Amer Sports Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

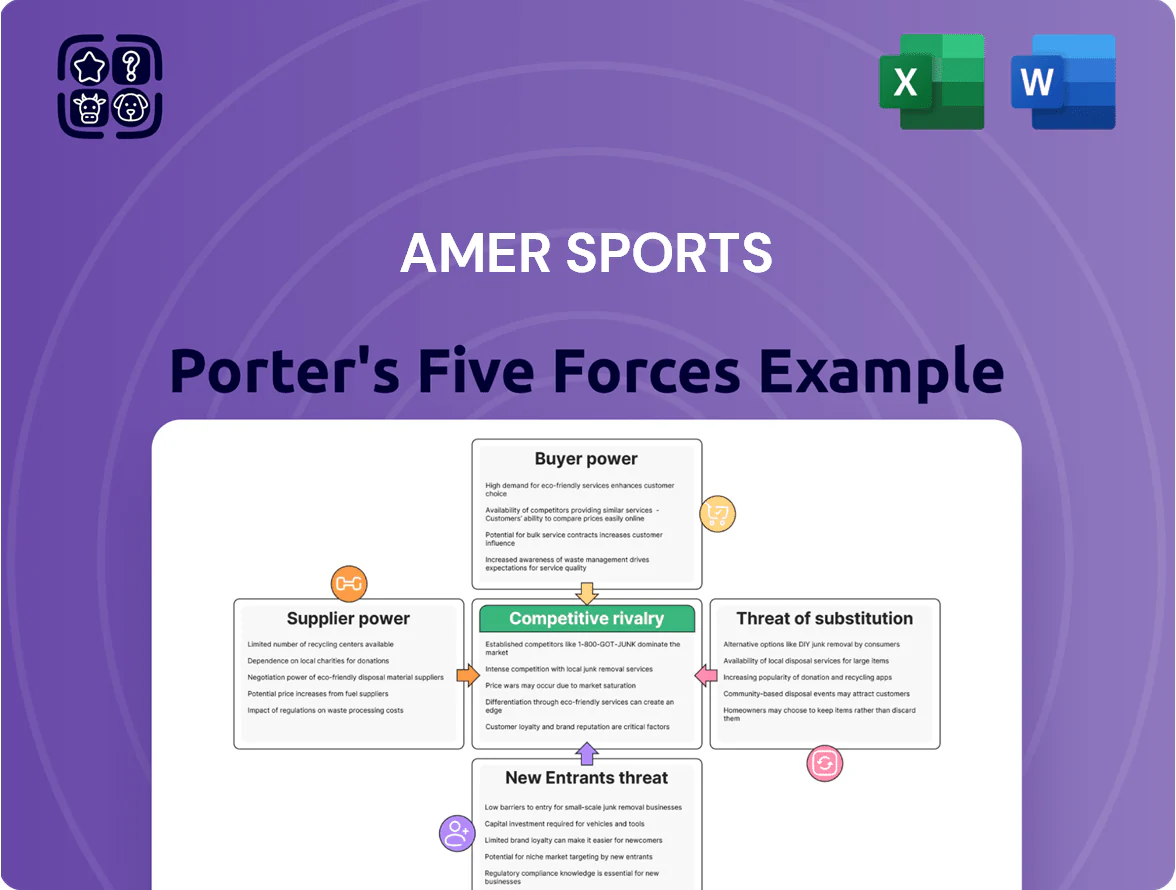

Amer Sports faces moderate buyer power, niche supplier leverage in technical materials, and steady rivalry among global sports brands—while barriers to entry and substitute threats shape margin pressures and innovation priorities; this snapshot highlights key tensions and strategic options.

Suppliers Bargaining Power

Dependence on Specialized Technical Materials

High-performance fabrics like Gore-Tex are critical for Arc'teryx to keep premium pricing; Gore (W. L. Gore & Associates) holds patents and limited capacity, giving suppliers high leverage. Switching costs are large — R&D and requalification can exceed $5–10M per product line and take 12–24 months. Amer Sports (owned by Anta Sports since 2019) needs long-term supply contracts and co‑development partnerships to secure materials and avoid margin erosion.

