Amcor PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive advantage with our targeted PESTLE Analysis of Amcor—uncover how political shifts, economic trends, social expectations, technological advances, legal changes, and environmental pressures will shape its strategy and performance; buy the full report to access deep, actionable insights ready for investment theses, strategic planning, or boardroom use.

Political factors

Trade Protectionism and Tariffs

Global trade in late 2025 remains affected by protectionism: US-China tariff frictions and EU safeguard measures raised average applied tariffs on packaging inputs by ~1.2 percentage points in 2024–25, per WTO data, increasing Amcor's cross-border input costs and logistics premiums.

For Amcor, tariff volatility elevates landed cost of polymers and aluminum, risking margin erosion—management reported input-cost headwinds of ~USD 120–160m in FY2024–25 tied to trade measures.

Strategic responses—nearshoring, diversified sourcing, tariff engineering, and localized production—are essential to sustain price competitiveness and supply continuity across its 40+ markets.

Government Sustainability Mandates

Governments are tightening plastic rules to hit 2030 climate targets, with the EU’s Single-Use Plastics Directive and extended producer responsibility expanding to 2025–2030; over 60 countries had national plastic waste policies by 2024. These mandates pressure packaging firms like Amcor to shift faster to recyclable/compostable materials to avoid fines or market bans, risking share loss if delayed. Amcor must sustain robust government relations and compliance spend—Amcor reported US$2.1bn capex in FY2024—to navigate evolving design and sourcing laws.

Geopolitical Stability in Emerging Markets

Amcor operates extensively in emerging markets—around 35% of 2024 revenue came from Asia-Pacific and Latin America—where political instability or sudden leadership changes can trigger abrupt regulatory shifts affecting packaging standards and taxes.

Political unrest or civil conflict risks physical assets and disrupted distribution; in 2023 supply-chain incidents in Latin America increased logistics costs by an estimated 2–3% for packaging firms.

Continuous monitoring of geopolitical indicators is essential for risk mitigation and capital allocation, especially as Amcor pursues ~4–6% organic growth in high-growth but volatile regions.

Global Tax Harmonization Efforts

The OECD/G20 Pillar Two global minimum tax (15%) and rising tax reform in 20+ jurisdictions can raise Amcor’s effective tax rate, potentially increasing cash tax outflows versus pre-2021 levels; multinationals reported average ETR rises of 1–3 percentage points in early adopters. Changes in green-tax incentives—e.g., EU carbon border adjustments and national green credits—can offset costs if Amcor’s packaging plants qualify.

Supply Chain Resiliency Policies

National-security driven policies push governments to onshore essential packaging; US CHIPS and Inflation Reduction Act subsidies and EU strategic autonomy plans increased local procurement—Amcor must expand regional plants to win contracts worth billions (e.g., government healthcare packaging procurement growth ~5–7% CAGR 2023–25).

Balancing global scale with localized manufacturing raises capex and operating costs; meeting local-content rules is now often mandatory to secure large public-sector deals and protect market share.

- Onshoring trend: rising government procurement of domestic packaging

- Capex impact: higher regional investment to meet local-content rules

- Revenue risk: noncompliance can forfeit multi-year public contracts

- Strategy: hybrid global-local footprint to retain scale benefits

Amcor faces margin squeeze: tariffs, Pillar Two and 60+ plastics rules hit costs, capex

Political risks—tariff spikes (+1.2 pp avg. 2024–25), OECD Pillar Two (15%) raising ETR ~1–3 pp, and 60+ national plastics regulations—pressure Amcor’s margins, capex (US$2.1bn FY2024) and sourcing; nearshoring and local-content compliance are required to secure public contracts and mitigate unrest in 35% revenue markets.

