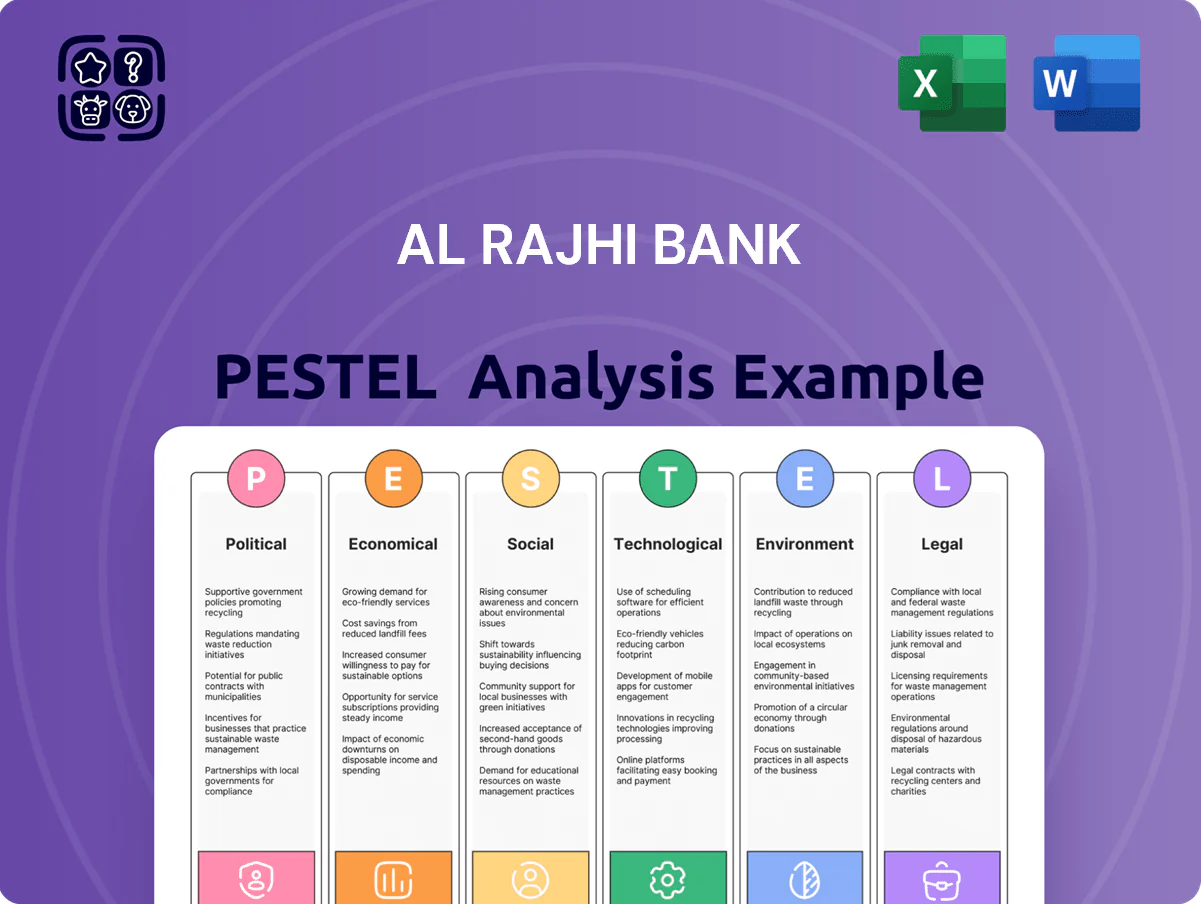

Al Rajhi Bank PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain actionable insight into how political shifts, economic cycles, social dynamics, technological innovation, legal reforms, and environmental trends are shaping Al Rajhi Bank’s strategic path—our concise PESTLE highlights critical drivers and risks to inform your decisions. Purchase the full analysis to access the complete, fully sourced report with editable charts and strategic recommendations for investors, consultants, and executives.

Political factors

Vision 2030 alignment

Al Rajhi Bank underpins Vision 2030 by financing home ownership—contributing to the goal of increasing home ownership to 70%—and by lending to SMEs; in 2024 the bank reported SAR 158bn in total financing, positioning it to back private sector growth.

Geopolitical stability in the GCC

The GCC political landscape directly affects investor confidence and cross-border trade for Saudi banks; GCC FDI inflows reached $87bn in 2024, supporting liquidity for institutions like Al Rajhi. Strengthened Saudi ties with the US and China in 2024–25 reduced perceived risk, evident as regional CDS spreads fell ~12% YTD. Al Rajhi actively monitors diplomatic shifts and sanctions risk to protect asset quality and cross-border operations.

