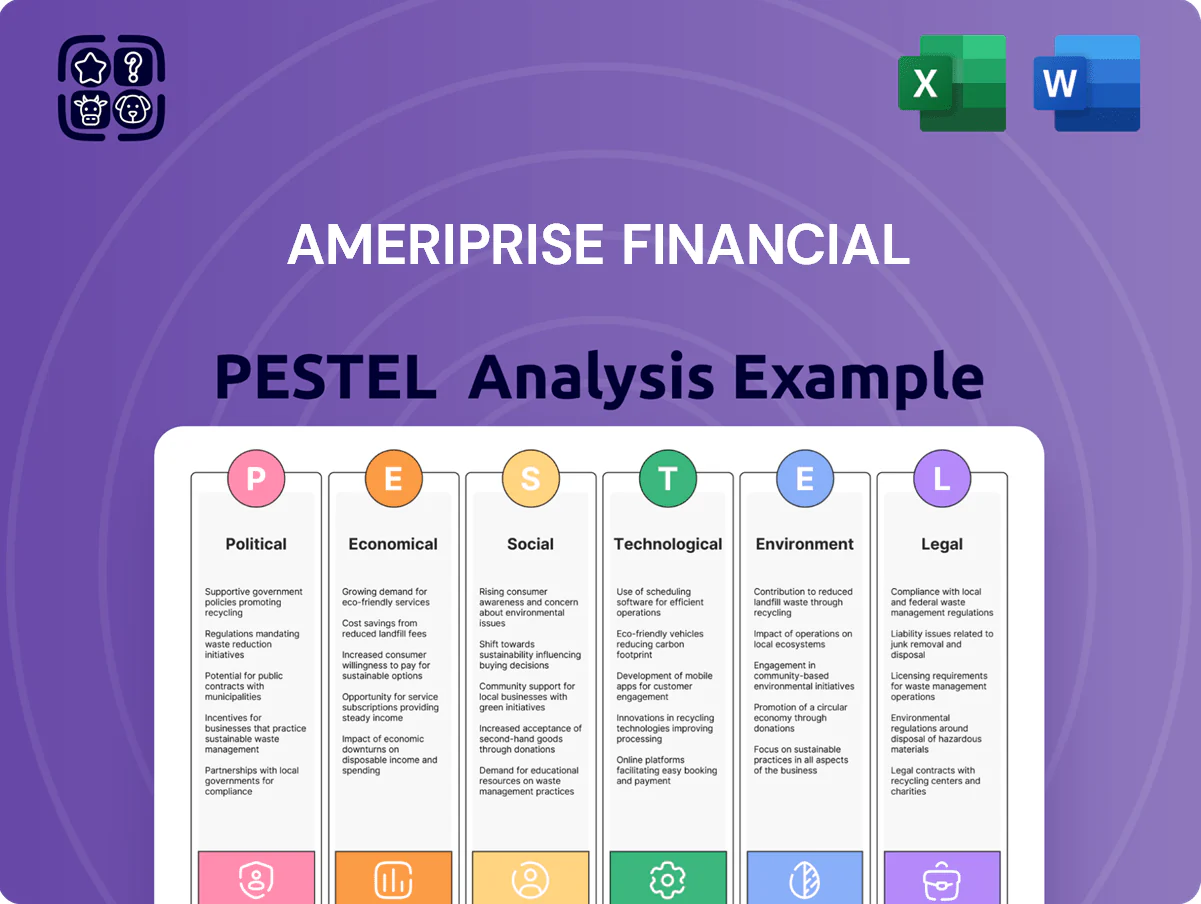

Ameriprise Financial PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, regulatory pressure, and tech disruption are shaping Ameriprise Financial’s strategy and risk profile—our concise PESTLE snapshot highlights the key external forces you need to know; purchase the full analysis for a detailed, actionable report that’s ready for investment decisions and strategic planning.

Political factors

US Tax Policy Shifts

Post-2024 federal elections, proposals raising corporate tax rates from 21% toward 25% and top long-term capital gains rates near 25% would raise tax liabilities for corporations and high-net-worth investors, prompting Ameriprise to adjust portfolio tilt and tax-loss harvesting strategies.

