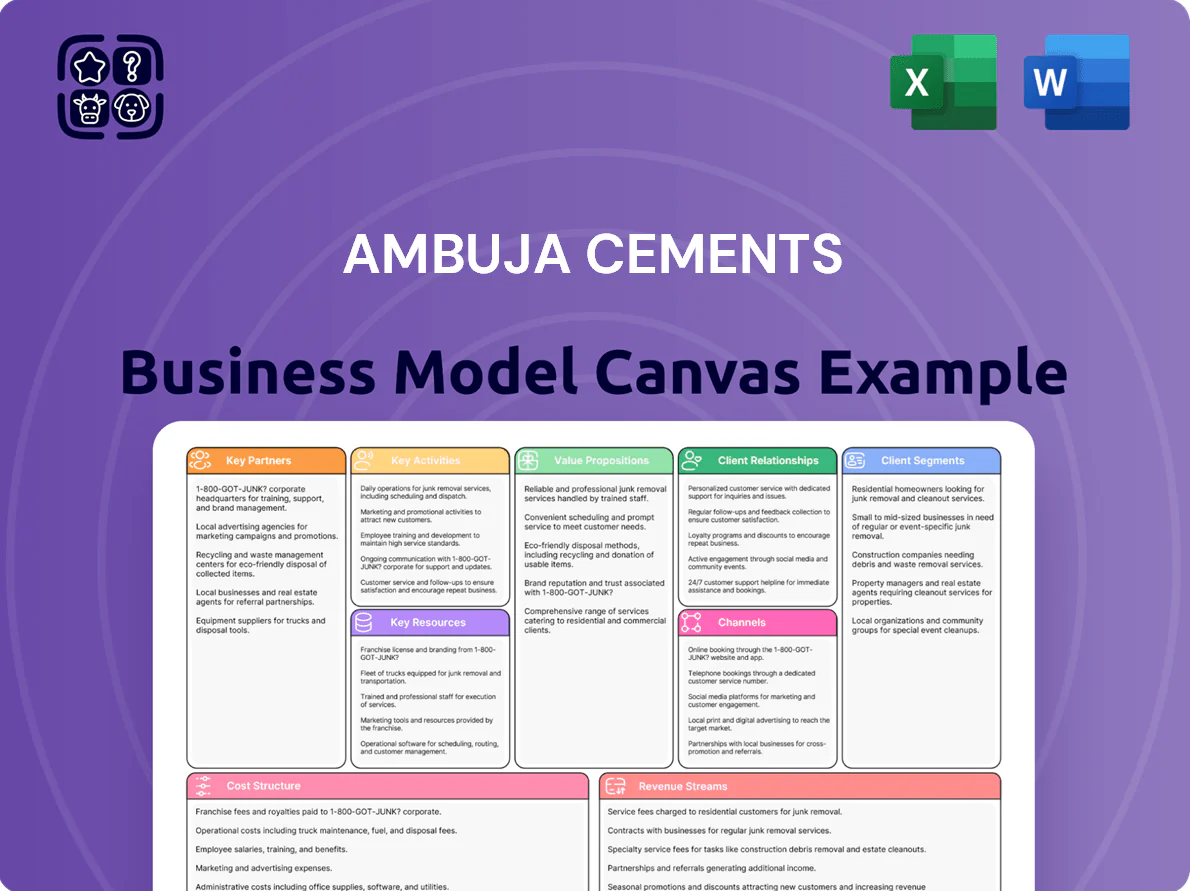

Ambuja Cements Business Model Canvas

Ambuja Cements: Compact Business Model Canvas — Strategy, Partners, Revenue

Unlock the full strategic blueprint behind Ambuja Cements’s business model—this concise Business Model Canvas maps value propositions, key partnerships, revenue streams, and cost drivers that fuel its market leadership in cement and building materials.

