AMG PESTLE Analysis

Skip the Research. Get the Strategy.

Uncover how political shifts, economic cycles, and tech disruption are shaping AMG's strategic path with our concise PESTLE Analysis—designed for investors and strategists who need fast, actionable insight; purchase the full report to access the complete, editable breakdown and evidence-backed recommendations.

Political factors

Geopolitical Stability and Cross-Border Capital Flows

The global nature of AMG’s affiliate network makes the firm highly sensitive to shifts in international relations and trade policy as of late 2025, with 60% of its $350bn AUM tied to affiliates in North America, Europe and APAC.

Political tensions in hubs like London, Hong Kong and Dubai have in recent years prompted episodic capital flight—EM outflows reached $120bn in 2024—risking AUM declines for exposed affiliates.

AMG must diversify its geographic footprint and maintain diplomatic intelligence; reallocating just 5% of AUM away from high-risk jurisdictions could shield roughly $17.5bn in assets.

Tax Policy Evolution in Major Economies

Government Fiscal Policy and Market Liquidity

National fiscal decisions, such as the US 2025 federal deficit projected at about 6.2% of GDP and $1.7tn in infrastructure outlays in 2024–25, directly influence market liquidity where AMG affiliates operate.

Expansive fiscal stances have lifted nominal asset valuations—global equity market cap rose ~12% in 2024—forcing rapid portfolio rebalancing across fixed income and alternatives.

AMG offers partners scenario-based guidance and liquidity stress testing, using real-time treasury yield curves and cash-flow models to position portfolios for multi-year stability.

Protectionism in Financial Services

A rising wave of protectionism could tilt regulations toward domestic asset managers, increasing entry costs in markets like India and Brazil where foreign AM share fell 5-8% in 2023–24; AMG faces higher compliance and potential market-access limits.

AMG reduces this risk by highlighting affiliate operational independence—local brands managing ~60% of its AUM in growth regions—leveraging regional expertise to retain market share.

- Protectionism rose in 2023–24; foreign AM market share down 5–8% in key EMs

- Potential higher compliance/entry costs for AMG

- ~60% of AMG AUM in growth regions managed by local affiliates

Global Regulatory Harmonization Efforts

Global moves toward regulatory harmonization—such as IOSCO initiatives and EU-US dialogues—can lower AMG’s cross-border compliance costs, while fragmentation (e.g., 2024-25 crypto/sustainable finance rule divergences) forces multi-jurisdictional frameworks that raise operational spend.

AMG’s efficiency in managing varied political mandates is a 2025 competitive edge, impacting scalability of its ~$3.3 trillion assets under management and compliance headcount/cost ratios.

- Harmonization reduces duplication and lowers compliance costs

- Fragmentation increases legal, reporting, and operational complexity

- Effective multi-jurisdiction management supports AMG’s scale on $3.3T AUM

AMG $3.3T at Geopolitical Risk—Reallocating 5% AUM Could Shield ~$17.5B

AMG’s $3.3T AUM is exposed to geopolitical shifts—60% tied to North America, Europe, APAC—so EM outflows ($120bn in 2024) and protectionism (foreign AM share down 5–8% in 2023–24) materially threaten revenue and access; reallocating 5% AUM (~$165bn) from high-risk jurisdictions could shield ~ $17.5bn. Tax and fiscal moves (US debt ~$35.9T, EU debt ~88% GDP) may compress margins; regulatory fragmentation raises compliance costs.

