Al Rajhi Bank Business Model Canvas

Al Rajhi Bank BMC: Sharia‑Compliant Strategy, Partners & Growth Blueprint

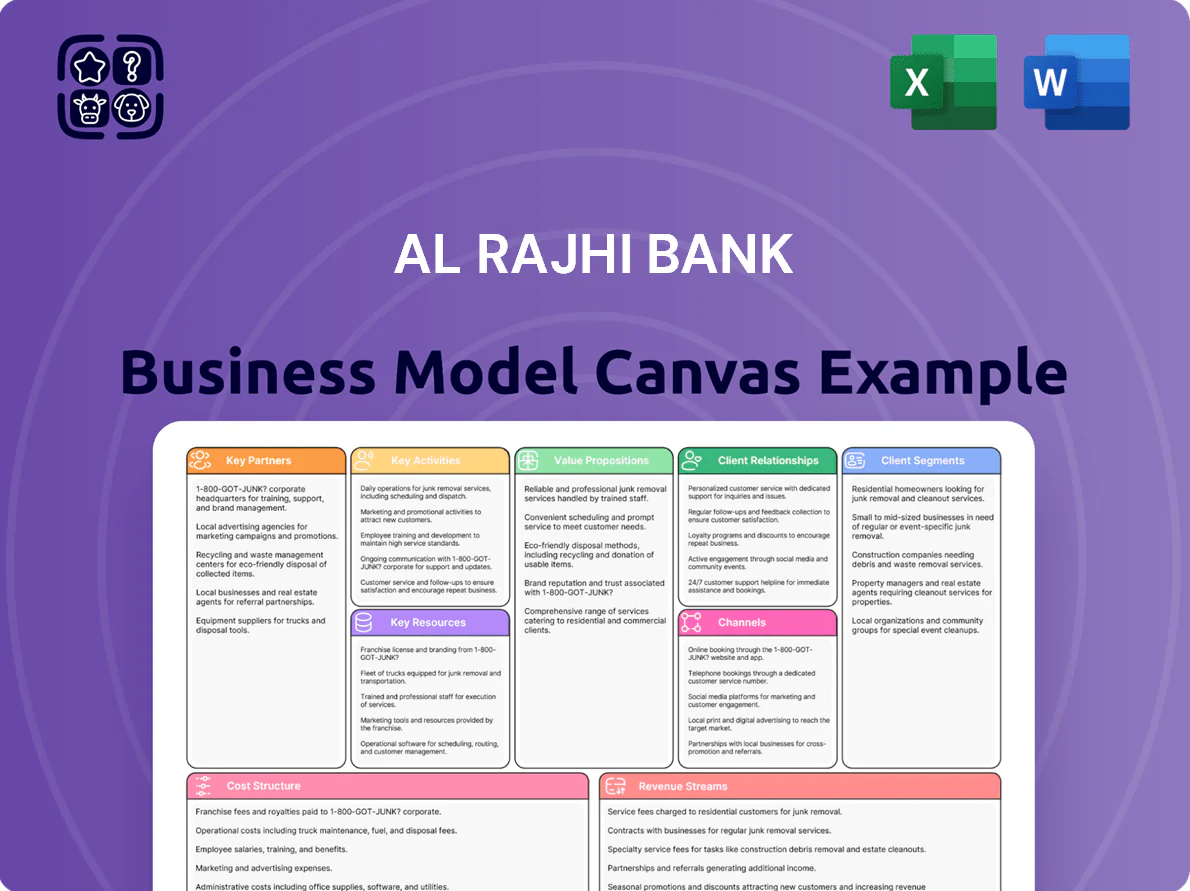

Unlock the full strategic blueprint behind Al Rajhi Bank’s business model—this concise Business Model Canvas maps customer segments, Sharia-compliant value propositions, key partnerships, and scalable revenue streams to reveal how the bank sustains growth and market leadership.

Partnerships

Strategic Fintech Collaborations

Al Rajhi Bank partners with fintechs to embed real-time payments and blockchain-based settlement, rolling out 12 P2P and automated-savings products across its platform and driving a 22% digital-transaction volume rise in 2024; by end-2025 these alliances are core to retaining its regional #1 digital banking share, supporting 18 million active mobile users and a 35% increase in mobile-originated deposits.