Partnerships

Adani Group Ecosystem Synergies

The Adani Group alliance gives Ambuja Cements preferential logistics via Adani Ports & SEZ and Adani Logistics, cutting average outbound lead times by ~15% and lowering freight costs; Ambuja reported consolidated freight savings ~₹180 crore in FY2024 linked to these tie-ups. The deal also secures cheaper power and fuel from Adani Power and renewables, with Ambuja accessing ~200 MW of captive and renewable capacity to trim energy costs and CO2 intensity.

ACC Limited Collaboration

As fellow Adani subsidiaries, Ambuja and ACC Limited share manufacturing know-how, R&D and logistics to drive supply-chain synergies; joint optimisation delivered about 25–35 billion INR in annual cost benefits by FY2024–25, per company disclosures. This operational tie lets Ambuja pursue a unified market strategy while keeping separate brands for distinct customer segments.

Dealer and Distributor Network

Ambuja Cements depends on a 50,000+ channel network of dealers, retailers, and stockists to deliver products across urban and remote rural India, sustaining a national market presence and supporting FY2024 domestic volume of about 23.5 million tonnes. The company spends materially on partner loyalty schemes, dealer training, and a dealer-facing digital platform—investments that cut stockouts and lifted channel sell-through by an estimated 4–6% in 2024.

Raw Material and Fuel Suppliers

Ambuja Cements locks long-term supply contracts for limestone, gypsum, fly ash and coal/petcoke to ensure steady kiln feed; in 2024 it sourced over 25% of its clinker inputs via captive mines and tied mines, reducing input volatility.

It partners with thermal power plants for fly ash—used in blended cements—procurring ~1.2 million tonnes in FY2024 to lower CO2 intensity per tonne of cement.

- Long-term contracts: stabilise prices and supply

- 25%+ clinker from captive/tied mines (2024)

- ~1.2 Mt fly ash procured in FY2024

- Coal/petcoke supply secured for continuous kiln ops

Technology and Research Institutions

Ambuja Cements partners with global tech firms and universities to commercialize low-carbon cements and sustainable construction—Ambuja Kawach (water‑repellent) reached 1.2 million m2 sales in 2024 and pilot Waste Heat Recovery Systems (WHRS) cut specific thermal energy by ~8% at two plants in 2023.

These collaborations fund R&D for decarbonization and automation, helping Ambuja aim for its 2030 target of reducing CO2 intensity by 25% versus 2019.

- Ambuja Kawach: 1.2M m2 sold (2024)

- WHRS pilots: ~8% thermal energy reduction (2023)

- 2030 CO2 intensity target: -25% vs 2019

Ambuja boosts efficiency: ₹180cr freight savings, 25% clinker, −25% CO2 by 2030

Adani tie-ups cut freight ~15% saving ~₹180 crore (FY2024); captive/tied mines supplied 25%+ clinker (2024); fly ash procured ~1.2 Mt (FY2024); Ambuja Kawach sales 1.2M m2 (2024); WHRS pilots −8% thermal energy (2023); 2030 CO2 intensity target −25% vs 2019.

| Metric | 2023–25 value |

|---|---|

| Freight savings | ~₹180 crore (FY2024) |

| Clinker from captive/tied mines | 25%+ (2024) |

| Fly ash procured | ~1.2 Mt (FY2024) |

| Ambuja Kawach sales | 1.2M m2 (2024) |

| WHRS thermal reduction | ~8% (2023) |

| 2030 CO2 target | −25% vs 2019 |

What is included in the product

A concise Business Model Canvas for Ambuja Cements mapping its nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—reflecting its integrated cement-manufacturing value chain, distribution-led sales model, sustainability and cost-efficiency advantages, competitive risks, and strategic levers for investors and analysts.

High-level, editable Business Model Canvas for Ambuja Cements that condenses strategy into a one-page snapshot, saving hours of structuring and ideal for quick executive reviews or team collaboration.