| Metric | Value |

|---|---|

| Total AUM | $3.3T (2025) |

| AUM in NA/EU/APAC | 60% (~$1.98T) |

| EM outflows | $120bn (2024) |

| Protectionism impact | Foreign AM share −5–8% (2023–24) |

| US federal debt | $35.9T (2025) |

| EU public debt | ~88% GDP (2024) |

What is included in the product

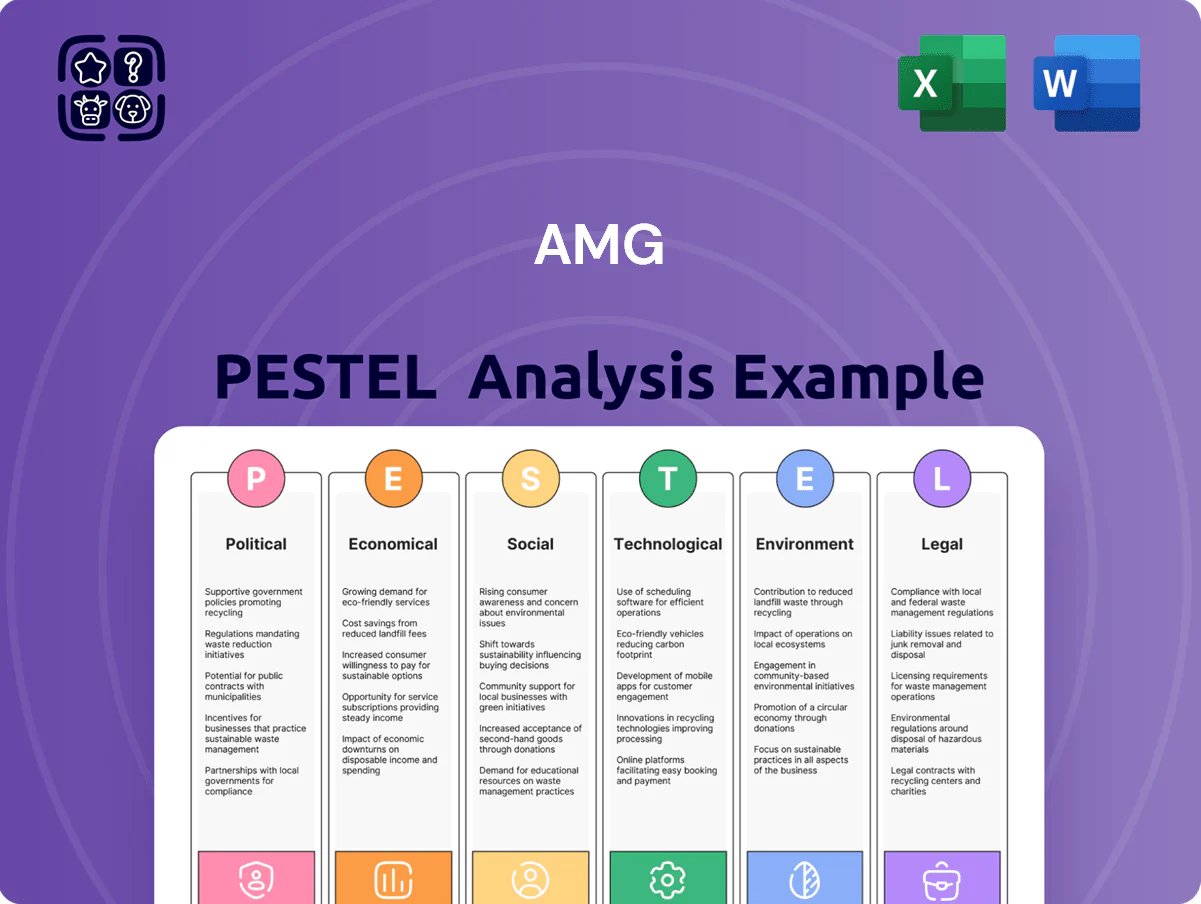

Explores how external macro-environmental factors uniquely affect AMG across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trend analysis to identify risks and opportunities for executives, investors, and strategists.

Provides a clean, visually segmented PESTLE summary of AMG that’s easy to drop into presentations or share across teams, helping stakeholders quickly grasp external risks and market positioning during planning sessions.

Economic factors

Interest Rate Environment and Asset Valuations

By end-2025, global policy rates largely stabilized near 3.5–4.5% in developed markets after 2022–24 volatility, compressing bond yields and lifting equity P/E multiples by ~10–15% vs 2023; AMG affiliates must recalibrate discount rates and lower return targets accordingly.

Revised cost-of-capital assumptions—up ~75–150bps vs pre-2022 norms—require AMG to adjust DCF inputs across strategies, impacting valuation of credit-sensitive assets and long-duration growth names.

AMG’s multi-style platform positions it to capture relative winners as cyclical sectors reprice with rate moves while defensive and income strategies benefit from higher yield floors and tighter spreads.

Inflationary Trends and Operating Costs

Persistent inflation—US CPI at 3.4% in 2024 and core CPI ~3.6%—raises AMG affiliates’ wage and tech costs, pressuring margins and real client returns; fee income is diluted unless AUM growth exceeds rising costs (AMG reported 2024 AUM up 5% year-over-year). AMG offsets this by pushing cost-efficient operating models, centralized tech investments and shared services to protect fee margins during economic uncertainty.

Market Volatility and Fee Revenue

AMG's fee revenue is highly tied to AUM performance; a 20% global equity drawdown in 2022 cut industry fee income sharply and AMG reported fee revenue volatility with assets under management falling 12% YoY to $127.5B in 2022, rebounding to about $140B by 2024 as markets recovered.

Currency Exchange Rate Fluctuations

With ~60% of revenues generated outside the US, AMG’s reported results are sensitive to USD strength; a 10% USD appreciation in 2023 reduced reported international revenue roughly by ~6–8% on translation.

Adverse FX moves can obscure affiliate growth when repatriated, even as local operations expand in euros, GBP and SGD.

AMG employs forwards, options and cross-currency swaps plus local-currency reinvestment; hedges covered an estimated 55–70% of near-term exposures in 2024.