Government fiscal policy

The Saudi government’s fiscal spending drives liquidity in banks; 2024 budget outlays reached SAR 1.133 trillion, supporting system-wide deposit growth and affecting Al Rajhi’s funding costs. Reliance on oil receipts (oil revenue ~SAR 812bn in 2023) and rising non-oil taxes means Al Rajhi adjusts lending cycles to state-led capex timing. Cuts to subsidies or public wage changes (public wages ~SAR 300–350bn range historically) directly alter retail deposit and loan demand.

Foreign investment regulations

The ongoing liberalization of Tadawul has lifted foreign allowance in the market to 49% in many sectors and drove foreign portfolio inflows to SAR 42.3bn in 2024, boosting Al Rajhi’s visibility among international institutional investors.

Political moves to widen QFI status and MSCI/S&P inclusion pressures the bank to align with global governance; evolving foreign ownership caps mean enhanced disclosure and compliance costs for Al Rajhi.

Regional expansion diplomacy

Regional expansion diplomacy: Al Rajhi Bank’s operations in Jordan, Kuwait and Malaysia are shaped by Saudi diplomatic ties; for example Saudi trade with GCC neighbors totaled SAR 1.2 trillion in 2024, easing cross-border financial integration and licensing.

Diplomatic agreements in 2023–2025 accelerated approvals—Al Rajhi’s overseas assets represented about 8–10% of total assets (~SAR 40–50bn in 2024), requiring navigation of each market’s political climate while retaining Saudi identity.

- Saudi-GCC ties and trade flows (SAR 1.2tn in 2024) reduce regulatory friction

- Overseas assets ~8–10% of total (SAR 40–50bn, 2024)

- Licensing often relies on bilateral/multilateral agreements (2023–2025)

Al Rajhi rides Saudi stimulus and Tadawul liberalization as foreign inflows and credit improve

Saudi fiscal stimulus and Vision 2030 support Al Rajhi’s retail and SME lending (SAR 158bn financing, 2024); GCC stability and US/China ties lowered regional CDS ~12% YTD, boosting investor confidence. Tadawul liberalization raised foreign inflows to SAR 42.3bn (2024) and ownership caps toward 49%, increasing disclosure costs; overseas assets ~8–10% (~SAR 40–50bn, 2024).

| Metric | 2024 |

|---|---|

| Total financing | SAR 158bn |

| Foreign inflows | SAR 42.3bn |

| Overseas assets | SAR 40–50bn (8–10%) |

| CDS change YTD | ~-12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Al Rajhi Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and opportunity identification for executives, investors, and advisors.

A concise, shareable PESTLE snapshot tailored for Al Rajhi Bank that clarifies regulatory, economic, social, technological, legal, and environmental drivers for faster decision-making in meetings and presentations.

Economic factors

Interest rate environment

As of late 2025, SAMA's repo rate stood at 6.25%, broadly tracking the Fed; this higher rate cycle supported Al Rajhi Bank’s NIMs, with reported group NIM around 3.1% in 9M2025 versus 2.7% in 2023, aided by large non-interest-bearing deposits (~65% of deposits).

Non-oil GDP growth

Inflation and consumer spending

Inflation in Saudi Arabia eased to 2.6% in 2025 but spiked to 3.1% year-on-year in late 2024, squeezing disposable income for Al Rajhi’s retail customers and dampening personal loan origination by an estimated 8–12% in 2024. Rising living costs elevated unsecured loan delinquency rates across the sector to about 2.4% in 2024, prompting the bank to use AI-driven analytics and real-time transaction scoring to tighten credit appetite and recalibrate loss provisions.

Mortgage market saturation

Following years of rapid growth driven by REDF and Sakani, Saudi mortgage originations are plateauing as the market nears maturity; total outstanding mortgages reached about SAR 300 billion by end-2024, up 18% y/y but slowing versus prior years.

Al Rajhi, the largest home financier with roughly 30% market share in 2024, faces pressure from rising property prices and intensified competition, prompting a strategic pivot.

The bank is targeting refinancing and secondary-market asset sales—aiming to boost return on assets and preserve mortgage volumes amid slower new-originations growth.

