Alumasc Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

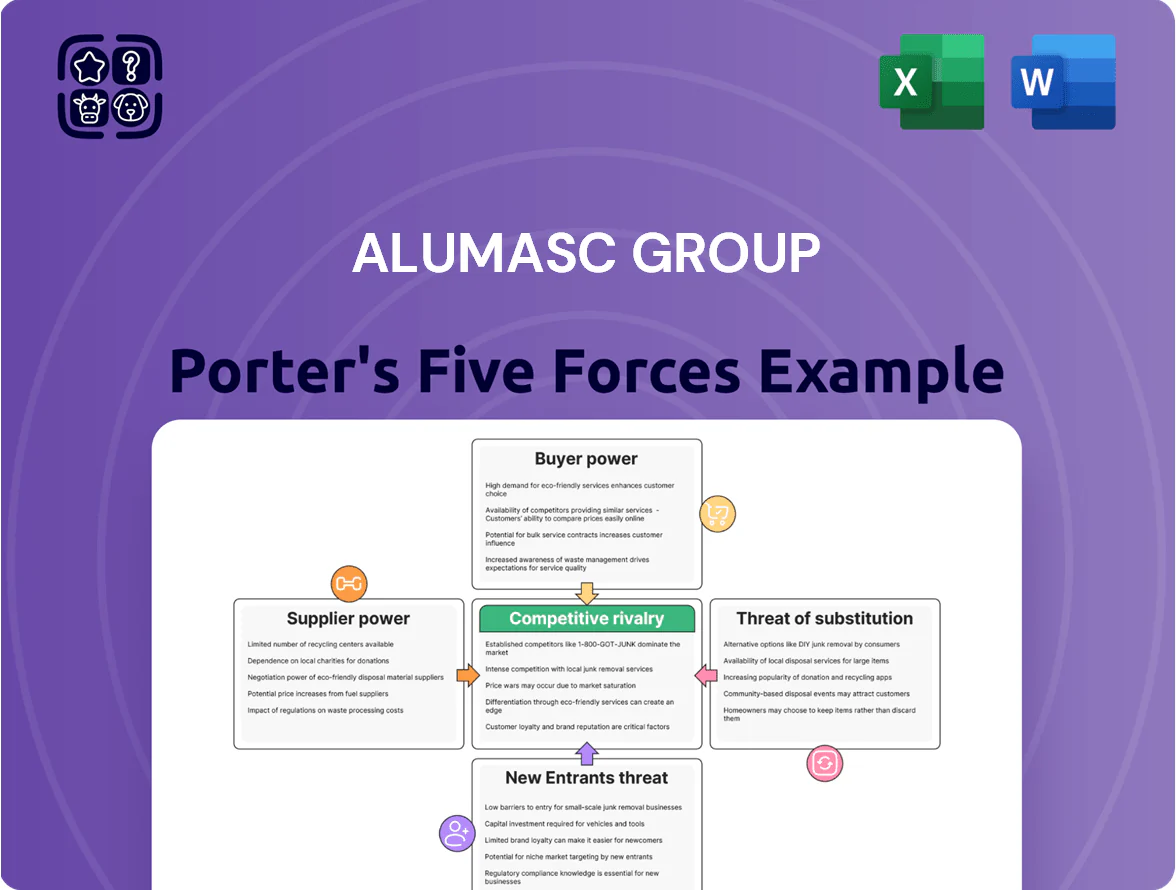

Alumasc Group faces moderate buyer power, niche supplier relationships, and steady threat from substitutes driven by sustainable building trends, while regulatory and scale barriers temper new entrants and competitive rivalry remains focused on product differentiation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Alumasc Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in raw material commodity pricing

Alumasc relies on aluminum, steel and specialized polymers; by late 2025 demand for low-carbon aluminum raised supplier leverage as certified metal prices climbed ~12–18% vs 2023, per London Metal Exchange and industry reports, forcing higher input costs or sourcing delays.