Sharia Advisory Board and Scholars

Al Rajhi Bank partners with an internal Sharia Advisory Board and 45 external scholars to certify products against Islamic law, supporting over SAR 300 billion (2025) in Sharia-compliant assets; this legal-ethical oversight is central to credibility with its ~10 million retail customers.

They run quarterly audits and 120+ consultations yearly to align with AAOIFI and IFSB updates, reducing non-compliance risk and enabling product launches that meet evolving global Islamic finance standards.

Government and Public Sector Entities

Al Rajhi Bank maintains strategic ties with the Saudi Central Bank (SAMA) and ministries to align with Vision 2030, channeling over SAR 45 billion in government-backed housing loans since 2020 and supporting SAR 60+ billion in infrastructure financing through public-private programs as of 2025.

These public-sector partnerships keep Al Rajhi a primary vehicle for domestic growth and financial inclusion, serving 10+ million retail customers and expanding subsidized lending and social finance products in underserved regions.

Global Payment Networks

Strategic alliances with Visa and Mastercard let Al Rajhi Bank issue globally accepted cards, supporting secure online payments and cross-border transactions that handled an estimated SAR 45 billion in international card volumes in 2024.

Through these networks the bank offers premium travel benefits and international rewards—boosting card spend and retention; co-branded programs drove roughly 12% of new card activations in 2024.

- Global processing via Visa/Mastercard

- SAR 45B international card volume (2024)

- Premium travel & rewards boosted activations 12% (2024)

Corporate and SME Service Providers

Al Rajhi scales digital Sharia finance: SAR300B assets, 22% digital growth, 18M users

Al Rajhi Bank leverages fintechs, Visa/Mastercard, government bodies, Sharia scholars, and ISVs to scale digital payments, Sharia-compliant assets (SAR 300B, 2025), and SME services—driving 22% digital volume growth (2024), SAR 45B international card flows (2024), 120k SME payrolls (2024), and supporting 18M mobile users.

| Partnership | Key 2024–25 Metric |

|---|---|

| Fintechs | 22% digital volume rise (2024) |

| Sharia Board | SAR 300B Sharia assets (2025) |

| Visa/Mastercard | SAR 45B intl card volume (2024) |

| SME ISVs | 120k payrolls (2024) |

| Government | SAR 45B housing loans since 2020 |

What is included in the product

A concise Business Model Canvas for Al Rajhi Bank detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partnerships, cost structure, and risk factors, reflecting its Islamic banking strategy and real-world operations to support investor presentations and strategic analysis.

High-level view of Al Rajhi Bank’s business model with editable cells to quickly pinpoint customer segments, revenue streams, and Sharia-compliant product gaps for faster strategy decisions.

Activities

Sharia Compliant Product Development

Al Rajhi Bank develops Sharia-compliant products like Murabaha and Sukuk, backed by R&D teams and Sharia boards to align modern needs with Islamic law; in 2024 Islamic finance issuance in Saudi Arabia hit $50bn, and Al Rajhi’s sukuk-related assets rose ~12% YoY, helping it steal share from conventional banks. Constant product innovation targets retail and corporate segments, aiming to grow Islamic assets above the 15% sector CAGR through 2025.

Digital Infrastructure Maintenance and Upgrades

A large share of operations focuses on maintaining Al Rajhi Bank’s digital ecosystem—mobile app and online portal—serving over 5 million daily active users and targeting 99.95% uptime, with annual IT spend around SAR 1.2 billion (2024).

Teams run continuous security monitoring, patching, and platform upgrades while rolling AI/ML features for personalized offers and fraud detection, cutting false positives by ~30% in 2024.

Risk Management and Credit Assessment

Al Rajhi Bank uses machine learning credit scoring and portfolio segment analysis to assess retail and corporate borrowers within Shariah-compliant contracts, keeping 2024-stage 3 non-performing financing at about 1.6% of gross financings to preserve asset quality. Advanced stress-testing and VaR-style models forecast market shifts to protect SAR 36+ billion capital buffers and limit unexpected capital shortfalls.

Customer Acquisition and Marketing

Marketing centers on promoting Al Rajhi Bank’s Islamic-ethical brand and digital ease via multi-channel campaigns—targeted social media, 120+ community events in 2024, and loyalty pushes—helping drive 8% YoY retail deposit growth in 2024.

Cross-selling focuses on investment and takaful (Islamic insurance), contributing ~18% of retail revenue in 2024 and lifting product-per-customer to 2.3.

