amaysim PESTLE Analysis

Your Competitive Advantage Starts with This Report

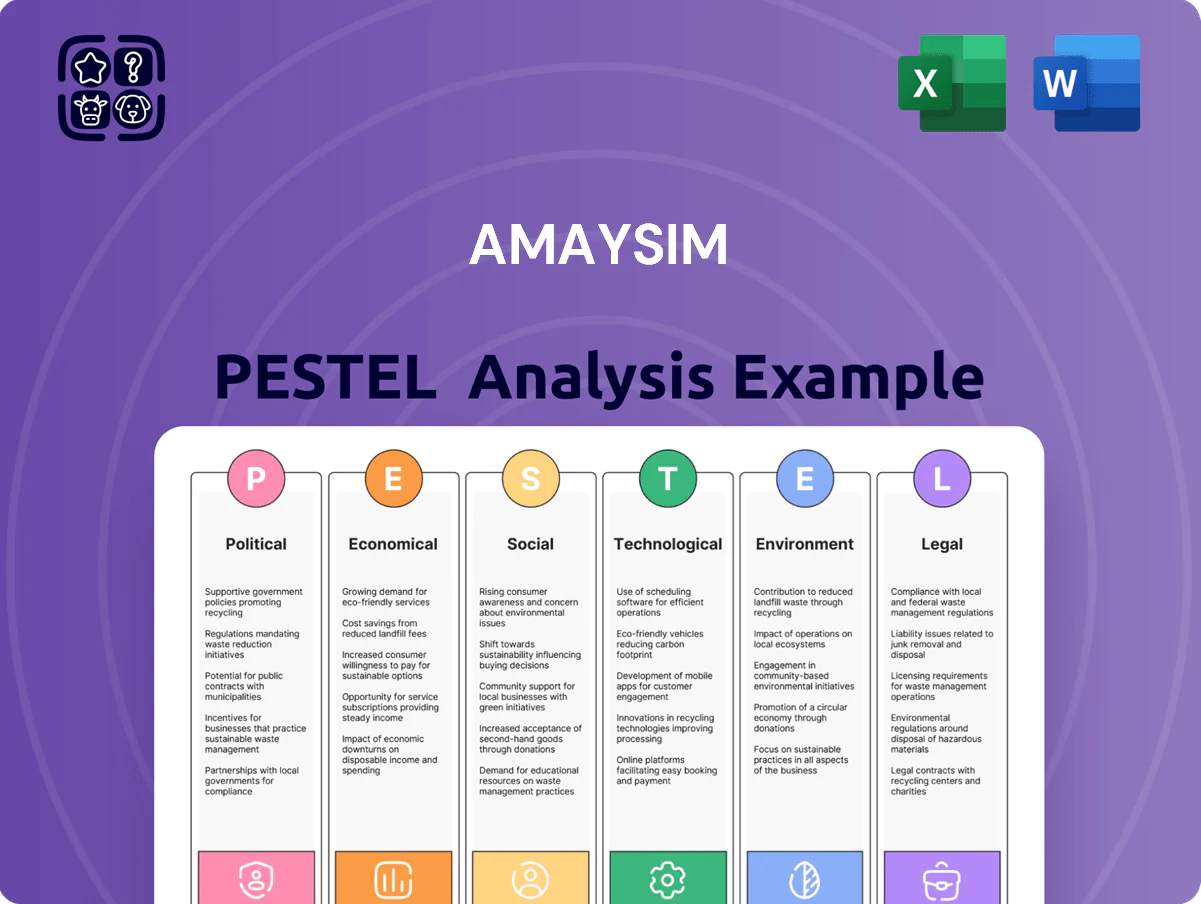

Gain a competitive advantage with our concise PESTLE Analysis of amaysim—exploring political, economic, social, technological, legal, and environmental forces shaping its strategy and risks; ideal for investors and strategists. Purchase the full report for a detailed, actionable breakdown you can use in forecasts, pitches, and strategic planning—download instantly to make smarter, faster decisions.

