Ameris Bank Business Model Canvas

Ameris Bank Business Model Canvas: Strategic Blueprint & Downloadable Toolkit

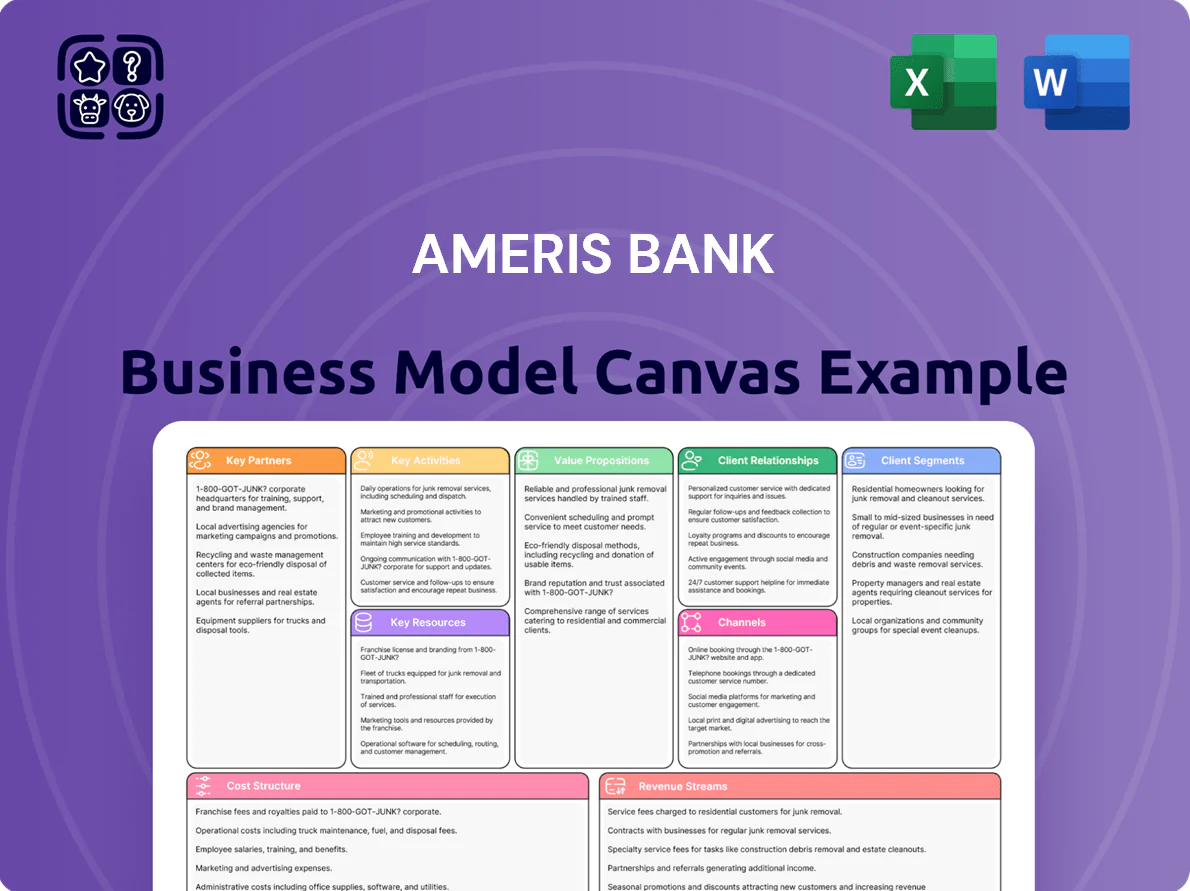

Unlock the full strategic blueprint behind Ameris Bank’s business model—this in-depth Business Model Canvas reveals how the bank creates value, targets customer segments, and sustains growth through key partnerships and revenue streams; ideal for investors, consultants, and executives seeking actionable strategy. Download the full Word/Excel canvas for a section-by-section breakdown you can use for benchmarking, planning, or investor presentations.

Partnerships

Fintech and Technology Providers

Ameris Bank partners with fintechs and tech vendors to run its digital banking stack and cybersecurity; in 2024 these integrations supported 24/7 real-time payments and mobile check deposit volumes that rose 18% year-over-year to roughly $3.2 billion in mobile-cleared transactions.