- Outstanding mortgages ~SAR 300bn (2024)

- Al Rajhi ~30% market share (2024)

- Growth rate slowed to ~18% y/y (2024)

- Focus: refinancing and secondary-market liquidity

Oil price volatility

Despite diversification, Saudi oil revenues remain material; a 2024 drop in crude prices shaved government oil income by an estimated SAR 120bn, pressuring public deposits and systemic liquidity that underpin banking sector funding.

Sharp oil revenue declines historically tighten liquidity, raising funding costs for banks like Al Rajhi; in 2024 average Saudi interbank rates rose ~40bps during price shocks, affecting margins.

Al Rajhi reported a Liquidity Coverage Ratio of 235% in 2024, well above SAMA minimums, providing a buffer against energy-market–driven shocks.

- Oil revenue sensitivity: SAR 120bn impact (2024)

- Interbank rate increase: ~40bps during shocks (2024)

- Al Rajhi LCR: 235% (2024)

SAMA 6.25% lifts NIM to 3.1%; GDP, tourism and mortgages fuel bank resilience

Higher SAMA rate (6.25% late-2025) supported NIM ~3.1% (9M2025) vs 2.7% (2023); non-oil GDP +4.1% (2024) and tourism +18% (2024) boost corporate/SME demand; mortgages ~SAR300bn (2024) with Al Rajhi ~30% share, growth slowing to 18% y/y; inflation ~2.6% (2025) raised unsecured delinquencies to ~2.4% (2024); LCR 235% (2024).

| Metric | Value |

|---|---|

| SAMA rate | 6.25% (late-2025) |

| Group NIM | 3.1% (9M2025) |

| Non-oil GDP | +4.1% (2024) |

| Mortgages | SAR300bn (2024) |

| Al Rajhi share | ~30% (2024) |

| Inflation | 2.6% (2025) |

| LCR | 235% (2024) |

Same Document Delivered

Al Rajhi Bank PESTLE Analysis

The preview shown here is the exact Al Rajhi Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain actionable insight into how political shifts, economic cycles, social dynamics, technological innovation, legal reforms, and environmental trends are shaping Al Rajhi Bank’s strategic path—our concise PESTLE highlights critical drivers and risks to inform your decisions. Purchase the full analysis to access the complete, fully sourced report with editable charts and strategic recommendations for investors, consultants, and executives.

Political factors

Vision 2030 alignment

Al Rajhi Bank underpins Vision 2030 by financing home ownership—contributing to the goal of increasing home ownership to 70%—and by lending to SMEs; in 2024 the bank reported SAR 158bn in total financing, positioning it to back private sector growth.

Geopolitical stability in the GCC

The GCC political landscape directly affects investor confidence and cross-border trade for Saudi banks; GCC FDI inflows reached $87bn in 2024, supporting liquidity for institutions like Al Rajhi. Strengthened Saudi ties with the US and China in 2024–25 reduced perceived risk, evident as regional CDS spreads fell ~12% YTD. Al Rajhi actively monitors diplomatic shifts and sanctions risk to protect asset quality and cross-border operations.

Government fiscal policy

The Saudi government’s fiscal spending drives liquidity in banks; 2024 budget outlays reached SAR 1.133 trillion, supporting system-wide deposit growth and affecting Al Rajhi’s funding costs. Reliance on oil receipts (oil revenue ~SAR 812bn in 2023) and rising non-oil taxes means Al Rajhi adjusts lending cycles to state-led capex timing. Cuts to subsidies or public wage changes (public wages ~SAR 300–350bn range historically) directly alter retail deposit and loan demand.

Foreign investment regulations

The ongoing liberalization of Tadawul has lifted foreign allowance in the market to 49% in many sectors and drove foreign portfolio inflows to SAR 42.3bn in 2024, boosting Al Rajhi’s visibility among international institutional investors.

Political moves to widen QFI status and MSCI/S&P inclusion pressures the bank to align with global governance; evolving foreign ownership caps mean enhanced disclosure and compliance costs for Al Rajhi.

Regional expansion diplomacy

Regional expansion diplomacy: Al Rajhi Bank’s operations in Jordan, Kuwait and Malaysia are shaped by Saudi diplomatic ties; for example Saudi trade with GCC neighbors totaled SAR 1.2 trillion in 2024, easing cross-border financial integration and licensing.

Diplomatic agreements in 2023–2025 accelerated approvals—Al Rajhi’s overseas assets represented about 8–10% of total assets (~SAR 40–50bn in 2024), requiring navigation of each market’s political climate while retaining Saudi identity.