Geographic Concentration of Manufacturing Partners

Raw Material Price Volatility and Pass-Through Costs

Suppliers of petroleum-based synthetics, specialty metals, and carbon fiber face global commodity swings—petrochemical prices rose ~35% in 2021–22 and carbon fiber spot costs jumped ~20% in 2023—pressuring Amer Sports’ input costs and forcing pass-through to margins.

Amer Sports offsets this by smart pricing and margin management; in 2024 gross margin recovered to ~39% after cost passthroughs and price increases.

The company reduces supplier power via multi-year contracts covering ~60–70% of key inputs and by diversifying sourcing across Europe, Asia, and North America to limit regional shocks.

Supplier Fragmentation in Equipment Segments

Supplier fragmentation in equipment segments means materials like wood cores and composite resins come from many small suppliers, lowering single-supplier leverage versus technical fabrics where suppliers are concentrated.

Amer Sports uses global procurement scale—about €1.8 billion group revenue in 2024—to negotiate volume discounts and enforce quality, cutting input cost volatility and supplier hold-up risk.

- Many small suppliers → low single-supplier power

- Technical fabrics more concentrated → higher supplier power

- Amer Sports scale (2024 revenue €1.8B) aids pricing & quality

Sustainability and Ethical Sourcing Compliance

Rising regulation and consumer demand push suppliers to meet ESG (environmental, social, governance) standards, shrinking the supplier pool but raising compliance value; by 2024 Amer Sports reported 85% of tier-1 suppliers meeting its supplier code and 60% tied into integrated audits, tying partners closer to the brand.

This alignment turns supplier relations collaborative: suppliers gain steady orders and joint sustainability projects, while Amer protects brand reputation—so supplier power is tempered by mutual dependence rather than pure leverage.

- 85% tier-1 suppliers compliant (Amer Sports, 2024)

- 60% under integrated audits (2024)

- Fewer but higher-quality suppliers → lower substitution

- Shared brand risk reduces unilateral supplier bargaining power

Specialized suppliers keep leverage despite Amer Sports' €1.8B revenue and risk buffers

Suppliers of technical fabrics (eg, W. L. Gore) and speciality inputs hold high leverage due to patents, limited capacity, and long requalification (12–24 months, €5–10M), while many small equipment-material suppliers lower single-supplier power; Amer Sports’ 2024 revenue ~€1.8B and 60–70% multi‑year coverage, plus 85% tier‑1 ESG compliance, reduce but do not eliminate supplier risk.

| Metric | Value (2024) |

|---|---|

| Group revenue | €1.8B |

| Multi‑year contracts (key inputs) | 60–70% |

| Tier‑1 ESG compliant | 85% |

| Requalification cost/time | €5–10M / 12–24 months |

What is included in the product

Tailored Porter's Five Forces analysis for Amer Sports, uncovering competitive dynamics, buyer and supplier power, substitution and entry risks, plus disruptive threats—ready for inclusion in reports or strategy decks.

A concise, one-sheet Porter's Five Forces summary for Amer Sports—quickly pinpoint bargaining power and competitive threats to streamline strategic decisions.

Customers Bargaining Power

Shift Toward Direct-to-Consumer Channels

Amer Sports expanded direct-to-consumer (DTC) sales to 28% of revenue in 2024, up from 19% in 2021, growing owned e-commerce and 210 branded stores to capture higher gross margins and first-party customer data.

High Brand Loyalty and Premium Positioning

Arc'teryx and Salomon drive strong loyalty: Arc'teryx grew revenue ~18% in 2024 within Amer Sports, and NPD Group showed premium outdoor gear price resilience, with 65% of core buyers saying they'd pay more for brand quality. This reduces price sensitivity among athletes and serious enthusiasts, so Amer Sports can sustain 15–25% higher ASPs (average selling prices) versus mass-market peers and maintain margin control.

Retailer Consolidation in Sporting Goods

Large retailers such as Dick’s Sporting Goods and JD Sports wield volume leverage—Dick’s had $9.4bn sales in FY2024 and JD Sports €8.6bn in 2023—letting them press Amer Sports for lower wholesale prices, exclusive SKUs, or paid marketing for prime shelf space.

