AltaGas PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, market dynamics, and environmental pressures are reshaping AltaGas’s prospects—our concise PESTLE snapshot highlights the risks and opportunities driving strategic decisions; purchase the full analysis for a complete, actionable briefing you can use in investment theses, board decks, or competitive plans.

Political factors

Cross-border Energy Trade Policies

The close US-Canada relationship shapes AltaGas’s midstream and export strategy, with 2024 cross-border pipeline flows exceeding 8.5 Bcf/d and ~35% of Canadian NGL exports routed to US markets, affecting throughput decisions and FCF forecasts.

Any tariff shifts or renegotiated trade terms could alter transport economics; a 5% tariff on NGLs would raise per-barrel transport costs by an estimated US$0.15–0.25, squeezing margins on export volumes.

Political stability in both countries supports long-term capex—AltaGas’s 2025–2027 planned infrastructure spend (~CAD 600–800m annually) relies on predictable permitting and tariff regimes.

Regulatory Oversight of Utilities

AltaGas operates regulated utilities in Maryland, Virginia and the District of Columbia where combined rate bases exceed US$1.2 billion; shifts in political appointments to state utility commissions can alter allowed returns on equity (ROE) typically ranging 8.5–11%, directly affecting cash flow and coverage ratios for the Utilities segment.

Energy Security and Export Priorities

Government support for LPG exports to Asia remains pivotal for the Ridley Island Propane Export Terminal, with Canada exporting 1.2 million tonnes of propane in 2024 and Asia demand growth projections of ~3–4% annually through 2030 supporting AltaGas's volumes. Political initiatives to bolster energy security and shift from high-carbon fuels have unlocked C$150–200 million in federal infrastructure incentives since 2023, aligning with AltaGas’s midstream strategy. Future growth hinges on continued alignment with federal mandates for energy infrastructure development and timely permitting to capture projected export revenues estimated at US$200–300 million annually by late 2020s.

Indigenous Relations and Land Rights

Political engagement with First Nations is central to AltaGas’s project development; in 2024 AltaGas reported Indigenous agreements covering over 1,200 km of pipeline corridors and partnerships delivering CA$45m in community investment commitments.

Evolving frameworks—Canada’s Duty to Consult and 2021 federal steps toward UNDRIP implementation—add procedural timelines that have delayed some midstream approvals by 6–18 months in recent projects.

Maintaining collaborative partnerships is vital for social license and regulatory approvals, with projects lacking agreements facing higher risk of injunctions and cost overruns often exceeding 10% of capital estimates.

- Indigenous agreements: >1,200 km; CA$45m commitments

- Approval delays: 6–18 months due to consultation/UNDRIP processes

- Financial risk: >10% capital overrun without agreements

Taxation and Fiscal Policy

Changes in corporate tax rates or new energy levies in Canada or the U.S. can reduce AltaGas net income and free cash flow; a 1 percentage-point rise in statutory tax rates could lower after-tax cash flow by an estimated C$15–25m annually based on 2024 EBITDA levels.

Political debates over carbon pricing and clean-energy tax credits—Canada’s SGER/CCIR shifts and U.S. IRA incentives—directly shape AltaGas capital allocation, influencing returns on LNG, renewables, and midstream investments.

Active monitoring of fiscal policy lets AltaGas optimize tax planning and investment mix to preserve margins and access incentives; in 2024 effective tax planning helped sustain adjusted EPS resilience versus peers.

- 1% tax-rate rise ≈ C$15–25m cash-flow impact

- Carbon-pricing shifts alter project NPV and OPEX

- Clean-energy credits (U.S. IRA, Canadian federal incentives) redirect capex

- Fiscal monitoring supports tax-efficiency and portfolio optimization

AltaGas export-led capex plan; Indigenous deals cut delays, tax hike risks CA$15–25m

Cross-border trade (2024: >8.5 Bcf/d pipeline flows; ~35% Canadian NGLs to US) and stable US/Canadian politics underpin AltaGas’s export and capex plans (2025–27: CA$600–800m/yr); Indigenous agreements (>1,200 km; CA$45m commitments) reduce approval delays (historically 6–18 months) and >10% capex overrun risk; 1ppt tax rise ≈ CA$15–25m cash-flow hit; propane exports 2024: 1.2mt.

