Amotiv Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

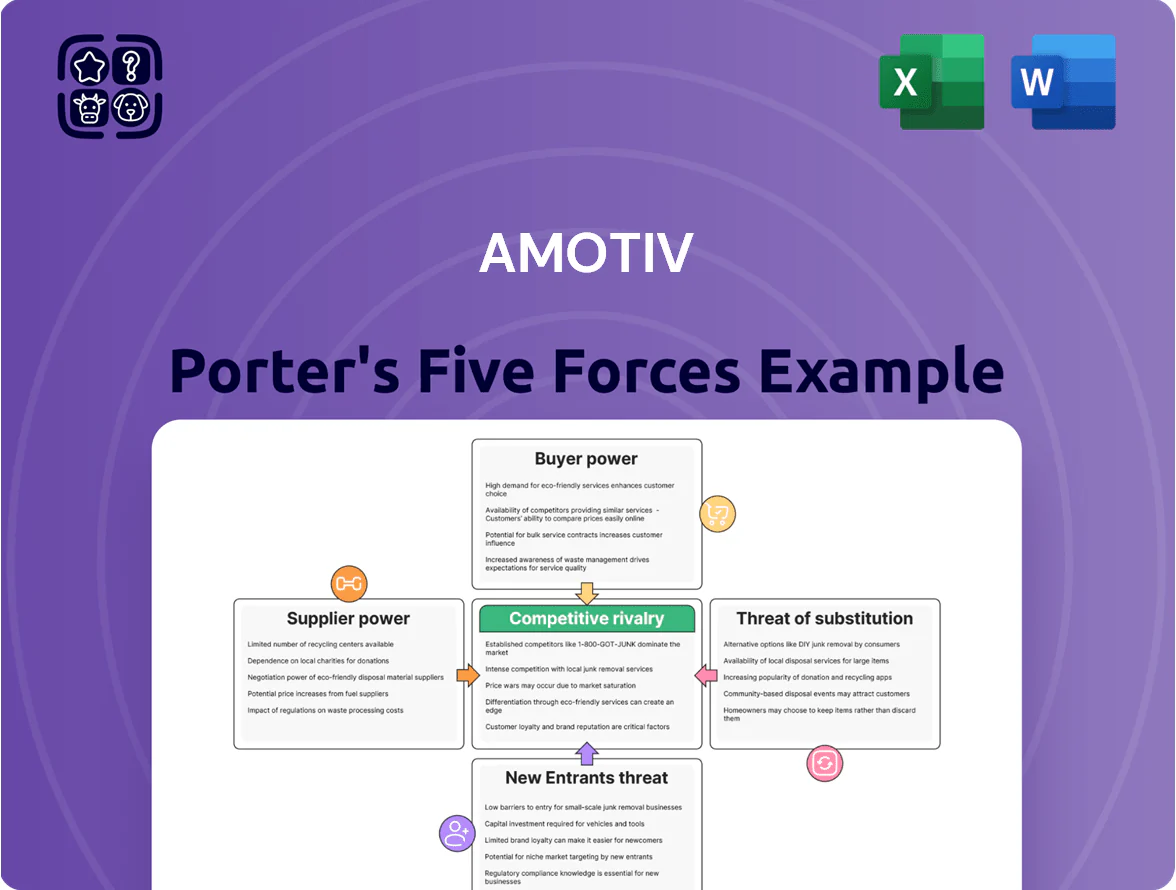

Amotiv faces moderate supplier bargaining and rising substitute threats amid intense rivalry from established tech incumbents and well-funded entrants, while customer switching costs and regulatory shifts shape strategic positioning.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Amotiv’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Component Manufacturer Concentration

Amotiv relies on specialized manufacturers for electronics and high-quality components, but global Tier 1 consolidation raises supplier leverage; the top 5 Tier 1s control ~60% of module revenue worldwide as of 2025, so pricing or allocation shifts can hit costs quickly.

Raw Material Price Volatility

Amotiv’s production costs track global steel, aluminum, and specialty-plastics prices; steel rose ~18% in 2024 and aluminum ~12% (LME averages), pushing input costs higher.