- ~60% revenues outside US

- 10% USD rise ≈ 6–8% reported revenue drag (2023)

- Hedging covers ~55–70% near-term exposure (2024)

- Local-currency reinvestment reduces repatriation volatility

Growth in Alternative Assets and Private Markets

The shift to private markets—private equity, private credit, and real assets—was a strong tailwind for AMG by 2025, with global private capital AUM reaching about $12.5 trillion in 2024 and continuing expansion into 2025.

Institutional demand for higher yields and diversification pushed allocations away from public stocks/bonds, directing substantial capital to AMG’s specialized affiliates focused on higher-margin alternatives.

Higher-margin products and multi-year lock-ups improved revenue visibility; private credit and real assets delivered steadier fee-based income and boosted AMG’s fee margin in recent reporting periods.

- Global private capital AUM ~ $12.5T (2024)

- Institutional allocations to alternatives rising vs. public markets (2023–25)

- Private strategies => higher fee margins and predictable lock-up revenue

Higher-for-longer rates squeeze valuations; $12.5T private AUM and FX drag revenue

Higher-for-longer rates (policy ~3.5–4.5% by end-2025) raised discount rates +75–150bps vs pre-2022, compressing valuations; US core CPI ~3.6% (2024) pressures costs; private capital AUM ~ $12.5T (2024) boosts AMG alternatives revenue; FX: ~60% revenue ex-US, 10% USD rise cut reported revenue ~6–8%; hedges covered ~55–70% (2024).

| Metric | 2024–25 |

|---|---|

| Policy rates | 3.5–4.5% |

| Core CPI (US) | ~3.6% |

| Private capital AUM | $12.5T |

| Revenue ex-US | ~60% |

| USD impact | 10% → −6–8% |

| Hedge coverage | 55–70% |

Preview the Actual Deliverable

AMG PESTLE Analysis

The preview shown here is the exact AMG PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Uncover how political shifts, economic cycles, and tech disruption are shaping AMG's strategic path with our concise PESTLE Analysis—designed for investors and strategists who need fast, actionable insight; purchase the full report to access the complete, editable breakdown and evidence-backed recommendations.

Political factors

Geopolitical Stability and Cross-Border Capital Flows

The global nature of AMG’s affiliate network makes the firm highly sensitive to shifts in international relations and trade policy as of late 2025, with 60% of its $350bn AUM tied to affiliates in North America, Europe and APAC.

Political tensions in hubs like London, Hong Kong and Dubai have in recent years prompted episodic capital flight—EM outflows reached $120bn in 2024—risking AUM declines for exposed affiliates.

AMG must diversify its geographic footprint and maintain diplomatic intelligence; reallocating just 5% of AUM away from high-risk jurisdictions could shield roughly $17.5bn in assets.

Tax Policy Evolution in Major Economies

Government Fiscal Policy and Market Liquidity

National fiscal decisions, such as the US 2025 federal deficit projected at about 6.2% of GDP and $1.7tn in infrastructure outlays in 2024–25, directly influence market liquidity where AMG affiliates operate.

Expansive fiscal stances have lifted nominal asset valuations—global equity market cap rose ~12% in 2024—forcing rapid portfolio rebalancing across fixed income and alternatives.

AMG offers partners scenario-based guidance and liquidity stress testing, using real-time treasury yield curves and cash-flow models to position portfolios for multi-year stability.

Protectionism in Financial Services

A rising wave of protectionism could tilt regulations toward domestic asset managers, increasing entry costs in markets like India and Brazil where foreign AM share fell 5-8% in 2023–24; AMG faces higher compliance and potential market-access limits.

AMG reduces this risk by highlighting affiliate operational independence—local brands managing ~60% of its AUM in growth regions—leveraging regional expertise to retain market share.

- Protectionism rose in 2023–24; foreign AM market share down 5–8% in key EMs

- Potential higher compliance/entry costs for AMG

- ~60% of AMG AUM in growth regions managed by local affiliates

Global Regulatory Harmonization Efforts

Global moves toward regulatory harmonization—such as IOSCO initiatives and EU-US dialogues—can lower AMG’s cross-border compliance costs, while fragmentation (e.g., 2024-25 crypto/sustainable finance rule divergences) forces multi-jurisdictional frameworks that raise operational spend.

AMG’s efficiency in managing varied political mandates is a 2025 competitive edge, impacting scalability of its ~$3.3 trillion assets under management and compliance headcount/cost ratios.

