AmBank Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

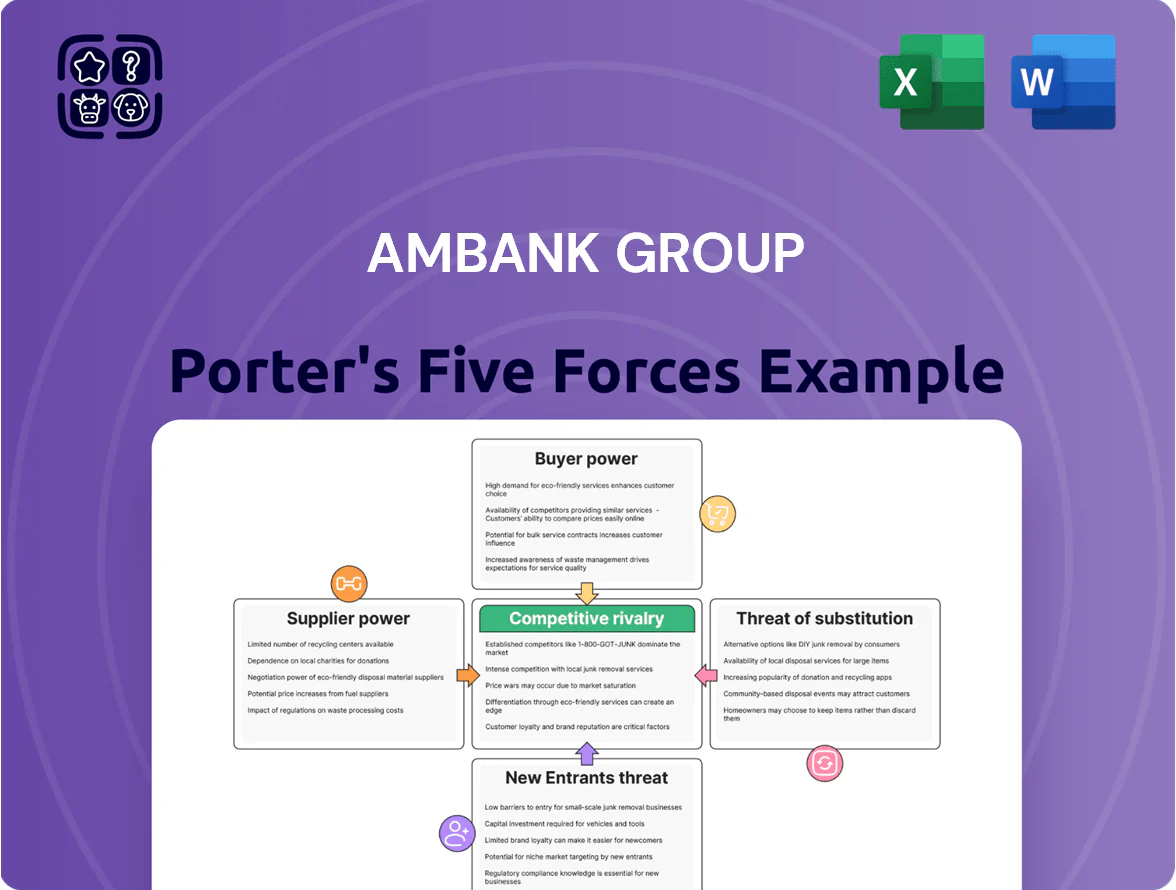

AmBank Group faces moderate buyer power, intense rivalry from regional banks, and regulatory pressures that shape pricing and product innovation, while digital entrants and fintechs raise the threat of substitutes and heighten the need for strategic differentiation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore AmBank Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Depositors as capital suppliers

Retail and corporate depositors supply AmBank Group’s core funding; Malaysia’s banking system held RM2.2 trillion in deposits in 2024, with digital banks gaining share, so low-cost stable deposits are scarce in 2025.

AmBank must match market rates—average CASA (current account savings account) ratios in Malaysia were ~33% in 2024—and improve service and digital UX to avoid outflows to larger incumbents or neo-banks.

Technology and infrastructure vendors

AmBank relies heavily on third-party cloud, cybersecurity and core-banking vendors; global providers like AWS, Microsoft and Temenos command pricing power since switching costs and technical risks can exceed RM100–300m and take 12–24 months.

In 2024 Malaysia banking cloud spend rose ~18% to an estimated RM1.2bn, so vendor contract stability directly affects AmBank’s cost base and time-to-market for digital services.

AmBank’s digital transformation roadmap assumes multi-year, cost-effective SLAs; loss of favorable terms or major vendor outages would materially raise operating expense and execution risk.