These chains can demand margin concessions and co-op funding; loss of favoured placement can cut brand sell-through by 10–20% based on retail studies, so Amer must balance concessions with margin protection.

Amer Sports is expanding direct channels—sales via independent digital platforms rose ~15% in 2024—reducing retailer dependence while investing in own e‑commerce to preserve pricing power.

Low Switching Costs for Lifestyle Apparel

- Low switching costs → higher buyer power

- Fashion-driven churn ~28% (US, 2024)

- Amer Sports premium pricing ~8–12%

- Counter: tech innovation + product ecosystems

Information Transparency and Price Comparison

- 72% of shoppers compare prices (2024)

- 5–10% price gap harms conversions

- Price integrity crucial to prevent churn

DTC growth and brand loyalty boost pricing—retail giants, churn, and price transparency cap margins

Customers have moderate bargaining power: strong DTC growth (28% of revenue in 2024) and premium loyalty (Arc'teryx +18% revenue 2024; 65% willing to pay more) support pricing power, but large retailers (Dick’s $9.4bn FY2024; JD Sports €8.6bn 2023), low switching costs (US apparel churn ~28% 2024), and price transparency (72% compare prices) constrain margins.

| Metric | Value |

|---|---|

| DTC share 2024 | 28% |

| Arc'teryx growth 2024 | ~18% |

| Dick’s sales FY2024 | $9.4bn |

| US apparel churn 2024 | 28% |

Preview the Actual Deliverable

Amer Sports Porter's Five Forces Analysis

This preview shows the exact Amer Sports Porter’s Five Forces analysis you’ll receive—fully written, formatted, and ready for immediate download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Amer Sports faces moderate buyer power, niche supplier leverage in technical materials, and steady rivalry among global sports brands—while barriers to entry and substitute threats shape margin pressures and innovation priorities; this snapshot highlights key tensions and strategic options.

Suppliers Bargaining Power

Dependence on Specialized Technical Materials

High-performance fabrics like Gore-Tex are critical for Arc'teryx to keep premium pricing; Gore (W. L. Gore & Associates) holds patents and limited capacity, giving suppliers high leverage. Switching costs are large — R&D and requalification can exceed $5–10M per product line and take 12–24 months. Amer Sports (owned by Anta Sports since 2019) needs long-term supply contracts and co‑development partnerships to secure materials and avoid margin erosion.

Geographic Concentration of Manufacturing Partners

Raw Material Price Volatility and Pass-Through Costs

Suppliers of petroleum-based synthetics, specialty metals, and carbon fiber face global commodity swings—petrochemical prices rose ~35% in 2021–22 and carbon fiber spot costs jumped ~20% in 2023—pressuring Amer Sports’ input costs and forcing pass-through to margins.

Amer Sports offsets this by smart pricing and margin management; in 2024 gross margin recovered to ~39% after cost passthroughs and price increases.

The company reduces supplier power via multi-year contracts covering ~60–70% of key inputs and by diversifying sourcing across Europe, Asia, and North America to limit regional shocks.

Supplier Fragmentation in Equipment Segments

Supplier fragmentation in equipment segments means materials like wood cores and composite resins come from many small suppliers, lowering single-supplier leverage versus technical fabrics where suppliers are concentrated.

Amer Sports uses global procurement scale—about €1.8 billion group revenue in 2024—to negotiate volume discounts and enforce quality, cutting input cost volatility and supplier hold-up risk.

- Many small suppliers → low single-supplier power

- Technical fabrics more concentrated → higher supplier power

- Amer Sports scale (2024 revenue €1.8B) aids pricing & quality

Sustainability and Ethical Sourcing Compliance

Rising regulation and consumer demand push suppliers to meet ESG (environmental, social, governance) standards, shrinking the supplier pool but raising compliance value; by 2024 Amer Sports reported 85% of tier-1 suppliers meeting its supplier code and 60% tied into integrated audits, tying partners closer to the brand.

This alignment turns supplier relations collaborative: suppliers gain steady orders and joint sustainability projects, while Amer protects brand reputation—so supplier power is tempered by mutual dependence rather than pure leverage.

