Ameriprise Financial Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

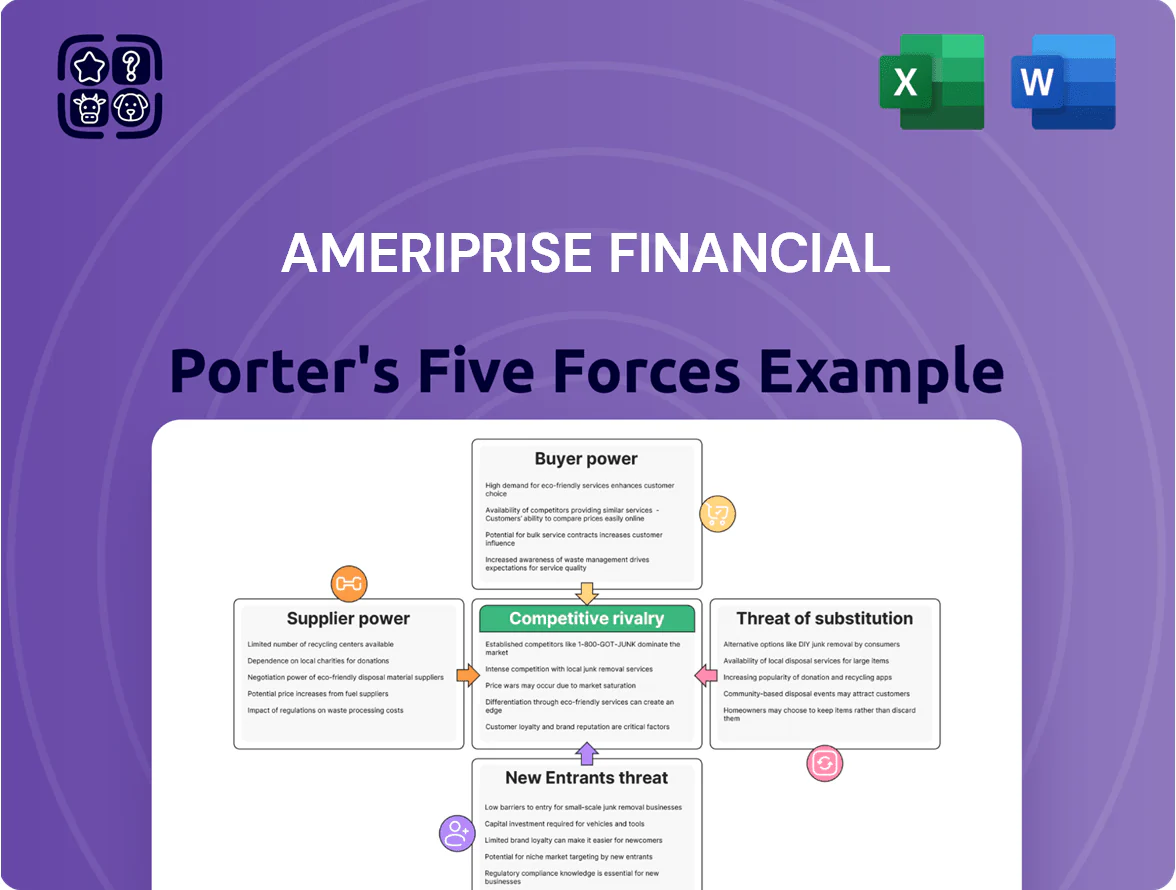

Ameriprise Financial faces intense rivalry from national brokers and fintech disruptors, moderate buyer power from fee-sensitive clients, and regulatory and technology-driven supplier dynamics shaping margins; barriers to entry are meaningful but evolving with digital platforms. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ameriprise Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Technological Infrastructure Providers

Ameriprise depends on specialized software and cloud providers for wealth-management platforms and client portals, creating high switching costs—enterprise cloud contracts often span 3–5 years and can exceed $50M annually for firms of similar scale. As digital transformation drives competitive edge, these suppliers gain leverage, especially for advanced cybersecurity and analytics where spending rose 18% industry-wide in 2024. Ameriprise must weigh vendor lock-in against urgent needs for real-time analytics and SOC‑grade security.

Human Capital and Financial Advisors

The primary suppliers for Ameriprise are its 10,000+ independent and employee financial advisors who drive client relationships and revenue; as of 2025 advisors managed about $1.2 trillion AUM for the firm. High industry demand for experienced advisors gives them leverage over commission splits, platform fees, and tech/support expectations, raising retention costs. Losing 1% of top-tier advisors could cut AUM by roughly $12 billion and reduce fee revenue proportionally, hurting growth and margins.