| Metric | 2024 / Impact |

|---|---|

| Cross-border flows | >8.5 Bcf/d |

| Canadian NGL to US | ~35% |

| Propane exports | 1.2 mt |

| Indigenous agreements | >1,200 km; CA$45m |

| Approval delays | 6–18 months |

| Tax sensitivity | 1ppt ≈ CA$15–25m |

What is included in the product

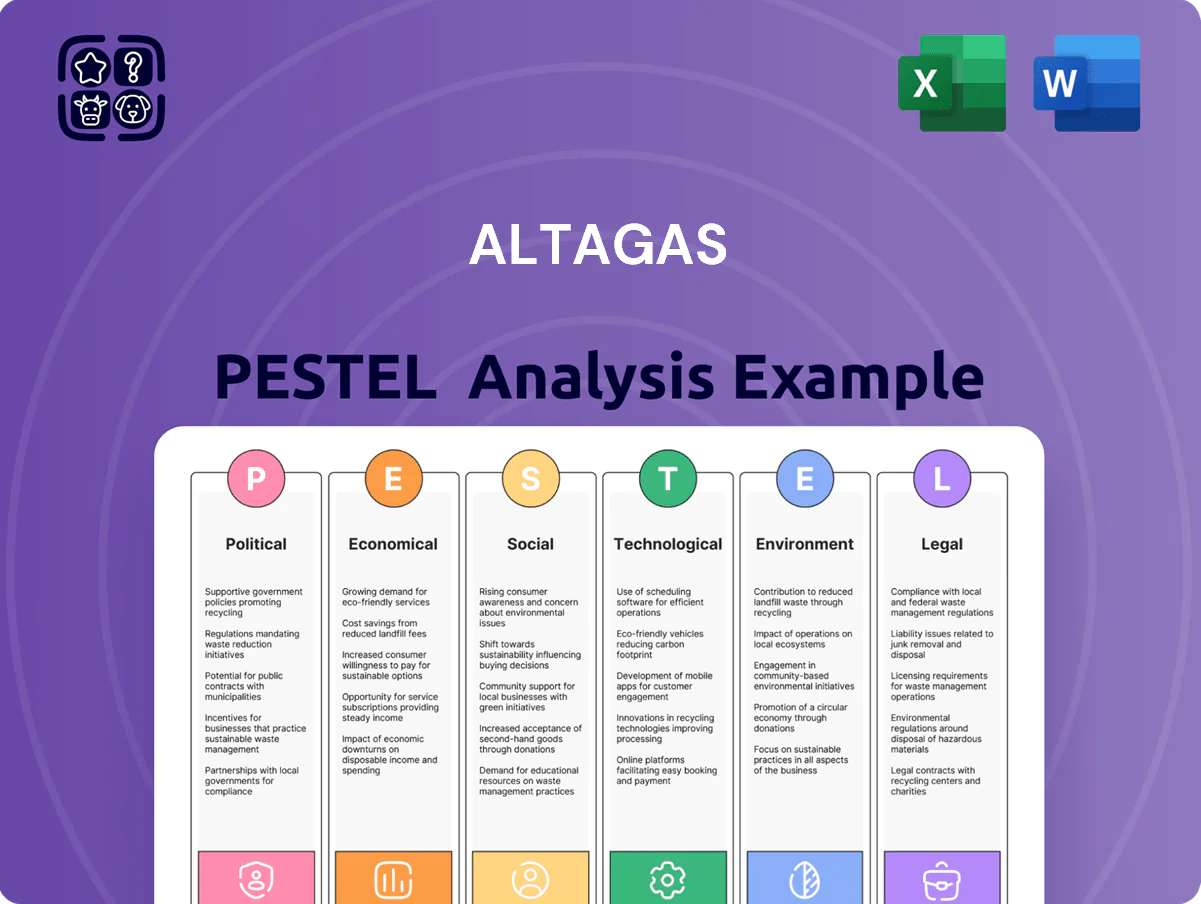

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect AltaGas, using current market and regulatory dynamics to identify risks and opportunities across its North American midstream and utilities operations.

A concise, shareable AltaGas PESTLE summary that’s visually segmented by category for quick interpretation, easily dropped into presentations or planning sessions to align teams and support discussions on external risk and market positioning.

