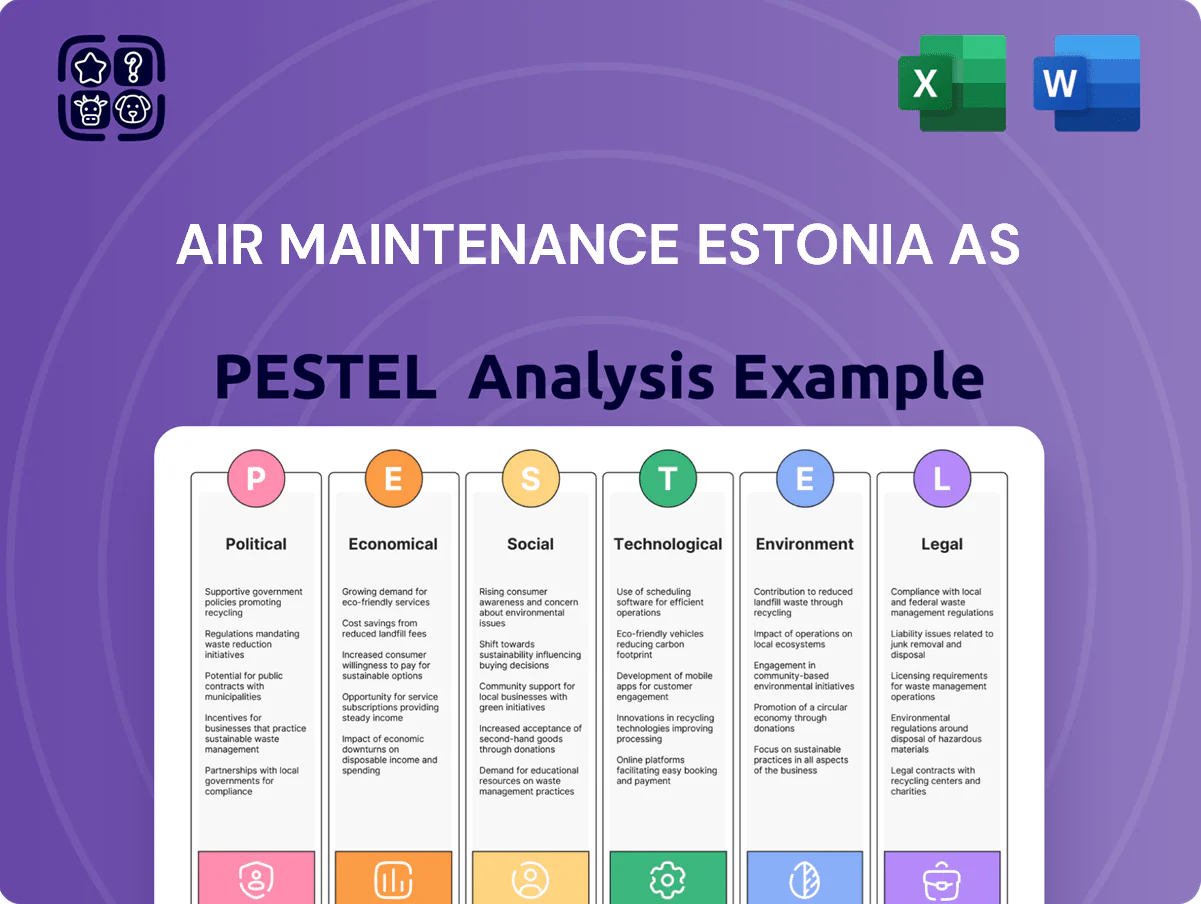

Air Maintenance Estonia AS PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces are shaping Air Maintenance Estonia AS and learn where strategic risks and growth opportunities lie; purchase the full PESTLE Analysis to access expert, ready-to-use insights and downloadable files that accelerate decision-making and competitive planning.

Political factors

EU Membership and Regulatory Alignment

Estonia's EU membership obliges Air Maintenance Estonia to follow harmonized EASA standards, reducing regulatory friction; in 2024 over 95% of EU-based MROs reported full EASA compliance, aiding cross-border parts movement.

The harmonization supports seamless transfer of aircraft/components across the EU single market, where intra-EU aviation trade valued €400+ billion in 2023.

