Amas Group NV Porter's Five Forces Analysis

From Overview to Strategy Blueprint

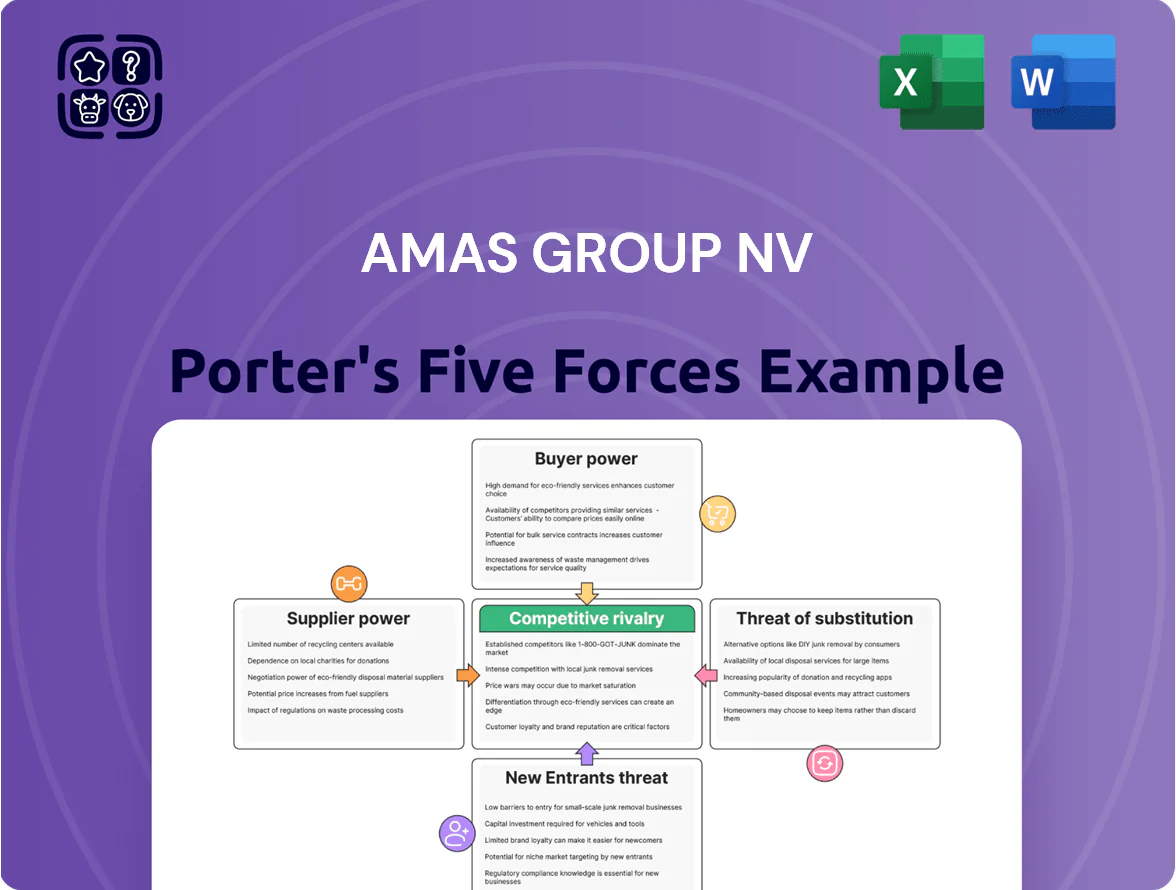

Amas Group NV faces moderate buyer power and rising substitute threats as digital channels lower switching costs, while supplier influence is manageable but concentration in key inputs poses risks; competitive rivalry is intense among regional players and regulatory shifts heighten barriers for new entrants. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Amas Group NV’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Major RPA Software Vendors

Amas Group depends on licenses from dominant RPA vendors UiPath, Blue Prism, and Microsoft; by end-2025 these three held roughly 65–70% global market share in RPA software, giving them pricing leverage over service partners. As vendors tighten licensing and shift to consumption or enterprise bundles, Amas faces margin pressure—each 5% license-price rise could cut gross margin by ~2 percentage points on RPA services. Contract renegotiations also risk delivery delays and higher implementation costs.