- Saudi-GCC ties and trade flows (SAR 1.2tn in 2024) reduce regulatory friction

- Overseas assets ~8–10% of total (SAR 40–50bn, 2024)

- Licensing often relies on bilateral/multilateral agreements (2023–2025)

Al Rajhi rides Saudi stimulus and Tadawul liberalization as foreign inflows and credit improve

Saudi fiscal stimulus and Vision 2030 support Al Rajhi’s retail and SME lending (SAR 158bn financing, 2024); GCC stability and US/China ties lowered regional CDS ~12% YTD, boosting investor confidence. Tadawul liberalization raised foreign inflows to SAR 42.3bn (2024) and ownership caps toward 49%, increasing disclosure costs; overseas assets ~8–10% (~SAR 40–50bn, 2024).

| Metric | 2024 |

|---|---|

| Total financing | SAR 158bn |

| Foreign inflows | SAR 42.3bn |

| Overseas assets | SAR 40–50bn (8–10%) |

| CDS change YTD | ~-12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Al Rajhi Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and opportunity identification for executives, investors, and advisors.

A concise, shareable PESTLE snapshot tailored for Al Rajhi Bank that clarifies regulatory, economic, social, technological, legal, and environmental drivers for faster decision-making in meetings and presentations.

Economic factors

Interest rate environment

As of late 2025, SAMA's repo rate stood at 6.25%, broadly tracking the Fed; this higher rate cycle supported Al Rajhi Bank’s NIMs, with reported group NIM around 3.1% in 9M2025 versus 2.7% in 2023, aided by large non-interest-bearing deposits (~65% of deposits).

Non-oil GDP growth

Inflation and consumer spending

Inflation in Saudi Arabia eased to 2.6% in 2025 but spiked to 3.1% year-on-year in late 2024, squeezing disposable income for Al Rajhi’s retail customers and dampening personal loan origination by an estimated 8–12% in 2024. Rising living costs elevated unsecured loan delinquency rates across the sector to about 2.4% in 2024, prompting the bank to use AI-driven analytics and real-time transaction scoring to tighten credit appetite and recalibrate loss provisions.

Mortgage market saturation

Following years of rapid growth driven by REDF and Sakani, Saudi mortgage originations are plateauing as the market nears maturity; total outstanding mortgages reached about SAR 300 billion by end-2024, up 18% y/y but slowing versus prior years.

Al Rajhi, the largest home financier with roughly 30% market share in 2024, faces pressure from rising property prices and intensified competition, prompting a strategic pivot.

The bank is targeting refinancing and secondary-market asset sales—aiming to boost return on assets and preserve mortgage volumes amid slower new-originations growth.

- Outstanding mortgages ~SAR 300bn (2024)

- Al Rajhi ~30% market share (2024)

- Growth rate slowed to ~18% y/y (2024)

- Focus: refinancing and secondary-market liquidity

Oil price volatility

Despite diversification, Saudi oil revenues remain material; a 2024 drop in crude prices shaved government oil income by an estimated SAR 120bn, pressuring public deposits and systemic liquidity that underpin banking sector funding.

Sharp oil revenue declines historically tighten liquidity, raising funding costs for banks like Al Rajhi; in 2024 average Saudi interbank rates rose ~40bps during price shocks, affecting margins.

Al Rajhi reported a Liquidity Coverage Ratio of 235% in 2024, well above SAMA minimums, providing a buffer against energy-market–driven shocks.

- Oil revenue sensitivity: SAR 120bn impact (2024)

- Interbank rate increase: ~40bps during shocks (2024)

- Al Rajhi LCR: 235% (2024)

SAMA 6.25% lifts NIM to 3.1%; GDP, tourism and mortgages fuel bank resilience

Higher SAMA rate (6.25% late-2025) supported NIM ~3.1% (9M2025) vs 2.7% (2023); non-oil GDP +4.1% (2024) and tourism +18% (2024) boost corporate/SME demand; mortgages ~SAR300bn (2024) with Al Rajhi ~30% share, growth slowing to 18% y/y; inflation ~2.6% (2025) raised unsecured delinquencies to ~2.4% (2024); LCR 235% (2024).

| Metric | Value |

|---|---|

| SAMA rate | 6.25% (late-2025) |

| Group NIM | 3.1% (9M2025) |

| Non-oil GDP | +4.1% (2024) |

| Mortgages | SAR300bn (2024) |

| Al Rajhi share | ~30% (2024) |

| Inflation | 2.6% (2025) |

| LCR | 235% (2024) |

Same Document Delivered

Al Rajhi Bank PESTLE Analysis

The preview shown here is the exact Al Rajhi Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.