Political backing for the Single European Sky aims to cut delays and fuel burn up to 10% regionally, improving turnaround efficiency for regional maintenance ops.

Geopolitical Security and Regional Stability

As a NATO eastern-front member, Estonia's political stability underpins international airline trust; in 2024 Estonia hosted NATO air policing and saw defense spending at 2.5% of GDP (EUR 2.5bn in 2024), signaling commitment to security.

Rising regional tensions—Russian military activity near borders increased 12% in 2023–24 according to NATO reporting—require AME to adopt enhanced security, insurance and contingency planning to guarantee uninterrupted MRO services.

AME must demonstrate rigorous asset protection, leveraging Tallinn’s secured facilities and compliance with EU Aviation Safety Agency and NATO-aligned protocols to reassure carriers and protect high-value aircraft during maintenance.

Government Support for Aviation Infrastructure

The Estonian government’s Transport Development Plan targets a 20% increase in air passenger and cargo throughput by 2030, directly boosting demand for MRO services and expanding Air Maintenance Estonia AS’s growth runway.

Planned investments of €200–300m in Tallinn Airport modernization and logistics links improve apron capacity and freight handling, enabling AME to scale operations and reduce turnaround times.

State-backed funding and a 15% enrollment rise (2023–2025) in technical aviation programmes help secure a steady pipeline of certified technicians for the aerospace sector.

International Trade Policy and Sanctions

Strict adherence to EU and UN sanctions is mandatory for EASA-certified Air Maintenance Estonia AS, requiring AML-style screening and export controls after the EU reported a 22% rise in aviation-related sanctions investigations in 2024.

AME must maintain rigorous compliance frameworks and documented due diligence to ensure no services or parts are supplied to restricted entities, avoiding fines that in EU cases have reached up to €50 million.

Shifts in trade relations—e.g., EU–US tariffs or supply frictions with Russia/China—can disrupt sourcing of avionics and composite components, where single-source risks account for an estimated 18% of OEM part supply chains in 2025.

- Mandatory sanctions screening; rising EU investigations (+22% in 2024)

- Compliance reduces risk of fines (up to €50M in precedent)

- Supply-chain exposure: 18% single-source risk for critical parts

Labor Migration and Work Visa Policies

Political decisions on non-EU skilled labor affect AME’s ability to fill specialized technician gaps; Estonia issued 7,200 work permits in 2024, with 14% in manufacturing and technical roles, indicating potential avenues for recruitment.

Streamlined aviation engineer permits—Estonia cut processing times to ~30 days in 2025 pilot reforms—help AME tap global talent to meet peak-season demand and protect €12–18m annual maintenance revenue.

Restrictive immigration stances risk capacity shortfalls during high-demand months, potentially raising overtime and subcontracting costs by 8–15%.

- 2024: 7,200 work permits in Estonia; 14% technical

- 2025 reform: ~30-day permit processing

- Revenue at risk: €12–18m; cost increases 8–15%

Estonia’s defense boost and transport growth fuel AME demand amid rising security and compliance risks

Estonia’s EASA/NATO alignment, rising defense spend (2.5% GDP, €2.5bn 2024) and Transport Plan (20% throughput ↑ by 2030) bolster demand and trust for AME, while increased regional tensions (+12% military activity 2023–24) and a 22% rise in EU aviation sanctions probes (2024) raise security, compliance and supply‑chain risks; 2024 work permits 7,200 (14% technical), 2025 permit reform ~30 days aid staffing.

| Metric | Value |

|---|---|

| Defense spend 2024 | 2.5% GDP (€2.5bn) |

| Throughput target | +20% by 2030 |

| Sanctions probes 2024 | +22% |

| Work permits 2024 | 7,200 (14% technical) |

| Border tensions 2023–24 | +12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Air Maintenance Estonia AS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, backed by current regional industry data and trends to identify threats and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of Air Maintenance Estonia AS that highlights regulatory, economic, social, technological, legal, and environmental factors to speed decision-making in meetings and strategy sessions.

Economic factors

Labor Cost Dynamics in the Baltic Region

Estonia offers skilled aviation technicians at roughly 30-40% lower labor costs than Western Europe, enabling Air Maintenance Estonia AS to deliver EASA-compliant heavy maintenance at competitive rates and win contracts from major carriers.

