Altus Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

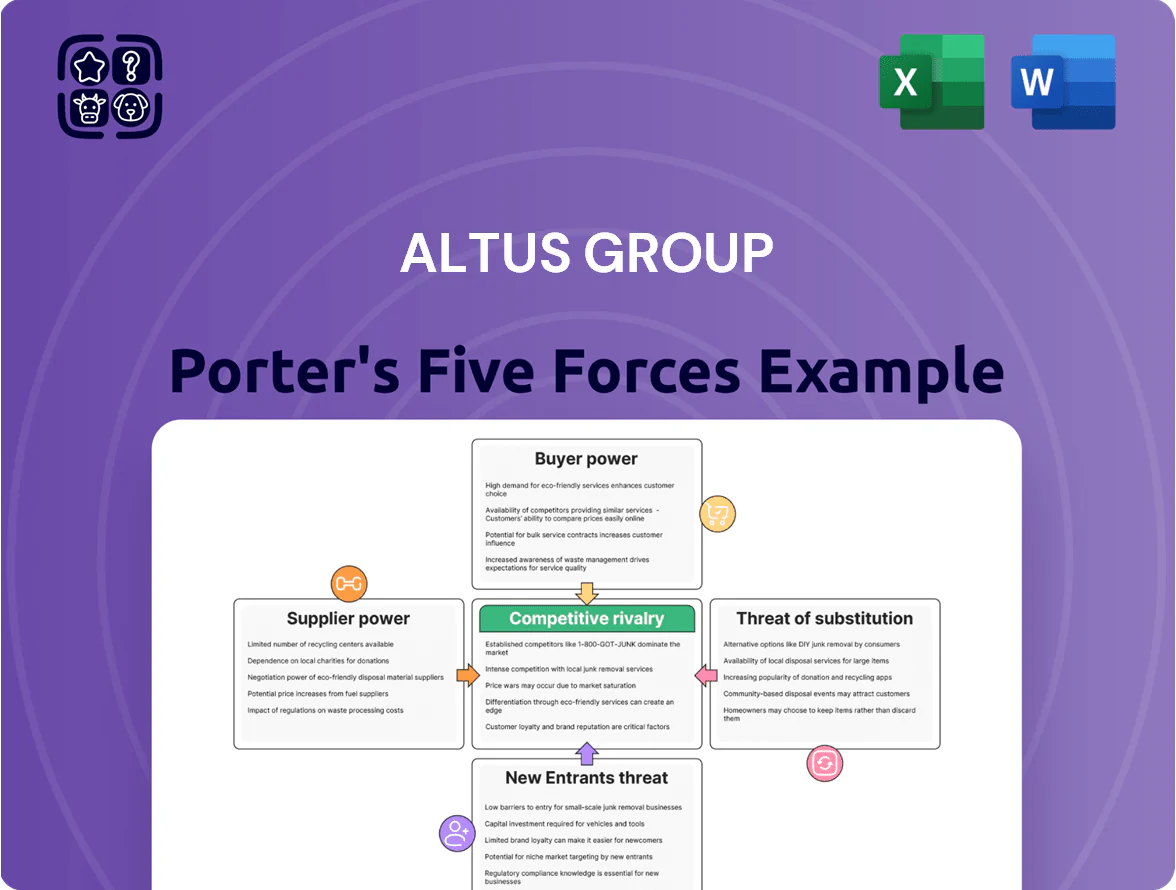

Altus Group faces a mix of concentrated buyer power, technology-driven substitutes, and regulatory complexity that shape its competitive positioning and margins—this snapshot highlights key pressures but omits detailed scoring, trend analysis, and tactical implications.

Suppliers Bargaining Power

Specialized Technology Talent

The competition for cloud and AI engineers stayed intense into 2025, with US median software engineer salaries rising ~8% year-over-year to about $150,000 and cloud/AI specialists commanding premiums of 15–30% per Dice and LinkedIn data.

Altus Group depends on these skills to maintain ARGUS and analytics; tech staffing made up an estimated 22% of its FY2024 SG&A, so talent cost swings hit margins directly.

High demand gives individual developers and tech leads leverage to push for higher pay, equity, and remote work, raising retention and hiring costs for Altus.

Cloud Infrastructure Providers

Altus Group increasingly depends on major cloud providers such as Microsoft Azure and Amazon Web Services to host its SaaS products, exposing it to an oligopoly where Azure and AWS held ~62% global IaaS/PaaS market share in 2024 (Synergy Research).

These providers can set pricing and SLA terms; a 20–40% migration cost premium and multi-month replatforming timelines make switching costly for Altus.