Activities

Manufacturing and Quality Control

Ambuja Cements runs large-scale clinker and cement production—Ordinary Portland Cement and Portland Pozzolana Cement—across 8 integrated plants and 10 grinding units, with combined capacity ~36.3 million tonnes per annum (2024).

Plants use PLC/SCADA automation and inline analyzers; strict QC labs perform >1,200 daily tests to meet IS, ASTM and EN standards, supporting FY2024 revenue of ₹18,162 crore and <0.5% product rejection.

Supply Chain and Logistics Management

Managing heavy raw materials and finished cement keeps costs low; transport accounts for ~18% of Ambuja Cements' FY2024 logistics cost helping protect EBITDA margins near 17.5% (FY2024). The firm uses multimodal rail, road and coastal shipping from 12 plants to 200+ distribution centers, cutting transit cost per tonne by ~12% since 2021.

Real-time digital tracking and inventory systems link 600+ truck fleets and rail rakes, reducing stockouts by 28% and lowering working capital tied to inventories by ~9 days versus 2020.

Sustainable Operations and Co-processing

Ambuja Cements co-processes alternative fuels and raw materials in kilns, safely disposing industrial and municipal waste to achieve thermal substitution—over 15% thermal substitution rate in FY2024, cutting coal use and CO2 intensity; co-processing revenues and cost savings reduced fuel spend by ~INR 350 crore in FY2024. The firm also runs water-harvesting and land-reclamation projects, remaining water-positive since 2017 with 2024 net positive water balance of ~6.2 million cubic metres.

Marketing and Brand Building

Ambuja Cements keeps premium positioning through sustained branding spend—about INR 250 crore in FY2024—using TV, digital and 45+ ground campaigns to highlight product strength and durability, supporting 6% volume growth in FY2024.

Marketing is segmented: homeowner-focused digital tools, contractor loyalty programs, and architect partnerships, driving 12% sales from institutional channels in 2024.

- INR 250 crore marketing spend FY2024

- 45+ ground campaigns, 6% volume growth FY2024

- 12% revenues from institutional channels 2024

Technical Services and Customer Support

Ambuja Cements deploys qualified civil engineers for on-site technical assistance—conducting concrete mix trials, giving construction guidance, and training masons—to ensure correct use of its specialized cement and improve structure durability; in 2024 Ambuja’s technical service reach covered over 120,000 site visits across India, reducing reported rework by ~18% year-on-year.

- On-site mix trials and guidance

- Mason training for best practices

- 120,000+ site visits in 2024

- ~18% drop in rework vs 2023

Ambuja: 36.3 Mtpa, INR18,162cr revenue, 17.5% EBITDA, water-positive & 15% TSR

Ambuja runs integrated clinker/cement production (36.3 Mtpa, 8 plants, 10 grinders), PLC/SCADA QC (1,200+ tests/day), multimodal logistics (18% of logistics cost, 12% transit saving since 2021), 15% thermal substitution, water-positive (+6.2 M m3 2024), INR 18,162 crore revenue and 17.5% EBITDA margin FY2024; 120,000+ site visits drove ~18% rework reduction.

| Metric | 2024 |

|---|---|

| Capacity | 36.3 Mtpa |

| Revenue | INR 18,162 cr |

| EBITDA | 17.5% |

| Thermal substitution | 15% |

| Water balance | +6.2 M m3 |

Preview Before You Purchase

Business Model Canvas

The Business Model Canvas for Ambuja Cements shown here is the actual deliverable, not a mockup—it's a direct excerpt from the file you will receive after purchase.

When you complete your order, you'll get the exact same professional document, formatted and ready to use for strategy, presentation, or editing in Word and Excel.

No placeholders or marketing samples—this preview reflects the full content and structure you'll download instantly upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Ambuja Cements: Compact Business Model Canvas — Strategy, Partners, Revenue

Unlock the full strategic blueprint behind Ambuja Cements’s business model—this concise Business Model Canvas maps value propositions, key partnerships, revenue streams, and cost drivers that fuel its market leadership in cement and building materials.

