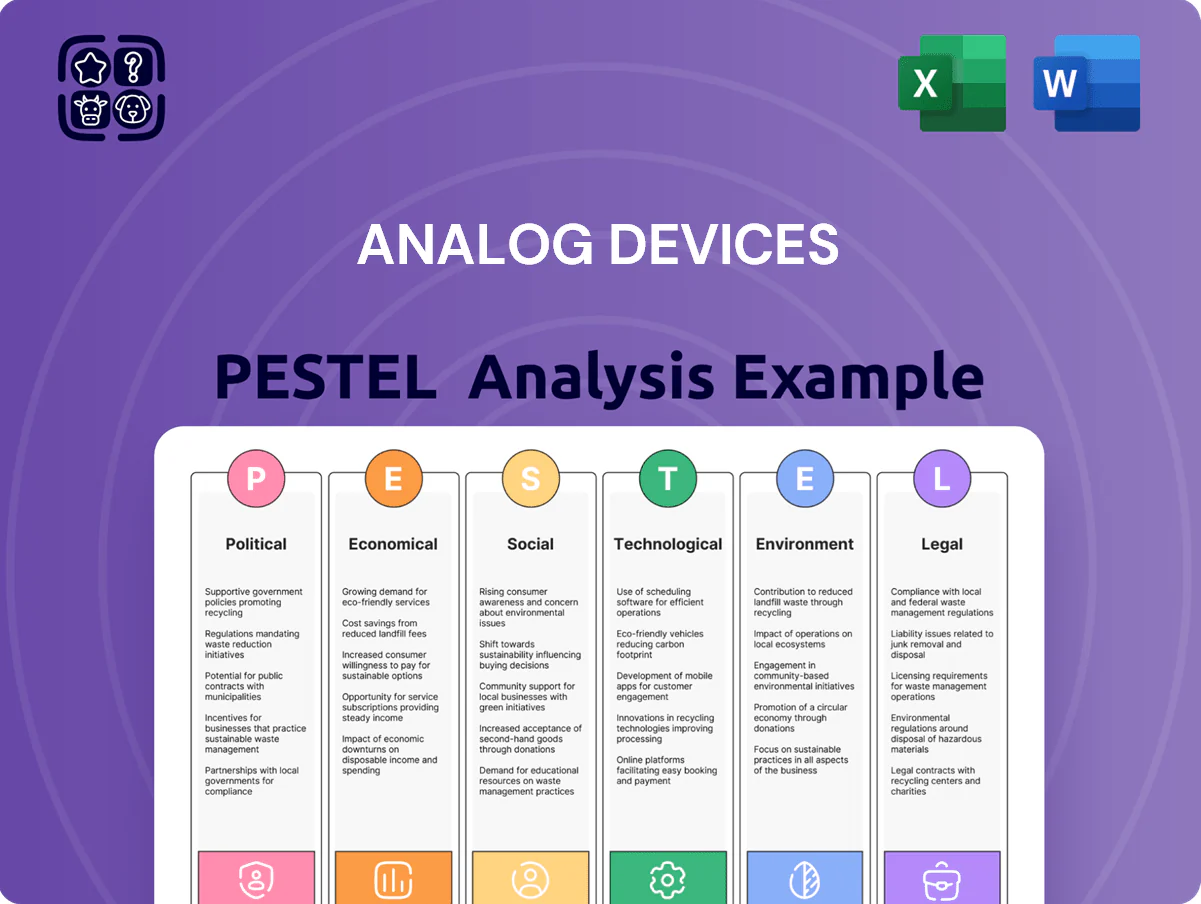

Analog Devices PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and rapid technological change are reshaping Analog Devices’ competitive landscape—our concise PESTLE snapshot highlights key external risks and opportunities. Buy the full PESTLE analysis to unlock detailed, actionable insights and ready-to-use slides that inform investment decisions and strategic planning. Download now for the complete, editable report.

Political factors

US-China Trade Restrictions

The US-China trade tensions have led to stricter export controls on high-performance analog and mixed-signal components, forcing Analog Devices to secure complex licenses to ship advanced products to China, which accounted for about 22% of ADI’s FY2025 revenue (~$1.9B of $8.7B). These controls drive supply-chain bifurcation and higher compliance costs, prompting ADI to pursue localized manufacturing and dual-sourcing in APAC to protect market share and revenue stability.