Political factors

Government Infrastructure Policy

The Australian government’s A$1.5 billion Regional Connectivity Program and A$1.1 billion 5G acceleration measures expand coverage, allowing amaysim to extend MVNO services into regional areas and serve an estimated 3.8 million regional users more reliably.

Federal subsidies for rural towers and spectrum allocation reforms reduce wholesale costs and boost amaysim’s addressable market, supporting growth after its 2024 mobile revenue of A$210 million.

Policy shifts in the National Broadband Network or incentives for private network investment can alter wholesale pricing and access terms, materially affecting amaysim’s margins and capital planning.

National Security and Cybersecurity Regulations

Strict government mandates on telecom security force amaysim to uphold high data-protection standards; Australia’s Security of Critical Infrastructure Act amendments (2021–2023) expanded obligations for providers, with penalties up to AUD 10 million for non-compliance.

Regulators’ focus on mitigating foreign interference and cyber threats means amaysim must allocate ongoing CAPEX and OPEX to cybersecurity; Australian telcos reported average security spend rises of ~18% in 2023.

These political priorities require continuous investment in secure systems to protect consumer data and preserve licences, impacting margins as compliance costs scale with userbase and network dependencies.

Digital Inclusion and Affordability Initiatives

Political pressure to ensure affordable mobile and internet access supports low-cost providers like amaysim, with Australia’s 2024 Digital Economy Strategy targeting universal connectivity and continued support for competitive retail markets. amaysim benefits from programs that encourage smaller players—Australia’s MVNO sector held about 9% of mobile subscribers in 2023—helping drive down prices for essential digital services. However, changes to social welfare or A$ subsidies could reduce spending power among amaysim’s budget-conscious customer base, where ARPU was A$26–30 in 2024.

Foreign Ownership and Investment Oversight

As amaysim resells services on the Optus network owned by Singtel, Australian government scrutiny of foreign ownership can affect its operating environment; Singtel reported FY2024 group revenue SGD 13.1bn, highlighting scale behind Optus.

Diplomatic and trade relations—particularly Australia–Singapore ties—shape Optus strategic choices; any FIRB tightening could trigger divestment pressures in a sector valued at AUD ~45bn in 2024.

Telecommunications Regulatory Reform

Ongoing debates to reform the Telecommunications Act could impose new compliance costs on MVNOs like amaysim, with regulatory change cycles accelerated by consumer-rights politics; Australian ACCC inquiries in 2024 noted 18% of complaints related to billing and switching issues, increasing scrutiny.

Politicians advocate for mandatory pricing transparency and simplified porting—measures that could reduce churn-related revenue but improve market entry; easier switching could raise annual churn by an estimated 2–4% for smaller carriers.

amaysim must stay agile operationally and financially, allocating regulatory change buffers—industry estimates in 2025 suggest compliance upgrade costs for MVNOs can range AUD 0.5–2.0m depending on systems integration needs.

- Potential new compliance costs: AUD 0.5–2.0m

- 2024 ACCC complaints: 18% billing/switching

- Estimated churn increase if switching eased: 2–4%

5G funding lifts amaysim growth but security, ACCC risks could dent ARPU and add costs

Political support for regional connectivity and 5G (A$2.6bn programs) expands amaysim’s addressable market; 2024 mobile revenue A$210m and ARPU A$26–30 benefit, while compliance under Security of Critical Infrastructure Act (penalties up to A$10m) and rising cybersecurity spend (~+18% in 2023) raise OPEX. FIRB/spectrum reforms and ACCC scrutiny (18% billing complaints in 2024) could change costs and churn (±2–4%).

| Metric | Value |

|---|---|

| Regional/5G funding | A$2.6bn |

| 2024 mobile revenue | A$210m |

| ARPU 2024 | A$26–30 |

| Security penalties | up to A$10m |

| Cyber spend rise 2023 | ~18% |

| ACCC billing complaints 2024 | 18% |

| Potential churn impact | 2–4% |

What is included in the product

Explores how external macro-environmental factors uniquely affect amaysim across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and opportunity identification for executives, investors, and advisors.

