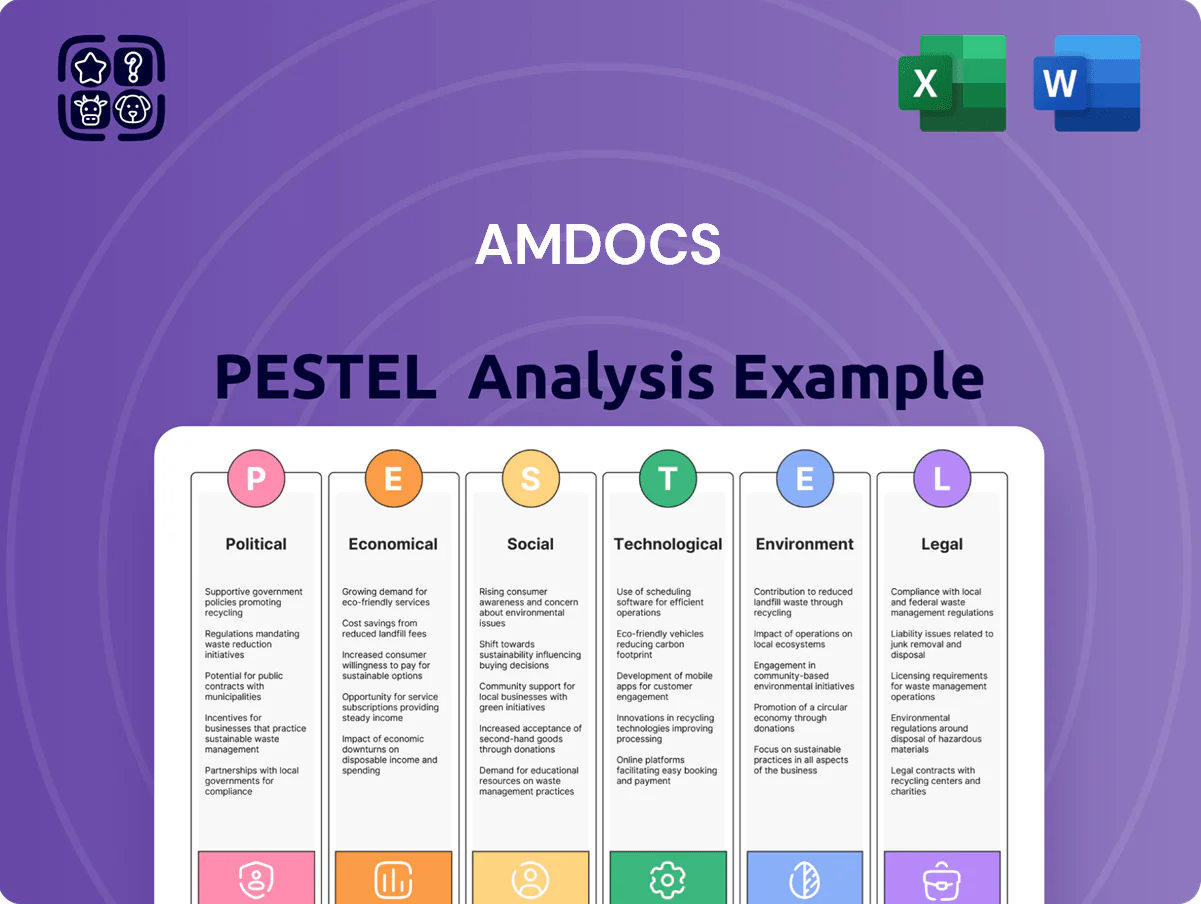

Amdocs PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain strategic clarity with our Amdocs PESTLE Analysis—concise, expert-led insights into political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory; perfect for investors and strategists. Purchase the full version to access the complete, editable report and actionable intelligence you can deploy immediately.

Political factors

Geopolitical instability in the Middle East

Amdocs operates major R&D and delivery centers in Israel, exposing it to Middle East geopolitical instability; in 2024 Israel accounted for an estimated 25–30% of Amdocs global headcount (~11,000–13,000 employees of ~43,000 total), heightening operational risk.

