.

| Segment | Key metric | 2024/25 |

|---|---|---|

| Deposits | Customer deposits | SAR 428bn |

| Retail financing | FCF / mkt share | SAR 12–15bn / 30–35% |

| Corporate | Market share / growth | ≈18% / 3–5% |

| Treasury | Liquid assets | SAR 200+bn |

Delivered as Shown

Al Rajhi Bank BCG Matrix

The file you're previewing is the exact Al Rajhi Bank BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document built for strategic decision-making and presentation.