| Metric | Value/Impact |

|---|---|

| Tariff change (2024–25) | +1.2 pp |

| Input-cost hit | US$120–160m |

| Capex FY2024 | US$2.1bn |

| Revenue in EMs | ~35% |

| OECD Pillar Two | 15%; ETR +1–3 pp |

| Countries with plastics policy (2024) | 60+ |

What is included in the product

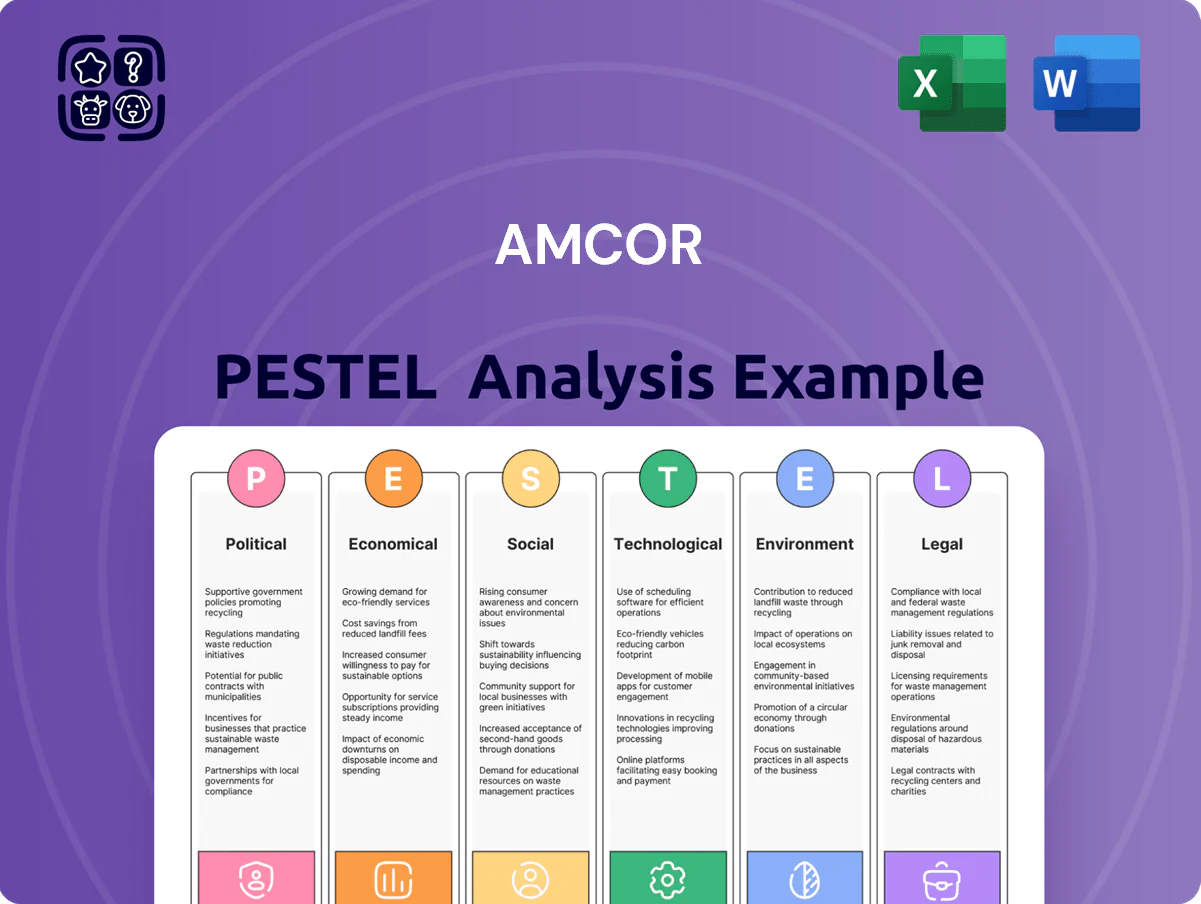

Explores how macro-environmental factors uniquely affect Amcor across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and industry trends to identify risks and opportunities.

Condenses Amcor's PESTLE into a sharp, shareable summary—segmented by category and written in plain language—so teams can quickly assess external risks, market drivers, and strategic implications for faster decision-making and presentation-ready use.

Economic factors

Raw Material Price Volatility

As 2025 ends, polymer, aluminum and paper input costs for Amcor remain tied to oil and commodity swings—polypropylene rose ~18% YoY and aluminum LME prices were up ~12% in 2025—forcing Amcor to rely on hedging and pass-throughs; failure to offset spikes can compress margins (Amcor reported a 2025 H1 gross margin of ~18.5%), so agile procurement and contract pricing are critical.