Recent regional conflicts have triggered personnel mobilization and localized disruptions, risking delays in 2024–25 project delivery and potential short-term revenue impacts given Q3 2024 services reliance on Israeli teams.

Management must continuously update business continuity and relocation plans—including backup capacity in Eastern Europe and India—to mitigate supply chain and workforce risks and preserve SLA commitments.

Global trade policies and protectionism

As a global provider, Amdocs is sensitive to trade agreements and rising protectionism in North America and Europe; 2024 WTO data shows global tariff measures increased 6% YoY, which can raise delivery costs for software exporters like Amdocs.

New tariffs or tighter cross-border data flow rules—e.g., EU’s 2023 Data Act and 2024 US CLOUD Act tensions—can complicate cloud deployments and add compliance costs estimated at millions annually for large vendors.

Shifts in West–emerging market relations, especially in India and Latin America where Amdocs reported ~30% of 2024 revenues from international services, require strategic pricing and localization to preserve margins.

Governmental focus on national security and 5G

Governments’ national security scrutiny of 5G is rising: over 40 countries implemented stricter vendor vetting by 2024, affecting telco contracts; Amdocs gains from state-led modernization—its 2024 revenue of $4.5bn benefits from digital infrastructure projects—but must pass rigorous clearances and compliance audits, and political shifts can swing multi-year transformation deals (often $50m–$500m) to accelerate or stall procurement timelines.

Taxation policy changes

Amdocs faces exposure to international tax reforms such as the OECD Pillar Two global minimum tax (15%), which could raise effective tax rates in low-tax jurisdictions where it earned part of its $4.0bn 2024 revenue, compressing net income and cash flow if regional tax incentives are eliminated.

Shifts in corporate tax rates in key hubs (Israel, US, UK) or removal of incentive regimes require active tax planning and could increase statutory tax expense above the company’s 2024 reported effective tax rate of ~15–18%.

- OECD Pillar Two: 15% minimum tax

- 2024 revenue: ~$4.0bn

- 2024 effective tax rate: ~15–18%

- Watch Israel, US, UK policy changes and tax-haven legislation

Public sector digital transformation initiatives

Many governments allocated over $600 billion to digital transformation in 2024–25, boosting demand for Amdocs’ consulting and systems-integration services in e-government and broadband projects.

Political mandates to close the digital divide—US IIJA, EU Digital Decade, India’s BharatNet upgrades—drive telecom modernization where Amdocs’ OSS/BSS expertise is core.

Aligning with government-funded infrastructure programs secures multi-year contracts often worth tens to hundreds of millions, supporting predictable revenue and backlog growth.

- 2024–25 public digital spend > $600B

- Major programs: IIJA, EU Digital Decade, BharatNet

- Typical government telecom contracts: $10M–$500M

- Supports long-term revenue/backlog expansion

Concentrated Israel Exposure, Trade & Tax Risks vs. $600B+ Politically Driven Digital Opportunity

Political risks include Israel-centric workforce exposure (2024: ~25–30% of ~43,000 headcount), regional conflict-driven delivery delays, trade protectionism raising export costs (WTO: +6% tariff measures YoY 2024), OECD Pillar Two 15% minimum tax pressure, and strong public digital spend (> $600B in 2024–25) that creates large but politically contingent contracts.

| Metric | 2024/2025 |

|---|---|

| Headcount Israel | 25–30% (~11–13k) |

| Global rev | ~$4.0–4.5B |

| Public digital spend | >$600B |

| OECD Pillar Two | 15% min |

What is included in the product

Explores how external macro-environmental factors uniquely affect Amdocs across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condensed Amdocs PESTLE summary for quick use in meetings or presentations, clearly segmented by factor to speed strategic discussions and decision-making.