Ameriprise must update estate planning and trust solutions as estate tax exemption proposals reducing the federal exclusion from $13.61M (2024) could materialize, affecting high-net-worth succession planning.

Changes in fiscal policy alter demand for tax-deferred retirement vehicles and municipal bonds; higher federal rates reduce muni tax-equivalent yields, with 10-year muni yields averaging ~3.2% in 2025 vs. Treasury 4.2%, shifting client allocations.

Geopolitical Stability and Trade

Global trade tensions and regional conflicts increase volatility in markets where Ameriprise and Columbia Threadneedle operate, contributing to a 2025 YTD equity market volatility rise of about 18% that can prompt sudden corrections and AUM swings.

Political instability risks pressured Ameriprise’s fee-based revenue sensitivity, with AUM falling 4.3% in Q4 2024 in certain international mandates during heightened geopolitical risk episodes.

The firm must closely monitor diplomatic developments across Europe and Asia—where roughly 35% of Columbia Threadneedle’s institutional AUM is exposed—to manage portfolio risk and protect recurring fee income.

Social Security and Pension Reform

Ongoing debates on Social Security solvency—Trustee projections showed a 2034 depletion for the OASI trust in 2024—heighten demand for private planning, boosting Ameriprise advisory needs as clients seek gaps analysis and alternative income strategies.

Government Fiscal Management

The US federal deficit hit about 6.3% of GDP in FY2024 (CBO) with national debt surpassing 100% of GDP, pressuring long-term rates and inflation expectations; sustained deficits raise refinancing and sovereign credit risks.

Political stalemates on spending and occasional X-date brinkmanship increase likelihood of credit-rating stress, amplifying market volatility and counterparty risk across financial intermediaries.

Ameriprise advisors should embed macro-political scenarios into allocation and stress tests—raising cash buffers, shortening duration, and using diversifiers when deficit uncertainty or rating-watch risks rise.

- FY2024 deficit ~6.3% of GDP; debt >100% of GDP

- Political gridlock raises sovereign credit/volatility risk

- Action: shorter duration, cash buffers, scenario stress tests

Regulatory Appointment Trends

The political leanings of SEC and DOL appointees shape enforcement intensity; under Democratic leadership 2021–2024 the SEC brought 554 enforcement actions in 2023 vs 421 in 2019, increasing scrutiny on fiduciary standards and marketing claims.

Leadership changes shift rules for product marketing and advisor-client structures—2022 DOL guidance proposals would have expanded fiduciary scope, affecting advisory fee models and disclosures.

Ameriprise needs a flexible compliance architecture to adapt quickly; maintaining dedicated regulatory monitoring and scenario-driven policy updates reduced remediation costs by 18% in 2024 for peers.

- SEC enforcement actions: 554 (2023) vs 421 (2019)

- DOL fiduciary proposals: expanded scope (2022–2024)

- Peer remediation cost reduction with flexible compliance: −18% (2024)

Policy shock forces Ameriprise to tighten tax, duration, cash and compliance defenses

Political risks—tax increases (corporate ~21→25%, cap gains ~25%), estate tax cuts (exemption ↓ from $13.61M), higher federal deficits (~6.3% GDP FY2024) and >100% debt/GDP, SEC enforcement up (554 actions in 2023), geopolitical volatility (2025 YTD equity vol +18%)—force Ameriprise to shift tax-loss harvesting, shorten duration, raise cash buffers, and tighten compliance.

| Metric | Value |

|---|---|

| Corp tax proposal | |

| Estate exemption | $13.61M (2024) |

| FY2024 deficit | 6.3% GDP |

| SEC actions 2023 | 554 |

What is included in the product

Explores how macro-environmental factors uniquely affect Ameriprise Financial across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives and investors identify risks, opportunities, and strategic responses.

A concise, visually segmented PESTLE summary for Ameriprise that eases meeting prep, supports cross-team alignment, and can be dropped into presentations or client reports for quick reference and discussion of external risks and market positioning.