Economic factors

Interest Rate Environment

As a capital-intensive utility with about CAD 6.8 billion of debt at YE 2024, AltaGas is highly sensitive to Bank of Canada rate moves; each 100 bp rise can materially raise annual interest expense and depress regulated-asset valuations used in rate base calculations.

Rising global rates through 2022–24 tightened financing costs, but a stabilizing policy outlook in late 2025—BoC at 4.25% and falling volatility—improves certainty for long-term project financing and supports dividend planning.

Natural Gas and NGL Price Volatility

While AltaGas utilities are largely insulated, Midstream profitability hinges on NGL price spreads; in 2024 propane averaged about US$0.58/gal in North America with Asia premiums lifting export margins, and AltaGas reported midstream adjusted EBITDA volatility of ±12% year-on-year in 2023–24 tied to spreads. Throughput at Ridley Island and other export terminals closely tracks Asian demand cycles, and Hedging (fixed-price contracts covering ~40–60% of volumes) limits but does not eliminate macro-driven revenue swings.

Inflationary Pressures on Operations

Persistent inflation raised Canadian CPI to 3.4% in 2024, increasing AltaGas labor, materials and maintenance costs; Q3 2024 operating expenses rose about 5–7% year-over-year, pressuring margins. AltaGas relies on utility rate filings to recover costs, but regulatory lag can delay reimbursement, squeezing cash flow. Higher steel and contractor rates—steel up ~15% vs 2022—risk budget overruns on midstream expansions, increasing capex forecasts.

Currency Exchange Rate Fluctuations

AltaGas earns a large share of revenue in USD while reporting in CAD; a 10% CAD weakening vs USD in 2024 would have increased translated EBITDA by roughly CAD 40–60 million given the company’s reported U.S.-linked cash flows (2024 guidance midpoint context).

The firm uses forward contracts and cross-currency swaps to hedge short- to medium-term exposure, but unhedged net assets and long-duration contracts leave results sensitive to multi-year CAD/USD trends;

Consumer Purchasing Power

The economic health of residential and commercial customers in the U.S. Northeast drives natural gas consumption; New England unemployment averaged 4.1% in 2024 and real household disposable income rose 1.8% YoY, supporting demand.

Economic downturns can cut gas usage and raise delinquencies—AltaGas saw Northeast utility arrears jump 22% during 2020 stress; similar contractions would pressure cash flows.

Stable regional GDP growth (New England GDP +1.5% in 2024) is essential for steady regulated business performance and revenue predictability.

- Unemployment NE 2024: 4.1%

- Real disposable income 2024: +1.8% YoY

- New England GDP 2024: +1.5%

- Utility arrears spike in downturns: +22% (2020)

AltaGas faces rate risk: CAD6.8B debt, BoC hikes lift costs; FX, propane drive EBITDA

AltaGas' CAD 6.8B debt makes it rate-sensitive; BoC at 4.25% (late 2025) raises interest costs and affects rate-base valuations. Midstream EBITDA ±12% YoY (2023–24) tracks NGL spreads—propane ≈ US$0.58/gal (2024) with exports aided by Asia premiums; hedges cover ~40–60% volumes. CPI 2024: 3.4% drove opex +5–7% YoY; USD revenue exposure means a 10% CAD move ≈ CAD 40–60M EBITDA impact.

| Metric | 2024/2025 |

|---|---|

| Debt (YE 2024) | CAD 6.8B |

| BoC rate (late 2025) | 4.25% |

| Propane (NA, 2024) | US$0.58/gal |

| CPI (Canada, 2024) | 3.4% |

| Midstream EBITDA vol. | ±12% YoY |

| Hedge coverage | 40–60% vols |

| FX sensitivity | 10% CAD move ≈ CAD 40–60M EBITDA |

Full Version Awaits

AltaGas PESTLE Analysis

The preview shown here is the exact AltaGas PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are precisely what you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, market dynamics, and environmental pressures are reshaping AltaGas’s prospects—our concise PESTLE snapshot highlights the risks and opportunities driving strategic decisions; purchase the full analysis for a complete, actionable briefing you can use in investment theses, board decks, or competitive plans.

