Ambuja Cements Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ambuja Cements’s competitive dynamics, market pressures, and strategic advantages in detail.

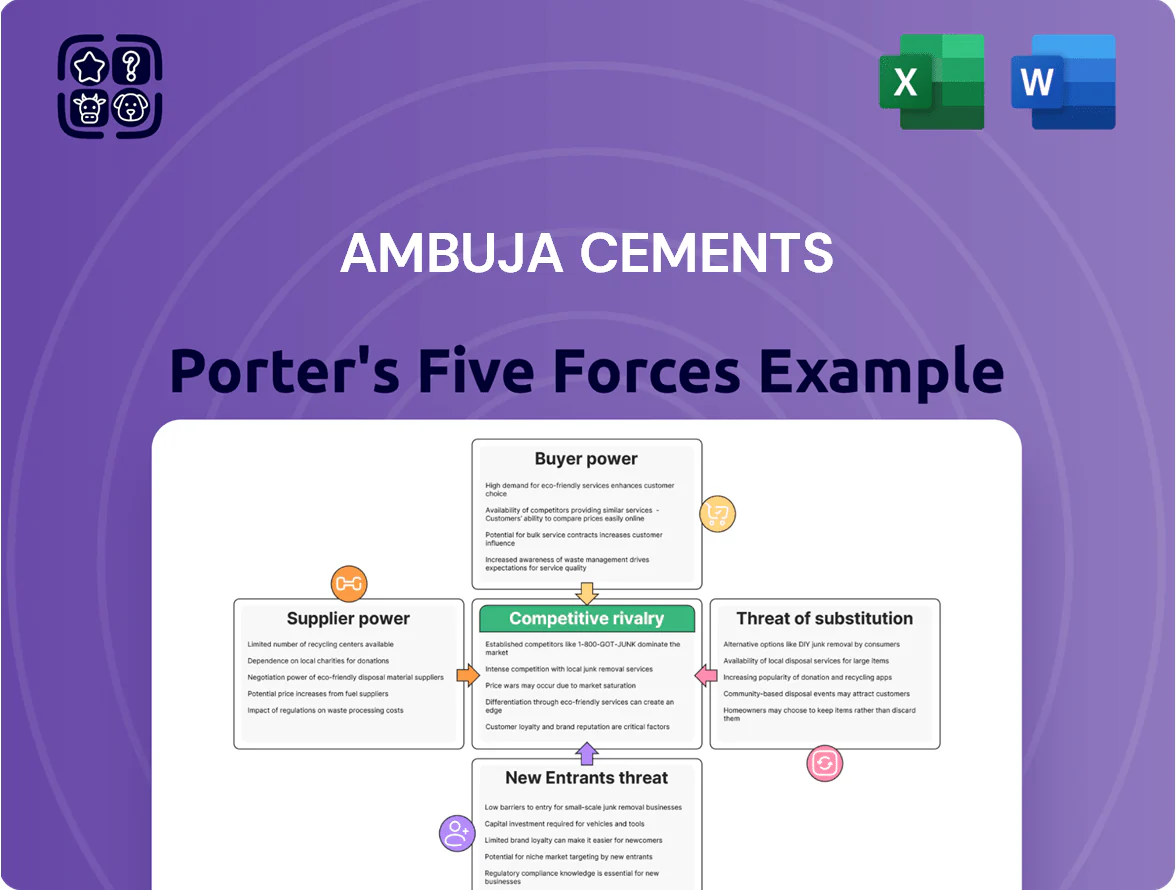

Suppliers Bargaining Power

Volatility in Energy and Fuel Procurement

Petcoke and coal made up roughly 28–32% of Ambuja Cements’ variable production cost in 2025; petcoke imports rose 14% YoY to 6.2 million tonnes, tying fuel spend to international prices.

Because about 40% of thermal fuel needs are met through imports or global-index contracts, sudden Brent or coal-price moves (eg, a $20/tonne coal jump) can shave 100–150 bps off operating margin within a quarter.

Access to Limestone and Raw Materials

Limestone, the key input for clinker, is obtained via government mining leases where the state sets auction terms and royalty rates; in 2024 India raised mineral royalties by up to 10% in some states, increasing feedstock costs for Ambuja Cements (Adani Group) and peers. Ambuja needs multi-decade reserves—company disclosures show ~30–40 years equivalent at current production—to avoid supply shocks as environmental clearances tighten and mining caps rise.