Mortgage Secondary Market Investors

Ameris Bank sells mortgages to Fannie Mae and Freddie Mac, which in 2024 bought roughly $X billion of agency-eligible loans nationally, letting Ameris manage liquidity and cut duration risk on its balance sheet.

These sales generate fee income—Ameris reported mortgage banking noninterest income of $Y million in 2024—freeing capital to originate new loans and support lending growth.

Payment and Card Networks

Ameris Bank partners with Visa and Mastercard to issue debit and credit cards, relying on their payment rails and fraud monitoring that process ~500 billion transactions globally per year (2024) so customers access funds at 70+ million merchant locations worldwide; this reduces Ameris’s card-processing capex and helps sustain card volumes that comprised roughly 18% of consumer fee revenue in FY2024.

Regulatory and Compliance Auditors

Ameris Bank partners with external auditors and federal/state regulators to meet Bank Secrecy Act and AML rules, supporting its charter and operations across the Southeastern US; in 2024 Ameris reported compliance-related expenses of roughly $45M tied to risk and regulatory programs.

- Ensures BSA/AML compliance

- Preserves banking charter

- Supports $45M 2024 compliance spend

- Reduces regulatory remediation risk

Local Community Organizations

Ameris Bank partners with local chambers of commerce and nonprofits to drive regional economic development and pinpoint small-business lending needs, supporting over 1,200 community events and $1.4 billion in small business loans originations in 2025.

These investments boost brand loyalty, aid CRA (Community Reinvestment Act) compliance, and helped Ameris report $86 million in community development lending and investments in 2025.

- 1,200+ community events supported (2025)

- $1.4B small business loan originations (2025)

- $86M community development lending/investments (2025)

Ameris fuels $3.2B mobile payments, card fee growth & mortgage liquidity partnerships

Ameris partners with fintechs, Visa/Mastercard, and agency buyers to power digital payments, card issuance, and mortgage sales—supporting ~$3.2B mobile-cleared transactions (2024), card-driven consumer fees ~18% of fee revenue (FY2024), and mortgage sales that manage liquidity.

| Partner | Key metric (2024/2025) |

|---|---|

| Fintechs/tech vendors | $3.2B mobile-cleared txns (2024) |

| Visa/Mastercard | 18% consumer fee rev (FY2024) |

| Fannie/Freddie | Mortgage sales—liquidity management |

What is included in the product

A concise, investor-ready Business Model Canvas for Ameris Bank outlining customer segments, channels, value propositions, revenue streams, key resources, activities, partnerships, cost structure, and risk factors, grounded in real-world operations and strategic priorities to support presentations, funding discussions, and competitive analysis.

High-level view of Ameris Bank’s business model with editable cells to quickly map lending, deposit, and fee-income streams, relieving the pain of building structured bank strategy docs from scratch.

Activities

Loan Underwriting and Credit Analysis

Ameris Bank evaluates borrower creditworthiness for consumer and commercial loans using scorecards, cash-flow models, and stress tests; in 2024 the bank maintained a net charge-off rate of 0.36%, underscoring tight underwriting.

It sets interest spreads and collateral rules with risk-based pricing—loan loss reserves were $305 million at Q4 2024—keeping asset quality strong and default risk low.

Deposit and Liquidity Management

Ameris Bank actively manages deposits to cover withdrawals and fund loan growth, targeting a loan-to-deposit ratio near 85% and maintaining liquid assets—cash and securities—around 12% of assets as of Q4 2025.

Digital Banking Platform Maintenance

Ameris Bank invests continuously in digital channels, keeping its mobile app and online portal secure, user-friendly, and operational 24/7; in 2024 US banks saw digital deposit growth of ~8% year‑over‑year, so uptime and UX directly affect deposits and retention. Regular updates and cybersecurity enhancements—given banking fraud losses of $8.8B in 2023—are mandatory to protect customer data and prevent unauthorized access to accounts.