Concise PESTLE summary tailored for amaysim that highlights regulatory, economic, and technological risks and opportunities for quick inclusion in presentations or decision briefs.

Economic factors

Cost of Living and Inflationary Pressures

Rising Australian inflation, which averaged 4.1% in 2024 after peaking at 7.8% in 2022, is driving consumers toward lower-cost mobile options, boosting demand for amaysim’s prepaid, no-frills plans as households cut discretionary spending. Amaysim can capture market share from traditional postpaid contracts by promoting price-sensitive plans; its FY2025 guidance should reflect this tailwind. Conversely, inflation raises amaysim’s operating costs via higher wages and supplier prices, with industry labour cost inflation near 5% adding margin pressure.

Wholesale Pricing Agreements

The economic viability of amaysim hinges on wholesale rates negotiated with Optus; in FY2024 amaysim reported network cost pressures as wholesale access fees represented a material portion of COGS, contributing to a gross margin squeeze versus FY2023. Fluctuations in Optus’s economic health—e.g., Singtel/Optus capex guidance of ~AU$2.5bn in 2024—can prompt wholesale price resets that amaysim must absorb or pass to customers, impacting ARPU and churn. Shifts in carrier capex and 5G rollout timing directly constrain MVNO margins, with industry wholesale rate volatility of ±5–8% materially affecting EBITDA for low-margin providers.

Interest Rate Fluctuations

amaysim’s asset-light model reduces capital intensity versus network owners, but rising interest rates still raised its weighted average cost of capital in 2024, increasing borrowing costs for marketing and M&A and potentially reducing cash available for customer acquisition; Australia’s cash rate rose to 4.35% by Dec 2023 and remained elevated through 2024, dampening consumer discretionary spending and ARPU growth; rate stabilization into 2025 would improve planning certainty for new service investments.

Labor Market Dynamics

The Australian labor market remains tight with unemployment at 3.7% (Dec 2025) and advertised vacancies up 12% year‑on‑year; specialized roles in digital marketing, software development and cybersecurity face acute shortages.

Amaysim must pay higher wages and recruitment costs—average tech salaries rose ~6% in 2024—raising administrative and operational overheads.

Economic migration—net overseas migration ~370,000 in 2023–24—boosts demand for flexible, low‑cost SIMs among international students and temporary workers.

- Tight labor market: 3.7% unemployment

- Tech salary growth: ~6% in 2024

- Vacancies +12% YoY

- NOM ~370,000 (2023–24) drives SIM demand

Currency Exchange Volatility

Fluctuations in the AUD—which fell about 8% vs USD in 2024 H1 and averaged 0.65 USD in 2024—raise costs for imported devices and international roaming/termination contracts, increasing COGS for handset bundles and add-ons.

As a service-focused MVNO, amaysim’s margins on international-heavy plans are exposed; a 10% AUD depreciation can similarly raise termination costs and compress margins unless passed to consumers.

- 2024 AUD average ~0.65 USD; 8% drop in 2024 H1

- Imported handset cost and roaming fees tied to FX

- 10% AUD devaluation materially compresses international-plan margins

Inflation, AUD weakness and wholesale swings squeeze amaysim margins despite prepaid demand

Inflation (4.1% in 2024) and elevated cash rates (4.35% end‑2023) boost demand for amaysim’s low‑cost plans but raise wage and supplier costs; wholesale rate volatility (±5–8%) from Optus and AUD weakness (2024 avg ~0.65 USD; 8% H1 drop) compress margins; net migration (~370k 2023–24) supports prepaid SIM growth.

| Metric | Value |

|---|---|

| Inflation 2024 | 4.1% |

| Cash rate | 4.35% |

| AUD avg 2024 | 0.65 USD |

| NOM 2023–24 | ~370,000 |

Same Document Delivered

amaysim PESTLE Analysis

The preview shown here is the exact amaysim PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a competitive advantage with our concise PESTLE Analysis of amaysim—exploring political, economic, social, technological, legal, and environmental forces shaping its strategy and risks; ideal for investors and strategists. Purchase the full report for a detailed, actionable breakdown you can use in forecasts, pitches, and strategic planning—download instantly to make smarter, faster decisions.

