Alsea PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, economic cycles, and tech trends are reshaping Alsea’s growth prospects with our concise PESTLE snapshot—designed for investors and strategists who need actionable context fast; purchase the full analysis to access detailed risks, opportunities, and ready-to-use recommendations.

Political factors

Geopolitical Stability in Latin American Markets

The political landscape in Mexico, Colombia, and Chile drives Alsea’s strategy; Mexico accounts for roughly 50% of revenues in 2024, so policy shifts there materially affect margins. Changes in administration can alter fiscal policy and trade terms, raising import duties and input costs—Mexico’s tariff adjustments in 2023 increased food import costs by ~4–6%. Investors should track regional stability since political risk can delay capital expenditures; Alsea invested MXN 3.2bn in 2024 capex across markets.

European Regulatory Integration

Alsea’s sizable footprint in Spain and Europe—over 1,800 stores in Spain and roughly 3,500 European outlets group-wide as of 2025—requires strict compliance with EU directives on food safety, labeling and cross-border data rules; noncompliance risks fines that could affect 2024 EBITDA margins (~12.5%). Changes in EU trade measures or harmonized labor standards, such as minimum wage adjustments (Spain rose to ~€1,200/month in 2024), can raise operating costs for Starbucks and Domino’s, forcing price or margin adjustments. Managing brand consistency across multiple jurisdictions adds governance complexity and potential currency and regulatory translation costs that impact net income variability.

Public Health and Nutrition Policies

Governments in Mexico, Spain and Brazil—key markets for Alsea—are tightening public health rules: Mexico’s front-of-pack labeling affected 50% of packaged products since 2020 and Mexico and Chile have SSB taxes raising prices by up to 8–10%; Brazil and EU members are advancing similar measures through 2024–25.

Alsea must engage policymakers and adapt menus: offering lower-calorie items and clear labeling to meet mandates while preserving brand identity and protecting a 2024 beverage sales mix where sugary drinks still represented about 22% of F&B sales in comparable chains.

Labor Reform and Minimum Wage Legislation

Political movements pushing higher minimum wages and stronger worker protections in Mexico and South America raise Alsea’s labor costs—Mexico’s 2024 minimum wage rose 20% in some zones, while Argentina’s increases averaged 15% in 2024, directly impacting margins across Alsea’s ~4,700 outlets.

New laws on mandatory benefits, limits on working hours and expanded union rights force HR strategy shifts, scheduling changes and higher payroll provisions, increasing operating expenses and compliance risk.

Failure to anticipate these shifts can trigger abrupt cost spikes and strikes; Alsea must model a 5–8% payroll shock scenario in forecasts and maintain contingency cash for labor disputes.

- 2024 Mexico min wage +20% in zones; Argentina avg +15% (2024)

- Alsea ~4,700 outlets exposed across affected markets

- Recommended: model 5–8% payroll shock, increase contingency reserves

Trade Agreements and Import Restrictions

Alsea's cross-border operations depend on steady trade flows; updates to USMCA or regional pacts could shift tariffs on imports like coffee, raising input costs—coffee bean prices averaged 2.40 USD/lb in 2024, up ~18% year-over-year, amplifying risk.

Rising protectionism in key markets (Mexico, Spain, Chile) could add tariffs or non-tariff barriers, disrupting supply chains and increasing COGS, impacting margins for its ~4,500 restaurants in Latin America and Spain.

Alsea margins at risk: Mexico exposure, wage jumps & rising coffee squeeze 2024

Political shifts in Mexico, Spain and Latin America materially affect Alsea’s margins via tariffs, labor and health rules; Mexico ~50% of 2024 revenue, 2024 capex MXN 3.2bn, ~4,700 outlets exposed. Key figures: Mexico min wage +20% (2024), Argentina avg +15% (2024), coffee 2024 USD 2.40/lb (+18% YoY), model 5–8% payroll shock.