Energy costs for primary manufacturing

Energy costs heavily affect Alumasc Group's primary manufacturing; precision engineering and metal fabrication can consume 200–400 kWh per tonne, pushing energy to ~6–12% of COGS based on 2024 industry averages.

Suppliers of electricity and carbon‑intensive inputs pass through UK grid price swings and the UK ETS carbon costs, which rose to ~£45/t CO2 in 2024, directly inflating Alumasc's input costs.

That pass‑through and volatile wholesale prices (UK day‑ahead averages spiking 60% in 2022–24) restrict Alumasc's ability to secure long fixed‑rate contracts without price risk.

Specialized technical components

Alumasc relies on high-performance seals and electronic monitors for its water-management and roofing systems, and only a handful of UK/EU suppliers meet the technical and BSI/CE regulatory standards; supplier concentration raises bargaining power. In 2024, industry reports show top 5 niche component makers control ~60% of the market for certified roofing electronics, pressuring margins—Alumasc faces supply-risk and potential 3–5% input-cost shocks.

Logistics and transportation constraints

The movement of bulky building products depends on a strained logistics network that saw UK HGV driver shortages of ~20% and diesel price swings of ±18% in 2025, raising transport costs for Alumasc.

Third-party logistics firms prioritized large-volume clients, forcing mid-sized suppliers like Alumasc to pay delivery-premiums reported at 5–12% for guaranteed slots.

Efficient distribution remains critical for Alumasc to protect its reliability in construction projects and avoid order delays that can hit revenue and margins.

- UK HGV driver shortfall ~20% (2025)

- Diesel price volatility ±18% (2025)

- Delivery-premiums paid 5–12%

- High-volume clients prioritized by 3PLs

Supplier integration and market position

Upstream suppliers are moving into forward integration, selling prefabricated components directly to developers, cutting into Alumasc Group’s sub-assembly margins and lowering its procurement leverage.

Alumasc must reinforce supplier ties and secure long-term contracts; in 2024 UK construction prefabrication grew ~9% and supplier-assisted projects rose, raising competitive risk.

High supplier power: concentrated low‑carbon supply, rising energy/ETS & logistics costs

Supplier power is high: certified low‑carbon aluminium/precision components are concentrated (top‑5 ~60%), energy and UK ETS costs (£45/t CO2 in 2024) push COGS 6–12%, logistics shocks (HGV shortfall ~20% in 2025, diesel ±18%) add 5–12% delivery premiums, and upstream forward integration (prefab +9% in 2024) reduces procurement leverage.

| Metric | Value |

|---|---|

| Top‑5 component share | ~60% |

| UK ETS price (2024) | £45/t CO2 |

| Energy share of COGS | 6–12% |

| HGV shortfall (2025) | ~20% |

| Diesel volatility (2025) | ±18% |

| Delivery premiums | 5–12% |

| Prefab growth (UK 2024) | +9% |

What is included in the product

Tailored Porter's Five Forces for Alumasc Group: analyzes competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifies disruptive forces and market entry barriers shaping its pricing power and profitability.

A concise, one-sheet Porter's Five Forces view of Alumasc Group—quickly pinpoint competitive pressures and relief strategies for boardrooms and investor decks.

Customers Bargaining Power

Consolidation of major Tier 1 contractors

Influence of architects and specifiers

Demand for ESG and carbon transparency

By 2025 buyers demand detailed Environmental Product Declarations (EPDs) and proof of low embodied carbon; 68% of UK construction clients stated EPDs as mandatory in 2024 procurement, forcing suppliers to comply.

Customers can reject non-compliant vendors, and large contractors wield outsized power—Top 10 UK housebuilders represent ~40% of sector spend—making ESG a de facto entry requirement.

For Alumasc, this shifts R&D and product specs toward low-carbon formulations and verified EPDs, risking lost contracts if it lags; a 5–10% revenue hit is plausible for delayed compliance.

Availability of alternative sourcing channels

The rise of digital procurement platforms lets buyers compare Alumasc’s water-management and roofing products with international suppliers in real time, increasing price pressure and eroding brand-based information asymmetry.