Suppliers typically pass through hikes during geopolitical shocks and 2022–24 supply disruptions, reducing Amotiv’s margin flexibility.

Without multi-year hedges or diversified sourcing, Amotiv cannot reliably control raw-material cost volatility and faces earnings variability.

Technological Proprietary Constraints

As vehicles gain software-defined features, Amotiv depends on a small set of proprietary-software and specialized-electronics suppliers; globally, 4 major Tier-1 telematics/software providers control ~60% of fleet telematics market (2024 IDC), giving suppliers leverage.

These vendors supply essential modules for maintenance and fleet-management; lost access would disrupt ops and reduce uptime, so Amotiv faces high supplier power.

Switching costs are steep: integrating new stacks can cost $2–5m and take 6–12 months per fleet, locking Amotiv to current suppliers.

Logistics and Distribution Costs

Suppliers of logistics and shipping services are critical to Amotiv’s inventory flow; in 2024 global freight rates rose ~28% year-over-year, so carriers can demand higher fees.

Rising fuel prices (average Brent up 15% in 2024) and transport labor shortages (IHS Markit reported 12% driver shortfall in 2024) tighten suppliers’ leverage.

Amotiv’s just-in-time/high-availability model leaves little room to refuse rate hikes, forcing margin compression or higher end prices.

- Freight rates +28% (2024)

- Brent +15% (2024)

- Driver shortfall ~12% (2024)

Supplier Integration Potential

There is a moderate threat of forward integration: in 2024 global OEM parts makers increased direct aftermarket sales by ~6%, showing manufacturers can and do move downstream to capture ~3–7 percentage points of distributor margin.

This risk lets manufacturers use direct parts access to undercut service pricing, so Amotiv must keep collaborative contracts, volume guarantees, and co-marketing to protect ~5–10% margin.

- 2024 OEM direct aftermarket growth ~6%

- Potential margin capture 3–7 p.p.

- Defensive moves: contracts, volume guarantees, co-marketing

Supplier squeeze: Amotiv faces concentrated vendors, rising input costs & margin risk

Amotiv faces high supplier power: top 5 Tier-1s hold ~60% module revenue (2025), key telematics vendors ~60% share (2024), steel +18% and aluminum +12% (2024), freight +28% and Brent +15% (2024); switching costs $2–5m and 6–12 months, OEM aftermarket push +6% (2024) risks 3–7 p.p. margin loss without contracts.

| Metric | Value (year) |

|---|---|

| Top-5 Tier1 share | ~60% (2025) |

| Telematics top-4 | ~60% (2024) |

| Steel / Aluminum | +18% / +12% (2024) |

| Freight / Brent | +28% / +15% (2024) |

| Switch cost / time | $2–5m, 6–12m |

| OEM aftermarket growth | +6% (2024) |

What is included in the product

Tailored exclusively for Amotiv, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary to guide pricing, positioning, and risk mitigation.

Compact, one-sheet Porter's Five Forces snapshot that translates competitive dynamics into actionable strategy—ideal for quick boardroom decisions.

Customers Bargaining Power

Retail Channel Consolidation

Fleet Manager Price Sensitivity

Corporate and government fleet managers focus on total cost of ownership and push for the lowest maintenance and leasing rates; in 2024, 62% of large fleets used competitive tendering to cut costs, forcing providers like Amotiv to trim margins.

The ability to switch national providers with little disruption—average churn-cost under $350 per vehicle—gives buyers strong leverage, driving contract negotiation toward price reductions and tighter SLAs.

Availability of Transparent Information

In the digital age, instant price comparison and review platforms cut information asymmetry, letting consumers and procurement teams demand price matching or higher service levels; 73% of buyers use online reviews before purchase (BrightLocal, 2024). This forces Amotiv to spend more on brand loyalty and service quality—expect customer retention programs and service investment to rise by 8–12% of marketing/operational budgets to prevent churn driven by price alone.

Low Switching Costs for Individuals

Individual vehicle owners face very low switching costs when moving from Amotiv to independents or chains; surveys show 62% of US car owners chose a new service provider after a single poor experience in 2024.

