Amer Sports PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic advantages with our focused PESTLE Analysis of Amer Sports—revealing how political, economic, social, technological, legal, and environmental forces shape growth and risk; ideal for investors, consultants, and strategists. Purchase the full report to access granular, actionable insights and ready-to-use slides and spreadsheets that accelerate smarter decisions.

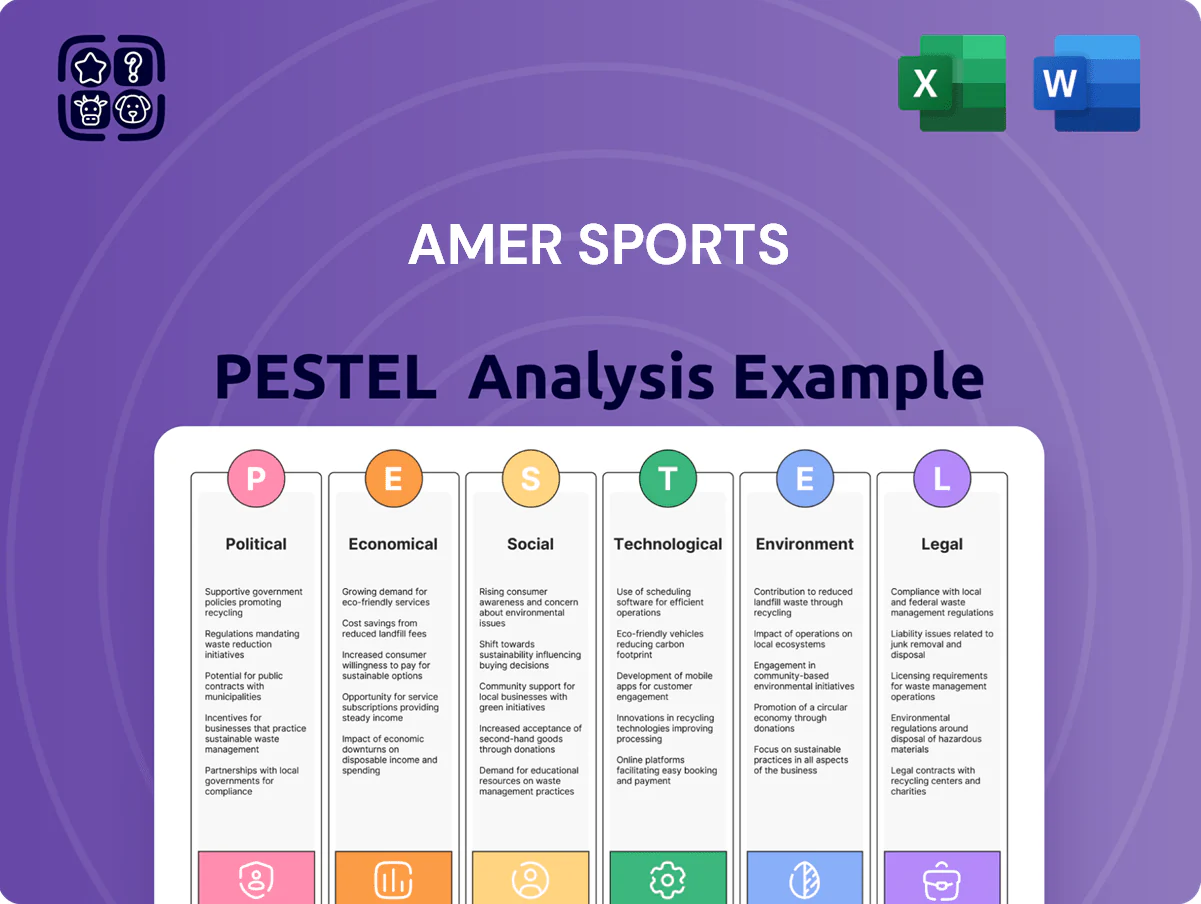

Political factors

US-China Trade Relations

The ongoing US-China trade tensions affect Amer Sports—majority-owned by Chinese consortium ANTA Sports—through exposure to cross-border capital flows and data-privacy scrutiny after ANTA’s 2019 acquisition; in 2024 heightened CFIUS-like reviews raised compliance costs for similar deals by an estimated 10–15% of transaction value.