Regulatory and Compliance Bodies

Regulatory agencies like the SEC and FINRA act as non-market suppliers of Ameriprise Financials (Ameriprise Financial, Inc.) legal framework, forcing compliance that cannot be negotiated; in 2024 Ameriprise reported $7.4 billion operating revenues, making regulatory costs a material margin pressure. Changes such as tightened fiduciary duty proposals or higher capital/stress-test requirements raise mandatory costs—SEC rule changes in 2023–2025 led many advisors to incur one-time compliance upgrades averaging $0.5–$2 million per firm. Compliance demands continuous spend: Ameriprise’s 2024 regulatory and compliance headcount rose 8% year-over-year and legal/administrative expenses increased roughly 6% to support new reporting, training, and capital monitoring. This non-voluntary cost base limits Ameriprise’s bargaining power versus suppliers of legal rules and elevates fixed operating leverage risk.

Third-Party Asset Managers

Ameriprise runs its own asset management but distributes many third-party funds to offer client choice; in 2024 roughly 30% of advisory platform AUM came from non-affiliated managers, giving those firms leverage over placement and fees.

Big fund families—Vanguard, BlackRock, Fidelity—can push for lower distribution fees and priority shelf spots, pressuring product margins; Ameriprise’s open-architecture stance preserves client choice but cedes pricing influence to external managers.

- ~30% third-party AUM (2024)

- Large families dictate shelf/fee terms

- Open-architecture boosts choice, cuts margins

Data and Research Providers

Data aggregators and research firms like Bloomberg and Morningstar supply the real-time market prices, analytics, and mutual-fund ratings Ameriprise needs for advice and portfolio construction.

With roughly 3–5 top-tier global providers dominating pricing and 60–80% market share in institutional terminals, these suppliers keep strong pricing power over distribution and APIs.

Ameriprise relies on this low-latency data to justify advisory fees; losing access or facing price hikes would raise operating costs and compress advisory margins.

- Few providers: 3–5 major firms

- Market share: 60–80% institutional terminals

- Impact: price hikes raise operating costs

- Dependence: real-time data fuels fee justification

Suppliers’ Scale and Rules Squeeze Ameriprise: Rising Costs, Limited Bargaining Power

Suppliers wield moderate-to-high power: cloud/software vendors (3–5 large providers) and data firms (Bloomberg, Refinitiv, Morningstar) impose multi-year contracts and price power; advisors (10,000+; ~ $1.2T AUM in 2025) and third-party fund families (~30% third-party AUM in 2024) extract fees and shelf terms, while regulators force non-negotiable compliance costs—together these raise costs and limit Ameriprise’s bargaining leverage.

| Supplier | Key stat | Impact |

|---|---|---|

| Advisors | 10,000+; $1.2T AUM (2025) | High retention cost; 1% loss ≈ $12B AUM |

| Cloud/software | 3–5 majors; $50M+/yr contracts | Switching costs; vendor lock-in |

| Third-party funds | ~30% AUM (2024) | Pressure on product margins |

| Data vendors | 3–5 providers; 60–80% market share | Pricing power; fee justification risk |

| Regulators | Compliance spend ↑8% headcount (2024) | Non-negotiable cost base |

What is included in the product

Tailored exclusively for Ameriprise Financial, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, and market entry risks while identifying disruptive threats and substitutes that challenge market share.

Condensed Porter's Five Forces snapshot for Ameriprise—quickly identify competitive pressures and relief points to streamline strategic decisions.

Customers Bargaining Power

High Price Sensitivity in Asset Management

Low Switching Costs for Individual Investors

Automated account transfers and digital onboarding cut switching friction for retail investors, and the ACAT system now moves most U.S. accounts in 3–7 business days; a 2024 Charles Schwab report found 42% of clients considered switching after poor digital service. That mobility lets Ameriprise clients move portfolios quickly if returns or advice disappoint, so customers increasingly demand personalized planning and mobile-first tools—pressuring fees and advisory retention rates.

Demand for Holistic Financial Planning

Clients increasingly prefer goal-based, holistic planning over transactions; a 2024 Cerulli Associates report found 62% of U.S. high-net-worth investors seek integrated advice covering investments, tax, estate, and insurance under one relationship, boosting customer leverage. This trend pressures Ameriprise Financial to bundle services into unified fee models—Advisor Group reported fee-based AUM grew 8% in 2024—so failing to adapt risks higher attrition.