Average nominal wages in Estonia rose about 8.5% year-on-year in 2024, pressuring margins and forcing AME to balance price competitiveness with higher retention pay and training investments to keep certified engineers.

Global Recovery of Narrow-Body Aircraft Demand

The sustained short-to-medium haul travel recovery has driven 2024 utilization of Boeing 737 and Airbus A320 families to ~85–90%, boosting demand in AME’s core specialties.

Airline fleet plans through 2025 project ~3,000 narrow-body deliveries globally, increasing base and line maintenance cycles and spare-part needs.

This creates a robust pipeline of multi-year service contracts, supporting predictable revenue and margin stability for Air Maintenance Estonia AS.

Supply Chain Inflation and Component Costs

Rising raw material and specialized component costs—aluminum up ~18% and avionics modules up ~22% in 2024—compress AME’s margins as maintenance labor rates cannot fully offset parts inflation.

Global supply-chain delays (average lead times for engine/avionics parts up 35% vs 2019) increase hangar turnaround, raising AOG exposure and potential penalty costs for operators.

AME must deploy sophisticated inventory management (safety stock, MRO consignment) and strategic sourcing (dual suppliers, long-term contracts) to buffer price volatility and preserve service reliability.

Currency Fluctuation and Exchange Rate Risk

Operating in the Eurozone gives AME invoice stability, but about 60–70% of global aircraft parts trade is USD-priced, so a 10% EUR-USD move can raise imported component costs by roughly the same amount, squeezing margins.

EUR weakening vs USD in 2023–2025 (EUR down ~8% vs USD from Jan 2023–Dec 2024) increased procurement costs and reduced competitiveness on non-EU bids priced in USD.

AME should use forward contracts, FX options and natural hedges; effective hedging could cut earnings volatility by an estimated 30–50% based on industry studies.

- High USD pricing exposure (~60–70% of parts)

- EUR fell ~8% vs USD 2023–2024, raising import costs

- 10% FX move ≈ 10% component cost impact

- Hedging (forwards/options) can reduce earnings volatility 30–50%

Interest Rates and Capital Expenditure

The ECB's deposit rate at 4.00% (Feb 2026) raises borrowing costs, increasing financing expenses for AME's hangar expansions and tooling purchases and potentially delaying CAPEX decisions.

Higher yields push AME toward conservative investment timing; in 2024–25 European corporate loan rates averaged ~4.5–5.5%, tightening access to affordable credit for modernization.

- ECB rate 4.00% (Feb 2026)

- EU corporate loan range 4.5–5.5% (2024–25)

- Higher rates increase CAPEX payback periods

Estonia: Lower labor costs, rising wages & supply pressures reshape narrow‑body supply chain

Estonia’s 30–40% lower labor costs vs Western Europe, 8.5% wage rise in 2024, 85–90% narrow‑body utilization, ~3,000 global narrow‑body deliveries through 2025, aluminum +18% and avionics +22% (2024), engine/avionics lead times +35% vs 2019, 60–70% parts USD‑priced, EUR −8% vs USD (2023–24), ECB rate 4.00% (Feb 2026).

| Metric | Value |

|---|---|

| Labor cost gap | −30–40% |

| Wage growth 2024 | +8.5% |

| Narrow‑body utilization 2024 | 85–90% |

| Narrow‑body deliveries to 2025 | ~3,000 |

| Aluminum / Avionics price change 2024 | +18% / +22% |

| Parts lead time vs 2019 | +35% |

| Parts USD exposure | 60–70% |

| EUR vs USD (2023–24) | −8% |

| ECB rate Feb 2026 | 4.00% |

Same Document Delivered

Air Maintenance Estonia AS PESTLE Analysis

The preview shown here is the exact PESTLE Analysis for Air Maintenance Estonia AS you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers—this is the real, finished file you’ll download immediately after payment, with the same content, layout, and structure visible here.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces are shaping Air Maintenance Estonia AS and learn where strategic risks and growth opportunities lie; purchase the full PESTLE Analysis to access expert, ready-to-use insights and downloadable files that accelerate decision-making and competitive planning.