- Targeted social ads → 25m impressions/month (2024)

- 120+ community events (2024)

- Loyalty promos → 8% YoY deposit growth (2024)

- Cross-sell → 18% retail revenue (2024)

Regulatory Compliance and Auditing

Al Rajhi Bank must run continuous compliance monitoring to meet Saudi Central Bank (SAMA) rules and IFRS standards, using monthly internal audits and quarterly reports—SAMA fined banks SAR 45m in 2023 for lapses, so rigorous checks protect the license and reputation.

Compliance teams prepare regulatory filings, publish transparent financial disclosures (2024 net income SAR 13.6bn), and coordinate external audits to ensure controls work and stakeholder trust stays high.

- Monthly internal audits

- Quarterly SAMA reporting

- Annual external audit

- Public IFRS financials (2024 net income SAR 13.6bn)

Al Rajhi: SAR13.6bn net, 5M DAU, SAR1.2bn IT, 8% deposit growth, 1.6% NPF

Al Rajhi runs Sharia product R&D, digital ops (5M DAU, SAR1.2bn IT spend 2024), ML credit scoring (stage‑3 NPF ~1.6%), marketing/cross‑sell drives 8% retail deposit growth and 18% retail revenue from takaful, and strict compliance (monthly audits; 2024 net income SAR13.6bn).

| Metric | 2024 |

|---|---|

| DAU | 5,000,000 |

| IT spend | SAR1.2bn |

| Stage‑3 NPF | 1.6% |

| Retail deposit growth YoY | 8% |

| Takaful revenue share | 18% |

| Net income | SAR13.6bn |

Full Version Awaits

Business Model Canvas

The document you're previewing is the authentic Al Rajhi Bank Business Model Canvas—not a mockup or sample—and it’s the exact file you’ll receive after purchase, fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Al Rajhi Bank BMC: Sharia‑Compliant Strategy, Partners & Growth Blueprint

Unlock the full strategic blueprint behind Al Rajhi Bank’s business model—this concise Business Model Canvas maps customer segments, Sharia-compliant value propositions, key partnerships, and scalable revenue streams to reveal how the bank sustains growth and market leadership.

Partnerships

Strategic Fintech Collaborations

Al Rajhi Bank partners with fintechs to embed real-time payments and blockchain-based settlement, rolling out 12 P2P and automated-savings products across its platform and driving a 22% digital-transaction volume rise in 2024; by end-2025 these alliances are core to retaining its regional #1 digital banking share, supporting 18 million active mobile users and a 35% increase in mobile-originated deposits.

Sharia Advisory Board and Scholars

Al Rajhi Bank partners with an internal Sharia Advisory Board and 45 external scholars to certify products against Islamic law, supporting over SAR 300 billion (2025) in Sharia-compliant assets; this legal-ethical oversight is central to credibility with its ~10 million retail customers.

They run quarterly audits and 120+ consultations yearly to align with AAOIFI and IFSB updates, reducing non-compliance risk and enabling product launches that meet evolving global Islamic finance standards.

Government and Public Sector Entities

Al Rajhi Bank maintains strategic ties with the Saudi Central Bank (SAMA) and ministries to align with Vision 2030, channeling over SAR 45 billion in government-backed housing loans since 2020 and supporting SAR 60+ billion in infrastructure financing through public-private programs as of 2025.

These public-sector partnerships keep Al Rajhi a primary vehicle for domestic growth and financial inclusion, serving 10+ million retail customers and expanding subsidized lending and social finance products in underserved regions.

Global Payment Networks

Strategic alliances with Visa and Mastercard let Al Rajhi Bank issue globally accepted cards, supporting secure online payments and cross-border transactions that handled an estimated SAR 45 billion in international card volumes in 2024.

Through these networks the bank offers premium travel benefits and international rewards—boosting card spend and retention; co-branded programs drove roughly 12% of new card activations in 2024.