Global Inflationary Pressures

Persistent inflation—global CPI averaging about 4.5% in 2024 with core inflation ~5% in key markets—erodes consumer purchasing power and raises Amcor’s input costs for resin, paper and freight, pressuring margins.

Rising labor (+3–6% wage inflation in 2023–24) and energy costs force Amcor toward automation and OEE improvements to protect adjusted EBIT margin (target ~12–14%).

Modeling the inflation-demand interplay is essential: NielsenIQ reported FMCG volume declines of ~1–2% YoY in 2024, informing Amcor’s volume forecasts and strategic price passes.

Currency Exchange Rate Fluctuations

As a US-dollar reported company operating across 40+ currencies, Amcor faces material FX risk: a 5% USD appreciation versus the euro, yuan or AUD could swing reported EBITDA by an estimated 2–4%, based on FY2024 revenue mix where ~35% was Europe/APAC.

Translation effects drove a ~US$30–50m annualized P&L impact in recent quarters; hedging and natural offsets limit volatility but not fully.

Financial teams must track ECB/People’s Bank of China/RBA moves and USD rate differentials—Fed tightening in 2022–24 widened FX swings and remains a primary driver.

Interest Rate Impacts on Capital

The prevailing interest rate environment at end-2025 raised global policy rates to about 4.5% on average, increasing Amcor’s average borrowing cost and pressuring free cash flow for expansions and acquisitions.

Higher rates make M&A pricier, prompting Amcor to favor internal R&D funding; its net debt/EBITDA of ~2.1x and interest coverage near 6x will be key metrics for investors monitoring monetary cycles.

- End-2025 policy rates ~4.5%

- Amcor net debt/EBITDA ~2.1x

- Interest coverage ~6x

- Higher rates favor internal funding over aggressive M&A

Emerging Market Growth Potential

Economic expansion in Asia-Pacific and Latin America—projected to account for over 60% of global GDP growth through 2025—boosts demand for packaging as rising middle classes increase spend on packaged food, beverages and personal care; e.g., Asia-Pacific FMCG volume growth ~3–4% CAGR (2023–25). Amcor’s market share gains hinge on scaling local manufacturing and supply chains to meet higher unit volumes while controlling capex and logistics costs.

- Asia-Pacific & Latin America driving ~60% of global GDP growth to 2025

- FMCG volume growth in region ~3–4% CAGR (2023–25)

- Amcor growth dependent on local scale, capex efficiency, supply-chain resilience

Input-cost surge, FX & rates squeeze margins while APAC/LatAm volume offsets risk

Input-cost volatility (polypropylene +18% YoY; aluminum LME +12% in 2025) and ~4.5% global CPI compress margins (2025 H1 gross ~18.5%); FX (5% USD move → ~2–4% EBITDA swing) and end‑2025 policy rates ~4.5% raise borrowing costs (net debt/EBITDA ~2.1x; interest coverage ~6x); APAC/LatAm growth (60% global GDP growth to 2025; FMCG +3–4% CAGR) supports volume upside.

| Metric | Value |

|---|---|

| Polypropylene YoY | +18% |

| Aluminum LME 2025 | +12% |

| Global CPI (2024) | ~4.5% |

| 5% USD move impact | EBITDA ±2–4% |

| Net debt/EBITDA | ~2.1x |

| Interest coverage | ~6x |

| Policy rates end‑2025 | ~4.5% |

| APAC/LatAm GDP share | ~60% growth to 2025 |

| FMCG volume (APAC) | +3–4% CAGR (23–25) |

What You See Is What You Get

Amcor PESTLE Analysis

The preview shown here is the exact Amcor PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying, delivered exactly as shown with no surprises. The content and structure visible in the preview are the same file you’ll download immediately after payment. Everything displayed is final, professionally structured, and ready for implementation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive advantage with our targeted PESTLE Analysis of Amcor—uncover how political shifts, economic trends, social expectations, technological advances, legal changes, and environmental pressures will shape its strategy and performance; buy the full report to access deep, actionable insights ready for investment theses, strategic planning, or boardroom use.