In 2024, global B2B e‑commerce surpassed $25.6 trillion (UNCTAD), and UK construction firms reported 34% higher use of online sourcing vs. 2019, enabling sourcing from lower‑cost markets and compressing Alumasc’s margins.

- Real‑time comparisons raise price competition

- Online sourcing cuts information asymmetry

- Global suppliers offer lower overheads

- 2024 B2B e‑commerce: $25.6T (UNCTAD)

Cyclical nature of the residential housing market

The bargaining power of residential developers shifts with the UK housing cycle; housing starts fell 18% YoY to Q3 2025, and mortgage rates averaged ~5.2% in late 2025, increasing sensitivity to cost for builders.

In downturns developers cut specs and demand price concessions, forcing Alumasc to justify premium drainage and roofing with lifecycle cost data and shorter lead-time offers.

- Housing starts -18% YoY (Q3 2025)

- UK mortgage avg ~5.2% (late 2025)

- Buyers gain leverage when starts fall

Buyers dominate: Tier‑1s grab 60%, longer terms, rising S&D costs amid market squeeze

| Metric | Value |

|---|---|

| Tier‑1 share | ~60% |

| Payment terms | 60–120 days |

| S&D 2024 | £8.9m (+6.8%) |

| EPD requirement | 68% (2024) |

| B2B e‑com 2024 | $25.6T |

| Housing starts Q3 2025 | -18% YoY |

| Mortgage rate late 2025 | ~5.2% |

Full Version Awaits

Alumasc Group Porter's Five Forces Analysis

This preview shows the exact Alumasc Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it covers supplier power, buyer power, rivalry, threat of entry, and threat of substitutes with data-driven insights.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Alumasc Group faces moderate buyer power, niche supplier relationships, and steady threat from substitutes driven by sustainable building trends, while regulatory and scale barriers temper new entrants and competitive rivalry remains focused on product differentiation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Alumasc Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in raw material commodity pricing

Alumasc relies on aluminum, steel and specialized polymers; by late 2025 demand for low-carbon aluminum raised supplier leverage as certified metal prices climbed ~12–18% vs 2023, per London Metal Exchange and industry reports, forcing higher input costs or sourcing delays.

Energy costs for primary manufacturing

Energy costs heavily affect Alumasc Group's primary manufacturing; precision engineering and metal fabrication can consume 200–400 kWh per tonne, pushing energy to ~6–12% of COGS based on 2024 industry averages.

Suppliers of electricity and carbon‑intensive inputs pass through UK grid price swings and the UK ETS carbon costs, which rose to ~£45/t CO2 in 2024, directly inflating Alumasc's input costs.

That pass‑through and volatile wholesale prices (UK day‑ahead averages spiking 60% in 2022–24) restrict Alumasc's ability to secure long fixed‑rate contracts without price risk.

Specialized technical components

Alumasc relies on high-performance seals and electronic monitors for its water-management and roofing systems, and only a handful of UK/EU suppliers meet the technical and BSI/CE regulatory standards; supplier concentration raises bargaining power. In 2024, industry reports show top 5 niche component makers control ~60% of the market for certified roofing electronics, pressuring margins—Alumasc faces supply-risk and potential 3–5% input-cost shocks.

Logistics and transportation constraints

The movement of bulky building products depends on a strained logistics network that saw UK HGV driver shortages of ~20% and diesel price swings of ±18% in 2025, raising transport costs for Alumasc.

Third-party logistics firms prioritized large-volume clients, forcing mid-sized suppliers like Alumasc to pay delivery-premiums reported at 5–12% for guaranteed slots.

Efficient distribution remains critical for Alumasc to protect its reliability in construction projects and avoid order delays that can hit revenue and margins.

- UK HGV driver shortfall ~20% (2025)

- Diesel price volatility ±18% (2025)

- Delivery-premiums paid 5–12%

- High-volume clients prioritized by 3PLs

Supplier integration and market position

Upstream suppliers are moving into forward integration, selling prefabricated components directly to developers, cutting into Alumasc Group’s sub-assembly margins and lowering its procurement leverage.