- Global processing via Visa/Mastercard

- SAR 45B international card volume (2024)

- Premium travel & rewards boosted activations 12% (2024)

Corporate and SME Service Providers

Al Rajhi scales digital Sharia finance: SAR300B assets, 22% digital growth, 18M users

Al Rajhi Bank leverages fintechs, Visa/Mastercard, government bodies, Sharia scholars, and ISVs to scale digital payments, Sharia-compliant assets (SAR 300B, 2025), and SME services—driving 22% digital volume growth (2024), SAR 45B international card flows (2024), 120k SME payrolls (2024), and supporting 18M mobile users.

| Partnership | Key 2024–25 Metric |

|---|---|

| Fintechs | 22% digital volume rise (2024) |

| Sharia Board | SAR 300B Sharia assets (2025) |

| Visa/Mastercard | SAR 45B intl card volume (2024) |

| SME ISVs | 120k payrolls (2024) |

| Government | SAR 45B housing loans since 2020 |

What is included in the product

A concise Business Model Canvas for Al Rajhi Bank detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partnerships, cost structure, and risk factors, reflecting its Islamic banking strategy and real-world operations to support investor presentations and strategic analysis.

High-level view of Al Rajhi Bank’s business model with editable cells to quickly pinpoint customer segments, revenue streams, and Sharia-compliant product gaps for faster strategy decisions.

Activities

Sharia Compliant Product Development

Al Rajhi Bank develops Sharia-compliant products like Murabaha and Sukuk, backed by R&D teams and Sharia boards to align modern needs with Islamic law; in 2024 Islamic finance issuance in Saudi Arabia hit $50bn, and Al Rajhi’s sukuk-related assets rose ~12% YoY, helping it steal share from conventional banks. Constant product innovation targets retail and corporate segments, aiming to grow Islamic assets above the 15% sector CAGR through 2025.

Digital Infrastructure Maintenance and Upgrades

A large share of operations focuses on maintaining Al Rajhi Bank’s digital ecosystem—mobile app and online portal—serving over 5 million daily active users and targeting 99.95% uptime, with annual IT spend around SAR 1.2 billion (2024).

Teams run continuous security monitoring, patching, and platform upgrades while rolling AI/ML features for personalized offers and fraud detection, cutting false positives by ~30% in 2024.

Risk Management and Credit Assessment

Al Rajhi Bank uses machine learning credit scoring and portfolio segment analysis to assess retail and corporate borrowers within Shariah-compliant contracts, keeping 2024-stage 3 non-performing financing at about 1.6% of gross financings to preserve asset quality. Advanced stress-testing and VaR-style models forecast market shifts to protect SAR 36+ billion capital buffers and limit unexpected capital shortfalls.

Customer Acquisition and Marketing

Marketing centers on promoting Al Rajhi Bank’s Islamic-ethical brand and digital ease via multi-channel campaigns—targeted social media, 120+ community events in 2024, and loyalty pushes—helping drive 8% YoY retail deposit growth in 2024.

Cross-selling focuses on investment and takaful (Islamic insurance), contributing ~18% of retail revenue in 2024 and lifting product-per-customer to 2.3.

- Targeted social ads → 25m impressions/month (2024)

- 120+ community events (2024)

- Loyalty promos → 8% YoY deposit growth (2024)

- Cross-sell → 18% retail revenue (2024)

Regulatory Compliance and Auditing

Al Rajhi Bank must run continuous compliance monitoring to meet Saudi Central Bank (SAMA) rules and IFRS standards, using monthly internal audits and quarterly reports—SAMA fined banks SAR 45m in 2023 for lapses, so rigorous checks protect the license and reputation.

Compliance teams prepare regulatory filings, publish transparent financial disclosures (2024 net income SAR 13.6bn), and coordinate external audits to ensure controls work and stakeholder trust stays high.

- Monthly internal audits

- Quarterly SAMA reporting

- Annual external audit

- Public IFRS financials (2024 net income SAR 13.6bn)

Al Rajhi: SAR13.6bn net, 5M DAU, SAR1.2bn IT, 8% deposit growth, 1.6% NPF

Al Rajhi runs Sharia product R&D, digital ops (5M DAU, SAR1.2bn IT spend 2024), ML credit scoring (stage‑3 NPF ~1.6%), marketing/cross‑sell drives 8% retail deposit growth and 18% retail revenue from takaful, and strict compliance (monthly audits; 2024 net income SAR13.6bn).

| Metric | 2024 |

|---|---|

| DAU | 5,000,000 |

| IT spend | SAR1.2bn |

| Stage‑3 NPF | 1.6% |

| Retail deposit growth YoY | 8% |

| Takaful revenue share | 18% |

| Net income | SAR13.6bn |

Full Version Awaits

Business Model Canvas

The document you're previewing is the authentic Al Rajhi Bank Business Model Canvas—not a mockup or sample—and it’s the exact file you’ll receive after purchase, fully formatted and ready to use.