Scarcity of Specialized Technical Talent

The global shortage of senior AI, RPA (robotic process automation) and data-engineering talent pushed average tech hiring premiums 18% higher in 2024, so suppliers of these skills hold strong leverage over firms like Amas Group NV.

Talent functions as the primary supplier in services; with 67% of firms reporting critical skill gaps in 2024, bargaining power forces Amas to raise pay and benefits to secure staff.

To retain human capital for complex projects, Amas likely must budget 12–25% higher total compensation per specialist versus 2022 levels, or risk project delays and margin pressure.

Dominance of Cloud Infrastructure Providers

Cloud services from AWS, Google Cloud and Microsoft Azure are critical for Amas Group NV’s automation stack, handling compute, storage and AI workloads; in 2024 AWS, GCP and Azure held about 64% of global cloud market share (Synergy Research Group). Switching clouds is technically hard and migration can cost millions plus months of downtime, so suppliers keep high leverage.

Third-Party API and Data Integration Costs

Third-party data feeds and niche APIs often charge $10k–$200k+ annually per feed; in 2024 enterprise API fees rose ~12% YoY, boosting supplier leverage.

Suppliers can hike access fees or tighten usage terms with little notice, forcing Amas Group NV to absorb costs or pass them to clients, risking margins and churn.

Amas must lock multi-year contracts, standardize adapters, and budget a 5–15% contingency for API cost volatility.

- 2024 API fee growth ~12% YoY

- Typical feed cost $10k–$200k+/yr

- Budget 5–15% contingency

Hardware and Equipment Procurement

- Hardware capex ~3–5% of IT budget

- Chip price volatility 12% YoY (2024, IDC)

- Shortage-driven capex spike up to 18%

- Multiple major vendors → low supplier power

Supplier power high: lock multi-year deals, budget API contingency & raise specialist pay

Suppliers (RPA vendors, cloud providers, talent, data feeds, hardware) hold moderate–high power: UiPath/Blue Prism/Microsoft ~65–70% RPA share (end-2025), AWS/GCP/Azure ~64% cloud share (2024), tech hiring premiums +18% (2024), API fees +12% YoY (2024); Amas needs multi-year contracts, 5–15% API contingency, and 12–25% higher comp per specialist to protect margins.

| Supplier | Key stat | Impact |

|---|---|---|

| RPA vendors | 65–70% market (end-2025) | Pricing leverage |

| Cloud | 64% market (2024) | High switching cost |

| Talent | +18% hiring prem (2024) | Higher comp 12–25% |

| APIs/data | +12% fees (2024) | Budget 5–15% contingency |

What is included in the product

Tailored Porter's Five Forces overview for Amas Group NV highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying key disruptive forces and entry barriers shaping its profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for Amas Group NV—instant clarity on competitive pressures to speed strategic choices and investor pitches.

Customers Bargaining Power

Availability of Alternative Service Providers

The market for business process optimization is crowded: over 15,000 consulting firms globally and ~4,200 boutique agencies focused on RPA and automation in 2024, so buyers can pit providers against each other to cut fees by 10–25% on average.

That choice power forces clients to demand stronger SLAs and faster ROI; Amas Group must prove differentiated outcomes—like reducing process costs >30% or cutting cycle time by 40%—to avoid churn.

Low Switching Costs for Clients

Low switching costs mean clients can move maintenance or new RPA work after a project ends; industry surveys show 62% of firms consider changing RPA vendors within 24 months, so Amas Group NV faces real churn risk.

Client Internalization of Automation Skills

Larger enterprise clients are building internal automation and analytics centers of excellence; McKinsey reported 58% of Fortune 500 firms had in‑house AI/automation teams by 2024, reducing spend with vendors like Amas Group and increasing buyer leverage in price and scope negotiations. As reliance on external providers falls, Amas must shift to complex, high‑value services—advanced ML, systems integration, change management—where clients lack deep expertise.

Focus on Measurable ROI and Performance

By end-2025 buyers demand measurable ROI; surveys show 68% of enterprise buyers require KPI-linked contracts and 54% delay purchases until pilot ROI exceeds vendor claims.

This outcome focus lets buyers force fee-for-performance terms tied to metrics like 15–25% efficiency gains or revenue uplift, shifting pricing power toward clients.

Amas Group must shift to value-aligned pricing—tying fees to client-realized savings or KPIs—to protect win rates and contract sizes.