Tariffs on Asian-made sporting goods can swing with diplomacy; US tariffs on Chinese imports averaged 7.5%–25% during 2018–2022 and could raise COGS by several percentage points, forcing flexible sourcing to protect 2025 gross margins projected near 45%.

Analysts should track diplomatic shifts and consumer sentiment: in 2023 US brand trust surveys showed 12% sensitivity to ownership origin, potentially impacting Amer Sports’ North American market access and sales mix.

Geopolitical Stability in Manufacturing Hubs

Amer Sports depends on suppliers and facilities across Southeast Asia and Europe; in 2024 about 62% of its manufacturing footprint was in Asia, exposing it to political unrest risks that caused average lead-time delays of 18% in regional shocks. Political instability can spike logistics costs—recent unrest in Southeast Asia raised freight premiums by up to 22%—so Amer must navigate varied regulations and ensure resilience through diversified sites to avoid over-reliance on any single jurisdiction.

Ownership and Corporate Governance Scrutiny

The influence of ANTA Sports, which increased its stake to 97.7% after the 2022 takeover valuing Amer Sports at ~US$5.2bn, raises political scrutiny over governance and cross-border compliance in key markets.

Western regulators have ramped filings and disclosure expectations for firms with significant Chinese ownership, citing transparency risks—Amer faces enhanced reporting in the EU and US.

This oversight impacts protection of IP and strategic assets across brands like Wilson and Atomic, where 2024 revenue contributions remain core to valuation.

Balancing a unified global corporate identity with regional political expectations is thus a material strategic and regulatory challenge for Amer Sports.

Global Trade Agreements and Tariffs

Changes in EU and USMCA rules alter COGS for Amer Sports, where 2024 tariff shifts raised average import duties on sporting goods by up to 3.1%, squeezing margins on premium footwear with gross margins near 45%.

Protectionist moves in 2025 saw several markets propose duties up to 10% on outdoor equipment, prompting Amer Sports to reassess supply chains and consider nearshoring to protect EBITDA.

Tracking customs preferential origin updates lets Amer Sports adjust pricing and logistics; in 2024 optimized routing reduced landed costs by about 1.8% in core European markets.

- Monitor EU/USMCA amendments affecting tariff codes

- Assess nearshoring where duties exceed 5%

- Use origin rules to retain preferential rates

- Reprice to protect gross margins (~45%)

Government Health and Wellness Initiatives

Many governments increased funding for public health: EU recovery and resilience plans allocated over EUR 100bn to health and recreation (2021–2024), boosting outdoor infrastructure that benefits Amer Sports brands.

Policy incentives for parks, ski resorts and community facilities expand TAM for Salomon and Arc'teryx by lowering participation costs; ski resort investments rose 12% YoY in 2023 in key markets.

Aligning CSR with government health agendas enhances regional political capital and access to public partnerships and grants that can offset product rollout costs and marketing spend.

- EUR 100bn+ EU health/recreation funding

- 12% YoY ski resort investment growth (2023)

- Expanded TAM via infrastructure lowers entry barriers

- CSR alignment increases public partnership opportunities

Regulatory, tariff and supply risks vs EUR100bn EU upside for ANTA-led group

US-China tensions and 97.7% ANTA ownership raise regulatory scrutiny and CFIUS-like reviews (2024 deal-compliance costs +10–15%); tariffs (2018–22 avg 7.5–25%) and 2024 duty shifts (+3.1%) pressure COGS and ~45% gross margins; 62% Asian manufacturing footprint caused 18% lead-time delays in shocks and up to +22% freight premiums; EU health/recreation funding EUR100bn+ expands TAM.

| Metric | Value (year) |

|---|---|

| ANTA stake | 97.7% (2022) |

| Deal valuation | ~US$5.2bn (2022) |

| Asian manufacturing | 62% (2024) |

| Gross margin | ~45% (2024) |

| CFIUS-like cost uplift | +10–15% (2024) |

| Avg tariffs (2018–22) | 7.5–25% |

| 2024 tariff shift | +3.1% |

| Freight premium in unrest | +22% |

| EU health funding | EUR100bn+ (2021–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Amer Sports across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify risks and opportunities for executives, investors, and strategists.