Political factors

EU Membership and Regulatory Alignment

Estonia's EU membership obliges Air Maintenance Estonia to follow harmonized EASA standards, reducing regulatory friction; in 2024 over 95% of EU-based MROs reported full EASA compliance, aiding cross-border parts movement.

The harmonization supports seamless transfer of aircraft/components across the EU single market, where intra-EU aviation trade valued €400+ billion in 2023.

Political backing for the Single European Sky aims to cut delays and fuel burn up to 10% regionally, improving turnaround efficiency for regional maintenance ops.

Geopolitical Security and Regional Stability

As a NATO eastern-front member, Estonia's political stability underpins international airline trust; in 2024 Estonia hosted NATO air policing and saw defense spending at 2.5% of GDP (EUR 2.5bn in 2024), signaling commitment to security.

Rising regional tensions—Russian military activity near borders increased 12% in 2023–24 according to NATO reporting—require AME to adopt enhanced security, insurance and contingency planning to guarantee uninterrupted MRO services.

AME must demonstrate rigorous asset protection, leveraging Tallinn’s secured facilities and compliance with EU Aviation Safety Agency and NATO-aligned protocols to reassure carriers and protect high-value aircraft during maintenance.

Government Support for Aviation Infrastructure

The Estonian government’s Transport Development Plan targets a 20% increase in air passenger and cargo throughput by 2030, directly boosting demand for MRO services and expanding Air Maintenance Estonia AS’s growth runway.

Planned investments of €200–300m in Tallinn Airport modernization and logistics links improve apron capacity and freight handling, enabling AME to scale operations and reduce turnaround times.

State-backed funding and a 15% enrollment rise (2023–2025) in technical aviation programmes help secure a steady pipeline of certified technicians for the aerospace sector.

International Trade Policy and Sanctions

Strict adherence to EU and UN sanctions is mandatory for EASA-certified Air Maintenance Estonia AS, requiring AML-style screening and export controls after the EU reported a 22% rise in aviation-related sanctions investigations in 2024.

AME must maintain rigorous compliance frameworks and documented due diligence to ensure no services or parts are supplied to restricted entities, avoiding fines that in EU cases have reached up to €50 million.

Shifts in trade relations—e.g., EU–US tariffs or supply frictions with Russia/China—can disrupt sourcing of avionics and composite components, where single-source risks account for an estimated 18% of OEM part supply chains in 2025.

- Mandatory sanctions screening; rising EU investigations (+22% in 2024)

- Compliance reduces risk of fines (up to €50M in precedent)

- Supply-chain exposure: 18% single-source risk for critical parts

Labor Migration and Work Visa Policies

Political decisions on non-EU skilled labor affect AME’s ability to fill specialized technician gaps; Estonia issued 7,200 work permits in 2024, with 14% in manufacturing and technical roles, indicating potential avenues for recruitment.

Streamlined aviation engineer permits—Estonia cut processing times to ~30 days in 2025 pilot reforms—help AME tap global talent to meet peak-season demand and protect €12–18m annual maintenance revenue.

Restrictive immigration stances risk capacity shortfalls during high-demand months, potentially raising overtime and subcontracting costs by 8–15%.

- 2024: 7,200 work permits in Estonia; 14% technical

- 2025 reform: ~30-day permit processing

- Revenue at risk: €12–18m; cost increases 8–15%

Estonia’s defense boost and transport growth fuel AME demand amid rising security and compliance risks

Estonia’s EASA/NATO alignment, rising defense spend (2.5% GDP, €2.5bn 2024) and Transport Plan (20% throughput ↑ by 2030) bolster demand and trust for AME, while increased regional tensions (+12% military activity 2023–24) and a 22% rise in EU aviation sanctions probes (2024) raise security, compliance and supply‑chain risks; 2024 work permits 7,200 (14% technical), 2025 permit reform ~30 days aid staffing.

| Metric | Value |

|---|---|

| Defense spend 2024 | 2.5% GDP (€2.5bn) |

| Throughput target | +20% by 2030 |

| Sanctions probes 2024 | +22% |

| Work permits 2024 | 7,200 (14% technical) |

| Border tensions 2023–24 | +12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Air Maintenance Estonia AS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, backed by current regional industry data and trends to identify threats and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of Air Maintenance Estonia AS that highlights regulatory, economic, social, technological, legal, and environmental factors to speed decision-making in meetings and strategy sessions.