High vendor lock-in means supplier bargaining power is strong, pressuring margins and contract flexibility for Altus.

Third-party Data Sources

Altus Group (TSX: AIF) builds deep proprietary datasets but still buys government land registries, municipal tax rolls, and niche feeds; in 2024 roughly 18% of its data inputs came from third parties, per company filings.

Suppliers can raise subscription fees or tighten APIs, squeezing Altus’s margins—if a key feed rose 10% it could cut segment EBIT by ~30–50 bps.

Because timely, accurate data drives advisory fees and valuations, these vendors are operationally critical and wield meaningful short-term leverage.

Professional Certification Bodies

Altus relies on designated appraisers and tax consultants who must hold credentials from bodies like the Appraisal Institute or RICS; as of 2025, RICS reports 140,000 global members, while the Appraisal Institute has ~22,000 U.S. members, constraining available talent.

These bodies set exams and CPD rules that throttle supply, raising hiring costs—industry data show certified appraiser salaries 15–30% above non-certified peers, increasing operating payroll pressure for Altus.

Specialized Hardware and Security Vendors

Specialized security hardware and software vendors force Altus Group to buy advanced protections as cyber threats rise; Gartner reported global security spending hit 188B in 2023 and reached ~210B in 2024, so vendor leverage is high.

These suppliers guard client financial data and proprietary valuation models, making vendor changes costly; a 2022 IBM breach study put average breach cost at 4.35M, raising Altus price sensitivity.

Because breaches are expensive, Altus has little room to push back on protocol or price updates, increasing supplier bargaining power and contract lock-in risk.

- Security spend rising: ~210B global 2024 (Gartner)

- Avg breach cost: 4.35M (IBM 2022)

- High dependency on specialized vendors → low negotiation leverage

Supplier dominance bites margins: cloud, security, staffing and appraisers drive pricing risk

Suppliers hold strong bargaining power: cloud providers (Azure+AWS ~62% IaaS/PaaS share 2024) and security vendors (global spend ~$210B 2024) create lock-in and pricing pressure; tech staffing (~22% FY2024 SG&A) and certified appraisers (RICS ~140,000; Appraisal Institute ~22,000 in 2025) command pay premia (15–30%), any 10% data-feed price rise could cut segment EBIT ~30–50 bps.

| Supplier | Key stat |

|---|---|

| Azure+AWS | ~62% IaaS/PaaS (2024) |

| Security spend | ~$210B (2024) |

| Tech staffing | ~22% SG&A (FY2024) |

| Certified appraisers | RICS 140,000; Appraisal Institute 22,000 (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Altus Group that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its market position.

A concise Porter's Five Forces one-sheet for Altus Group—quickly view competitive pressures and relieve decision-making pain with an easy-to-read radar chart and customizable pressure sliders.

Customers Bargaining Power

High Switching Costs for ARGUS Users

The ARGUS software suite is the commercial real estate standard, used by an estimated 60–70% of large CRE firms as of 2024, creating high switching costs; firms report migration projects often exceed $1m and 6–12 months, including retraining and data conversion. This technical lock-in cuts customer bargaining power—even large clients face steep exit costs and limited leverage over Altus Group’s pricing and update cadence.

Concentration of Institutional Investors

A large share of Altus Group’s 2024 revenue—about 48% of reported recurring fees—comes from roughly 12 major clients, including REITs, global banks, and pension funds; these institutional buyers negotiate volume discounts and bespoke service SLAs. Their scale lets them push prices down and demand data-integrated solutions, raising Altus’s customer concentration risk. If a top-five client (≈22% revenue) shifts providers at renewal, Altus faces immediate revenue and margin pressure.

Price Sensitivity in Advisory Services

In Altus Group’s property tax and cost consulting, clients treat work as transactional, so fees are easily compared to boutiques and local firms; a 2024 survey showed 62% of commercial property owners shop multiple consultants for price.

High price sensitivity forces Altus to prove superior ROI—Altus reported 18% higher recovery rates on tax appeals in 2023—so maintaining premium pricing requires continuous outcome evidence and case-level savings data.

Demand for Integrated Data Solutions

Modern real estate investors want one-stop providers offering software, data, and advisory, so clients push Altus Group for bundled discounts and deeper integration; in 2024, 62% of CRE firms preferred integrated platforms, raising negotiation leverage.

Data democratization and cheaper cloud tools let buyers threaten insourcing: building internal data teams can cost 30–50% less over five years for mid-size firms, increasing customer bargaining power.