Logistics and Transportation Dependencies

Moving cement needs heavy use of Indian Railways and trucks; freight can be 12–18% of customer price, so rail tariffs and trucking rates strongly shape Ambuja Cements’ cost base. In FY2024 Ambuja reported logistics expense rise of ~9% y/y, showing sensitivity to transport inflation; a 10% freight hike would cut operating margin by roughly 1–1.5 percentage points, hurting regional competitiveness. Disruptions in rail or diesel supply quickly raise costs and shift market share.

Adani Group Ecosystem Synergies

As part of the Adani Group, Ambuja Cements gains power, logistics and port synergies that cut supplier bargaining power by lowering input costs and delivery times; Adani’s captive power reduced Ambuja’s fuel purchase exposure—coal imports dropped ~18% in FY2024 versus peers.

Backward integration lets Ambuja bypass third-party markups, using group procurement to secure clinker, fuel and freight at scale; this reduced COGS pressure and improved EBITDA margin resilience in 2024.

- Captive power lowers fuel spend

- Port access shortens lead times

- Group procurement increases purchasing leverage

- FY2024: ~18% lower coal import reliance

Technological and Equipment Suppliers

The shift to green cement and automation needs specialized kilns and grinding units from a few global engineering firms, giving suppliers moderate bargaining power because of technical complexity and recurrent maintenance contracts.

Ambuja Cements’ planned 2025 expansion—~5 Mtpa capacity additions and capex ~Rs 4,000 crore—raises volume leverage, enabling price concessions, longer warranties, and bundled-servicing terms.

- Few global suppliers → moderate power

- Specialized equipment → long-term service dependency

- Ambuja 2025 capex Rs 4,000 crore → strong volume leverage

- Bulk orders → negotiate price, warranty, service

Fuel costs, logistics, and capex drive margins—coal import cuts boost Ambuja's leverage

Suppliers have moderate power: fuel (petcoke/coal) drove 28–32% of variable costs in 2025, with 40% imports; a $20/tonne coal rise cuts margins ~100–150bps/quarter. Limestone royalties rose up to 10% in 2024; Ambuja holds 30–40 years reserves. Logistics = 12–18% of price; FY2024 logistics +9% y/y. Adani synergies cut coal imports ~18% in FY2024, and 2025 capex Rs 4,000 crore boosts buying leverage.

| Metric | Value (latest) |

|---|---|

| Fuel share of variable cost | 28–32% (2025) |

| Import exposure (thermal fuel) | ≈40% |

| Petcoke imports | 6.2 Mt (2025, +14% YoY) |

| Coal import reduction | −18% (Ambuja vs peers, FY2024) |

| Limestone reserves | 30–40 yrs equiv. |

| Logistics share | 12–18% of price |

| Logistics cost change | +9% y/y (FY2024) |

| Planned capex | Rs 4,000 crore (2025) |

What is included in the product

Tailored Porter's Five Forces assessment for Ambuja Cements, revealing competitive intensity, buyer and supplier power, substitution risks, and barriers deterring new entrants to clarify strategic positioning and profitability drivers.

Ambuja Cements Porter's Five Forces summarized on one sheet—quickly spot supplier, buyer, and competitive pressures to guide pricing and capacity decisions.

Customers Bargaining Power

Fragmented Retail Buyer Base

The individual home builder segment accounts for about 40–45% of India’s cement consumption and has very low per-buyer bargaining power, since purchases are small and irregular (CRISIL, 2024: India cement demand ~360 Mt). Dealers and brand recall drive choices more than price haggling, so Ambuja Cements (2024 revenue Rs 26,072 crore) sustains broadly stable retail pricing across regions thanks to this fragmentation.

Institutional and Infrastructure Leverage

Large real-estate developers and government infrastructure projects exert strong bargaining power over Ambuja Cements because single contracts can exceed 100,000 tonnes, pushing firms into competitive tenders that drove Ambuja to offer discounts of 3–6% on large bids in 2024.

Low Switching Costs for Commodity Products

Despite Ambuja Cements’ brand work, cement is still seen as a commodity by many; industry data shows organized players (Ambuja, UltraTech, Shree) held ~70% of India’s 2024 capacity, so buyers switch easily on price differences. Low switching costs mean a 5–8% price gap can push volume toward rivals, keeping Ambuja under constant pressure to stay price-competitive while sustaining quality and a FY2024 gross margin near 26%.

Brand Equity and Trust

Ambuja Cements’ Giant brand drives loyalty that reduces price sensitivity; branded volumes accounted for ~62% of sales in FY2024, supporting a ~3–5% premium versus local unorganized players.