Partnerships

Adani Group Ecosystem Synergies

The Adani Group alliance gives Ambuja Cements preferential logistics via Adani Ports & SEZ and Adani Logistics, cutting average outbound lead times by ~15% and lowering freight costs; Ambuja reported consolidated freight savings ~₹180 crore in FY2024 linked to these tie-ups. The deal also secures cheaper power and fuel from Adani Power and renewables, with Ambuja accessing ~200 MW of captive and renewable capacity to trim energy costs and CO2 intensity.

ACC Limited Collaboration

As fellow Adani subsidiaries, Ambuja and ACC Limited share manufacturing know-how, R&D and logistics to drive supply-chain synergies; joint optimisation delivered about 25–35 billion INR in annual cost benefits by FY2024–25, per company disclosures. This operational tie lets Ambuja pursue a unified market strategy while keeping separate brands for distinct customer segments.

Dealer and Distributor Network

Ambuja Cements depends on a 50,000+ channel network of dealers, retailers, and stockists to deliver products across urban and remote rural India, sustaining a national market presence and supporting FY2024 domestic volume of about 23.5 million tonnes. The company spends materially on partner loyalty schemes, dealer training, and a dealer-facing digital platform—investments that cut stockouts and lifted channel sell-through by an estimated 4–6% in 2024.

Raw Material and Fuel Suppliers

Ambuja Cements locks long-term supply contracts for limestone, gypsum, fly ash and coal/petcoke to ensure steady kiln feed; in 2024 it sourced over 25% of its clinker inputs via captive mines and tied mines, reducing input volatility.

It partners with thermal power plants for fly ash—used in blended cements—procurring ~1.2 million tonnes in FY2024 to lower CO2 intensity per tonne of cement.

- Long-term contracts: stabilise prices and supply

- 25%+ clinker from captive/tied mines (2024)

- ~1.2 Mt fly ash procured in FY2024

- Coal/petcoke supply secured for continuous kiln ops

Technology and Research Institutions

Ambuja Cements partners with global tech firms and universities to commercialize low-carbon cements and sustainable construction—Ambuja Kawach (water‑repellent) reached 1.2 million m2 sales in 2024 and pilot Waste Heat Recovery Systems (WHRS) cut specific thermal energy by ~8% at two plants in 2023.

These collaborations fund R&D for decarbonization and automation, helping Ambuja aim for its 2030 target of reducing CO2 intensity by 25% versus 2019.

- Ambuja Kawach: 1.2M m2 sold (2024)

- WHRS pilots: ~8% thermal energy reduction (2023)

- 2030 CO2 intensity target: -25% vs 2019

Ambuja boosts efficiency: ₹180cr freight savings, 25% clinker, −25% CO2 by 2030

Adani tie-ups cut freight ~15% saving ~₹180 crore (FY2024); captive/tied mines supplied 25%+ clinker (2024); fly ash procured ~1.2 Mt (FY2024); Ambuja Kawach sales 1.2M m2 (2024); WHRS pilots −8% thermal energy (2023); 2030 CO2 intensity target −25% vs 2019.

| Metric | 2023–25 value |

|---|---|

| Freight savings | ~₹180 crore (FY2024) |

| Clinker from captive/tied mines | 25%+ (2024) |

| Fly ash procured | ~1.2 Mt (FY2024) |

| Ambuja Kawach sales | 1.2M m2 (2024) |

| WHRS thermal reduction | ~8% (2023) |

| 2030 CO2 target | −25% vs 2019 |

What is included in the product

A concise Business Model Canvas for Ambuja Cements mapping its nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—reflecting its integrated cement-manufacturing value chain, distribution-led sales model, sustainability and cost-efficiency advantages, competitive risks, and strategic levers for investors and analysts.