- 62% of CRE firms prefer integrated platforms (2024 survey)

- Clients demand bundled discounts and tighter API/UX integration

- Insourcing data teams can cut 5-year costs by 30–50% for mid-size firms

- Altus faces pricing pressure and must enhance product bundling

Access to Alternative Boutique Consultants

Altus Group's global reach is constrained by customers' access to local boutique consultants for property tax and development advisory; in 2024 an estimated 35% of North American mid-market clients used local specialists for cost or service reasons.

Smaller firms' lower overhead and bespoke service give clients a viable fallback, so Altus cannot sharply raise fees in specific markets without risking churn.

Concentrated revenue empowers buyers: ARGUS lock-in vs. discount-seeking top clients

Customers hold moderate bargaining power: ARGUS lock-in (60–70% large-firm share, migrations >$1m/6–12m) reduces churn, but top-12 clients drive ~48% recurring revenue (top-5 ≈22%), pushing for discounts and SLAs; 62% prefer integrated platforms; 62% shop consultants for tax work; insourcing can cut 5-year costs 30–50%, and ~35% mid-market use local specialists.

| Metric | 2024/2025 |

|---|---|

| ARGUS share | 60–70% |

| Migration cost/time | $1m+, 6–12m |

| Recurring revenue from top-12 | 48% |

| Top-5 revenue | ≈22% |

| Prefer integrated | 62% |

| Shop consultants | 62% |

| Insourcing 5yr cost cut | 30–50% |

| Mid-market use local | ≈35% |

What You See Is What You Get

Altus Group Porter's Five Forces Analysis

This preview shows the exact Altus Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders, fully formatted and ready for use.

The document displayed here is a portion of the full, professionally written analysis you'll be able to download the moment you buy, containing the same insights, data and structure.

No mockups or samples: this is the actual deliverable, available instantly after payment and requiring no additional setup or customization.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Altus Group faces a mix of concentrated buyer power, technology-driven substitutes, and regulatory complexity that shape its competitive positioning and margins—this snapshot highlights key pressures but omits detailed scoring, trend analysis, and tactical implications.

Suppliers Bargaining Power

Specialized Technology Talent

The competition for cloud and AI engineers stayed intense into 2025, with US median software engineer salaries rising ~8% year-over-year to about $150,000 and cloud/AI specialists commanding premiums of 15–30% per Dice and LinkedIn data.

Altus Group depends on these skills to maintain ARGUS and analytics; tech staffing made up an estimated 22% of its FY2024 SG&A, so talent cost swings hit margins directly.

High demand gives individual developers and tech leads leverage to push for higher pay, equity, and remote work, raising retention and hiring costs for Altus.

Cloud Infrastructure Providers

Altus Group increasingly depends on major cloud providers such as Microsoft Azure and Amazon Web Services to host its SaaS products, exposing it to an oligopoly where Azure and AWS held ~62% global IaaS/PaaS market share in 2024 (Synergy Research).

These providers can set pricing and SLA terms; a 20–40% migration cost premium and multi-month replatforming timelines make switching costly for Altus.

High vendor lock-in means supplier bargaining power is strong, pressuring margins and contract flexibility for Altus.

Third-party Data Sources

Altus Group (TSX: AIF) builds deep proprietary datasets but still buys government land registries, municipal tax rolls, and niche feeds; in 2024 roughly 18% of its data inputs came from third parties, per company filings.

Suppliers can raise subscription fees or tighten APIs, squeezing Altus’s margins—if a key feed rose 10% it could cut segment EBIT by ~30–50 bps.

Because timely, accurate data drives advisory fees and valuations, these vendors are operationally critical and wield meaningful short-term leverage.

Professional Certification Bodies

Altus relies on designated appraisers and tax consultants who must hold credentials from bodies like the Appraisal Institute or RICS; as of 2025, RICS reports 140,000 global members, while the Appraisal Institute has ~22,000 U.S. members, constraining available talent.

These bodies set exams and CPD rules that throttle supply, raising hiring costs—industry data show certified appraiser salaries 15–30% above non-certified peers, increasing operating payroll pressure for Altus.

Specialized Hardware and Security Vendors

Specialized security hardware and software vendors force Altus Group to buy advanced protections as cyber threats rise; Gartner reported global security spending hit 188B in 2023 and reached ~210B in 2024, so vendor leverage is high.

These suppliers guard client financial data and proprietary valuation models, making vendor changes costly; a 2022 IBM breach study put average breach cost at 4.35M, raising Altus price sensitivity.

Because breaches are expensive, Altus has little room to push back on protocol or price updates, increasing supplier bargaining power and contract lock-in risk.