Political factors

Trade Protectionism and Tariffs

Global trade in late 2025 remains affected by protectionism: US-China tariff frictions and EU safeguard measures raised average applied tariffs on packaging inputs by ~1.2 percentage points in 2024–25, per WTO data, increasing Amcor's cross-border input costs and logistics premiums.

For Amcor, tariff volatility elevates landed cost of polymers and aluminum, risking margin erosion—management reported input-cost headwinds of ~USD 120–160m in FY2024–25 tied to trade measures.

Strategic responses—nearshoring, diversified sourcing, tariff engineering, and localized production—are essential to sustain price competitiveness and supply continuity across its 40+ markets.

Government Sustainability Mandates

Governments are tightening plastic rules to hit 2030 climate targets, with the EU’s Single-Use Plastics Directive and extended producer responsibility expanding to 2025–2030; over 60 countries had national plastic waste policies by 2024. These mandates pressure packaging firms like Amcor to shift faster to recyclable/compostable materials to avoid fines or market bans, risking share loss if delayed. Amcor must sustain robust government relations and compliance spend—Amcor reported US$2.1bn capex in FY2024—to navigate evolving design and sourcing laws.

Geopolitical Stability in Emerging Markets

Amcor operates extensively in emerging markets—around 35% of 2024 revenue came from Asia-Pacific and Latin America—where political instability or sudden leadership changes can trigger abrupt regulatory shifts affecting packaging standards and taxes.

Political unrest or civil conflict risks physical assets and disrupted distribution; in 2023 supply-chain incidents in Latin America increased logistics costs by an estimated 2–3% for packaging firms.

Continuous monitoring of geopolitical indicators is essential for risk mitigation and capital allocation, especially as Amcor pursues ~4–6% organic growth in high-growth but volatile regions.

Global Tax Harmonization Efforts

The OECD/G20 Pillar Two global minimum tax (15%) and rising tax reform in 20+ jurisdictions can raise Amcor’s effective tax rate, potentially increasing cash tax outflows versus pre-2021 levels; multinationals reported average ETR rises of 1–3 percentage points in early adopters. Changes in green-tax incentives—e.g., EU carbon border adjustments and national green credits—can offset costs if Amcor’s packaging plants qualify.

Supply Chain Resiliency Policies

National-security driven policies push governments to onshore essential packaging; US CHIPS and Inflation Reduction Act subsidies and EU strategic autonomy plans increased local procurement—Amcor must expand regional plants to win contracts worth billions (e.g., government healthcare packaging procurement growth ~5–7% CAGR 2023–25).

Balancing global scale with localized manufacturing raises capex and operating costs; meeting local-content rules is now often mandatory to secure large public-sector deals and protect market share.

- Onshoring trend: rising government procurement of domestic packaging

- Capex impact: higher regional investment to meet local-content rules

- Revenue risk: noncompliance can forfeit multi-year public contracts

- Strategy: hybrid global-local footprint to retain scale benefits

Amcor faces margin squeeze: tariffs, Pillar Two and 60+ plastics rules hit costs, capex

Political risks—tariff spikes (+1.2 pp avg. 2024–25), OECD Pillar Two (15%) raising ETR ~1–3 pp, and 60+ national plastics regulations—pressure Amcor’s margins, capex (US$2.1bn FY2024) and sourcing; nearshoring and local-content compliance are required to secure public contracts and mitigate unrest in 35% revenue markets.

| Metric | Value/Impact |

|---|---|

| Tariff change (2024–25) | +1.2 pp |

| Input-cost hit | US$120–160m |

| Capex FY2024 | US$2.1bn |

| Revenue in EMs | ~35% |

| OECD Pillar Two | 15%; ETR +1–3 pp |

| Countries with plastics policy (2024) | 60+ |

What is included in the product

Explores how macro-environmental factors uniquely affect Amcor across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and industry trends to identify risks and opportunities.

Condenses Amcor's PESTLE into a sharp, shareable summary—segmented by category and written in plain language—so teams can quickly assess external risks, market drivers, and strategic implications for faster decision-making and presentation-ready use.