Condensed Amer Sports PESTLE that’s visually segmented for quick reference, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Consumer Discretionary Spending Trends

Demand for premium sporting goods is highly income-sensitive; OECD real disposable income fell 1.2% y/y in 2024 in major markets, pressuring mid-market sales while Arc'teryx retained share among top deciles.

Inflation eased to 3.4% OECD average by Q3 2025 but real consumer spending growth slowed as global policy rates averaged 4.1%, reducing purchasing power for outdoor enthusiasts.

During downturns replacement cycles lengthened—average outdoor gear replacement intervals rose from 5.2 years (2021) to 6.1 years (2024) per industry surveys.

Analysts monitor consumer sentiment: the Conference Board U.S. index dropped to 78.6 in 2025, guiding revenue forecasts for luxury performance segments.

Currency Exchange Rate Volatility

Operating globally with roughly 40% sales in EUR, 35% in USD and 15% in CNY, Amer Sports faces transaction and translation risks that drove a reported FX headwind of about EUR 40m in 2024.

A stronger EUR vs USD can depress reported margins for European brands like Peak Performance and Salomon, contributing to a 2–3 percentage-point swing in segment EBIT in 2023–24.

The company uses forward contracts and options—hedging roughly 70% of exposure—but persistent currency imbalances still pressure international pricing and market competitiveness.

Investors dissect FX effects to separate organic revenue growth from currency-driven gains, noting that currency swings accounted for an estimated 4% of YoY revenue variance in 2024.

Raw Material and Energy Costs

The production of Amer Sports’ high-performance footwear and technical apparel relies heavily on petroleum-based synthetics and specialized textiles; a 2024 IEA-driven spike in oil to ~USD 85/barrel raised polymer feedstock costs by ~12–15%, pressuring input margins.

Volatility in global energy markets lifts manufacturing overhead and transport costs for bulky goods like Wilson tennis balls—sea freight rates averaged 2,100 USD/FEU in 2024, up ~18% vs 2022.

Price rises in technical membranes and carbon fiber—carbon fiber spot prices rose ~10% in 2023–24—can compress gross margins if not passed to consumers amid competitive retail pricing.

Efficient resource management, lean inventory and supply-chain optimization (nearshoring, long-term supplier contracts) proved critical in 2024 to protect profitability amid rising input and logistics costs.

Growth of the Asian Middle Class

The continued expansion of Asia's middle class—projected to reach 3.5 billion people by 2030 per Brookings—is a major growth lever for Amer Sports, as rising disposable incomes in China and Southeast Asia increase demand for premium Western sports brands.

Amer Sports is expanding retail footprints and localized marketing; Greater China contributed about 18% of parent revenues in 2024, signaling successful penetration versus slower growth in Western Europe and North America.

- Asia middle class to 2030: ~3.5bn (Brookings)

- Greater China revenue share 2024: ~18%

- Higher willingness-to-pay for premium Western brands

- Strategy: retail expansion + localized marketing

Labor Market Dynamics and Costs

- Wage inflation 4–6% China, 3–5% Eastern Europe (2023–25)

- R&D intensity ~4–6% of sales; talent salary inflation 6–8%

- Automation capex rising 10–15% in sector

- Trends affect scalability, margins, and ethical sourcing costs

2024–25 economic squeeze: incomes down, inflation up, EUR40m FX hit, China 18% sales

Economic headwinds in 2024–25 compressed demand and margins: OECD real disposable income -1.2% (2024), inflation ~3.4% (Q3 2025), global policy rates ~4.1%; FX cost ~EUR 40m headwind (2024); input cost pressures from oil ~USD85/bbl and polymer +12–15%; Greater China ~18% revenue (2024); wage inflation China 4–6% (2023–25).

| Metric | Value |

|---|---|

| OECD real disposable income (2024) | -1.2% |

| Inflation (OECD, Q3 2025) | 3.4% |

| FX headwind (2024) | ~EUR 40m |

| Greater China revenue (2024) | ~18% |

Full Version Awaits

Amer Sports PESTLE Analysis

The preview shown here is the exact Amer Sports PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic advantages with our focused PESTLE Analysis of Amer Sports—revealing how political, economic, social, technological, legal, and environmental forces shape growth and risk; ideal for investors, consultants, and strategists. Purchase the full report to access granular, actionable insights and ready-to-use slides and spreadsheets that accelerate smarter decisions.