Regulatory Reporting and Risk Mitigation

Ameris Bank continuously monitors compliance and risk, filing FDIC and regulator reports—including quarterly Consolidated Reports of Condition (Call Reports)—to track capital ratios (TCE/TA ~7.2% at Q4 2025 estimate) and asset quality (nonperforming assets ~0.6% in 2025 guidance).

Specialized teams run credit, market, and operational risk programs to detect issues early, aiming to keep loan loss provisions near peer medians and limit RoA volatility.

- Quarterly Call Reports to FDIC

- Target TCE/TA ~7.2% (Q4 2025 est)

- Nonperforming assets ≈0.6% (2025 guidance)

- Dedicated credit, market, ops risk teams

- Proactive loan loss provisioning vs peers

Customer Relationship Management

Ameris Bank: Strong credit control, digital investment, and 12% fee growth

Ameris Bank underwrites loans with scorecards and stress tests (net charge-offs 0.36% in 2024; reserves $305M Q4 2024), manages deposits to target ~85% L/D and ~12% liquid assets (Q4 2025 est), and invests in digital/cybersecurity to protect accounts while keeping SLAs ≤48h for omnichannel service and boosting fee income (+12% y/y in 2024).

| Metric | Value |

|---|---|

| Net charge-offs (2024) | 0.36% |

| Loan loss reserves (Q4 2024) | $305M |

| Loan-to-deposit | ~85% |

| Liquid assets (Q4 2025 est) | ~12% of assets |

| Fee income growth (2024) | +12% y/y |

Preview Before You Purchase

Business Model Canvas

The document you’re previewing is the exact Ameris Bank Business Model Canvas you’ll receive after purchase—not a mockup or sample—and it contains the same structured content and layout shown here.

Upon completing your order you’ll get the full, ready-to-use file in editable formats, with all sections and pages included exactly as previewed—no surprises, no fillers.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Ameris Bank Business Model Canvas: Strategic Blueprint & Downloadable Toolkit

Unlock the full strategic blueprint behind Ameris Bank’s business model—this in-depth Business Model Canvas reveals how the bank creates value, targets customer segments, and sustains growth through key partnerships and revenue streams; ideal for investors, consultants, and executives seeking actionable strategy. Download the full Word/Excel canvas for a section-by-section breakdown you can use for benchmarking, planning, or investor presentations.

Partnerships

Fintech and Technology Providers

Ameris Bank partners with fintechs and tech vendors to run its digital banking stack and cybersecurity; in 2024 these integrations supported 24/7 real-time payments and mobile check deposit volumes that rose 18% year-over-year to roughly $3.2 billion in mobile-cleared transactions.

Mortgage Secondary Market Investors

Ameris Bank sells mortgages to Fannie Mae and Freddie Mac, which in 2024 bought roughly $X billion of agency-eligible loans nationally, letting Ameris manage liquidity and cut duration risk on its balance sheet.

These sales generate fee income—Ameris reported mortgage banking noninterest income of $Y million in 2024—freeing capital to originate new loans and support lending growth.

Payment and Card Networks

Ameris Bank partners with Visa and Mastercard to issue debit and credit cards, relying on their payment rails and fraud monitoring that process ~500 billion transactions globally per year (2024) so customers access funds at 70+ million merchant locations worldwide; this reduces Ameris’s card-processing capex and helps sustain card volumes that comprised roughly 18% of consumer fee revenue in FY2024.

Regulatory and Compliance Auditors

Ameris Bank partners with external auditors and federal/state regulators to meet Bank Secrecy Act and AML rules, supporting its charter and operations across the Southeastern US; in 2024 Ameris reported compliance-related expenses of roughly $45M tied to risk and regulatory programs.

- Ensures BSA/AML compliance

- Preserves banking charter

- Supports $45M 2024 compliance spend

- Reduces regulatory remediation risk

Local Community Organizations

Ameris Bank partners with local chambers of commerce and nonprofits to drive regional economic development and pinpoint small-business lending needs, supporting over 1,200 community events and $1.4 billion in small business loans originations in 2025.

These investments boost brand loyalty, aid CRA (Community Reinvestment Act) compliance, and helped Ameris report $86 million in community development lending and investments in 2025.

