amwell Boston Consulting Group Matrix

See the Bigger Picture

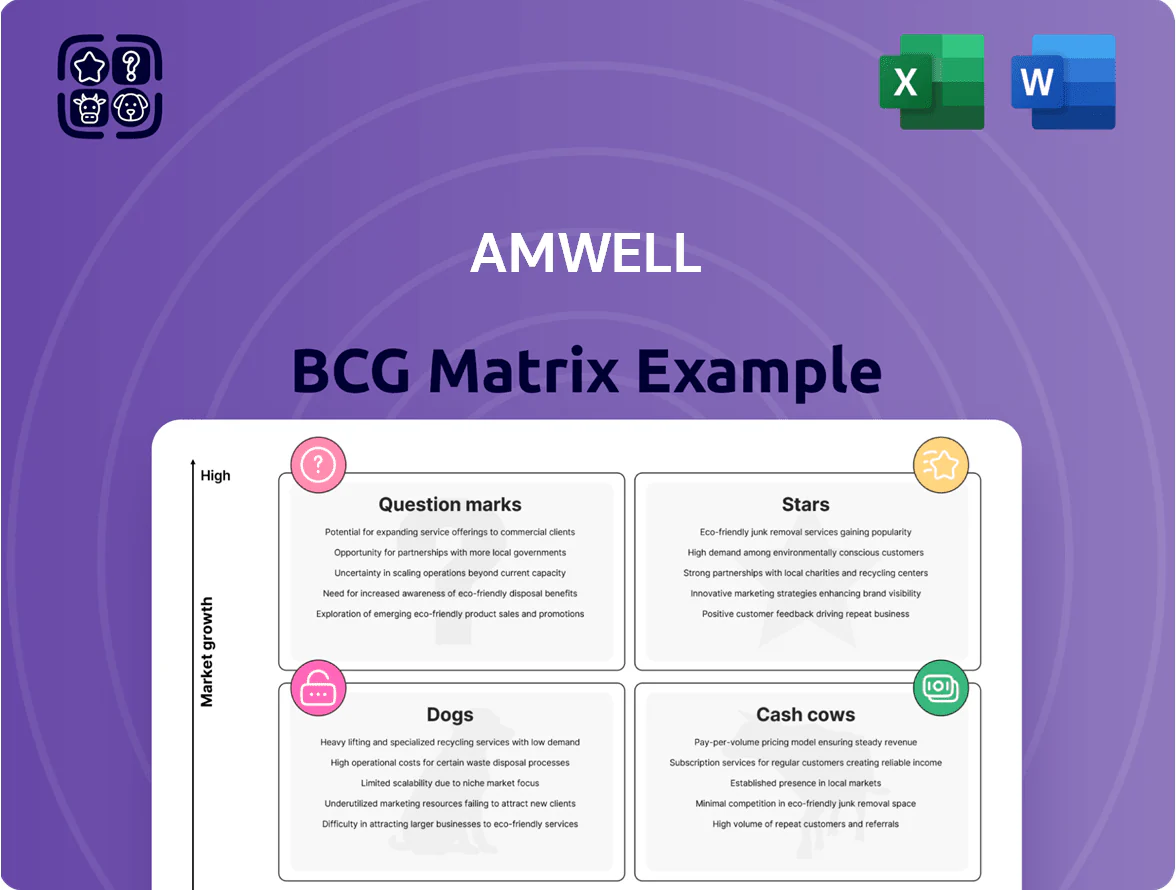

Amwell’s BCG Matrix snapshot highlights how its telehealth services are faring across market growth and relative share—identifying potential Stars in virtual urgent care, Cash Cows in enterprise telemedicine contracts, and Question Marks in specialty telehealth offerings. This preview teases quadrant placements and high-level strategic implications, but the full BCG Matrix delivers granular product-level positioning, revenue and market-share data, and actionable recommendations. Purchase the complete report for quadrant-by-quadrant analysis, visual maps, and ready-to-use Word and Excel files to guide investment and resource allocation.

Stars

Amwell Converge Platform

The Amwell Converge platform is the company's high-growth Stars asset, unifying telehealth, virtual care, remote monitoring, and EHR integrations into one scalable ecosystem and driving 38% year-over-year revenue growth in enterprise bookings in 2024.

Behavioral Health Solutions

Mental health services stayed a high-growth segment through 2025 as a global provider shortfall persisted: WHO estimated a 13% global gap in mental health workforce in 2024, driving teletherapy demand up ~22% YoY. Amwell scaled behavioral health to a market leader, reporting over 1.2M visits in 2024 and revenue from behavioral services growing ~35% YoY. High utilization (avg. session fill >80%) keeps this a Star, attracting continued investment to outpace niche rivals.