Political factors

US-China Trade Relations

The ongoing US-China trade tensions affect Amer Sports—majority-owned by Chinese consortium ANTA Sports—through exposure to cross-border capital flows and data-privacy scrutiny after ANTA’s 2019 acquisition; in 2024 heightened CFIUS-like reviews raised compliance costs for similar deals by an estimated 10–15% of transaction value.

Tariffs on Asian-made sporting goods can swing with diplomacy; US tariffs on Chinese imports averaged 7.5%–25% during 2018–2022 and could raise COGS by several percentage points, forcing flexible sourcing to protect 2025 gross margins projected near 45%.

Analysts should track diplomatic shifts and consumer sentiment: in 2023 US brand trust surveys showed 12% sensitivity to ownership origin, potentially impacting Amer Sports’ North American market access and sales mix.

Geopolitical Stability in Manufacturing Hubs

Amer Sports depends on suppliers and facilities across Southeast Asia and Europe; in 2024 about 62% of its manufacturing footprint was in Asia, exposing it to political unrest risks that caused average lead-time delays of 18% in regional shocks. Political instability can spike logistics costs—recent unrest in Southeast Asia raised freight premiums by up to 22%—so Amer must navigate varied regulations and ensure resilience through diversified sites to avoid over-reliance on any single jurisdiction.

Ownership and Corporate Governance Scrutiny

The influence of ANTA Sports, which increased its stake to 97.7% after the 2022 takeover valuing Amer Sports at ~US$5.2bn, raises political scrutiny over governance and cross-border compliance in key markets.

Western regulators have ramped filings and disclosure expectations for firms with significant Chinese ownership, citing transparency risks—Amer faces enhanced reporting in the EU and US.

This oversight impacts protection of IP and strategic assets across brands like Wilson and Atomic, where 2024 revenue contributions remain core to valuation.

Balancing a unified global corporate identity with regional political expectations is thus a material strategic and regulatory challenge for Amer Sports.

Global Trade Agreements and Tariffs

Changes in EU and USMCA rules alter COGS for Amer Sports, where 2024 tariff shifts raised average import duties on sporting goods by up to 3.1%, squeezing margins on premium footwear with gross margins near 45%.

Protectionist moves in 2025 saw several markets propose duties up to 10% on outdoor equipment, prompting Amer Sports to reassess supply chains and consider nearshoring to protect EBITDA.

Tracking customs preferential origin updates lets Amer Sports adjust pricing and logistics; in 2024 optimized routing reduced landed costs by about 1.8% in core European markets.

- Monitor EU/USMCA amendments affecting tariff codes

- Assess nearshoring where duties exceed 5%

- Use origin rules to retain preferential rates

- Reprice to protect gross margins (~45%)

Government Health and Wellness Initiatives

Many governments increased funding for public health: EU recovery and resilience plans allocated over EUR 100bn to health and recreation (2021–2024), boosting outdoor infrastructure that benefits Amer Sports brands.

Policy incentives for parks, ski resorts and community facilities expand TAM for Salomon and Arc'teryx by lowering participation costs; ski resort investments rose 12% YoY in 2023 in key markets.

Aligning CSR with government health agendas enhances regional political capital and access to public partnerships and grants that can offset product rollout costs and marketing spend.

- EUR 100bn+ EU health/recreation funding

- 12% YoY ski resort investment growth (2023)

- Expanded TAM via infrastructure lowers entry barriers

- CSR alignment increases public partnership opportunities

Regulatory, tariff and supply risks vs EUR100bn EU upside for ANTA-led group

US-China tensions and 97.7% ANTA ownership raise regulatory scrutiny and CFIUS-like reviews (2024 deal-compliance costs +10–15%); tariffs (2018–22 avg 7.5–25%) and 2024 duty shifts (+3.1%) pressure COGS and ~45% gross margins; 62% Asian manufacturing footprint caused 18% lead-time delays in shocks and up to +22% freight premiums; EU health/recreation funding EUR100bn+ expands TAM.

| Metric | Value (year) |

|---|---|

| ANTA stake | 97.7% (2022) |

| Deal valuation | ~US$5.2bn (2022) |

| Asian manufacturing | 62% (2024) |

| Gross margin | ~45% (2024) |

| CFIUS-like cost uplift | +10–15% (2024) |

| Avg tariffs (2018–22) | 7.5–25% |

| 2024 tariff shift | +3.1% |

| Freight premium in unrest | +22% |

| EU health funding | EUR100bn+ (2021–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Amer Sports across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify risks and opportunities for executives, investors, and strategists.