Economic factors

Interest rate environment and capital costs

Fluctuations in global interest rates affect Amdocs’ borrowing costs and clients’ capex; US Fed hikes in 2022–23 pushed global corporate borrowing spreads up, with average BBB yields rising ~200 bps, squeezing telecom capex. High rates prompted some carriers to delay multi-year digital transformation projects or seek contract renegotiations, reducing near-term OSS/BSS spend by an estimated low-single-digit percentage. Conversely, 2024–25 rate stabilization and easing in select markets supported renewed investment in next‑gen OSS/BSS platforms, with telecom IT budgets projected to grow ~3–5% annually through 2026.

Currency exchange rate volatility

With roughly 60% of revenue denominated in USD while significant costs are in ILS and INR, Amdocs faces marked FX risk; a 10% move in USD/ILS or USD/INR could swing operating profit by tens of millions—Amdocs reported FX losses of $24m in FY2024. Currency swings also affect the cost competitiveness of delivery centers in India and Israel, where wage inflation is local-currency linked. The company uses forward contracts and options to hedge exposures, yet extreme volatility, like the 2022–24 emerging-market currency stress, remains a material headwind to reported earnings.

Inflationary pressures on operational costs

Global inflation has driven wage growth for high-skilled software engineers and IT consultants, with tech salaries rising about 6-9% in 2023-2024 across major delivery hubs, increasing Amdocs' labor cost base. Rising wages in India, Eastern Europe and North America risk squeezing margins if Amdocs cannot secure price adjustments; industry bill rates rose roughly 4-7% in 2024. Balancing talent retention programs against operational overhead control remains a key economic challenge in this inflationary context.

Corporate spending trends in the telecom sector

The economic health of the communications, media, and entertainment sectors drives demand for Amdocs; global telecom capex fell about 2% in 2024 while digital services spend grew ~4%, shifting client priorities.

In downturns clients favor cost-optimization—Amdocs saw ~60% of 2024 deals tied to OSS/BSS and efficiency projects versus 40% for digital CX platforms.

Amdocs must balance efficiency tools and growth platforms to serve cycles, targeting a product mix that can capture both cost-saving and revenue-generating initiatives.

- 2024 telecom capex -2%

- Digital services spend +4% (2024)

- 60% deals efficiency-focused (2024)

- 40% deals growth-focused (2024)

Global supply chain stability

While primarily a software provider, Amdocs depends on hardware and cloud infrastructure; global semiconductor shortages raised server prices ~15% in 2021–22 and cloud CAPEX growth hit 20% YoY in 2023, risking delayed implementations and higher cloud delivery costs.

Economic disruption in semiconductor or server markets can push project timelines and inflate OPEX, threatening Amdocs’ ability to meet SLA-backed penalties and margins; resilient supplier diversification and cloud capacity contracts mitigate risk.

- Hardware/cloud cost volatility: server prices +15% (2021–22)

- Cloud CAPEX growth: ~20% YoY (2023)

- Supply resilience needed to protect SLAs and margins

Amdocs braces for rate-driven capex cuts, FX hits and wage/cloud cost pressure

Macroeconomic shifts impact Amdocs via interest-rate-driven capex cuts (telecom capex -2% in 2024), FX exposure (USD revenue ~60%; FY2024 FX loss $24m), wage inflation (tech salaries +6–9% 2023–24) and hardware/cloud cost volatility (server prices +15% 2021–22; cloud CAPEX +20% YoY 2023), forcing a mix of efficiency (60% deals 2024) and growth offerings.

| Metric | Value |

|---|---|

| Telecom capex (2024) | -2% |

| Digital services spend (2024) | +4% |

| USD revenue share | ~60% |

| FY2024 FX loss | $24m |

| Tech wage growth (2023–24) | +6–9% |

| Server price shock (2021–22) | +15% |

| Cloud CAPEX growth (2023) | +20% YoY |

| Deals efficiency-focused (2024) | 60% |

Preview the Actual Deliverable

Amdocs PESTLE Analysis

The preview shown here is the exact Amdocs PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain strategic clarity with our Amdocs PESTLE Analysis—concise, expert-led insights into political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory; perfect for investors and strategists. Purchase the full version to access the complete, editable report and actionable intelligence you can deploy immediately.