Economic factors

Labor Cost Dynamics in the Baltic Region

Estonia offers skilled aviation technicians at roughly 30-40% lower labor costs than Western Europe, enabling Air Maintenance Estonia AS to deliver EASA-compliant heavy maintenance at competitive rates and win contracts from major carriers.

Average nominal wages in Estonia rose about 8.5% year-on-year in 2024, pressuring margins and forcing AME to balance price competitiveness with higher retention pay and training investments to keep certified engineers.

Global Recovery of Narrow-Body Aircraft Demand

The sustained short-to-medium haul travel recovery has driven 2024 utilization of Boeing 737 and Airbus A320 families to ~85–90%, boosting demand in AME’s core specialties.

Airline fleet plans through 2025 project ~3,000 narrow-body deliveries globally, increasing base and line maintenance cycles and spare-part needs.

This creates a robust pipeline of multi-year service contracts, supporting predictable revenue and margin stability for Air Maintenance Estonia AS.

Supply Chain Inflation and Component Costs

Rising raw material and specialized component costs—aluminum up ~18% and avionics modules up ~22% in 2024—compress AME’s margins as maintenance labor rates cannot fully offset parts inflation.

Global supply-chain delays (average lead times for engine/avionics parts up 35% vs 2019) increase hangar turnaround, raising AOG exposure and potential penalty costs for operators.

AME must deploy sophisticated inventory management (safety stock, MRO consignment) and strategic sourcing (dual suppliers, long-term contracts) to buffer price volatility and preserve service reliability.

Currency Fluctuation and Exchange Rate Risk

Operating in the Eurozone gives AME invoice stability, but about 60–70% of global aircraft parts trade is USD-priced, so a 10% EUR-USD move can raise imported component costs by roughly the same amount, squeezing margins.

EUR weakening vs USD in 2023–2025 (EUR down ~8% vs USD from Jan 2023–Dec 2024) increased procurement costs and reduced competitiveness on non-EU bids priced in USD.

AME should use forward contracts, FX options and natural hedges; effective hedging could cut earnings volatility by an estimated 30–50% based on industry studies.

- High USD pricing exposure (~60–70% of parts)

- EUR fell ~8% vs USD 2023–2024, raising import costs

- 10% FX move ≈ 10% component cost impact

- Hedging (forwards/options) can reduce earnings volatility 30–50%

Interest Rates and Capital Expenditure

The ECB's deposit rate at 4.00% (Feb 2026) raises borrowing costs, increasing financing expenses for AME's hangar expansions and tooling purchases and potentially delaying CAPEX decisions.

Higher yields push AME toward conservative investment timing; in 2024–25 European corporate loan rates averaged ~4.5–5.5%, tightening access to affordable credit for modernization.

- ECB rate 4.00% (Feb 2026)

- EU corporate loan range 4.5–5.5% (2024–25)

- Higher rates increase CAPEX payback periods

Estonia: Lower labor costs, rising wages & supply pressures reshape narrow‑body supply chain

Estonia’s 30–40% lower labor costs vs Western Europe, 8.5% wage rise in 2024, 85–90% narrow‑body utilization, ~3,000 global narrow‑body deliveries through 2025, aluminum +18% and avionics +22% (2024), engine/avionics lead times +35% vs 2019, 60–70% parts USD‑priced, EUR −8% vs USD (2023–24), ECB rate 4.00% (Feb 2026).

| Metric | Value |

|---|---|

| Labor cost gap | −30–40% |

| Wage growth 2024 | +8.5% |

| Narrow‑body utilization 2024 | 85–90% |

| Narrow‑body deliveries to 2025 | ~3,000 |

| Aluminum / Avionics price change 2024 | +18% / +22% |

| Parts lead time vs 2019 | +35% |

| Parts USD exposure | 60–70% |

| EUR vs USD (2023–24) | −8% |

| ECB rate Feb 2026 | 4.00% |

Same Document Delivered

Air Maintenance Estonia AS PESTLE Analysis

The preview shown here is the exact PESTLE Analysis for Air Maintenance Estonia AS you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers—this is the real, finished file you’ll download immediately after payment, with the same content, layout, and structure visible here.