- 68% require KPI contracts

- 54% delay until pilot ROI verified

- Target metrics: 15–25% efficiency gain

- Adopt fee-for-performance pricing

Concentration of Large Enterprise Clients

If 40–60% of Amas Group NV’s 2024 revenue comes from five or fewer corporate clients, those buyers wield strong bargaining power and can push for price discounts and bespoke service-level agreements.

Major accounts can demand dedicated support and customization, lowering margins: a 5–10% price concession on a €200m client book cuts gross profit by €10–20m annually.

Failing to meet these clients’ specs risks churn and concentrated revenue loss—losing one top client could shave 8–15% off total revenue.

- 40–60% revenue concentration

- 5–10% discount impact = €10–20m margin loss

- Single-client loss = 8–15% revenue hit

Client power crushes margins: KPI contracts, vendor churn risk, €10–20m hit on €200m

Buyers hold strong power: >15,000 consultancies and ~4,200 RPA boutiques in 2024 push fees down 10–25% and demand KPI‑linked SLAs; 62% consider switching RPA vendors within 24 months; 68% require KPI contracts and 54% delay until pilot ROI verified. If 40–60% of 2024 revenue stems from ≤5 clients, a single loss could cut 8–15% of revenue, and 5–10% discounts on a €200m book shave €10–20m gross profit.

| Metric | Value |

|---|---|

| Consultancies (2024) | >15,000 |

| RPA boutiques (2024) | ~4,200 |

| Switching intent | 62% (24 months) |

| KPI contracts | 68% |

| Pilot ROI delay | 54% |

| Revenue concentration | 40–60% |

| Single-client revenue hit | 8–15% |

| Discount impact on €200m | €10–20m |

Same Document Delivered

Amas Group NV Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Amas Group NV you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted analysis file you'll be able to download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Amas Group NV faces moderate buyer power and rising substitute threats as digital channels lower switching costs, while supplier influence is manageable but concentration in key inputs poses risks; competitive rivalry is intense among regional players and regulatory shifts heighten barriers for new entrants. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Amas Group NV’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Major RPA Software Vendors

Amas Group depends on licenses from dominant RPA vendors UiPath, Blue Prism, and Microsoft; by end-2025 these three held roughly 65–70% global market share in RPA software, giving them pricing leverage over service partners. As vendors tighten licensing and shift to consumption or enterprise bundles, Amas faces margin pressure—each 5% license-price rise could cut gross margin by ~2 percentage points on RPA services. Contract renegotiations also risk delivery delays and higher implementation costs.

Scarcity of Specialized Technical Talent

The global shortage of senior AI, RPA (robotic process automation) and data-engineering talent pushed average tech hiring premiums 18% higher in 2024, so suppliers of these skills hold strong leverage over firms like Amas Group NV.

Talent functions as the primary supplier in services; with 67% of firms reporting critical skill gaps in 2024, bargaining power forces Amas to raise pay and benefits to secure staff.

To retain human capital for complex projects, Amas likely must budget 12–25% higher total compensation per specialist versus 2022 levels, or risk project delays and margin pressure.

Dominance of Cloud Infrastructure Providers

Cloud services from AWS, Google Cloud and Microsoft Azure are critical for Amas Group NV’s automation stack, handling compute, storage and AI workloads; in 2024 AWS, GCP and Azure held about 64% of global cloud market share (Synergy Research Group). Switching clouds is technically hard and migration can cost millions plus months of downtime, so suppliers keep high leverage.

Third-Party API and Data Integration Costs

Third-party data feeds and niche APIs often charge $10k–$200k+ annually per feed; in 2024 enterprise API fees rose ~12% YoY, boosting supplier leverage.

Suppliers can hike access fees or tighten usage terms with little notice, forcing Amas Group NV to absorb costs or pass them to clients, risking margins and churn.

Amas must lock multi-year contracts, standardize adapters, and budget a 5–15% contingency for API cost volatility.