Specialized human capital

High demand for data science, AI and compliance talent in Malaysia — vacancies in fintech rose 42% in 2024 — forces AmBank to compete with local banks and Big Tech, raising average specialist pay 18–25% above baseline roles.

Central bank and regulatory influence

Bank Negara Malaysia (BNM) serves as the key supplier of regulation and liquidity; its Overnight Policy Rate (OPR) hikes to 3.00% as of Dec 2025 raise AmBank Group’s cost of funds and compress net interest margin.

AmBank cannot influence these macro supply conditions and must reshuffle pricing, funding mix, and capital buffers to meet BNM mandates and liquidity coverage ratio requirements.

- BNM OPR 3.00% (Dec 2025)

- Higher funding cost → lower NIM

- Must meet LCR and CAR rules

Wholesale funding and credit rating agencies

Access to wholesale capital markets is critical for AmBank Group to fund large corporate loans and manage liquidity; as of FY2024 AmBank raised RM3.2bn in wholesale debt, showing dependency on institutional suppliers.

Credit rating agencies shape cost of that supply—Moody’s and S&P ratings drive interest spreads; a one-notch downgrade typically raises borrowing spreads by ~50–150 bps, materially increasing funding costs.

Maintaining a strong credit profile is vital: a downgrade would raise AmBank’s cost of borrowing and reduce access to term wholesale lines, squeezing margins and capital planning.

- Wholesale debt raised FY2024: RM3.2bn

- Downgrade impact: +50–150 bps spread

- Risk: higher funding cost, reduced term access

Supplier power squeezes AmBank: rising costs, tighter funding and margin pressure

Suppliers (depositors, vendors, talent, BNM, wholesale markets) exert strong bargaining power on AmBank: tight low‑cost deposit supply (Malaysia deposits RM2.2T in 2024; CASA ~33%), rising cloud spend (RM1.2B, +18% in 2024), specialist pay +18–25%, and BNM OPR 3.00% (Dec 2025) which raises funding cost and compresses NIM; FY2024 wholesale debt RM3.2B—downgrades add ~50–150bps to spreads.

| Metric | Value |

|---|---|

| Malaysia deposits (2024) | RM2.2T |

| CASA (avg 2024) | ~33% |

| Cloud spend (2024) | RM1.2B (+18%) |

| Specialist pay rise (2024) | +18–25% |

| BNM OPR | 3.00% (Dec 2025) |

| AmBank wholesale debt FY2024 | RM3.2B |

| Downgrade spread impact | +50–150bps |

What is included in the product

Provides a concise Porter’s Five Forces assessment tailored to AmBank Group, revealing competitive intensity, buyer and supplier leverage, entry barriers, and substitution risks that shape its profitability and strategic positioning.

A concise Porter's Five Forces snapshot for AmBank Group—pinpoint competitive pressures and regulatory risks at a glance to speed strategic decisions.

Customers Bargaining Power

Low switching costs for retail users

The rise of digital banking and standardized retail products means Malaysian customers can switch banks quickly; AmBank faced net retail deposit outflows in Q3 2024, and industry data shows 38% of customers considered switching in 2024. Mobile apps and instant e-KYC let users move funds over hours for small rate or UX gains, giving individual customers high bargaining power over AmBank.

Price sensitivity in loan products

Malaysian consumers and SMEs react strongly to interest spreads: a 25bp change can shift applications by ~3–5%, and mortgage spreads averaged 1.6% in 2024, per BNM data, so AmBank must match market pricing to keep volumes.

Online comparison portals and fintechs now list real-time rates; search-driven switching rose ~18% in 2023, forcing AmBank to cut margins or add fee waivers, cashback, and bundled advisory to retain clients.

Demands for digital-first experiences

By end-2025 customers treat seamless, hyper-personalized banking as table stakes: 74% of APAC consumers expect real-time personalization, and 62% will switch banks for better digital experiences (2024 Accenture, PwC data). If AmBank misses these tech expectations, churn risk rises quickly as agile digital-first challengers grab market share, giving buyers strong leverage to demand continuous innovation and polished interfaces.

Bargaining strength of corporate clients

Large corporate and government-linked clients wield strong bargaining power at AmBank Group, often representing single-account deposits or lending limits exceeding RM500m and annual transaction volumes >RM1bn, enabling demands for bespoke interest rates, lower fees, and tailored credit facilities.

AmBank must deliver custom cash-management, syndicated loan pricing and relationship banking to retain these high-net-worth accounts or risk loss to larger Malaysian banks like Maybank and CIMB or international banks.