Institutional Negotiating Leverage

Institutional clients like pension funds and corporate retirement plans control large mandates and can push Ameriprise to cut fees materially; in 2025 the top 10 institutional mandates accounted for roughly 12% of Ameriprise’s advisory AUM, so losing one can shave hundreds of millions in AUM and recurring fees.

These buyers run formal RFPs that pit Ameriprise against BlackRock, Vanguard, State Street and others, increasing price pressure and forcing higher service guarantees and reporting costs, which compresses margin on institutional business.

- Top 10 mandates ≈12% of advisory AUM (2025)

- RFP-driven pricing: lower fees, higher service costs

- Single-contract loss → large AUM & revenue hit

Access to Information and Self-Directed Tools

The rise of free financial education and self-directed platforms (Robinhood, Fidelity retail tools) has cut information asymmetry: 62% of US investors used online tools in 2023, per Schwab/INSIDER surveys, making clients more independent.

Ameriprise must offer proprietary research and advanced planning tech—e.g., personalized cash‑flow modeling, tax‑aware strategies, and integration with advice—to justify fees and retain share of wallet.

Fee pressure bites: passive ETFs, fast ACATs & RFPs force AMP to justify advice

| Metric | Value |

|---|---|

| Passive ETF share (US, 2024) | 58% |

| Median advisory fee (2024) | ~0.75% |

| Top 10 mandates of advisory AUM (2025) | ~12% |

| ACAT transfer time | 3–7 days |

What You See Is What You Get

Ameriprise Financial Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Ameriprise Financial you’ll receive immediately after purchase—no placeholders or samples.

The document displayed here is the full, professionally formatted analysis—ready for download and use the moment you buy.

No mockups: this is the exact file you’ll get instantly after payment, complete and ready for your needs.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Ameriprise Financial faces intense rivalry from national brokers and fintech disruptors, moderate buyer power from fee-sensitive clients, and regulatory and technology-driven supplier dynamics shaping margins; barriers to entry are meaningful but evolving with digital platforms. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ameriprise Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Technological Infrastructure Providers

Ameriprise depends on specialized software and cloud providers for wealth-management platforms and client portals, creating high switching costs—enterprise cloud contracts often span 3–5 years and can exceed $50M annually for firms of similar scale. As digital transformation drives competitive edge, these suppliers gain leverage, especially for advanced cybersecurity and analytics where spending rose 18% industry-wide in 2024. Ameriprise must weigh vendor lock-in against urgent needs for real-time analytics and SOC‑grade security.

Human Capital and Financial Advisors

The primary suppliers for Ameriprise are its 10,000+ independent and employee financial advisors who drive client relationships and revenue; as of 2025 advisors managed about $1.2 trillion AUM for the firm. High industry demand for experienced advisors gives them leverage over commission splits, platform fees, and tech/support expectations, raising retention costs. Losing 1% of top-tier advisors could cut AUM by roughly $12 billion and reduce fee revenue proportionally, hurting growth and margins.

Regulatory and Compliance Bodies

Regulatory agencies like the SEC and FINRA act as non-market suppliers of Ameriprise Financials (Ameriprise Financial, Inc.) legal framework, forcing compliance that cannot be negotiated; in 2024 Ameriprise reported $7.4 billion operating revenues, making regulatory costs a material margin pressure. Changes such as tightened fiduciary duty proposals or higher capital/stress-test requirements raise mandatory costs—SEC rule changes in 2023–2025 led many advisors to incur one-time compliance upgrades averaging $0.5–$2 million per firm. Compliance demands continuous spend: Ameriprise’s 2024 regulatory and compliance headcount rose 8% year-over-year and legal/administrative expenses increased roughly 6% to support new reporting, training, and capital monitoring. This non-voluntary cost base limits Ameriprise’s bargaining power versus suppliers of legal rules and elevates fixed operating leverage risk.

Third-Party Asset Managers

Ameriprise runs its own asset management but distributes many third-party funds to offer client choice; in 2024 roughly 30% of advisory platform AUM came from non-affiliated managers, giving those firms leverage over placement and fees.

Big fund families—Vanguard, BlackRock, Fidelity—can push for lower distribution fees and priority shelf spots, pressuring product margins; Ameriprise’s open-architecture stance preserves client choice but cedes pricing influence to external managers.

- ~30% third-party AUM (2024)

- Large families dictate shelf/fee terms

- Open-architecture boosts choice, cuts margins

Data and Research Providers

Data aggregators and research firms like Bloomberg and Morningstar supply the real-time market prices, analytics, and mutual-fund ratings Ameriprise needs for advice and portfolio construction.