| Metric | 2024/2025 Value |

|---|---|

| Mexico revenue share | ~50% |

| Outlets exposed | ~4,700 |

| Capex 2024 | MXN 3.2bn |

| Mexico min wage (2024) | +20% in zones |

| Argentina wage (2024) | +15% avg |

| Coffee price 2024 | USD 2.40/lb (+18% YoY) |

| Payroll shock to model | 5–8% |

What is included in the product

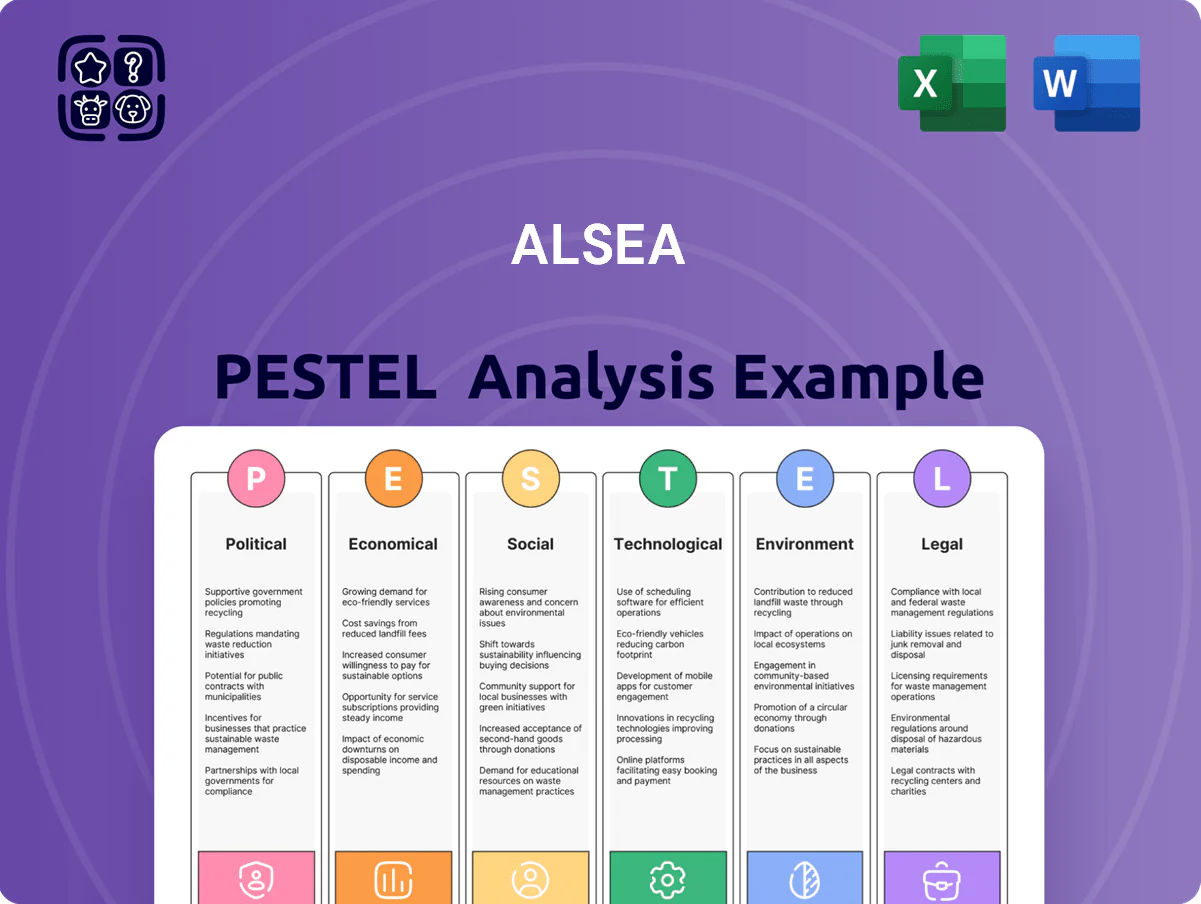

Explores how external macro-environmental factors uniquely affect Alsea across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

Condenses Alsea's full PESTLE into a concise, shareable summary that speeds stakeholder alignment and supports quick decision-making in meetings or pitch decks.