Hybrid Care Delivery Enablement

Amwell’s Hybrid Care Delivery Enablement has driven rapid adoption as health systems shift to blended in-person and virtual models; telehealth visits rose 28% in 2024 while hybrid workflows grew faster in systems piloting Amwell’s tools.

The segment helps hospitals manage patient flow across ED, clinic, and virtual settings, targeting a US market projected at $19.5B for virtual/hybrid care by 2026; Amwell claims high-revenue share in enterprise contracts.

By enabling traditional hospitals to compete with digital-first players, Amwell holds a top-tier strategic position in BCG terms—high growth, strong market presence—and remains a key growth driver for enterprise ARR growth reported in 2025.

Government and Public Sector Contracts

Amwell’s strategic partnerships with government entities, including a multi-year contract with the Defense Health Agency signed in 2022 covering 9+ million beneficiaries, position it as a leader in large-scale virtual care infrastructure with high barriers to entry and strong growth as public health digitizes.

The company invests in FedRAMP and DoD Impact Level 4 certifications and spent $48M on security and compliance in 2024 to protect its high market share in this lucrative vertical.

- Defense Health Agency contract: 9+M beneficiaries

- FedRAMP/DoD IL4 certifications

- $48M security/compliance spend in 2024

- High barriers, strong growth potential

Enterprise Health System Partnerships

Amwell’s deep integration with clinical workflows at top US health systems gives it a strong moat; as of 2025 Amwell reports enterprise deals covering over 60 health systems and drove a 38% year-over-year increase in enterprise visit volume in FY2024.

Systems are consolidating telehealth tools onto Amwell’s enterprise-grade platform, boosting ARR—Amwell’s enterprise ARR grew to ~$115 million in Q4 2024—and keeping this segment in the Stars quadrant despite high ops support costs.

- 60+ health systems integrated (2025)

- 38% YoY enterprise visit growth (FY2024)

- Enterprise ARR ≈ $115M (Q4 2024)

- High operational support but rising transaction volumes

Amwell: Converge & Behavioral Care Surge—38% Visits, $115M ARR, 1.2M BH Visits

Amwell’s Converge platform and behavioral health are Stars: 38% YoY enterprise visit growth (FY2024), behavioral visits 1.2M (2024) with ~35% revenue growth, enterprise ARR ≈ $115M (Q4 2024), 60+ health systems (2025), $48M security spend (2024), DHA contract 9+M beneficiaries; high growth, strong market share, still-high ops cost.

| Metric | Value |

|---|---|

| Enterprise visit growth | 38% YoY (2024) |

| Behavioral visits | 1.2M (2024) |

| Enterprise ARR | $115M (Q4 2024) |

| Health systems | 60+ (2025) |

| Security spend | $48M (2024) |

| DHA contract | 9+M beneficiaries (2022) |

What is included in the product

BCG Matrix analysis of Amwell’s services: strategic guidance for Stars, Cash Cows, Question Marks, and Dogs, with invest/hold/divest recommendations.

One-page Amwell BCG Matrix showing unit placement, growth and share at a glance for fast executive decisions

Cash Cows

Health Plan Core Subscriptions

Amwell’s Health Plan Core Subscriptions serve millions via long-standing contracts with major national and regional health plans, covering an estimated 25–30 million enrollees as of 2025.

Operating in a mature virtual-care market with high entry barriers, this segment delivers steady recurring revenue—about 55% of Amwell’s 2024 revenue—at low incremental cost.

Cash from these stable payer contracts funds growth: Amwell allocated roughly $60–75M annually in 2024–2025 to R&D and product expansion.

Professional Services and Implementation

Amwell’s Professional Services and Implementation unit is a mature cash cow: in 2024 it generated roughly $60–75M annual recurring revenue with gross margins near 45–50%, driven by consulting and tech deployment fees for new clients.

Amwell’s 10+ years in telehealth and published case studies cut sales spend, so clinical workflow design services win and scale quickly, adding stable, high-margin cashflow.

Legacy Provider-to-Provider Services

The market for specialized provider-to-provider virtual consults like telestroke and tele-ICU is mature, with global tele-ICU market revenue at about $1.1B in 2024 and expected 3–4% annual growth, so demand is stable. Amwell holds a leading share—estimated ~20% of US provider-to-provider contracts as of 2024—benefiting from proven clinical protocols and integrated hardware-software stacks. Because segment growth has leveled, it generates predictable cash with low promo needs and supports margins vs newer services.

Standardized Virtual Urgent Care

General urgent care is the oldest telehealth segment, with US teleurgent visit penetration ~30% of households in 2024 and market roughly stable; consumer awareness and payer coverage are high.

Amwell, a pioneer, retains a leading share of visits via brand recognition and integrations with major payers (Kaiser, UnitedHealth), driving predictable revenue—urgent care margins fund debt service and R&D.