Political factors

Geopolitical instability in the Middle East

Amdocs operates major R&D and delivery centers in Israel, exposing it to Middle East geopolitical instability; in 2024 Israel accounted for an estimated 25–30% of Amdocs global headcount (~11,000–13,000 employees of ~43,000 total), heightening operational risk.

Recent regional conflicts have triggered personnel mobilization and localized disruptions, risking delays in 2024–25 project delivery and potential short-term revenue impacts given Q3 2024 services reliance on Israeli teams.

Management must continuously update business continuity and relocation plans—including backup capacity in Eastern Europe and India—to mitigate supply chain and workforce risks and preserve SLA commitments.

Global trade policies and protectionism

As a global provider, Amdocs is sensitive to trade agreements and rising protectionism in North America and Europe; 2024 WTO data shows global tariff measures increased 6% YoY, which can raise delivery costs for software exporters like Amdocs.

New tariffs or tighter cross-border data flow rules—e.g., EU’s 2023 Data Act and 2024 US CLOUD Act tensions—can complicate cloud deployments and add compliance costs estimated at millions annually for large vendors.

Shifts in West–emerging market relations, especially in India and Latin America where Amdocs reported ~30% of 2024 revenues from international services, require strategic pricing and localization to preserve margins.

Governmental focus on national security and 5G

Governments’ national security scrutiny of 5G is rising: over 40 countries implemented stricter vendor vetting by 2024, affecting telco contracts; Amdocs gains from state-led modernization—its 2024 revenue of $4.5bn benefits from digital infrastructure projects—but must pass rigorous clearances and compliance audits, and political shifts can swing multi-year transformation deals (often $50m–$500m) to accelerate or stall procurement timelines.

Taxation policy changes

Amdocs faces exposure to international tax reforms such as the OECD Pillar Two global minimum tax (15%), which could raise effective tax rates in low-tax jurisdictions where it earned part of its $4.0bn 2024 revenue, compressing net income and cash flow if regional tax incentives are eliminated.

Shifts in corporate tax rates in key hubs (Israel, US, UK) or removal of incentive regimes require active tax planning and could increase statutory tax expense above the company’s 2024 reported effective tax rate of ~15–18%.

- OECD Pillar Two: 15% minimum tax

- 2024 revenue: ~$4.0bn

- 2024 effective tax rate: ~15–18%

- Watch Israel, US, UK policy changes and tax-haven legislation

Public sector digital transformation initiatives

Many governments allocated over $600 billion to digital transformation in 2024–25, boosting demand for Amdocs’ consulting and systems-integration services in e-government and broadband projects.

Political mandates to close the digital divide—US IIJA, EU Digital Decade, India’s BharatNet upgrades—drive telecom modernization where Amdocs’ OSS/BSS expertise is core.

Aligning with government-funded infrastructure programs secures multi-year contracts often worth tens to hundreds of millions, supporting predictable revenue and backlog growth.

- 2024–25 public digital spend > $600B

- Major programs: IIJA, EU Digital Decade, BharatNet

- Typical government telecom contracts: $10M–$500M

- Supports long-term revenue/backlog expansion

Concentrated Israel Exposure, Trade & Tax Risks vs. $600B+ Politically Driven Digital Opportunity

Political risks include Israel-centric workforce exposure (2024: ~25–30% of ~43,000 headcount), regional conflict-driven delivery delays, trade protectionism raising export costs (WTO: +6% tariff measures YoY 2024), OECD Pillar Two 15% minimum tax pressure, and strong public digital spend (> $600B in 2024–25) that creates large but politically contingent contracts.

| Metric | 2024/2025 |

|---|---|

| Headcount Israel | 25–30% (~11–13k) |

| Global rev | ~$4.0–4.5B |

| Public digital spend | >$600B |

| OECD Pillar Two | 15% min |

What is included in the product

Explores how external macro-environmental factors uniquely affect Amdocs across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condensed Amdocs PESTLE summary for quick use in meetings or presentations, clearly segmented by factor to speed strategic discussions and decision-making.