Maintenance is often seen as a commodity, so brand loyalty erodes without steady excellence and competitive pricing—Amotiv must match average hourly labor rates (~$120 in 2024) to stay relevant.

This ease of movement forces Amotiv to boost customer experience and loyalty programs; retailers with rewards saw a 14% retention lift in 2023.

- 62% switched after one bad visit (2024 survey)

- Average labor rate ~$120/hr (US, 2024)

- Rewards programs +14% retention (2023)

Volume Discount Expectations

Large buyers expect tiered pricing: in 2024 fleets buying 10k+ units secured average discounts of 12–18%, pressuring Amotiv to offer deeper cuts as customers consolidate.

Consolidation raises bargaining power; top 5 logistics groups now control ~38% of US fleet procurement, so discount demands will grow.

Amotiv should bundle services—fleet analytics, predictive maintenance, telematics—with pricing to keep gross margins above 25% while meeting volume expectations.

- 2024 avg discount for 10k+ orders: 12–18%

- Top 5 buyers control ~38% US procurement

- Target gross margin with bundles: >25%

Customer concentration & churn squeeze Amotiv—bundle services to protect 25%+ margins

| Metric | 2024 |

|---|---|

| Top-3 retailer share | ~45% |

| Amotiv volume to top-3 | ~60% |

| Fleet discounts (10k+) | 12–18% |

| Top-5 buyer control | ~38% |

| Owner churn after 1 bad visit | 62% |

| Avg labor rate | $120/hr |

| Target gross margin | >25% |

Same Document Delivered

Amotiv Porter's Five Forces Analysis

This preview shows the exact Amotiv Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professional, and ready to use with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Amotiv faces moderate supplier bargaining and rising substitute threats amid intense rivalry from established tech incumbents and well-funded entrants, while customer switching costs and regulatory shifts shape strategic positioning.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Amotiv’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Component Manufacturer Concentration

Amotiv relies on specialized manufacturers for electronics and high-quality components, but global Tier 1 consolidation raises supplier leverage; the top 5 Tier 1s control ~60% of module revenue worldwide as of 2025, so pricing or allocation shifts can hit costs quickly.

Raw Material Price Volatility

Amotiv’s production costs track global steel, aluminum, and specialty-plastics prices; steel rose ~18% in 2024 and aluminum ~12% (LME averages), pushing input costs higher.

Suppliers typically pass through hikes during geopolitical shocks and 2022–24 supply disruptions, reducing Amotiv’s margin flexibility.

Without multi-year hedges or diversified sourcing, Amotiv cannot reliably control raw-material cost volatility and faces earnings variability.

Technological Proprietary Constraints

As vehicles gain software-defined features, Amotiv depends on a small set of proprietary-software and specialized-electronics suppliers; globally, 4 major Tier-1 telematics/software providers control ~60% of fleet telematics market (2024 IDC), giving suppliers leverage.

These vendors supply essential modules for maintenance and fleet-management; lost access would disrupt ops and reduce uptime, so Amotiv faces high supplier power.

Switching costs are steep: integrating new stacks can cost $2–5m and take 6–12 months per fleet, locking Amotiv to current suppliers.

Logistics and Distribution Costs

Suppliers of logistics and shipping services are critical to Amotiv’s inventory flow; in 2024 global freight rates rose ~28% year-over-year, so carriers can demand higher fees.

Rising fuel prices (average Brent up 15% in 2024) and transport labor shortages (IHS Markit reported 12% driver shortfall in 2024) tighten suppliers’ leverage.

Amotiv’s just-in-time/high-availability model leaves little room to refuse rate hikes, forcing margin compression or higher end prices.

- Freight rates +28% (2024)

- Brent +15% (2024)

- Driver shortfall ~12% (2024)

Supplier Integration Potential

There is a moderate threat of forward integration: in 2024 global OEM parts makers increased direct aftermarket sales by ~6%, showing manufacturers can and do move downstream to capture ~3–7 percentage points of distributor margin.