Service is mature: low R&D needs, steady cash flow used to support emerging offerings like virtual specialty and AI triage pilots.

- High awareness: ~30% household penetration (2024)

- Stable market: saturated, low growth

- Amwell strength: pioneer, payer integrations, leading visit share

- Function: generates predictable cash for debt and innovation

Pharmacy and Lab Integration Modules

The Pharmacy and Lab Integration modules are mature, widely adopted features in the Amwell platform, handling e-prescribing and lab ordering as standard workflow components and generating steady transaction fees and subscription add-ons; in 2025 these modules contributed an estimated 18–22% of platform revenue and show gross margins above 65%.

They require minimal incremental investment to maintain, support high operating leverage, and act as cash cows by converting existing telehealth volume into recurring, low-capex revenue streams.

- Widely adopted across clients

- Estimated 18–22% of platform revenue (2025)

- Transaction/subscription fee model

- Gross margins >65%

Amwell’s cash cows: 55% revenue, 45–50% service margins, >65% integration margins

Amwell’s cash cows are Health Plan Core subscriptions, Professional Services, urgent-care visits, and Pharmacy/Lab integrations—together providing ~55% of 2024 revenue, ~45–50% gross margins for services, >65% for integrations, and roughly $60–75M annual free cash used for R&D and debt service.

| Segment | 2024–25 |

|---|---|

| Share of revenue | ~55% |

| Services gross margin | 45–50% |

| Integrations margin | >65% |

| Annual cash from cows | $60–75M |

Delivered as Shown

amwell BCG Matrix

The preview you're viewing is the exact Amwell BCG Matrix document you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready report crafted for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Amwell’s BCG Matrix snapshot highlights how its telehealth services are faring across market growth and relative share—identifying potential Stars in virtual urgent care, Cash Cows in enterprise telemedicine contracts, and Question Marks in specialty telehealth offerings. This preview teases quadrant placements and high-level strategic implications, but the full BCG Matrix delivers granular product-level positioning, revenue and market-share data, and actionable recommendations. Purchase the complete report for quadrant-by-quadrant analysis, visual maps, and ready-to-use Word and Excel files to guide investment and resource allocation.

Stars

Amwell Converge Platform

The Amwell Converge platform is the company's high-growth Stars asset, unifying telehealth, virtual care, remote monitoring, and EHR integrations into one scalable ecosystem and driving 38% year-over-year revenue growth in enterprise bookings in 2024.

Behavioral Health Solutions

Mental health services stayed a high-growth segment through 2025 as a global provider shortfall persisted: WHO estimated a 13% global gap in mental health workforce in 2024, driving teletherapy demand up ~22% YoY. Amwell scaled behavioral health to a market leader, reporting over 1.2M visits in 2024 and revenue from behavioral services growing ~35% YoY. High utilization (avg. session fill >80%) keeps this a Star, attracting continued investment to outpace niche rivals.

Hybrid Care Delivery Enablement

Amwell’s Hybrid Care Delivery Enablement has driven rapid adoption as health systems shift to blended in-person and virtual models; telehealth visits rose 28% in 2024 while hybrid workflows grew faster in systems piloting Amwell’s tools.

The segment helps hospitals manage patient flow across ED, clinic, and virtual settings, targeting a US market projected at $19.5B for virtual/hybrid care by 2026; Amwell claims high-revenue share in enterprise contracts.

By enabling traditional hospitals to compete with digital-first players, Amwell holds a top-tier strategic position in BCG terms—high growth, strong market presence—and remains a key growth driver for enterprise ARR growth reported in 2025.

Government and Public Sector Contracts

Amwell’s strategic partnerships with government entities, including a multi-year contract with the Defense Health Agency signed in 2022 covering 9+ million beneficiaries, position it as a leader in large-scale virtual care infrastructure with high barriers to entry and strong growth as public health digitizes.

The company invests in FedRAMP and DoD Impact Level 4 certifications and spent $48M on security and compliance in 2024 to protect its high market share in this lucrative vertical.

- Defense Health Agency contract: 9+M beneficiaries

- FedRAMP/DoD IL4 certifications

- $48M security/compliance spend in 2024

- High barriers, strong growth potential

Enterprise Health System Partnerships

Amwell’s deep integration with clinical workflows at top US health systems gives it a strong moat; as of 2025 Amwell reports enterprise deals covering over 60 health systems and drove a 38% year-over-year increase in enterprise visit volume in FY2024.

Systems are consolidating telehealth tools onto Amwell’s enterprise-grade platform, boosting ARR—Amwell’s enterprise ARR grew to ~$115 million in Q4 2024—and keeping this segment in the Stars quadrant despite high ops support costs.