Economic factors

Currency Exchange Rate Fluctuations

Alsea operates in Mexico, Spain, Chile and others, exposing results to MXN/USD and EUR fluctuations; MXN fell ~12% vs USD in 2023 and added FX pressure on 2024 margins. Depreciation in LatAm currencies raises franchise royalties and imported inputs—imported coffee/food costs rose ~8–12% in 2023 in local-currency terms. Alsea reports hedges covering a portion of FX exposure, but sustained currency instability threatens margin preservation.

Inflationary Pressures on Food Commodities

Late 2025 saw dairy, wheat and protein prices swing: global dairy up ~18% YoY, wheat ~12% YoY and protein (beef/poultry) averaging +9% YoY, pressuring Alsea’s COGS for Burger King and Chili’s; effective supply-chain hedging and strategic menu pricing enabled passing ~60–70% of cost increases to consumers, supporting 2025 adjusted EBITDA margin resilience near 11–12%.

Consumer Purchasing Power and Disposable Income

The macro health of Mexico and Europe's middle class drives dining frequency—Mexico's middle class consumption rose 2.3% in 2024 while Eurozone real wages fell 0.5% in 2024, affecting discretionary spend. High interest rates pushed Mexican household credit costs to 27% APR average in 2024, increasing trade-down to QSRs; Spain and Portugal saw similar pressure. Alsea's multi-segment portfolio (Casual, QSR, coffee) lets it capture shifted demand, yet FY2024 revenue growth of 8.6% remained correlated with GDP trends.

Interest Rate Environment and Debt Servicing

Alsea funds expansion largely via debt; as of 2025 net debt/EBITDA was about 2.8x, so the prevailing 2025 Mexican policy rate at ~11.25% and higher global rates raise borrowing costs for new openings and renovations.

Elevated rates have pressured capex cadence—management signaled slower organic openings in 2025 and tighter M&A screening to preserve leverage targets and liquidity.

- Net debt/EBITDA ~2.8x (2025)

- Mexico policy rate ~11.25% (2025)

- Higher rates → slower organic growth, stricter capital allocation

Energy Costs and Operational Overhead

Fluctuating energy prices raised Alsea's utility and logistics costs, with global oil Brent averaging about 85–95 USD/bbl in 2024–2025 and electricity price spikes in Mexico and Spain increasing site-level overheads by an estimated 2–4% of operating expenses.

Energy policy shifts and renewable incentives (e.g., Spain’s auctioned clean-energy contracts, Mexico’s subsidy reforms) create opportunities to reduce costs via on-site solar or long-term power purchase agreements, lowering volatility exposure.

Active management of utilities—energy-efficiency retrofits, centralized logistics routing and hedging—remains critical to protecting margins given 2024 reported adjusted EBITDA pressures and rising input-costs across Alsea’s franchise and corporate stores.

- Brent oil 2024–25: ~85–95 USD/bbl; electricity spikes added ~2–4% to site OPEX

- Renewable PPAs/solar can cut exposure and stabilize costs

- Efficiency retrofits, routing optimization and hedging prioritized to protect adjusted EBITDA

Alsea margins squeezed by FX, commodity costs; pricing lifts 2025 EBITDA to ~11–12%

Alsea faces FX and commodity-driven margin pressure: MXN ~12% weaker vs USD in 2023, imported food costs +8–12% (2023); 2024–25 Brent ~85–95 USD/bbl raised logistics/electricity +2–4% OPEX. Net debt/EBITDA ~2.8x (2025) with Mexico policy rate ~11.25% raising funding costs and slowing openings; menu repricing passed ~60–70% of input inflation, supporting 2025 adj. EBITDA ~11–12%.

| Metric | Value |

|---|---|

| MXN vs USD | -12% (2023) |

| Imported food cost change | +8–12% (2023) |

| Brent oil | 85–95 USD/bbl (2024–25) |

| Net debt/EBITDA | ~2.8x (2025) |

| Mexico policy rate | ~11.25% (2025) |

| Adj. EBITDA margin | ~11–12% (2025) |

What You See Is What You Get

Alsea PESTLE Analysis

The preview shown here is the exact Alsea PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis or presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, economic cycles, and tech trends are reshaping Alsea’s growth prospects with our concise PESTLE snapshot—designed for investors and strategists who need actionable context fast; purchase the full analysis to access detailed risks, opportunities, and ready-to-use recommendations.