Political factors

Government Infrastructure Policy

The Australian government’s A$1.5 billion Regional Connectivity Program and A$1.1 billion 5G acceleration measures expand coverage, allowing amaysim to extend MVNO services into regional areas and serve an estimated 3.8 million regional users more reliably.

Federal subsidies for rural towers and spectrum allocation reforms reduce wholesale costs and boost amaysim’s addressable market, supporting growth after its 2024 mobile revenue of A$210 million.

Policy shifts in the National Broadband Network or incentives for private network investment can alter wholesale pricing and access terms, materially affecting amaysim’s margins and capital planning.

National Security and Cybersecurity Regulations

Strict government mandates on telecom security force amaysim to uphold high data-protection standards; Australia’s Security of Critical Infrastructure Act amendments (2021–2023) expanded obligations for providers, with penalties up to AUD 10 million for non-compliance.

Regulators’ focus on mitigating foreign interference and cyber threats means amaysim must allocate ongoing CAPEX and OPEX to cybersecurity; Australian telcos reported average security spend rises of ~18% in 2023.

These political priorities require continuous investment in secure systems to protect consumer data and preserve licences, impacting margins as compliance costs scale with userbase and network dependencies.

Digital Inclusion and Affordability Initiatives

Political pressure to ensure affordable mobile and internet access supports low-cost providers like amaysim, with Australia’s 2024 Digital Economy Strategy targeting universal connectivity and continued support for competitive retail markets. amaysim benefits from programs that encourage smaller players—Australia’s MVNO sector held about 9% of mobile subscribers in 2023—helping drive down prices for essential digital services. However, changes to social welfare or A$ subsidies could reduce spending power among amaysim’s budget-conscious customer base, where ARPU was A$26–30 in 2024.

Foreign Ownership and Investment Oversight

As amaysim resells services on the Optus network owned by Singtel, Australian government scrutiny of foreign ownership can affect its operating environment; Singtel reported FY2024 group revenue SGD 13.1bn, highlighting scale behind Optus.

Diplomatic and trade relations—particularly Australia–Singapore ties—shape Optus strategic choices; any FIRB tightening could trigger divestment pressures in a sector valued at AUD ~45bn in 2024.

Telecommunications Regulatory Reform

Ongoing debates to reform the Telecommunications Act could impose new compliance costs on MVNOs like amaysim, with regulatory change cycles accelerated by consumer-rights politics; Australian ACCC inquiries in 2024 noted 18% of complaints related to billing and switching issues, increasing scrutiny.

Politicians advocate for mandatory pricing transparency and simplified porting—measures that could reduce churn-related revenue but improve market entry; easier switching could raise annual churn by an estimated 2–4% for smaller carriers.

amaysim must stay agile operationally and financially, allocating regulatory change buffers—industry estimates in 2025 suggest compliance upgrade costs for MVNOs can range AUD 0.5–2.0m depending on systems integration needs.

- Potential new compliance costs: AUD 0.5–2.0m

- 2024 ACCC complaints: 18% billing/switching

- Estimated churn increase if switching eased: 2–4%

5G funding lifts amaysim growth but security, ACCC risks could dent ARPU and add costs

Political support for regional connectivity and 5G (A$2.6bn programs) expands amaysim’s addressable market; 2024 mobile revenue A$210m and ARPU A$26–30 benefit, while compliance under Security of Critical Infrastructure Act (penalties up to A$10m) and rising cybersecurity spend (~+18% in 2023) raise OPEX. FIRB/spectrum reforms and ACCC scrutiny (18% billing complaints in 2024) could change costs and churn (±2–4%).

| Metric | Value |

|---|---|

| Regional/5G funding | A$2.6bn |

| 2024 mobile revenue | A$210m |

| ARPU 2024 | A$26–30 |

| Security penalties | up to A$10m |

| Cyber spend rise 2023 | ~18% |

| ACCC billing complaints 2024 | 18% |

| Potential churn impact | 2–4% |

What is included in the product

Explores how external macro-environmental factors uniquely affect amaysim across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and opportunity identification for executives, investors, and advisors.