Economic factors

Interest rate environment and capital costs

Fluctuations in global interest rates affect Amdocs’ borrowing costs and clients’ capex; US Fed hikes in 2022–23 pushed global corporate borrowing spreads up, with average BBB yields rising ~200 bps, squeezing telecom capex. High rates prompted some carriers to delay multi-year digital transformation projects or seek contract renegotiations, reducing near-term OSS/BSS spend by an estimated low-single-digit percentage. Conversely, 2024–25 rate stabilization and easing in select markets supported renewed investment in next‑gen OSS/BSS platforms, with telecom IT budgets projected to grow ~3–5% annually through 2026.

Currency exchange rate volatility

With roughly 60% of revenue denominated in USD while significant costs are in ILS and INR, Amdocs faces marked FX risk; a 10% move in USD/ILS or USD/INR could swing operating profit by tens of millions—Amdocs reported FX losses of $24m in FY2024. Currency swings also affect the cost competitiveness of delivery centers in India and Israel, where wage inflation is local-currency linked. The company uses forward contracts and options to hedge exposures, yet extreme volatility, like the 2022–24 emerging-market currency stress, remains a material headwind to reported earnings.

Inflationary pressures on operational costs

Global inflation has driven wage growth for high-skilled software engineers and IT consultants, with tech salaries rising about 6-9% in 2023-2024 across major delivery hubs, increasing Amdocs' labor cost base. Rising wages in India, Eastern Europe and North America risk squeezing margins if Amdocs cannot secure price adjustments; industry bill rates rose roughly 4-7% in 2024. Balancing talent retention programs against operational overhead control remains a key economic challenge in this inflationary context.

Corporate spending trends in the telecom sector

The economic health of the communications, media, and entertainment sectors drives demand for Amdocs; global telecom capex fell about 2% in 2024 while digital services spend grew ~4%, shifting client priorities.

In downturns clients favor cost-optimization—Amdocs saw ~60% of 2024 deals tied to OSS/BSS and efficiency projects versus 40% for digital CX platforms.

Amdocs must balance efficiency tools and growth platforms to serve cycles, targeting a product mix that can capture both cost-saving and revenue-generating initiatives.

- 2024 telecom capex -2%

- Digital services spend +4% (2024)

- 60% deals efficiency-focused (2024)

- 40% deals growth-focused (2024)

Global supply chain stability

While primarily a software provider, Amdocs depends on hardware and cloud infrastructure; global semiconductor shortages raised server prices ~15% in 2021–22 and cloud CAPEX growth hit 20% YoY in 2023, risking delayed implementations and higher cloud delivery costs.

Economic disruption in semiconductor or server markets can push project timelines and inflate OPEX, threatening Amdocs’ ability to meet SLA-backed penalties and margins; resilient supplier diversification and cloud capacity contracts mitigate risk.

- Hardware/cloud cost volatility: server prices +15% (2021–22)

- Cloud CAPEX growth: ~20% YoY (2023)

- Supply resilience needed to protect SLAs and margins

Amdocs braces for rate-driven capex cuts, FX hits and wage/cloud cost pressure

Macroeconomic shifts impact Amdocs via interest-rate-driven capex cuts (telecom capex -2% in 2024), FX exposure (USD revenue ~60%; FY2024 FX loss $24m), wage inflation (tech salaries +6–9% 2023–24) and hardware/cloud cost volatility (server prices +15% 2021–22; cloud CAPEX +20% YoY 2023), forcing a mix of efficiency (60% deals 2024) and growth offerings.

| Metric | Value |

|---|---|

| Telecom capex (2024) | -2% |

| Digital services spend (2024) | +4% |

| USD revenue share | ~60% |

| FY2024 FX loss | $24m |

| Tech wage growth (2023–24) | +6–9% |

| Server price shock (2021–22) | +15% |

| Cloud CAPEX growth (2023) | +20% YoY |

| Deals efficiency-focused (2024) | 60% |

Preview the Actual Deliverable

Amdocs PESTLE Analysis

The preview shown here is the exact Amdocs PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.