CHIPS and Science Act Incentives

Geopolitical Stability in Manufacturing Hubs

Analog Devices depends on specialized foundries and assembly partners in politically sensitive regions such as Taiwan and Southeast Asia, where Taiwan accounts for roughly 20–25% of global wafer fabrication capacity and Southeast Asia hosts significant OSAT capacity; disruptions there could sharply constrain supply. Any escalation in regional conflicts risks interrupting wafer supply and finished IC shipments, potentially delaying deliveries to ADI’s $11.3B 2025 revenue base. Maintaining diversified geographic operations and dual-sourcing strategies remains a strategic priority to mitigate localized political unrest or territorial disputes affecting production continuity.

Global Protectionist Policies

Countries worldwide are implementing semiconductor sovereignty measures; by 2025 over 20 nations had announced incentives or mandates, pushing Analog Devices to work with multiple regulators to meet local content and manufacturing rules.

Compliance raises operating costs—capex for regional fabs and supply-chain shifts—yet offers ADI opportunities to win regional contracts and increase FY2025 revenue exposure in targeted markets.

- 20+ countries with sovereignty policies by 2025

- Higher capex and compliance costs vs regional market access

- Opportunity: deeper integration into local industrial ecosystems

Government Defense Spending

Analog Devices is a key supplier to aerospace and defense, so its revenue is sensitive to US defense budgets—FY2025 DoD base budget was about $842 billion, influencing procurement cycles and contract timing.

Rising focus on electronic warfare, secure comms, and advanced radar boosts demand for ADI high-reliability signal processors; defense semiconductor content per platform has risen an estimated 10–15% YoY in recent defense procurements.

Shifts in administration or military priorities can materially affect long-term contracts and R&D funding, causing revenue volatility given ADI’s exposure to multi-year defense programs.

- FY2025 DoD base budget ~ $842B

- Defense semiconductor content growth ~10–15% YoY

- Revenue sensitivity linked to multi-year contracts and procurement cycles

Geopolitics, CHIPS cash & defense spend reshape ADI: China exposure, capex & market gains

Political risks—US-China export controls (China ~22% of ADI FY2025 revenue ~$1.9B), CHIPS Act incentives (~$52B national fund) boosting ADI capex (FY2024 capex $1.6B), Taiwan/SE Asia supply sensitivity (Taiwan ~20–25% global fab capacity), and FY2025 DoD budget ~$842B—drive higher compliance costs, localized investment, and defense market opportunity.

| Metric | Value |

|---|---|

| China revenue share FY2025 | ~22% ($1.9B) |

| FY2024 capex | $1.6B |

| CHIPS Act funding | ~$52B |

| FY2025 DoD budget | $842B |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Analog Devices, linking each dimension to industry data and regional market dynamics to highlight risks and growth levers.

A concise, visually segmented PESTLE snapshot for Analog Devices that streamlines external risk assessment and market-position discussions during meetings or presentations.

Economic factors

Industrial Sector Cyclicality

The demand for Analog Devices analog ICs tracks global industrial activity; industrial electronics accounted for about 28% of ADI’s FY2025 revenue, so a 2023–24 manufacturing slowdown triggered inventory corrections and reduced order visibility, with industrial revenue down ~6% YoY in FY2024. Conversely, industrial capex recovery and investments in smart sensors and power management—projected 4–6% CAGR in industrial automation through 2026—drive strong upside.

Automotive Electrification Demand

Demand for EV-related systems drives Analog Devices, with automotive revenue up 12% in FY2025 to about $2.8B, supported by BMS and cabin-electronics content growth as EV global sales hit 14.1M units in 2024 (up ~40% y/y).

Higher interest rates and softer luxury EV purchases cooled 2024 US EV sales growth vs. 2023, risking near-term capital-spend delays in this high-ticket segment.

Long-term EV and autonomy forecasts—IEA projecting 400M EVs by 2040 under stated policies—create stable baseline semiconductor demand, benefiting ADI’s specialized analog/AD-conversion products.

Interest Rate Sensitivity

Higher global interest rates—US Fed funds at 5.25–5.50% in 2024—tighten capex for Analog Devices’ communications and industrial customers, with 2024 telecom capex growth forecast cut to ~2–3% vs prior double digits. Elevated borrowing costs can delay 5G rollouts and factory overhauls, reducing near-term demand for ADCs and RF ICs. ADI must preserve liquidity—cash and equivalents of $3.1B (FY2024)—and push high-value, fast-ROI solutions to sustain orders.

Currency Exchange Volatility

As a global firm with ~60% of revenue from outside the US, Analog Devices is exposed to USD/EUR/JPY swings; the dollar strengthened ~8% vs. euro and ~10% vs. yen in 2022–2024, pressuring international pricing and competitiveness.