In premium housing, builders prefer Ambuja for perceived structural reliability, aiding repeat contracts and higher-mix sales; national urban housing starts rose 11% in 2024, boosting demand for trusted brands.

- Branded share ~62% FY2024

- Price premium ~3–5%

- Urban housing starts +11% 2024

Digitalization of Sales and Distribution

The 2025 rise of digital procurement platforms gives buyers real-time pricing and regional comparisons, raising market transparency and nudging bargaining power toward customers who can track price swings across states.

Ambuja combats this by rolling out dealer-facing apps and value-added services—its Ambuja B2B platform reported 18% dealer adoption in 2025—locking loyalty and blunting price-only switching.

- 2025 platforms = real-time pricing

- Transparency ↑, regional monitoring easier

- Ambuja B2B app: 18% dealer adoption 2025

- Value services used to retain dealers

Mixed buyer power: branded strength offsets big-bid discounts as dealer app adoption rises

Customers’ power is mixed: fragmented individual buyers (~40–45% of demand) have low bargaining clout, while large developers/govt contracts (often >100,000 t) exert strong pressure—Ambuja offered 3–6% discounts on big bids in 2024; branded volumes ~62% FY2024 support a 3–5% premium; Ambuja B2B app dealer adoption 18% in 2025, countering rising transparency from digital procurement.

| Metric | Value |

|---|---|

| Individual buyer share | 40–45% |

| Branded volume | 62% FY2024 |

| Discounts on large bids | 3–6% 2024 |

| Gross margin | ~26% FY2024 |

| Dealer app adoption | 18% 2025 |

Full Version Awaits

Ambuja Cements Porter's Five Forces Analysis

This preview shows the exact Ambuja Cements Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document provides a concise assessment of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with data-driven insights. It's fully formatted, ready to download and use the moment you buy. Purchase grants instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ambuja Cements’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Energy and Fuel Procurement

Petcoke and coal made up roughly 28–32% of Ambuja Cements’ variable production cost in 2025; petcoke imports rose 14% YoY to 6.2 million tonnes, tying fuel spend to international prices.

Because about 40% of thermal fuel needs are met through imports or global-index contracts, sudden Brent or coal-price moves (eg, a $20/tonne coal jump) can shave 100–150 bps off operating margin within a quarter.

Access to Limestone and Raw Materials

Limestone, the key input for clinker, is obtained via government mining leases where the state sets auction terms and royalty rates; in 2024 India raised mineral royalties by up to 10% in some states, increasing feedstock costs for Ambuja Cements (Adani Group) and peers. Ambuja needs multi-decade reserves—company disclosures show ~30–40 years equivalent at current production—to avoid supply shocks as environmental clearances tighten and mining caps rise.

Logistics and Transportation Dependencies

Moving cement needs heavy use of Indian Railways and trucks; freight can be 12–18% of customer price, so rail tariffs and trucking rates strongly shape Ambuja Cements’ cost base. In FY2024 Ambuja reported logistics expense rise of ~9% y/y, showing sensitivity to transport inflation; a 10% freight hike would cut operating margin by roughly 1–1.5 percentage points, hurting regional competitiveness. Disruptions in rail or diesel supply quickly raise costs and shift market share.

Adani Group Ecosystem Synergies

As part of the Adani Group, Ambuja Cements gains power, logistics and port synergies that cut supplier bargaining power by lowering input costs and delivery times; Adani’s captive power reduced Ambuja’s fuel purchase exposure—coal imports dropped ~18% in FY2024 versus peers.

Backward integration lets Ambuja bypass third-party markups, using group procurement to secure clinker, fuel and freight at scale; this reduced COGS pressure and improved EBITDA margin resilience in 2024.

- Captive power lowers fuel spend

- Port access shortens lead times

- Group procurement increases purchasing leverage

- FY2024: ~18% lower coal import reliance

Technological and Equipment Suppliers

The shift to green cement and automation needs specialized kilns and grinding units from a few global engineering firms, giving suppliers moderate bargaining power because of technical complexity and recurrent maintenance contracts.

Ambuja Cements’ planned 2025 expansion—~5 Mtpa capacity additions and capex ~Rs 4,000 crore—raises volume leverage, enabling price concessions, longer warranties, and bundled-servicing terms.