- Security spend rising: ~210B global 2024 (Gartner)

- Avg breach cost: 4.35M (IBM 2022)

- High dependency on specialized vendors → low negotiation leverage

Supplier dominance bites margins: cloud, security, staffing and appraisers drive pricing risk

Suppliers hold strong bargaining power: cloud providers (Azure+AWS ~62% IaaS/PaaS share 2024) and security vendors (global spend ~$210B 2024) create lock-in and pricing pressure; tech staffing (~22% FY2024 SG&A) and certified appraisers (RICS ~140,000; Appraisal Institute ~22,000 in 2025) command pay premia (15–30%), any 10% data-feed price rise could cut segment EBIT ~30–50 bps.

| Supplier | Key stat |

|---|---|

| Azure+AWS | ~62% IaaS/PaaS (2024) |

| Security spend | ~$210B (2024) |

| Tech staffing | ~22% SG&A (FY2024) |

| Certified appraisers | RICS 140,000; Appraisal Institute 22,000 (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Altus Group that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its market position.

A concise Porter's Five Forces one-sheet for Altus Group—quickly view competitive pressures and relieve decision-making pain with an easy-to-read radar chart and customizable pressure sliders.

Customers Bargaining Power

High Switching Costs for ARGUS Users

The ARGUS software suite is the commercial real estate standard, used by an estimated 60–70% of large CRE firms as of 2024, creating high switching costs; firms report migration projects often exceed $1m and 6–12 months, including retraining and data conversion. This technical lock-in cuts customer bargaining power—even large clients face steep exit costs and limited leverage over Altus Group’s pricing and update cadence.

Concentration of Institutional Investors

A large share of Altus Group’s 2024 revenue—about 48% of reported recurring fees—comes from roughly 12 major clients, including REITs, global banks, and pension funds; these institutional buyers negotiate volume discounts and bespoke service SLAs. Their scale lets them push prices down and demand data-integrated solutions, raising Altus’s customer concentration risk. If a top-five client (≈22% revenue) shifts providers at renewal, Altus faces immediate revenue and margin pressure.

Price Sensitivity in Advisory Services

In Altus Group’s property tax and cost consulting, clients treat work as transactional, so fees are easily compared to boutiques and local firms; a 2024 survey showed 62% of commercial property owners shop multiple consultants for price.

High price sensitivity forces Altus to prove superior ROI—Altus reported 18% higher recovery rates on tax appeals in 2023—so maintaining premium pricing requires continuous outcome evidence and case-level savings data.

Demand for Integrated Data Solutions

Modern real estate investors want one-stop providers offering software, data, and advisory, so clients push Altus Group for bundled discounts and deeper integration; in 2024, 62% of CRE firms preferred integrated platforms, raising negotiation leverage.

Data democratization and cheaper cloud tools let buyers threaten insourcing: building internal data teams can cost 30–50% less over five years for mid-size firms, increasing customer bargaining power.

- 62% of CRE firms prefer integrated platforms (2024 survey)

- Clients demand bundled discounts and tighter API/UX integration

- Insourcing data teams can cut 5-year costs by 30–50% for mid-size firms

- Altus faces pricing pressure and must enhance product bundling

Access to Alternative Boutique Consultants

Altus Group's global reach is constrained by customers' access to local boutique consultants for property tax and development advisory; in 2024 an estimated 35% of North American mid-market clients used local specialists for cost or service reasons.

Smaller firms' lower overhead and bespoke service give clients a viable fallback, so Altus cannot sharply raise fees in specific markets without risking churn.

Concentrated revenue empowers buyers: ARGUS lock-in vs. discount-seeking top clients

Customers hold moderate bargaining power: ARGUS lock-in (60–70% large-firm share, migrations >$1m/6–12m) reduces churn, but top-12 clients drive ~48% recurring revenue (top-5 ≈22%), pushing for discounts and SLAs; 62% prefer integrated platforms; 62% shop consultants for tax work; insourcing can cut 5-year costs 30–50%, and ~35% mid-market use local specialists.

| Metric | 2024/2025 |

|---|---|

| ARGUS share | 60–70% |

| Migration cost/time | $1m+, 6–12m |

| Recurring revenue from top-12 | 48% |

| Top-5 revenue | ≈22% |

| Prefer integrated | 62% |

| Shop consultants | 62% |

| Insourcing 5yr cost cut | 30–50% |

| Mid-market use local | ≈35% |

What You See Is What You Get

Altus Group Porter's Five Forces Analysis

This preview shows the exact Altus Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders, fully formatted and ready for use.

The document displayed here is a portion of the full, professionally written analysis you'll be able to download the moment you buy, containing the same insights, data and structure.

No mockups or samples: this is the actual deliverable, available instantly after payment and requiring no additional setup or customization.