- 2024 API fee growth ~12% YoY

- Typical feed cost $10k–$200k+/yr

- Budget 5–15% contingency

Hardware and Equipment Procurement

- Hardware capex ~3–5% of IT budget

- Chip price volatility 12% YoY (2024, IDC)

- Shortage-driven capex spike up to 18%

- Multiple major vendors → low supplier power

Supplier power high: lock multi-year deals, budget API contingency & raise specialist pay

Suppliers (RPA vendors, cloud providers, talent, data feeds, hardware) hold moderate–high power: UiPath/Blue Prism/Microsoft ~65–70% RPA share (end-2025), AWS/GCP/Azure ~64% cloud share (2024), tech hiring premiums +18% (2024), API fees +12% YoY (2024); Amas needs multi-year contracts, 5–15% API contingency, and 12–25% higher comp per specialist to protect margins.

| Supplier | Key stat | Impact |

|---|---|---|

| RPA vendors | 65–70% market (end-2025) | Pricing leverage |

| Cloud | 64% market (2024) | High switching cost |

| Talent | +18% hiring prem (2024) | Higher comp 12–25% |

| APIs/data | +12% fees (2024) | Budget 5–15% contingency |

What is included in the product

Tailored Porter's Five Forces overview for Amas Group NV highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying key disruptive forces and entry barriers shaping its profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for Amas Group NV—instant clarity on competitive pressures to speed strategic choices and investor pitches.

Customers Bargaining Power

Availability of Alternative Service Providers

The market for business process optimization is crowded: over 15,000 consulting firms globally and ~4,200 boutique agencies focused on RPA and automation in 2024, so buyers can pit providers against each other to cut fees by 10–25% on average.

That choice power forces clients to demand stronger SLAs and faster ROI; Amas Group must prove differentiated outcomes—like reducing process costs >30% or cutting cycle time by 40%—to avoid churn.

Low Switching Costs for Clients

Low switching costs mean clients can move maintenance or new RPA work after a project ends; industry surveys show 62% of firms consider changing RPA vendors within 24 months, so Amas Group NV faces real churn risk.

Client Internalization of Automation Skills

Larger enterprise clients are building internal automation and analytics centers of excellence; McKinsey reported 58% of Fortune 500 firms had in‑house AI/automation teams by 2024, reducing spend with vendors like Amas Group and increasing buyer leverage in price and scope negotiations. As reliance on external providers falls, Amas must shift to complex, high‑value services—advanced ML, systems integration, change management—where clients lack deep expertise.

Focus on Measurable ROI and Performance

By end-2025 buyers demand measurable ROI; surveys show 68% of enterprise buyers require KPI-linked contracts and 54% delay purchases until pilot ROI exceeds vendor claims.

This outcome focus lets buyers force fee-for-performance terms tied to metrics like 15–25% efficiency gains or revenue uplift, shifting pricing power toward clients.

Amas Group must shift to value-aligned pricing—tying fees to client-realized savings or KPIs—to protect win rates and contract sizes.

- 68% require KPI contracts

- 54% delay until pilot ROI verified

- Target metrics: 15–25% efficiency gain

- Adopt fee-for-performance pricing

Concentration of Large Enterprise Clients

If 40–60% of Amas Group NV’s 2024 revenue comes from five or fewer corporate clients, those buyers wield strong bargaining power and can push for price discounts and bespoke service-level agreements.

Major accounts can demand dedicated support and customization, lowering margins: a 5–10% price concession on a €200m client book cuts gross profit by €10–20m annually.

Failing to meet these clients’ specs risks churn and concentrated revenue loss—losing one top client could shave 8–15% off total revenue.

- 40–60% revenue concentration

- 5–10% discount impact = €10–20m margin loss

- Single-client loss = 8–15% revenue hit

Client power crushes margins: KPI contracts, vendor churn risk, €10–20m hit on €200m

Buyers hold strong power: >15,000 consultancies and ~4,200 RPA boutiques in 2024 push fees down 10–25% and demand KPI‑linked SLAs; 62% consider switching RPA vendors within 24 months; 68% require KPI contracts and 54% delay until pilot ROI verified. If 40–60% of 2024 revenue stems from ≤5 clients, a single loss could cut 8–15% of revenue, and 5–10% discounts on a €200m book shave €10–20m gross profit.

| Metric | Value |

|---|---|

| Consultancies (2024) | >15,000 |

| RPA boutiques (2024) | ~4,200 |

| Switching intent | 62% (24 months) |

| KPI contracts | 68% |

| Pilot ROI delay | 54% |

| Revenue concentration | 40–60% |

| Single-client revenue hit | 8–15% |

| Discount impact on €200m | €10–20m |

Same Document Delivered

Amas Group NV Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Amas Group NV you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted analysis file you'll be able to download and use the moment you buy.