- Few global suppliers → moderate power

- Specialized equipment → long-term service dependency

- Ambuja 2025 capex Rs 4,000 crore → strong volume leverage

- Bulk orders → negotiate price, warranty, service

Fuel costs, logistics, and capex drive margins—coal import cuts boost Ambuja's leverage

Suppliers have moderate power: fuel (petcoke/coal) drove 28–32% of variable costs in 2025, with 40% imports; a $20/tonne coal rise cuts margins ~100–150bps/quarter. Limestone royalties rose up to 10% in 2024; Ambuja holds 30–40 years reserves. Logistics = 12–18% of price; FY2024 logistics +9% y/y. Adani synergies cut coal imports ~18% in FY2024, and 2025 capex Rs 4,000 crore boosts buying leverage.

| Metric | Value (latest) |

|---|---|

| Fuel share of variable cost | 28–32% (2025) |

| Import exposure (thermal fuel) | ≈40% |

| Petcoke imports | 6.2 Mt (2025, +14% YoY) |

| Coal import reduction | −18% (Ambuja vs peers, FY2024) |

| Limestone reserves | 30–40 yrs equiv. |

| Logistics share | 12–18% of price |

| Logistics cost change | +9% y/y (FY2024) |

| Planned capex | Rs 4,000 crore (2025) |

What is included in the product

Tailored Porter's Five Forces assessment for Ambuja Cements, revealing competitive intensity, buyer and supplier power, substitution risks, and barriers deterring new entrants to clarify strategic positioning and profitability drivers.

Ambuja Cements Porter's Five Forces summarized on one sheet—quickly spot supplier, buyer, and competitive pressures to guide pricing and capacity decisions.

Customers Bargaining Power

Fragmented Retail Buyer Base

The individual home builder segment accounts for about 40–45% of India’s cement consumption and has very low per-buyer bargaining power, since purchases are small and irregular (CRISIL, 2024: India cement demand ~360 Mt). Dealers and brand recall drive choices more than price haggling, so Ambuja Cements (2024 revenue Rs 26,072 crore) sustains broadly stable retail pricing across regions thanks to this fragmentation.

Institutional and Infrastructure Leverage

Large real-estate developers and government infrastructure projects exert strong bargaining power over Ambuja Cements because single contracts can exceed 100,000 tonnes, pushing firms into competitive tenders that drove Ambuja to offer discounts of 3–6% on large bids in 2024.

Low Switching Costs for Commodity Products

Despite Ambuja Cements’ brand work, cement is still seen as a commodity by many; industry data shows organized players (Ambuja, UltraTech, Shree) held ~70% of India’s 2024 capacity, so buyers switch easily on price differences. Low switching costs mean a 5–8% price gap can push volume toward rivals, keeping Ambuja under constant pressure to stay price-competitive while sustaining quality and a FY2024 gross margin near 26%.

Brand Equity and Trust

Ambuja Cements’ Giant brand drives loyalty that reduces price sensitivity; branded volumes accounted for ~62% of sales in FY2024, supporting a ~3–5% premium versus local unorganized players.

In premium housing, builders prefer Ambuja for perceived structural reliability, aiding repeat contracts and higher-mix sales; national urban housing starts rose 11% in 2024, boosting demand for trusted brands.

- Branded share ~62% FY2024

- Price premium ~3–5%

- Urban housing starts +11% 2024

Digitalization of Sales and Distribution

The 2025 rise of digital procurement platforms gives buyers real-time pricing and regional comparisons, raising market transparency and nudging bargaining power toward customers who can track price swings across states.

Ambuja combats this by rolling out dealer-facing apps and value-added services—its Ambuja B2B platform reported 18% dealer adoption in 2025—locking loyalty and blunting price-only switching.

- 2025 platforms = real-time pricing

- Transparency ↑, regional monitoring easier

- Ambuja B2B app: 18% dealer adoption 2025

- Value services used to retain dealers

Mixed buyer power: branded strength offsets big-bid discounts as dealer app adoption rises

Customers’ power is mixed: fragmented individual buyers (~40–45% of demand) have low bargaining clout, while large developers/govt contracts (often >100,000 t) exert strong pressure—Ambuja offered 3–6% discounts on big bids in 2024; branded volumes ~62% FY2024 support a 3–5% premium; Ambuja B2B app dealer adoption 18% in 2025, countering rising transparency from digital procurement.

| Metric | Value |

|---|---|

| Individual buyer share | 40–45% |

| Branded volume | 62% FY2024 |

| Discounts on large bids | 3–6% 2024 |

| Gross margin | ~26% FY2024 |

| Dealer app adoption | 18% 2025 |

Full Version Awaits

Ambuja Cements Porter's Five Forces Analysis

This preview shows the exact Ambuja Cements Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document provides a concise assessment of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with data-driven insights. It's fully formatted, ready to download and use the moment you buy. Purchase grants instant access to this same file.