- 85% tier-1 suppliers compliant (Amer Sports, 2024)

- 60% under integrated audits (2024)

- Fewer but higher-quality suppliers → lower substitution

- Shared brand risk reduces unilateral supplier bargaining power

Specialized suppliers keep leverage despite Amer Sports' €1.8B revenue and risk buffers

Suppliers of technical fabrics (eg, W. L. Gore) and speciality inputs hold high leverage due to patents, limited capacity, and long requalification (12–24 months, €5–10M), while many small equipment-material suppliers lower single-supplier power; Amer Sports’ 2024 revenue ~€1.8B and 60–70% multi‑year coverage, plus 85% tier‑1 ESG compliance, reduce but do not eliminate supplier risk.

| Metric | Value (2024) |

|---|---|

| Group revenue | €1.8B |

| Multi‑year contracts (key inputs) | 60–70% |

| Tier‑1 ESG compliant | 85% |

| Requalification cost/time | €5–10M / 12–24 months |

What is included in the product

Tailored Porter's Five Forces analysis for Amer Sports, uncovering competitive dynamics, buyer and supplier power, substitution and entry risks, plus disruptive threats—ready for inclusion in reports or strategy decks.

A concise, one-sheet Porter's Five Forces summary for Amer Sports—quickly pinpoint bargaining power and competitive threats to streamline strategic decisions.

Customers Bargaining Power

Shift Toward Direct-to-Consumer Channels

Amer Sports expanded direct-to-consumer (DTC) sales to 28% of revenue in 2024, up from 19% in 2021, growing owned e-commerce and 210 branded stores to capture higher gross margins and first-party customer data.

High Brand Loyalty and Premium Positioning

Arc'teryx and Salomon drive strong loyalty: Arc'teryx grew revenue ~18% in 2024 within Amer Sports, and NPD Group showed premium outdoor gear price resilience, with 65% of core buyers saying they'd pay more for brand quality. This reduces price sensitivity among athletes and serious enthusiasts, so Amer Sports can sustain 15–25% higher ASPs (average selling prices) versus mass-market peers and maintain margin control.

Retailer Consolidation in Sporting Goods

Large retailers such as Dick’s Sporting Goods and JD Sports wield volume leverage—Dick’s had $9.4bn sales in FY2024 and JD Sports €8.6bn in 2023—letting them press Amer Sports for lower wholesale prices, exclusive SKUs, or paid marketing for prime shelf space.

These chains can demand margin concessions and co-op funding; loss of favoured placement can cut brand sell-through by 10–20% based on retail studies, so Amer must balance concessions with margin protection.

Amer Sports is expanding direct channels—sales via independent digital platforms rose ~15% in 2024—reducing retailer dependence while investing in own e‑commerce to preserve pricing power.

Low Switching Costs for Lifestyle Apparel

- Low switching costs → higher buyer power

- Fashion-driven churn ~28% (US, 2024)

- Amer Sports premium pricing ~8–12%

- Counter: tech innovation + product ecosystems

Information Transparency and Price Comparison

- 72% of shoppers compare prices (2024)

- 5–10% price gap harms conversions

- Price integrity crucial to prevent churn

DTC growth and brand loyalty boost pricing—retail giants, churn, and price transparency cap margins

Customers have moderate bargaining power: strong DTC growth (28% of revenue in 2024) and premium loyalty (Arc'teryx +18% revenue 2024; 65% willing to pay more) support pricing power, but large retailers (Dick’s $9.4bn FY2024; JD Sports €8.6bn 2023), low switching costs (US apparel churn ~28% 2024), and price transparency (72% compare prices) constrain margins.

| Metric | Value |

|---|---|

| DTC share 2024 | 28% |

| Arc'teryx growth 2024 | ~18% |

| Dick’s sales FY2024 | $9.4bn |

| US apparel churn 2024 | 28% |

Preview the Actual Deliverable

Amer Sports Porter's Five Forces Analysis

This preview shows the exact Amer Sports Porter’s Five Forces analysis you’ll receive—fully written, formatted, and ready for immediate download with no placeholders or mockups.