Political factors

Cross-border Energy Trade Policies

The close US-Canada relationship shapes AltaGas’s midstream and export strategy, with 2024 cross-border pipeline flows exceeding 8.5 Bcf/d and ~35% of Canadian NGL exports routed to US markets, affecting throughput decisions and FCF forecasts.

Any tariff shifts or renegotiated trade terms could alter transport economics; a 5% tariff on NGLs would raise per-barrel transport costs by an estimated US$0.15–0.25, squeezing margins on export volumes.

Political stability in both countries supports long-term capex—AltaGas’s 2025–2027 planned infrastructure spend (~CAD 600–800m annually) relies on predictable permitting and tariff regimes.

Regulatory Oversight of Utilities

AltaGas operates regulated utilities in Maryland, Virginia and the District of Columbia where combined rate bases exceed US$1.2 billion; shifts in political appointments to state utility commissions can alter allowed returns on equity (ROE) typically ranging 8.5–11%, directly affecting cash flow and coverage ratios for the Utilities segment.

Energy Security and Export Priorities

Government support for LPG exports to Asia remains pivotal for the Ridley Island Propane Export Terminal, with Canada exporting 1.2 million tonnes of propane in 2024 and Asia demand growth projections of ~3–4% annually through 2030 supporting AltaGas's volumes. Political initiatives to bolster energy security and shift from high-carbon fuels have unlocked C$150–200 million in federal infrastructure incentives since 2023, aligning with AltaGas’s midstream strategy. Future growth hinges on continued alignment with federal mandates for energy infrastructure development and timely permitting to capture projected export revenues estimated at US$200–300 million annually by late 2020s.

Indigenous Relations and Land Rights

Political engagement with First Nations is central to AltaGas’s project development; in 2024 AltaGas reported Indigenous agreements covering over 1,200 km of pipeline corridors and partnerships delivering CA$45m in community investment commitments.

Evolving frameworks—Canada’s Duty to Consult and 2021 federal steps toward UNDRIP implementation—add procedural timelines that have delayed some midstream approvals by 6–18 months in recent projects.

Maintaining collaborative partnerships is vital for social license and regulatory approvals, with projects lacking agreements facing higher risk of injunctions and cost overruns often exceeding 10% of capital estimates.

- Indigenous agreements: >1,200 km; CA$45m commitments

- Approval delays: 6–18 months due to consultation/UNDRIP processes

- Financial risk: >10% capital overrun without agreements

Taxation and Fiscal Policy

Changes in corporate tax rates or new energy levies in Canada or the U.S. can reduce AltaGas net income and free cash flow; a 1 percentage-point rise in statutory tax rates could lower after-tax cash flow by an estimated C$15–25m annually based on 2024 EBITDA levels.

Political debates over carbon pricing and clean-energy tax credits—Canada’s SGER/CCIR shifts and U.S. IRA incentives—directly shape AltaGas capital allocation, influencing returns on LNG, renewables, and midstream investments.

Active monitoring of fiscal policy lets AltaGas optimize tax planning and investment mix to preserve margins and access incentives; in 2024 effective tax planning helped sustain adjusted EPS resilience versus peers.

- 1% tax-rate rise ≈ C$15–25m cash-flow impact

- Carbon-pricing shifts alter project NPV and OPEX

- Clean-energy credits (U.S. IRA, Canadian federal incentives) redirect capex

- Fiscal monitoring supports tax-efficiency and portfolio optimization

AltaGas export-led capex plan; Indigenous deals cut delays, tax hike risks CA$15–25m

Cross-border trade (2024: >8.5 Bcf/d pipeline flows; ~35% Canadian NGLs to US) and stable US/Canadian politics underpin AltaGas’s export and capex plans (2025–27: CA$600–800m/yr); Indigenous agreements (>1,200 km; CA$45m commitments) reduce approval delays (historically 6–18 months) and >10% capex overrun risk; 1ppt tax rise ≈ CA$15–25m cash-flow hit; propane exports 2024: 1.2mt.

| Metric | 2024 / Impact |

|---|---|

| Cross-border flows | >8.5 Bcf/d |

| Canadian NGL to US | ~35% |

| Propane exports | 1.2 mt |

| Indigenous agreements | >1,200 km; CA$45m |

| Approval delays | 6–18 months |

| Tax sensitivity | 1ppt ≈ CA$15–25m |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect AltaGas, using current market and regulatory dynamics to identify risks and opportunities across its North American midstream and utilities operations.