Economic factors

Interest Rate Stabilization

Following Fed stabilization in 2024–25 with the federal funds rate holding near 5.25–5.50%, Ameriprise faces compressed yields on cash and CD products, pressuring net interest margins in wealth management banking; however, steady rates boosted 2024 U.S. equity market flows (S&P 500 total return ~24% in 2024) and increased refinancing activity, while Ameriprise’s balance sheet management remains critical to protect 2025 guidance for Protection and Retirement revenues.

Inflationary Pressures

Persistent or volatile U.S. CPI — 3.4% in 2024 and easing to ~3.0% early 2025 — erodes real portfolio returns and retiree purchasing power, forcing Ameriprise to emphasize TIPS, real assets, and inflation-linked annuities to preserve client goals.

Higher wage inflation for financial advisors—avg. industry compensation rising ~6–8% in 2024—raises operating costs, compressing margins unless fee structures or AUM growth offset the pressure.

Market Volatility Trends

Equity and fixed-income returns drive Ameriprise AUM and fees; 2024 US equity YTD returns ~17% and 10-yr Treasury yields rose from 1.5% (2021) to ~4.2% (2024), shifting client allocations and fee income.

Periodic corrections—S&P 500 drawdowns of ~18% in 2022—force Ameriprise to deliver high-touch advisory services to curb emotional selling by retail clients.

Sustained bull markets increase transactional activity, while prolonged bear phases shift revenue toward recurring fee-based advisory accounts, altering margin profiles and capital allocation.

Consumer Wealth and Labor Markets

Strong US payrolls and 2024 median wage growth near 4% bolstered disposable income, supporting higher investment flows and insurance premium capacity for Ameriprise; April 2025 unemployment was 3.7%, sustaining client contributions to advisory and retirement plans.

Growth among small-business owners, with nonfarm proprietors’ income rising ~3% YoY in 2024, increases retirement plan uptake for Ameriprise, while an economic slowdown and rising unemployment would cut new asset inflows and raise policy lapses.

- Unemployment 3.7% (Apr 2025)

- Median wage growth ~4% (2024)

- Nonfarm proprietor income +3% YoY (2024)

- Slower GDP/unemployment rise → lower inflows, higher lapses

Global Economic Divergence

- Developed growth ~1.5-2% (2024) vs EM ~4-5% (2024)

- Eurozone stagnation ~0.6% (2024) risks outflows

- APAC/EM represent ~22% of global equity market cap (2024)

- Geographic rebalancing needed to protect Columbia Threadneedle AUM

Higher rates, rising stocks, and real-asset demand reshape 2024–25 allocations

Higher 2024–25 rates (FFR ~5.25–5.50%) compressed deposit/cash yields but boosted equity flows (S&P 500 +24% in 2024); CPI ~3.4% (2024) to ~3.0% (early 2025) pressured real returns, driving demand for TIPS/real assets; wage growth ~4% and unemployment 3.7% (Apr 2025) supported inflows, while EM vs DM GDP split (EM ~4–5%, DM ~1.5–2% in 2024) shifted geographic allocation.

| Metric | Value (2024/Apr 2025) |

|---|---|

| Federal funds rate | 5.25–5.50% |

| S&P 500 total return | ~24% (2024) |

| CPI | ~3.4% (2024) |

| Unemployment | 3.7% (Apr 2025) |

| Median wage growth | ~4% (2024) |

| EM vs DM GDP | EM ~4–5%, DM ~1.5–2% (2024) |

Same Document Delivered

Ameriprise Financial PESTLE Analysis

The preview shown here is the exact Ameriprise Financial PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown, with no placeholders or teasers. The content, layout, and structure visible here are the same file you’ll download immediately after payment. What you see is the final, professionally structured document you’ll own after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, regulatory pressure, and tech disruption are shaping Ameriprise Financial’s strategy and risk profile—our concise PESTLE snapshot highlights the key external forces you need to know; purchase the full analysis for a detailed, actionable report that’s ready for investment decisions and strategic planning.