This risk lets manufacturers use direct parts access to undercut service pricing, so Amotiv must keep collaborative contracts, volume guarantees, and co-marketing to protect ~5–10% margin.

- 2024 OEM direct aftermarket growth ~6%

- Potential margin capture 3–7 p.p.

- Defensive moves: contracts, volume guarantees, co-marketing

Supplier squeeze: Amotiv faces concentrated vendors, rising input costs & margin risk

Amotiv faces high supplier power: top 5 Tier-1s hold ~60% module revenue (2025), key telematics vendors ~60% share (2024), steel +18% and aluminum +12% (2024), freight +28% and Brent +15% (2024); switching costs $2–5m and 6–12 months, OEM aftermarket push +6% (2024) risks 3–7 p.p. margin loss without contracts.

| Metric | Value (year) |

|---|---|

| Top-5 Tier1 share | ~60% (2025) |

| Telematics top-4 | ~60% (2024) |

| Steel / Aluminum | +18% / +12% (2024) |

| Freight / Brent | +28% / +15% (2024) |

| Switch cost / time | $2–5m, 6–12m |

| OEM aftermarket growth | +6% (2024) |

What is included in the product

Tailored exclusively for Amotiv, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary to guide pricing, positioning, and risk mitigation.

Compact, one-sheet Porter's Five Forces snapshot that translates competitive dynamics into actionable strategy—ideal for quick boardroom decisions.

Customers Bargaining Power

Retail Channel Consolidation

Fleet Manager Price Sensitivity

Corporate and government fleet managers focus on total cost of ownership and push for the lowest maintenance and leasing rates; in 2024, 62% of large fleets used competitive tendering to cut costs, forcing providers like Amotiv to trim margins.

The ability to switch national providers with little disruption—average churn-cost under $350 per vehicle—gives buyers strong leverage, driving contract negotiation toward price reductions and tighter SLAs.

Availability of Transparent Information

In the digital age, instant price comparison and review platforms cut information asymmetry, letting consumers and procurement teams demand price matching or higher service levels; 73% of buyers use online reviews before purchase (BrightLocal, 2024). This forces Amotiv to spend more on brand loyalty and service quality—expect customer retention programs and service investment to rise by 8–12% of marketing/operational budgets to prevent churn driven by price alone.

Low Switching Costs for Individuals

Individual vehicle owners face very low switching costs when moving from Amotiv to independents or chains; surveys show 62% of US car owners chose a new service provider after a single poor experience in 2024.

Maintenance is often seen as a commodity, so brand loyalty erodes without steady excellence and competitive pricing—Amotiv must match average hourly labor rates (~$120 in 2024) to stay relevant.

This ease of movement forces Amotiv to boost customer experience and loyalty programs; retailers with rewards saw a 14% retention lift in 2023.

- 62% switched after one bad visit (2024 survey)

- Average labor rate ~$120/hr (US, 2024)

- Rewards programs +14% retention (2023)

Volume Discount Expectations

Large buyers expect tiered pricing: in 2024 fleets buying 10k+ units secured average discounts of 12–18%, pressuring Amotiv to offer deeper cuts as customers consolidate.

Consolidation raises bargaining power; top 5 logistics groups now control ~38% of US fleet procurement, so discount demands will grow.

Amotiv should bundle services—fleet analytics, predictive maintenance, telematics—with pricing to keep gross margins above 25% while meeting volume expectations.

- 2024 avg discount for 10k+ orders: 12–18%

- Top 5 buyers control ~38% US procurement

- Target gross margin with bundles: >25%

Customer concentration & churn squeeze Amotiv—bundle services to protect 25%+ margins

| Metric | 2024 |

|---|---|

| Top-3 retailer share | ~45% |

| Amotiv volume to top-3 | ~60% |

| Fleet discounts (10k+) | 12–18% |

| Top-5 buyer control | ~38% |

| Owner churn after 1 bad visit | 62% |

| Avg labor rate | $120/hr |

| Target gross margin | >25% |

Same Document Delivered

Amotiv Porter's Five Forces Analysis

This preview shows the exact Amotiv Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professional, and ready to use with no placeholders or samples.