Condensed Amer Sports PESTLE that’s visually segmented for quick reference, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Consumer Discretionary Spending Trends

Demand for premium sporting goods is highly income-sensitive; OECD real disposable income fell 1.2% y/y in 2024 in major markets, pressuring mid-market sales while Arc'teryx retained share among top deciles.

Inflation eased to 3.4% OECD average by Q3 2025 but real consumer spending growth slowed as global policy rates averaged 4.1%, reducing purchasing power for outdoor enthusiasts.

During downturns replacement cycles lengthened—average outdoor gear replacement intervals rose from 5.2 years (2021) to 6.1 years (2024) per industry surveys.

Analysts monitor consumer sentiment: the Conference Board U.S. index dropped to 78.6 in 2025, guiding revenue forecasts for luxury performance segments.

Currency Exchange Rate Volatility

Operating globally with roughly 40% sales in EUR, 35% in USD and 15% in CNY, Amer Sports faces transaction and translation risks that drove a reported FX headwind of about EUR 40m in 2024.

A stronger EUR vs USD can depress reported margins for European brands like Peak Performance and Salomon, contributing to a 2–3 percentage-point swing in segment EBIT in 2023–24.

The company uses forward contracts and options—hedging roughly 70% of exposure—but persistent currency imbalances still pressure international pricing and market competitiveness.

Investors dissect FX effects to separate organic revenue growth from currency-driven gains, noting that currency swings accounted for an estimated 4% of YoY revenue variance in 2024.

Raw Material and Energy Costs

The production of Amer Sports’ high-performance footwear and technical apparel relies heavily on petroleum-based synthetics and specialized textiles; a 2024 IEA-driven spike in oil to ~USD 85/barrel raised polymer feedstock costs by ~12–15%, pressuring input margins.

Volatility in global energy markets lifts manufacturing overhead and transport costs for bulky goods like Wilson tennis balls—sea freight rates averaged 2,100 USD/FEU in 2024, up ~18% vs 2022.

Price rises in technical membranes and carbon fiber—carbon fiber spot prices rose ~10% in 2023–24—can compress gross margins if not passed to consumers amid competitive retail pricing.

Efficient resource management, lean inventory and supply-chain optimization (nearshoring, long-term supplier contracts) proved critical in 2024 to protect profitability amid rising input and logistics costs.

Growth of the Asian Middle Class

The continued expansion of Asia's middle class—projected to reach 3.5 billion people by 2030 per Brookings—is a major growth lever for Amer Sports, as rising disposable incomes in China and Southeast Asia increase demand for premium Western sports brands.

Amer Sports is expanding retail footprints and localized marketing; Greater China contributed about 18% of parent revenues in 2024, signaling successful penetration versus slower growth in Western Europe and North America.

- Asia middle class to 2030: ~3.5bn (Brookings)

- Greater China revenue share 2024: ~18%

- Higher willingness-to-pay for premium Western brands

- Strategy: retail expansion + localized marketing

Labor Market Dynamics and Costs

- Wage inflation 4–6% China, 3–5% Eastern Europe (2023–25)

- R&D intensity ~4–6% of sales; talent salary inflation 6–8%

- Automation capex rising 10–15% in sector

- Trends affect scalability, margins, and ethical sourcing costs

2024–25 economic squeeze: incomes down, inflation up, EUR40m FX hit, China 18% sales

Economic headwinds in 2024–25 compressed demand and margins: OECD real disposable income -1.2% (2024), inflation ~3.4% (Q3 2025), global policy rates ~4.1%; FX cost ~EUR 40m headwind (2024); input cost pressures from oil ~USD85/bbl and polymer +12–15%; Greater China ~18% revenue (2024); wage inflation China 4–6% (2023–25).

| Metric | Value |

|---|---|

| OECD real disposable income (2024) | -1.2% |

| Inflation (OECD, Q3 2025) | 3.4% |

| FX headwind (2024) | ~EUR 40m |

| Greater China revenue (2024) | ~18% |

Full Version Awaits

Amer Sports PESTLE Analysis

The preview shown here is the exact Amer Sports PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.