Political factors

US Tax Policy Shifts

Post-2024 federal elections, proposals raising corporate tax rates from 21% toward 25% and top long-term capital gains rates near 25% would raise tax liabilities for corporations and high-net-worth investors, prompting Ameriprise to adjust portfolio tilt and tax-loss harvesting strategies.

Ameriprise must update estate planning and trust solutions as estate tax exemption proposals reducing the federal exclusion from $13.61M (2024) could materialize, affecting high-net-worth succession planning.

Changes in fiscal policy alter demand for tax-deferred retirement vehicles and municipal bonds; higher federal rates reduce muni tax-equivalent yields, with 10-year muni yields averaging ~3.2% in 2025 vs. Treasury 4.2%, shifting client allocations.

Geopolitical Stability and Trade

Global trade tensions and regional conflicts increase volatility in markets where Ameriprise and Columbia Threadneedle operate, contributing to a 2025 YTD equity market volatility rise of about 18% that can prompt sudden corrections and AUM swings.

Political instability risks pressured Ameriprise’s fee-based revenue sensitivity, with AUM falling 4.3% in Q4 2024 in certain international mandates during heightened geopolitical risk episodes.

The firm must closely monitor diplomatic developments across Europe and Asia—where roughly 35% of Columbia Threadneedle’s institutional AUM is exposed—to manage portfolio risk and protect recurring fee income.

Social Security and Pension Reform

Ongoing debates on Social Security solvency—Trustee projections showed a 2034 depletion for the OASI trust in 2024—heighten demand for private planning, boosting Ameriprise advisory needs as clients seek gaps analysis and alternative income strategies.

Government Fiscal Management

The US federal deficit hit about 6.3% of GDP in FY2024 (CBO) with national debt surpassing 100% of GDP, pressuring long-term rates and inflation expectations; sustained deficits raise refinancing and sovereign credit risks.

Political stalemates on spending and occasional X-date brinkmanship increase likelihood of credit-rating stress, amplifying market volatility and counterparty risk across financial intermediaries.

Ameriprise advisors should embed macro-political scenarios into allocation and stress tests—raising cash buffers, shortening duration, and using diversifiers when deficit uncertainty or rating-watch risks rise.

- FY2024 deficit ~6.3% of GDP; debt >100% of GDP

- Political gridlock raises sovereign credit/volatility risk

- Action: shorter duration, cash buffers, scenario stress tests

Regulatory Appointment Trends

The political leanings of SEC and DOL appointees shape enforcement intensity; under Democratic leadership 2021–2024 the SEC brought 554 enforcement actions in 2023 vs 421 in 2019, increasing scrutiny on fiduciary standards and marketing claims.

Leadership changes shift rules for product marketing and advisor-client structures—2022 DOL guidance proposals would have expanded fiduciary scope, affecting advisory fee models and disclosures.

Ameriprise needs a flexible compliance architecture to adapt quickly; maintaining dedicated regulatory monitoring and scenario-driven policy updates reduced remediation costs by 18% in 2024 for peers.

- SEC enforcement actions: 554 (2023) vs 421 (2019)

- DOL fiduciary proposals: expanded scope (2022–2024)

- Peer remediation cost reduction with flexible compliance: −18% (2024)

Policy shock forces Ameriprise to tighten tax, duration, cash and compliance defenses

Political risks—tax increases (corporate ~21→25%, cap gains ~25%), estate tax cuts (exemption ↓ from $13.61M), higher federal deficits (~6.3% GDP FY2024) and >100% debt/GDP, SEC enforcement up (554 actions in 2023), geopolitical volatility (2025 YTD equity vol +18%)—force Ameriprise to shift tax-loss harvesting, shorten duration, raise cash buffers, and tighten compliance.

| Metric | Value |

|---|---|

| Corp tax proposal | |

| Estate exemption | $13.61M (2024) |

| FY2024 deficit | 6.3% GDP |

| SEC actions 2023 | 554 |

What is included in the product

Explores how macro-environmental factors uniquely affect Ameriprise Financial across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives and investors identify risks, opportunities, and strategic responses.