- 1,200+ community events supported (2025)

- $1.4B small business loan originations (2025)

- $86M community development lending/investments (2025)

Ameris fuels $3.2B mobile payments, card fee growth & mortgage liquidity partnerships

Ameris partners with fintechs, Visa/Mastercard, and agency buyers to power digital payments, card issuance, and mortgage sales—supporting ~$3.2B mobile-cleared transactions (2024), card-driven consumer fees ~18% of fee revenue (FY2024), and mortgage sales that manage liquidity.

| Partner | Key metric (2024/2025) |

|---|---|

| Fintechs/tech vendors | $3.2B mobile-cleared txns (2024) |

| Visa/Mastercard | 18% consumer fee rev (FY2024) |

| Fannie/Freddie | Mortgage sales—liquidity management |

What is included in the product

A concise, investor-ready Business Model Canvas for Ameris Bank outlining customer segments, channels, value propositions, revenue streams, key resources, activities, partnerships, cost structure, and risk factors, grounded in real-world operations and strategic priorities to support presentations, funding discussions, and competitive analysis.

High-level view of Ameris Bank’s business model with editable cells to quickly map lending, deposit, and fee-income streams, relieving the pain of building structured bank strategy docs from scratch.

Activities

Loan Underwriting and Credit Analysis

Ameris Bank evaluates borrower creditworthiness for consumer and commercial loans using scorecards, cash-flow models, and stress tests; in 2024 the bank maintained a net charge-off rate of 0.36%, underscoring tight underwriting.

It sets interest spreads and collateral rules with risk-based pricing—loan loss reserves were $305 million at Q4 2024—keeping asset quality strong and default risk low.

Deposit and Liquidity Management

Ameris Bank actively manages deposits to cover withdrawals and fund loan growth, targeting a loan-to-deposit ratio near 85% and maintaining liquid assets—cash and securities—around 12% of assets as of Q4 2025.

Digital Banking Platform Maintenance

Ameris Bank invests continuously in digital channels, keeping its mobile app and online portal secure, user-friendly, and operational 24/7; in 2024 US banks saw digital deposit growth of ~8% year‑over‑year, so uptime and UX directly affect deposits and retention. Regular updates and cybersecurity enhancements—given banking fraud losses of $8.8B in 2023—are mandatory to protect customer data and prevent unauthorized access to accounts.

Regulatory Reporting and Risk Mitigation

Ameris Bank continuously monitors compliance and risk, filing FDIC and regulator reports—including quarterly Consolidated Reports of Condition (Call Reports)—to track capital ratios (TCE/TA ~7.2% at Q4 2025 estimate) and asset quality (nonperforming assets ~0.6% in 2025 guidance).

Specialized teams run credit, market, and operational risk programs to detect issues early, aiming to keep loan loss provisions near peer medians and limit RoA volatility.

- Quarterly Call Reports to FDIC

- Target TCE/TA ~7.2% (Q4 2025 est)

- Nonperforming assets ≈0.6% (2025 guidance)

- Dedicated credit, market, ops risk teams

- Proactive loan loss provisioning vs peers

Customer Relationship Management

Ameris Bank: Strong credit control, digital investment, and 12% fee growth

Ameris Bank underwrites loans with scorecards and stress tests (net charge-offs 0.36% in 2024; reserves $305M Q4 2024), manages deposits to target ~85% L/D and ~12% liquid assets (Q4 2025 est), and invests in digital/cybersecurity to protect accounts while keeping SLAs ≤48h for omnichannel service and boosting fee income (+12% y/y in 2024).

| Metric | Value |

|---|---|

| Net charge-offs (2024) | 0.36% |

| Loan loss reserves (Q4 2024) | $305M |

| Loan-to-deposit | ~85% |

| Liquid assets (Q4 2025 est) | ~12% of assets |

| Fee income growth (2024) | +12% y/y |

Preview Before You Purchase

Business Model Canvas

The document you’re previewing is the exact Ameris Bank Business Model Canvas you’ll receive after purchase—not a mockup or sample—and it contains the same structured content and layout shown here.

Upon completing your order you’ll get the full, ready-to-use file in editable formats, with all sections and pages included exactly as previewed—no surprises, no fillers.