A concise, shareable AltaGas PESTLE summary that’s visually segmented by category for quick interpretation, easily dropped into presentations or planning sessions to align teams and support discussions on external risk and market positioning.

Economic factors

Interest Rate Environment

As a capital-intensive utility with about CAD 6.8 billion of debt at YE 2024, AltaGas is highly sensitive to Bank of Canada rate moves; each 100 bp rise can materially raise annual interest expense and depress regulated-asset valuations used in rate base calculations.

Rising global rates through 2022–24 tightened financing costs, but a stabilizing policy outlook in late 2025—BoC at 4.25% and falling volatility—improves certainty for long-term project financing and supports dividend planning.

Natural Gas and NGL Price Volatility

While AltaGas utilities are largely insulated, Midstream profitability hinges on NGL price spreads; in 2024 propane averaged about US$0.58/gal in North America with Asia premiums lifting export margins, and AltaGas reported midstream adjusted EBITDA volatility of ±12% year-on-year in 2023–24 tied to spreads. Throughput at Ridley Island and other export terminals closely tracks Asian demand cycles, and Hedging (fixed-price contracts covering ~40–60% of volumes) limits but does not eliminate macro-driven revenue swings.

Inflationary Pressures on Operations

Persistent inflation raised Canadian CPI to 3.4% in 2024, increasing AltaGas labor, materials and maintenance costs; Q3 2024 operating expenses rose about 5–7% year-over-year, pressuring margins. AltaGas relies on utility rate filings to recover costs, but regulatory lag can delay reimbursement, squeezing cash flow. Higher steel and contractor rates—steel up ~15% vs 2022—risk budget overruns on midstream expansions, increasing capex forecasts.

Currency Exchange Rate Fluctuations

AltaGas earns a large share of revenue in USD while reporting in CAD; a 10% CAD weakening vs USD in 2024 would have increased translated EBITDA by roughly CAD 40–60 million given the company’s reported U.S.-linked cash flows (2024 guidance midpoint context).

The firm uses forward contracts and cross-currency swaps to hedge short- to medium-term exposure, but unhedged net assets and long-duration contracts leave results sensitive to multi-year CAD/USD trends;

Consumer Purchasing Power

The economic health of residential and commercial customers in the U.S. Northeast drives natural gas consumption; New England unemployment averaged 4.1% in 2024 and real household disposable income rose 1.8% YoY, supporting demand.

Economic downturns can cut gas usage and raise delinquencies—AltaGas saw Northeast utility arrears jump 22% during 2020 stress; similar contractions would pressure cash flows.

Stable regional GDP growth (New England GDP +1.5% in 2024) is essential for steady regulated business performance and revenue predictability.

- Unemployment NE 2024: 4.1%

- Real disposable income 2024: +1.8% YoY

- New England GDP 2024: +1.5%

- Utility arrears spike in downturns: +22% (2020)

AltaGas faces rate risk: CAD6.8B debt, BoC hikes lift costs; FX, propane drive EBITDA

AltaGas' CAD 6.8B debt makes it rate-sensitive; BoC at 4.25% (late 2025) raises interest costs and affects rate-base valuations. Midstream EBITDA ±12% YoY (2023–24) tracks NGL spreads—propane ≈ US$0.58/gal (2024) with exports aided by Asia premiums; hedges cover ~40–60% volumes. CPI 2024: 3.4% drove opex +5–7% YoY; USD revenue exposure means a 10% CAD move ≈ CAD 40–60M EBITDA impact.

| Metric | 2024/2025 |

|---|---|

| Debt (YE 2024) | CAD 6.8B |

| BoC rate (late 2025) | 4.25% |

| Propane (NA, 2024) | US$0.58/gal |

| CPI (Canada, 2024) | 3.4% |

| Midstream EBITDA vol. | ±12% YoY |

| Hedge coverage | 40–60% vols |

| FX sensitivity | 10% CAD move ≈ CAD 40–60M EBITDA |

Full Version Awaits

AltaGas PESTLE Analysis

The preview shown here is the exact AltaGas PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are precisely what you’ll download immediately after payment.