With roughly 3–5 top-tier global providers dominating pricing and 60–80% market share in institutional terminals, these suppliers keep strong pricing power over distribution and APIs.

Ameriprise relies on this low-latency data to justify advisory fees; losing access or facing price hikes would raise operating costs and compress advisory margins.

- Few providers: 3–5 major firms

- Market share: 60–80% institutional terminals

- Impact: price hikes raise operating costs

- Dependence: real-time data fuels fee justification

Suppliers’ Scale and Rules Squeeze Ameriprise: Rising Costs, Limited Bargaining Power

Suppliers wield moderate-to-high power: cloud/software vendors (3–5 large providers) and data firms (Bloomberg, Refinitiv, Morningstar) impose multi-year contracts and price power; advisors (10,000+; ~ $1.2T AUM in 2025) and third-party fund families (~30% third-party AUM in 2024) extract fees and shelf terms, while regulators force non-negotiable compliance costs—together these raise costs and limit Ameriprise’s bargaining leverage.

| Supplier | Key stat | Impact |

|---|---|---|

| Advisors | 10,000+; $1.2T AUM (2025) | High retention cost; 1% loss ≈ $12B AUM |

| Cloud/software | 3–5 majors; $50M+/yr contracts | Switching costs; vendor lock-in |

| Third-party funds | ~30% AUM (2024) | Pressure on product margins |

| Data vendors | 3–5 providers; 60–80% market share | Pricing power; fee justification risk |

| Regulators | Compliance spend ↑8% headcount (2024) | Non-negotiable cost base |

What is included in the product

Tailored exclusively for Ameriprise Financial, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, and market entry risks while identifying disruptive threats and substitutes that challenge market share.

Condensed Porter's Five Forces snapshot for Ameriprise—quickly identify competitive pressures and relief points to streamline strategic decisions.

Customers Bargaining Power

High Price Sensitivity in Asset Management

Low Switching Costs for Individual Investors

Automated account transfers and digital onboarding cut switching friction for retail investors, and the ACAT system now moves most U.S. accounts in 3–7 business days; a 2024 Charles Schwab report found 42% of clients considered switching after poor digital service. That mobility lets Ameriprise clients move portfolios quickly if returns or advice disappoint, so customers increasingly demand personalized planning and mobile-first tools—pressuring fees and advisory retention rates.

Demand for Holistic Financial Planning

Clients increasingly prefer goal-based, holistic planning over transactions; a 2024 Cerulli Associates report found 62% of U.S. high-net-worth investors seek integrated advice covering investments, tax, estate, and insurance under one relationship, boosting customer leverage. This trend pressures Ameriprise Financial to bundle services into unified fee models—Advisor Group reported fee-based AUM grew 8% in 2024—so failing to adapt risks higher attrition.

Institutional Negotiating Leverage

Institutional clients like pension funds and corporate retirement plans control large mandates and can push Ameriprise to cut fees materially; in 2025 the top 10 institutional mandates accounted for roughly 12% of Ameriprise’s advisory AUM, so losing one can shave hundreds of millions in AUM and recurring fees.

These buyers run formal RFPs that pit Ameriprise against BlackRock, Vanguard, State Street and others, increasing price pressure and forcing higher service guarantees and reporting costs, which compresses margin on institutional business.

- Top 10 mandates ≈12% of advisory AUM (2025)

- RFP-driven pricing: lower fees, higher service costs

- Single-contract loss → large AUM & revenue hit

Access to Information and Self-Directed Tools

The rise of free financial education and self-directed platforms (Robinhood, Fidelity retail tools) has cut information asymmetry: 62% of US investors used online tools in 2023, per Schwab/INSIDER surveys, making clients more independent.

Ameriprise must offer proprietary research and advanced planning tech—e.g., personalized cash‑flow modeling, tax‑aware strategies, and integration with advice—to justify fees and retain share of wallet.

Fee pressure bites: passive ETFs, fast ACATs & RFPs force AMP to justify advice

| Metric | Value |

|---|---|

| Passive ETF share (US, 2024) | 58% |

| Median advisory fee (2024) | ~0.75% |

| Top 10 mandates of advisory AUM (2025) | ~12% |

| ACAT transfer time | 3–7 days |

What You See Is What You Get

Ameriprise Financial Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Ameriprise Financial you’ll receive immediately after purchase—no placeholders or samples.

The document displayed here is the full, professionally formatted analysis—ready for download and use the moment you buy.

No mockups: this is the exact file you’ll get instantly after payment, complete and ready for your needs.