Economic factors

Raw Material Price Volatility

As 2025 ends, polymer, aluminum and paper input costs for Amcor remain tied to oil and commodity swings—polypropylene rose ~18% YoY and aluminum LME prices were up ~12% in 2025—forcing Amcor to rely on hedging and pass-throughs; failure to offset spikes can compress margins (Amcor reported a 2025 H1 gross margin of ~18.5%), so agile procurement and contract pricing are critical.

Global Inflationary Pressures

Persistent inflation—global CPI averaging about 4.5% in 2024 with core inflation ~5% in key markets—erodes consumer purchasing power and raises Amcor’s input costs for resin, paper and freight, pressuring margins.

Rising labor (+3–6% wage inflation in 2023–24) and energy costs force Amcor toward automation and OEE improvements to protect adjusted EBIT margin (target ~12–14%).

Modeling the inflation-demand interplay is essential: NielsenIQ reported FMCG volume declines of ~1–2% YoY in 2024, informing Amcor’s volume forecasts and strategic price passes.

Currency Exchange Rate Fluctuations

As a US-dollar reported company operating across 40+ currencies, Amcor faces material FX risk: a 5% USD appreciation versus the euro, yuan or AUD could swing reported EBITDA by an estimated 2–4%, based on FY2024 revenue mix where ~35% was Europe/APAC.

Translation effects drove a ~US$30–50m annualized P&L impact in recent quarters; hedging and natural offsets limit volatility but not fully.

Financial teams must track ECB/People’s Bank of China/RBA moves and USD rate differentials—Fed tightening in 2022–24 widened FX swings and remains a primary driver.

Interest Rate Impacts on Capital

The prevailing interest rate environment at end-2025 raised global policy rates to about 4.5% on average, increasing Amcor’s average borrowing cost and pressuring free cash flow for expansions and acquisitions.

Higher rates make M&A pricier, prompting Amcor to favor internal R&D funding; its net debt/EBITDA of ~2.1x and interest coverage near 6x will be key metrics for investors monitoring monetary cycles.

- End-2025 policy rates ~4.5%

- Amcor net debt/EBITDA ~2.1x

- Interest coverage ~6x

- Higher rates favor internal funding over aggressive M&A

Emerging Market Growth Potential

Economic expansion in Asia-Pacific and Latin America—projected to account for over 60% of global GDP growth through 2025—boosts demand for packaging as rising middle classes increase spend on packaged food, beverages and personal care; e.g., Asia-Pacific FMCG volume growth ~3–4% CAGR (2023–25). Amcor’s market share gains hinge on scaling local manufacturing and supply chains to meet higher unit volumes while controlling capex and logistics costs.

- Asia-Pacific & Latin America driving ~60% of global GDP growth to 2025

- FMCG volume growth in region ~3–4% CAGR (2023–25)

- Amcor growth dependent on local scale, capex efficiency, supply-chain resilience

Input-cost surge, FX & rates squeeze margins while APAC/LatAm volume offsets risk

Input-cost volatility (polypropylene +18% YoY; aluminum LME +12% in 2025) and ~4.5% global CPI compress margins (2025 H1 gross ~18.5%); FX (5% USD move → ~2–4% EBITDA swing) and end‑2025 policy rates ~4.5% raise borrowing costs (net debt/EBITDA ~2.1x; interest coverage ~6x); APAC/LatAm growth (60% global GDP growth to 2025; FMCG +3–4% CAGR) supports volume upside.

| Metric | Value |

|---|---|

| Polypropylene YoY | +18% |

| Aluminum LME 2025 | +12% |

| Global CPI (2024) | ~4.5% |

| 5% USD move impact | EBITDA ±2–4% |

| Net debt/EBITDA | ~2.1x |

| Interest coverage | ~6x |

| Policy rates end‑2025 | ~4.5% |

| APAC/LatAm GDP share | ~60% growth to 2025 |

| FMCG volume (APAC) | +3–4% CAGR (23–25) |

What You See Is What You Get

Amcor PESTLE Analysis

The preview shown here is the exact Amcor PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying, delivered exactly as shown with no surprises. The content and structure visible in the preview are the same file you’ll download immediately after payment. Everything displayed is final, professionally structured, and ready for implementation.