Alumasc must reinforce supplier ties and secure long-term contracts; in 2024 UK construction prefabrication grew ~9% and supplier-assisted projects rose, raising competitive risk.

High supplier power: concentrated low‑carbon supply, rising energy/ETS & logistics costs

Supplier power is high: certified low‑carbon aluminium/precision components are concentrated (top‑5 ~60%), energy and UK ETS costs (£45/t CO2 in 2024) push COGS 6–12%, logistics shocks (HGV shortfall ~20% in 2025, diesel ±18%) add 5–12% delivery premiums, and upstream forward integration (prefab +9% in 2024) reduces procurement leverage.

| Metric | Value |

|---|---|

| Top‑5 component share | ~60% |

| UK ETS price (2024) | £45/t CO2 |

| Energy share of COGS | 6–12% |

| HGV shortfall (2025) | ~20% |

| Diesel volatility (2025) | ±18% |

| Delivery premiums | 5–12% |

| Prefab growth (UK 2024) | +9% |

What is included in the product

Tailored Porter's Five Forces for Alumasc Group: analyzes competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifies disruptive forces and market entry barriers shaping its pricing power and profitability.

A concise, one-sheet Porter's Five Forces view of Alumasc Group—quickly pinpoint competitive pressures and relief strategies for boardrooms and investor decks.

Customers Bargaining Power

Consolidation of major Tier 1 contractors

Influence of architects and specifiers

Demand for ESG and carbon transparency

By 2025 buyers demand detailed Environmental Product Declarations (EPDs) and proof of low embodied carbon; 68% of UK construction clients stated EPDs as mandatory in 2024 procurement, forcing suppliers to comply.

Customers can reject non-compliant vendors, and large contractors wield outsized power—Top 10 UK housebuilders represent ~40% of sector spend—making ESG a de facto entry requirement.

For Alumasc, this shifts R&D and product specs toward low-carbon formulations and verified EPDs, risking lost contracts if it lags; a 5–10% revenue hit is plausible for delayed compliance.

Availability of alternative sourcing channels

The rise of digital procurement platforms lets buyers compare Alumasc’s water-management and roofing products with international suppliers in real time, increasing price pressure and eroding brand-based information asymmetry.

In 2024, global B2B e‑commerce surpassed $25.6 trillion (UNCTAD), and UK construction firms reported 34% higher use of online sourcing vs. 2019, enabling sourcing from lower‑cost markets and compressing Alumasc’s margins.

- Real‑time comparisons raise price competition

- Online sourcing cuts information asymmetry

- Global suppliers offer lower overheads

- 2024 B2B e‑commerce: $25.6T (UNCTAD)

Cyclical nature of the residential housing market

The bargaining power of residential developers shifts with the UK housing cycle; housing starts fell 18% YoY to Q3 2025, and mortgage rates averaged ~5.2% in late 2025, increasing sensitivity to cost for builders.

In downturns developers cut specs and demand price concessions, forcing Alumasc to justify premium drainage and roofing with lifecycle cost data and shorter lead-time offers.

- Housing starts -18% YoY (Q3 2025)

- UK mortgage avg ~5.2% (late 2025)

- Buyers gain leverage when starts fall

Buyers dominate: Tier‑1s grab 60%, longer terms, rising S&D costs amid market squeeze

| Metric | Value |

|---|---|

| Tier‑1 share | ~60% |

| Payment terms | 60–120 days |

| S&D 2024 | £8.9m (+6.8%) |

| EPD requirement | 68% (2024) |

| B2B e‑com 2024 | $25.6T |

| Housing starts Q3 2025 | -18% YoY |

| Mortgage rate late 2025 | ~5.2% |

Full Version Awaits

Alumasc Group Porter's Five Forces Analysis

This preview shows the exact Alumasc Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it covers supplier power, buyer power, rivalry, threat of entry, and threat of substitutes with data-driven insights.