Concise PESTLE summary tailored for amaysim that highlights regulatory, economic, and technological risks and opportunities for quick inclusion in presentations or decision briefs.

Economic factors

Cost of Living and Inflationary Pressures

Rising Australian inflation, which averaged 4.1% in 2024 after peaking at 7.8% in 2022, is driving consumers toward lower-cost mobile options, boosting demand for amaysim’s prepaid, no-frills plans as households cut discretionary spending. Amaysim can capture market share from traditional postpaid contracts by promoting price-sensitive plans; its FY2025 guidance should reflect this tailwind. Conversely, inflation raises amaysim’s operating costs via higher wages and supplier prices, with industry labour cost inflation near 5% adding margin pressure.

Wholesale Pricing Agreements

The economic viability of amaysim hinges on wholesale rates negotiated with Optus; in FY2024 amaysim reported network cost pressures as wholesale access fees represented a material portion of COGS, contributing to a gross margin squeeze versus FY2023. Fluctuations in Optus’s economic health—e.g., Singtel/Optus capex guidance of ~AU$2.5bn in 2024—can prompt wholesale price resets that amaysim must absorb or pass to customers, impacting ARPU and churn. Shifts in carrier capex and 5G rollout timing directly constrain MVNO margins, with industry wholesale rate volatility of ±5–8% materially affecting EBITDA for low-margin providers.

Interest Rate Fluctuations

amaysim’s asset-light model reduces capital intensity versus network owners, but rising interest rates still raised its weighted average cost of capital in 2024, increasing borrowing costs for marketing and M&A and potentially reducing cash available for customer acquisition; Australia’s cash rate rose to 4.35% by Dec 2023 and remained elevated through 2024, dampening consumer discretionary spending and ARPU growth; rate stabilization into 2025 would improve planning certainty for new service investments.

Labor Market Dynamics

The Australian labor market remains tight with unemployment at 3.7% (Dec 2025) and advertised vacancies up 12% year‑on‑year; specialized roles in digital marketing, software development and cybersecurity face acute shortages.

Amaysim must pay higher wages and recruitment costs—average tech salaries rose ~6% in 2024—raising administrative and operational overheads.

Economic migration—net overseas migration ~370,000 in 2023–24—boosts demand for flexible, low‑cost SIMs among international students and temporary workers.

- Tight labor market: 3.7% unemployment

- Tech salary growth: ~6% in 2024

- Vacancies +12% YoY

- NOM ~370,000 (2023–24) drives SIM demand

Currency Exchange Volatility

Fluctuations in the AUD—which fell about 8% vs USD in 2024 H1 and averaged 0.65 USD in 2024—raise costs for imported devices and international roaming/termination contracts, increasing COGS for handset bundles and add-ons.

As a service-focused MVNO, amaysim’s margins on international-heavy plans are exposed; a 10% AUD depreciation can similarly raise termination costs and compress margins unless passed to consumers.

- 2024 AUD average ~0.65 USD; 8% drop in 2024 H1

- Imported handset cost and roaming fees tied to FX

- 10% AUD devaluation materially compresses international-plan margins

Inflation, AUD weakness and wholesale swings squeeze amaysim margins despite prepaid demand

Inflation (4.1% in 2024) and elevated cash rates (4.35% end‑2023) boost demand for amaysim’s low‑cost plans but raise wage and supplier costs; wholesale rate volatility (±5–8%) from Optus and AUD weakness (2024 avg ~0.65 USD; 8% H1 drop) compress margins; net migration (~370k 2023–24) supports prepaid SIM growth.

| Metric | Value |

|---|---|

| Inflation 2024 | 4.1% |

| Cash rate | 4.35% |

| AUD avg 2024 | 0.65 USD |

| NOM 2023–24 | ~370,000 |

Same Document Delivered

amaysim PESTLE Analysis

The preview shown here is the exact amaysim PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.