- Single-account deposits often >RM500m

- Annual transaction volumes >RM1bn

- Negotiate lower fees, bespoke rates, credit terms

- Retention requires tailored solutions, relationship depth

Transparency and information access

Greater fee transparency and independent review sites have eroded banks’ information edge; 72% of Malaysian retail customers used online comparison tools in 2024, per a Bank Negara Malaysia survey, cutting time-to-switch and fee surprises.

Customers now see hidden fees, service scores, and product returns before contacting AmBank, raising collective bargaining power and forcing price and service parity across retail banking.

- 72% used comparison tools (BNM, 2024)

- Lowered switching friction — digital onboarding up 18% (AmBank FY2024)

- Public fee matrices increase negotiation leverage

High customer leverage: digital switching and bespoke demands force AmBank rate matches

Customers—both retail and large corporates—hold high bargaining power over AmBank due to easy digital switching, price-sensitive demand (25bp → ~3–5% volume shift), and transparency (72% used comparison tools in 2024); large clients often command bespoke terms (>RM500m deposits, >RM1bn annual flows), forcing AmBank to match rates, waive fees, or offer tailored solutions to prevent churn.

| Metric | 2024/25 |

|---|---|

| Retail switch intent | 38% |

| Comparison tool use | 72% |

| Switching uplift per 25bp | 3–5% |

| Large client deposit | >RM500m |

| Annual volume (large) | >RM1bn |

Preview the Actual Deliverable

AmBank Group Porter's Five Forces Analysis

This preview shows the exact AmBank Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted version you’ll be able to download and use the moment you buy.

You're viewing the final deliverable: the complete, ready-to-use analysis file that will be available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

AmBank Group faces moderate buyer power, intense rivalry from regional banks, and regulatory pressures that shape pricing and product innovation, while digital entrants and fintechs raise the threat of substitutes and heighten the need for strategic differentiation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore AmBank Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Depositors as capital suppliers

Retail and corporate depositors supply AmBank Group’s core funding; Malaysia’s banking system held RM2.2 trillion in deposits in 2024, with digital banks gaining share, so low-cost stable deposits are scarce in 2025.

AmBank must match market rates—average CASA (current account savings account) ratios in Malaysia were ~33% in 2024—and improve service and digital UX to avoid outflows to larger incumbents or neo-banks.

Technology and infrastructure vendors

AmBank relies heavily on third-party cloud, cybersecurity and core-banking vendors; global providers like AWS, Microsoft and Temenos command pricing power since switching costs and technical risks can exceed RM100–300m and take 12–24 months.

In 2024 Malaysia banking cloud spend rose ~18% to an estimated RM1.2bn, so vendor contract stability directly affects AmBank’s cost base and time-to-market for digital services.

AmBank’s digital transformation roadmap assumes multi-year, cost-effective SLAs; loss of favorable terms or major vendor outages would materially raise operating expense and execution risk.

Specialized human capital

High demand for data science, AI and compliance talent in Malaysia — vacancies in fintech rose 42% in 2024 — forces AmBank to compete with local banks and Big Tech, raising average specialist pay 18–25% above baseline roles.

Central bank and regulatory influence

Bank Negara Malaysia (BNM) serves as the key supplier of regulation and liquidity; its Overnight Policy Rate (OPR) hikes to 3.00% as of Dec 2025 raise AmBank Group’s cost of funds and compress net interest margin.

AmBank cannot influence these macro supply conditions and must reshuffle pricing, funding mix, and capital buffers to meet BNM mandates and liquidity coverage ratio requirements.

- BNM OPR 3.00% (Dec 2025)

- Higher funding cost → lower NIM

- Must meet LCR and CAR rules

Wholesale funding and credit rating agencies

Access to wholesale capital markets is critical for AmBank Group to fund large corporate loans and manage liquidity; as of FY2024 AmBank raised RM3.2bn in wholesale debt, showing dependency on institutional suppliers.

Credit rating agencies shape cost of that supply—Moody’s and S&P ratings drive interest spreads; a one-notch downgrade typically raises borrowing spreads by ~50–150 bps, materially increasing funding costs.

Maintaining a strong credit profile is vital: a downgrade would raise AmBank’s cost of borrowing and reduce access to term wholesale lines, squeezing margins and capital planning.