Political factors

Geopolitical Stability in Latin American Markets

The political landscape in Mexico, Colombia, and Chile drives Alsea’s strategy; Mexico accounts for roughly 50% of revenues in 2024, so policy shifts there materially affect margins. Changes in administration can alter fiscal policy and trade terms, raising import duties and input costs—Mexico’s tariff adjustments in 2023 increased food import costs by ~4–6%. Investors should track regional stability since political risk can delay capital expenditures; Alsea invested MXN 3.2bn in 2024 capex across markets.

European Regulatory Integration

Alsea’s sizable footprint in Spain and Europe—over 1,800 stores in Spain and roughly 3,500 European outlets group-wide as of 2025—requires strict compliance with EU directives on food safety, labeling and cross-border data rules; noncompliance risks fines that could affect 2024 EBITDA margins (~12.5%). Changes in EU trade measures or harmonized labor standards, such as minimum wage adjustments (Spain rose to ~€1,200/month in 2024), can raise operating costs for Starbucks and Domino’s, forcing price or margin adjustments. Managing brand consistency across multiple jurisdictions adds governance complexity and potential currency and regulatory translation costs that impact net income variability.

Public Health and Nutrition Policies

Governments in Mexico, Spain and Brazil—key markets for Alsea—are tightening public health rules: Mexico’s front-of-pack labeling affected 50% of packaged products since 2020 and Mexico and Chile have SSB taxes raising prices by up to 8–10%; Brazil and EU members are advancing similar measures through 2024–25.

Alsea must engage policymakers and adapt menus: offering lower-calorie items and clear labeling to meet mandates while preserving brand identity and protecting a 2024 beverage sales mix where sugary drinks still represented about 22% of F&B sales in comparable chains.

Labor Reform and Minimum Wage Legislation

Political movements pushing higher minimum wages and stronger worker protections in Mexico and South America raise Alsea’s labor costs—Mexico’s 2024 minimum wage rose 20% in some zones, while Argentina’s increases averaged 15% in 2024, directly impacting margins across Alsea’s ~4,700 outlets.

New laws on mandatory benefits, limits on working hours and expanded union rights force HR strategy shifts, scheduling changes and higher payroll provisions, increasing operating expenses and compliance risk.

Failure to anticipate these shifts can trigger abrupt cost spikes and strikes; Alsea must model a 5–8% payroll shock scenario in forecasts and maintain contingency cash for labor disputes.

- 2024 Mexico min wage +20% in zones; Argentina avg +15% (2024)

- Alsea ~4,700 outlets exposed across affected markets

- Recommended: model 5–8% payroll shock, increase contingency reserves

Trade Agreements and Import Restrictions

Alsea's cross-border operations depend on steady trade flows; updates to USMCA or regional pacts could shift tariffs on imports like coffee, raising input costs—coffee bean prices averaged 2.40 USD/lb in 2024, up ~18% year-over-year, amplifying risk.

Rising protectionism in key markets (Mexico, Spain, Chile) could add tariffs or non-tariff barriers, disrupting supply chains and increasing COGS, impacting margins for its ~4,500 restaurants in Latin America and Spain.

Alsea margins at risk: Mexico exposure, wage jumps & rising coffee squeeze 2024

Political shifts in Mexico, Spain and Latin America materially affect Alsea’s margins via tariffs, labor and health rules; Mexico ~50% of 2024 revenue, 2024 capex MXN 3.2bn, ~4,700 outlets exposed. Key figures: Mexico min wage +20% (2024), Argentina avg +15% (2024), coffee 2024 USD 2.40/lb (+18% YoY), model 5–8% payroll shock.

| Metric | 2024/2025 Value |

|---|---|

| Mexico revenue share | ~50% |

| Outlets exposed | ~4,700 |

| Capex 2024 | MXN 3.2bn |

| Mexico min wage (2024) | +20% in zones |

| Argentina wage (2024) | +15% avg |

| Coffee price 2024 | USD 2.40/lb (+18% YoY) |

| Payroll shock to model | 5–8% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Alsea across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

Condenses Alsea's full PESTLE into a concise, shareable summary that speeds stakeholder alignment and supports quick decision-making in meetings or pitch decks.