- Harmonization reduces duplication and lowers compliance costs

- Fragmentation increases legal, reporting, and operational complexity

- Effective multi-jurisdiction management supports AMG’s scale on $3.3T AUM

AMG $3.3T at Geopolitical Risk—Reallocating 5% AUM Could Shield ~$17.5B

AMG’s $3.3T AUM is exposed to geopolitical shifts—60% tied to North America, Europe, APAC—so EM outflows ($120bn in 2024) and protectionism (foreign AM share down 5–8% in 2023–24) materially threaten revenue and access; reallocating 5% AUM (~$165bn) from high-risk jurisdictions could shield ~ $17.5bn. Tax and fiscal moves (US debt ~$35.9T, EU debt ~88% GDP) may compress margins; regulatory fragmentation raises compliance costs.

| Metric | Value |

|---|---|

| Total AUM | $3.3T (2025) |

| AUM in NA/EU/APAC | 60% (~$1.98T) |

| EM outflows | $120bn (2024) |

| Protectionism impact | Foreign AM share −5–8% (2023–24) |

| US federal debt | $35.9T (2025) |

| EU public debt | ~88% GDP (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect AMG across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trend analysis to identify risks and opportunities for executives, investors, and strategists.

Provides a clean, visually segmented PESTLE summary of AMG that’s easy to drop into presentations or share across teams, helping stakeholders quickly grasp external risks and market positioning during planning sessions.

Economic factors

Interest Rate Environment and Asset Valuations

By end-2025, global policy rates largely stabilized near 3.5–4.5% in developed markets after 2022–24 volatility, compressing bond yields and lifting equity P/E multiples by ~10–15% vs 2023; AMG affiliates must recalibrate discount rates and lower return targets accordingly.

Revised cost-of-capital assumptions—up ~75–150bps vs pre-2022 norms—require AMG to adjust DCF inputs across strategies, impacting valuation of credit-sensitive assets and long-duration growth names.

AMG’s multi-style platform positions it to capture relative winners as cyclical sectors reprice with rate moves while defensive and income strategies benefit from higher yield floors and tighter spreads.

Inflationary Trends and Operating Costs

Persistent inflation—US CPI at 3.4% in 2024 and core CPI ~3.6%—raises AMG affiliates’ wage and tech costs, pressuring margins and real client returns; fee income is diluted unless AUM growth exceeds rising costs (AMG reported 2024 AUM up 5% year-over-year). AMG offsets this by pushing cost-efficient operating models, centralized tech investments and shared services to protect fee margins during economic uncertainty.

Market Volatility and Fee Revenue

AMG's fee revenue is highly tied to AUM performance; a 20% global equity drawdown in 2022 cut industry fee income sharply and AMG reported fee revenue volatility with assets under management falling 12% YoY to $127.5B in 2022, rebounding to about $140B by 2024 as markets recovered.

Currency Exchange Rate Fluctuations

With ~60% of revenues generated outside the US, AMG’s reported results are sensitive to USD strength; a 10% USD appreciation in 2023 reduced reported international revenue roughly by ~6–8% on translation.

Adverse FX moves can obscure affiliate growth when repatriated, even as local operations expand in euros, GBP and SGD.

AMG employs forwards, options and cross-currency swaps plus local-currency reinvestment; hedges covered an estimated 55–70% of near-term exposures in 2024.

- ~60% revenues outside US

- 10% USD rise ≈ 6–8% reported revenue drag (2023)

- Hedging covers ~55–70% near-term exposure (2024)

- Local-currency reinvestment reduces repatriation volatility

Growth in Alternative Assets and Private Markets

The shift to private markets—private equity, private credit, and real assets—was a strong tailwind for AMG by 2025, with global private capital AUM reaching about $12.5 trillion in 2024 and continuing expansion into 2025.

Institutional demand for higher yields and diversification pushed allocations away from public stocks/bonds, directing substantial capital to AMG’s specialized affiliates focused on higher-margin alternatives.

Higher-margin products and multi-year lock-ups improved revenue visibility; private credit and real assets delivered steadier fee-based income and boosted AMG’s fee margin in recent reporting periods.

- Global private capital AUM ~ $12.5T (2024)

- Institutional allocations to alternatives rising vs. public markets (2023–25)

- Private strategies => higher fee margins and predictable lock-up revenue

Higher-for-longer rates squeeze valuations; $12.5T private AUM and FX drag revenue

Higher-for-longer rates (policy ~3.5–4.5% by end-2025) raised discount rates +75–150bps vs pre-2022, compressing valuations; US core CPI ~3.6% (2024) pressures costs; private capital AUM ~ $12.5T (2024) boosts AMG alternatives revenue; FX: ~60% revenue ex-US, 10% USD rise cut reported revenue ~6–8%; hedges covered ~55–70% (2024).

| Metric | 2024–25 |

|---|---|

| Policy rates | 3.5–4.5% |

| Core CPI (US) | ~3.6% |

| Private capital AUM | $12.5T |

| Revenue ex-US | ~60% |

| USD impact | 10% → −6–8% |

| Hedge coverage | 55–70% |

Preview the Actual Deliverable

AMG PESTLE Analysis

The preview shown here is the exact AMG PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.