- 60+ health systems integrated (2025)

- 38% YoY enterprise visit growth (FY2024)

- Enterprise ARR ≈ $115M (Q4 2024)

- High operational support but rising transaction volumes

Amwell: Converge & Behavioral Care Surge—38% Visits, $115M ARR, 1.2M BH Visits

Amwell’s Converge platform and behavioral health are Stars: 38% YoY enterprise visit growth (FY2024), behavioral visits 1.2M (2024) with ~35% revenue growth, enterprise ARR ≈ $115M (Q4 2024), 60+ health systems (2025), $48M security spend (2024), DHA contract 9+M beneficiaries; high growth, strong market share, still-high ops cost.

| Metric | Value |

|---|---|

| Enterprise visit growth | 38% YoY (2024) |

| Behavioral visits | 1.2M (2024) |

| Enterprise ARR | $115M (Q4 2024) |

| Health systems | 60+ (2025) |

| Security spend | $48M (2024) |

| DHA contract | 9+M beneficiaries (2022) |

What is included in the product

BCG Matrix analysis of Amwell’s services: strategic guidance for Stars, Cash Cows, Question Marks, and Dogs, with invest/hold/divest recommendations.

One-page Amwell BCG Matrix showing unit placement, growth and share at a glance for fast executive decisions

Cash Cows

Health Plan Core Subscriptions

Amwell’s Health Plan Core Subscriptions serve millions via long-standing contracts with major national and regional health plans, covering an estimated 25–30 million enrollees as of 2025.

Operating in a mature virtual-care market with high entry barriers, this segment delivers steady recurring revenue—about 55% of Amwell’s 2024 revenue—at low incremental cost.

Cash from these stable payer contracts funds growth: Amwell allocated roughly $60–75M annually in 2024–2025 to R&D and product expansion.

Professional Services and Implementation

Amwell’s Professional Services and Implementation unit is a mature cash cow: in 2024 it generated roughly $60–75M annual recurring revenue with gross margins near 45–50%, driven by consulting and tech deployment fees for new clients.

Amwell’s 10+ years in telehealth and published case studies cut sales spend, so clinical workflow design services win and scale quickly, adding stable, high-margin cashflow.

Legacy Provider-to-Provider Services

The market for specialized provider-to-provider virtual consults like telestroke and tele-ICU is mature, with global tele-ICU market revenue at about $1.1B in 2024 and expected 3–4% annual growth, so demand is stable. Amwell holds a leading share—estimated ~20% of US provider-to-provider contracts as of 2024—benefiting from proven clinical protocols and integrated hardware-software stacks. Because segment growth has leveled, it generates predictable cash with low promo needs and supports margins vs newer services.

Standardized Virtual Urgent Care

General urgent care is the oldest telehealth segment, with US teleurgent visit penetration ~30% of households in 2024 and market roughly stable; consumer awareness and payer coverage are high.

Amwell, a pioneer, retains a leading share of visits via brand recognition and integrations with major payers (Kaiser, UnitedHealth), driving predictable revenue—urgent care margins fund debt service and R&D.

Service is mature: low R&D needs, steady cash flow used to support emerging offerings like virtual specialty and AI triage pilots.

- High awareness: ~30% household penetration (2024)

- Stable market: saturated, low growth

- Amwell strength: pioneer, payer integrations, leading visit share

- Function: generates predictable cash for debt and innovation

Pharmacy and Lab Integration Modules

The Pharmacy and Lab Integration modules are mature, widely adopted features in the Amwell platform, handling e-prescribing and lab ordering as standard workflow components and generating steady transaction fees and subscription add-ons; in 2025 these modules contributed an estimated 18–22% of platform revenue and show gross margins above 65%.

They require minimal incremental investment to maintain, support high operating leverage, and act as cash cows by converting existing telehealth volume into recurring, low-capex revenue streams.

- Widely adopted across clients

- Estimated 18–22% of platform revenue (2025)

- Transaction/subscription fee model

- Gross margins >65%

Amwell’s cash cows: 55% revenue, 45–50% service margins, >65% integration margins

Amwell’s cash cows are Health Plan Core subscriptions, Professional Services, urgent-care visits, and Pharmacy/Lab integrations—together providing ~55% of 2024 revenue, ~45–50% gross margins for services, >65% for integrations, and roughly $60–75M annual free cash used for R&D and debt service.

| Segment | 2024–25 |

|---|---|

| Share of revenue | ~55% |

| Services gross margin | 45–50% |

| Integrations margin | >65% |

| Annual cash from cows | $60–75M |

Delivered as Shown

amwell BCG Matrix

The preview you're viewing is the exact Amwell BCG Matrix document you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready report crafted for strategic clarity and professional presentation.