A concise, visually segmented PESTLE summary for Ameriprise that eases meeting prep, supports cross-team alignment, and can be dropped into presentations or client reports for quick reference and discussion of external risks and market positioning.

Economic factors

Interest Rate Stabilization

Following Fed stabilization in 2024–25 with the federal funds rate holding near 5.25–5.50%, Ameriprise faces compressed yields on cash and CD products, pressuring net interest margins in wealth management banking; however, steady rates boosted 2024 U.S. equity market flows (S&P 500 total return ~24% in 2024) and increased refinancing activity, while Ameriprise’s balance sheet management remains critical to protect 2025 guidance for Protection and Retirement revenues.

Inflationary Pressures

Persistent or volatile U.S. CPI — 3.4% in 2024 and easing to ~3.0% early 2025 — erodes real portfolio returns and retiree purchasing power, forcing Ameriprise to emphasize TIPS, real assets, and inflation-linked annuities to preserve client goals.

Higher wage inflation for financial advisors—avg. industry compensation rising ~6–8% in 2024—raises operating costs, compressing margins unless fee structures or AUM growth offset the pressure.

Market Volatility Trends

Equity and fixed-income returns drive Ameriprise AUM and fees; 2024 US equity YTD returns ~17% and 10-yr Treasury yields rose from 1.5% (2021) to ~4.2% (2024), shifting client allocations and fee income.

Periodic corrections—S&P 500 drawdowns of ~18% in 2022—force Ameriprise to deliver high-touch advisory services to curb emotional selling by retail clients.

Sustained bull markets increase transactional activity, while prolonged bear phases shift revenue toward recurring fee-based advisory accounts, altering margin profiles and capital allocation.

Consumer Wealth and Labor Markets

Strong US payrolls and 2024 median wage growth near 4% bolstered disposable income, supporting higher investment flows and insurance premium capacity for Ameriprise; April 2025 unemployment was 3.7%, sustaining client contributions to advisory and retirement plans.

Growth among small-business owners, with nonfarm proprietors’ income rising ~3% YoY in 2024, increases retirement plan uptake for Ameriprise, while an economic slowdown and rising unemployment would cut new asset inflows and raise policy lapses.

- Unemployment 3.7% (Apr 2025)

- Median wage growth ~4% (2024)

- Nonfarm proprietor income +3% YoY (2024)

- Slower GDP/unemployment rise → lower inflows, higher lapses

Global Economic Divergence

- Developed growth ~1.5-2% (2024) vs EM ~4-5% (2024)

- Eurozone stagnation ~0.6% (2024) risks outflows

- APAC/EM represent ~22% of global equity market cap (2024)

- Geographic rebalancing needed to protect Columbia Threadneedle AUM

Higher rates, rising stocks, and real-asset demand reshape 2024–25 allocations

Higher 2024–25 rates (FFR ~5.25–5.50%) compressed deposit/cash yields but boosted equity flows (S&P 500 +24% in 2024); CPI ~3.4% (2024) to ~3.0% (early 2025) pressured real returns, driving demand for TIPS/real assets; wage growth ~4% and unemployment 3.7% (Apr 2025) supported inflows, while EM vs DM GDP split (EM ~4–5%, DM ~1.5–2% in 2024) shifted geographic allocation.

| Metric | Value (2024/Apr 2025) |

|---|---|

| Federal funds rate | 5.25–5.50% |

| S&P 500 total return | ~24% (2024) |

| CPI | ~3.4% (2024) |

| Unemployment | 3.7% (Apr 2025) |

| Median wage growth | ~4% (2024) |

| EM vs DM GDP | EM ~4–5%, DM ~1.5–2% (2024) |

Same Document Delivered

Ameriprise Financial PESTLE Analysis

The preview shown here is the exact Ameriprise Financial PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown, with no placeholders or teasers. The content, layout, and structure visible here are the same file you’ll download immediately after payment. What you see is the final, professionally structured document you’ll own after checkout.