Economic factors

Currency Exchange Rate Fluctuations

Alsea operates in Mexico, Spain, Chile and others, exposing results to MXN/USD and EUR fluctuations; MXN fell ~12% vs USD in 2023 and added FX pressure on 2024 margins. Depreciation in LatAm currencies raises franchise royalties and imported inputs—imported coffee/food costs rose ~8–12% in 2023 in local-currency terms. Alsea reports hedges covering a portion of FX exposure, but sustained currency instability threatens margin preservation.

Inflationary Pressures on Food Commodities

Late 2025 saw dairy, wheat and protein prices swing: global dairy up ~18% YoY, wheat ~12% YoY and protein (beef/poultry) averaging +9% YoY, pressuring Alsea’s COGS for Burger King and Chili’s; effective supply-chain hedging and strategic menu pricing enabled passing ~60–70% of cost increases to consumers, supporting 2025 adjusted EBITDA margin resilience near 11–12%.

Consumer Purchasing Power and Disposable Income

The macro health of Mexico and Europe's middle class drives dining frequency—Mexico's middle class consumption rose 2.3% in 2024 while Eurozone real wages fell 0.5% in 2024, affecting discretionary spend. High interest rates pushed Mexican household credit costs to 27% APR average in 2024, increasing trade-down to QSRs; Spain and Portugal saw similar pressure. Alsea's multi-segment portfolio (Casual, QSR, coffee) lets it capture shifted demand, yet FY2024 revenue growth of 8.6% remained correlated with GDP trends.

Interest Rate Environment and Debt Servicing

Alsea funds expansion largely via debt; as of 2025 net debt/EBITDA was about 2.8x, so the prevailing 2025 Mexican policy rate at ~11.25% and higher global rates raise borrowing costs for new openings and renovations.

Elevated rates have pressured capex cadence—management signaled slower organic openings in 2025 and tighter M&A screening to preserve leverage targets and liquidity.

- Net debt/EBITDA ~2.8x (2025)

- Mexico policy rate ~11.25% (2025)

- Higher rates → slower organic growth, stricter capital allocation

Energy Costs and Operational Overhead

Fluctuating energy prices raised Alsea's utility and logistics costs, with global oil Brent averaging about 85–95 USD/bbl in 2024–2025 and electricity price spikes in Mexico and Spain increasing site-level overheads by an estimated 2–4% of operating expenses.

Energy policy shifts and renewable incentives (e.g., Spain’s auctioned clean-energy contracts, Mexico’s subsidy reforms) create opportunities to reduce costs via on-site solar or long-term power purchase agreements, lowering volatility exposure.

Active management of utilities—energy-efficiency retrofits, centralized logistics routing and hedging—remains critical to protecting margins given 2024 reported adjusted EBITDA pressures and rising input-costs across Alsea’s franchise and corporate stores.

- Brent oil 2024–25: ~85–95 USD/bbl; electricity spikes added ~2–4% to site OPEX

- Renewable PPAs/solar can cut exposure and stabilize costs

- Efficiency retrofits, routing optimization and hedging prioritized to protect adjusted EBITDA

Alsea margins squeezed by FX, commodity costs; pricing lifts 2025 EBITDA to ~11–12%

Alsea faces FX and commodity-driven margin pressure: MXN ~12% weaker vs USD in 2023, imported food costs +8–12% (2023); 2024–25 Brent ~85–95 USD/bbl raised logistics/electricity +2–4% OPEX. Net debt/EBITDA ~2.8x (2025) with Mexico policy rate ~11.25% raising funding costs and slowing openings; menu repricing passed ~60–70% of input inflation, supporting 2025 adj. EBITDA ~11–12%.

| Metric | Value |

|---|---|

| MXN vs USD | -12% (2023) |

| Imported food cost change | +8–12% (2023) |

| Brent oil | 85–95 USD/bbl (2024–25) |

| Net debt/EBITDA | ~2.8x (2025) |

| Mexico policy rate | ~11.25% (2025) |

| Adj. EBITDA margin | ~11–12% (2025) |

What You See Is What You Get

Alsea PESTLE Analysis

The preview shown here is the exact Alsea PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis or presentation.