- Wholesale debt raised FY2024: RM3.2bn

- Downgrade impact: +50–150 bps spread

- Risk: higher funding cost, reduced term access

Supplier power squeezes AmBank: rising costs, tighter funding and margin pressure

Suppliers (depositors, vendors, talent, BNM, wholesale markets) exert strong bargaining power on AmBank: tight low‑cost deposit supply (Malaysia deposits RM2.2T in 2024; CASA ~33%), rising cloud spend (RM1.2B, +18% in 2024), specialist pay +18–25%, and BNM OPR 3.00% (Dec 2025) which raises funding cost and compresses NIM; FY2024 wholesale debt RM3.2B—downgrades add ~50–150bps to spreads.

| Metric | Value |

|---|---|

| Malaysia deposits (2024) | RM2.2T |

| CASA (avg 2024) | ~33% |

| Cloud spend (2024) | RM1.2B (+18%) |

| Specialist pay rise (2024) | +18–25% |

| BNM OPR | 3.00% (Dec 2025) |

| AmBank wholesale debt FY2024 | RM3.2B |

| Downgrade spread impact | +50–150bps |

What is included in the product

Provides a concise Porter’s Five Forces assessment tailored to AmBank Group, revealing competitive intensity, buyer and supplier leverage, entry barriers, and substitution risks that shape its profitability and strategic positioning.

A concise Porter's Five Forces snapshot for AmBank Group—pinpoint competitive pressures and regulatory risks at a glance to speed strategic decisions.

Customers Bargaining Power

Low switching costs for retail users

The rise of digital banking and standardized retail products means Malaysian customers can switch banks quickly; AmBank faced net retail deposit outflows in Q3 2024, and industry data shows 38% of customers considered switching in 2024. Mobile apps and instant e-KYC let users move funds over hours for small rate or UX gains, giving individual customers high bargaining power over AmBank.

Price sensitivity in loan products

Malaysian consumers and SMEs react strongly to interest spreads: a 25bp change can shift applications by ~3–5%, and mortgage spreads averaged 1.6% in 2024, per BNM data, so AmBank must match market pricing to keep volumes.

Online comparison portals and fintechs now list real-time rates; search-driven switching rose ~18% in 2023, forcing AmBank to cut margins or add fee waivers, cashback, and bundled advisory to retain clients.

Demands for digital-first experiences

By end-2025 customers treat seamless, hyper-personalized banking as table stakes: 74% of APAC consumers expect real-time personalization, and 62% will switch banks for better digital experiences (2024 Accenture, PwC data). If AmBank misses these tech expectations, churn risk rises quickly as agile digital-first challengers grab market share, giving buyers strong leverage to demand continuous innovation and polished interfaces.

Bargaining strength of corporate clients

Large corporate and government-linked clients wield strong bargaining power at AmBank Group, often representing single-account deposits or lending limits exceeding RM500m and annual transaction volumes >RM1bn, enabling demands for bespoke interest rates, lower fees, and tailored credit facilities.

AmBank must deliver custom cash-management, syndicated loan pricing and relationship banking to retain these high-net-worth accounts or risk loss to larger Malaysian banks like Maybank and CIMB or international banks.

- Single-account deposits often >RM500m

- Annual transaction volumes >RM1bn

- Negotiate lower fees, bespoke rates, credit terms

- Retention requires tailored solutions, relationship depth

Transparency and information access

Greater fee transparency and independent review sites have eroded banks’ information edge; 72% of Malaysian retail customers used online comparison tools in 2024, per a Bank Negara Malaysia survey, cutting time-to-switch and fee surprises.

Customers now see hidden fees, service scores, and product returns before contacting AmBank, raising collective bargaining power and forcing price and service parity across retail banking.

- 72% used comparison tools (BNM, 2024)

- Lowered switching friction — digital onboarding up 18% (AmBank FY2024)

- Public fee matrices increase negotiation leverage

High customer leverage: digital switching and bespoke demands force AmBank rate matches

Customers—both retail and large corporates—hold high bargaining power over AmBank due to easy digital switching, price-sensitive demand (25bp → ~3–5% volume shift), and transparency (72% used comparison tools in 2024); large clients often command bespoke terms (>RM500m deposits, >RM1bn annual flows), forcing AmBank to match rates, waive fees, or offer tailored solutions to prevent churn.

| Metric | 2024/25 |

|---|---|

| Retail switch intent | 38% |

| Comparison tool use | 72% |

| Switching uplift per 25bp | 3–5% |

| Large client deposit | >RM500m |

| Annual volume (large) | >RM1bn |

Preview the Actual Deliverable

AmBank Group Porter's Five Forces Analysis

This preview shows the exact AmBank Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted version you’ll be able to download and use the moment you buy.

You're viewing the final deliverable: the complete, ready-to-use analysis file that will be available instantly after payment.