High-level, editable Business Model Canvas for Ambuja Cements that condenses strategy into a one-page snapshot, saving hours of structuring and ideal for quick executive reviews or team collaboration.

Activities

Manufacturing and Quality Control

Ambuja Cements runs large-scale clinker and cement production—Ordinary Portland Cement and Portland Pozzolana Cement—across 8 integrated plants and 10 grinding units, with combined capacity ~36.3 million tonnes per annum (2024).

Plants use PLC/SCADA automation and inline analyzers; strict QC labs perform >1,200 daily tests to meet IS, ASTM and EN standards, supporting FY2024 revenue of ₹18,162 crore and <0.5% product rejection.

Supply Chain and Logistics Management

Managing heavy raw materials and finished cement keeps costs low; transport accounts for ~18% of Ambuja Cements' FY2024 logistics cost helping protect EBITDA margins near 17.5% (FY2024). The firm uses multimodal rail, road and coastal shipping from 12 plants to 200+ distribution centers, cutting transit cost per tonne by ~12% since 2021.

Real-time digital tracking and inventory systems link 600+ truck fleets and rail rakes, reducing stockouts by 28% and lowering working capital tied to inventories by ~9 days versus 2020.

Sustainable Operations and Co-processing

Ambuja Cements co-processes alternative fuels and raw materials in kilns, safely disposing industrial and municipal waste to achieve thermal substitution—over 15% thermal substitution rate in FY2024, cutting coal use and CO2 intensity; co-processing revenues and cost savings reduced fuel spend by ~INR 350 crore in FY2024. The firm also runs water-harvesting and land-reclamation projects, remaining water-positive since 2017 with 2024 net positive water balance of ~6.2 million cubic metres.

Marketing and Brand Building

Ambuja Cements keeps premium positioning through sustained branding spend—about INR 250 crore in FY2024—using TV, digital and 45+ ground campaigns to highlight product strength and durability, supporting 6% volume growth in FY2024.

Marketing is segmented: homeowner-focused digital tools, contractor loyalty programs, and architect partnerships, driving 12% sales from institutional channels in 2024.

- INR 250 crore marketing spend FY2024

- 45+ ground campaigns, 6% volume growth FY2024

- 12% revenues from institutional channels 2024

Technical Services and Customer Support

Ambuja Cements deploys qualified civil engineers for on-site technical assistance—conducting concrete mix trials, giving construction guidance, and training masons—to ensure correct use of its specialized cement and improve structure durability; in 2024 Ambuja’s technical service reach covered over 120,000 site visits across India, reducing reported rework by ~18% year-on-year.

- On-site mix trials and guidance

- Mason training for best practices

- 120,000+ site visits in 2024

- ~18% drop in rework vs 2023

Ambuja: 36.3 Mtpa, INR18,162cr revenue, 17.5% EBITDA, water-positive & 15% TSR

Ambuja runs integrated clinker/cement production (36.3 Mtpa, 8 plants, 10 grinders), PLC/SCADA QC (1,200+ tests/day), multimodal logistics (18% of logistics cost, 12% transit saving since 2021), 15% thermal substitution, water-positive (+6.2 M m3 2024), INR 18,162 crore revenue and 17.5% EBITDA margin FY2024; 120,000+ site visits drove ~18% rework reduction.

| Metric | 2024 |

|---|---|

| Capacity | 36.3 Mtpa |

| Revenue | INR 18,162 cr |

| EBITDA | 17.5% |

| Thermal substitution | 15% |

| Water balance | +6.2 M m3 |

Preview Before You Purchase

Business Model Canvas

The Business Model Canvas for Ambuja Cements shown here is the actual deliverable, not a mockup—it's a direct excerpt from the file you will receive after purchase.

When you complete your order, you'll get the exact same professional document, formatted and ready to use for strategy, presentation, or editing in Word and Excel.

No placeholders or marketing samples—this preview reflects the full content and structure you'll download instantly upon purchase.