Management employs hedging—forward contracts and currency swaps—to smooth FX impact, but ADI reported FX headwinds reducing FY2024 revenue growth by ~1–2 percentage points and compressing gross margin by ~30–60 basis points.

- ~60% revenue outside US

- USD up ~8% vs EUR, ~10% vs JPY (2022–24)

- Hedging used; FY2024 FX reduced revenue growth ~1–2 ppt

- Gross margin hit ~30–60 bps from FX

Inflationary Pressure on Inputs

- Input inflation ~8–10% y/y in 2024

- ADI FY2024 gross margin 64.2%

- Tech wage growth ~6–7% in 2024

- Mitigation: efficiency, pricing, yield

ADI gains from industrial & $2.8B automotive amid FX headwinds and 64.2% margin

Global industrial and automotive demand drives ADI—industrial was ~28% of FY2025 revenue; automotive ~$2.8B (FY2025). FX headwinds (USD up ~8% vs EUR, ~10% vs JPY, 2022–24) cut FY2024 revenue growth ~1–2ppt and gross margin ~30–60bps. Input inflation ~8–10% in 2024 pressured COGS; FY2024 gross margin 64.2%; cash $3.1B.

| Metric | Value |

|---|---|

| Industrial mix | ~28% |

| Automotive rev FY2025 | $2.8B |

| USD moves (22–24) | +8% vs EUR, +10% vs JPY |

| Input inflation 2024 | 8–10% |

| FY2024 gross margin | 64.2% |

| Cash (FY2024) | $3.1B |

What You See Is What You Get

Analog Devices PESTLE Analysis

The preview shown here is the exact Analog Devices PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and rapid technological change are reshaping Analog Devices’ competitive landscape—our concise PESTLE snapshot highlights key external risks and opportunities. Buy the full PESTLE analysis to unlock detailed, actionable insights and ready-to-use slides that inform investment decisions and strategic planning. Download now for the complete, editable report.

Political factors

US-China Trade Restrictions

The US-China trade tensions have led to stricter export controls on high-performance analog and mixed-signal components, forcing Analog Devices to secure complex licenses to ship advanced products to China, which accounted for about 22% of ADI’s FY2025 revenue (~$1.9B of $8.7B). These controls drive supply-chain bifurcation and higher compliance costs, prompting ADI to pursue localized manufacturing and dual-sourcing in APAC to protect market share and revenue stability.

CHIPS and Science Act Incentives

Geopolitical Stability in Manufacturing Hubs

Analog Devices depends on specialized foundries and assembly partners in politically sensitive regions such as Taiwan and Southeast Asia, where Taiwan accounts for roughly 20–25% of global wafer fabrication capacity and Southeast Asia hosts significant OSAT capacity; disruptions there could sharply constrain supply. Any escalation in regional conflicts risks interrupting wafer supply and finished IC shipments, potentially delaying deliveries to ADI’s $11.3B 2025 revenue base. Maintaining diversified geographic operations and dual-sourcing strategies remains a strategic priority to mitigate localized political unrest or territorial disputes affecting production continuity.

Global Protectionist Policies

Countries worldwide are implementing semiconductor sovereignty measures; by 2025 over 20 nations had announced incentives or mandates, pushing Analog Devices to work with multiple regulators to meet local content and manufacturing rules.

Compliance raises operating costs—capex for regional fabs and supply-chain shifts—yet offers ADI opportunities to win regional contracts and increase FY2025 revenue exposure in targeted markets.

- 20+ countries with sovereignty policies by 2025

- Higher capex and compliance costs vs regional market access

- Opportunity: deeper integration into local industrial ecosystems

Government Defense Spending

Analog Devices is a key supplier to aerospace and defense, so its revenue is sensitive to US defense budgets—FY2025 DoD base budget was about $842 billion, influencing procurement cycles and contract timing.

Rising focus on electronic warfare, secure comms, and advanced radar boosts demand for ADI high-reliability signal processors; defense semiconductor content per platform has risen an estimated 10–15% YoY in recent defense procurements.

Shifts in administration or military priorities can materially affect long-term contracts and R&D funding, causing revenue volatility given ADI’s exposure to multi-year defense programs.

- FY2025 DoD base budget ~ $842B

- Defense semiconductor content growth ~10–15% YoY

- Revenue sensitivity linked to multi-year contracts and procurement cycles

Geopolitics, CHIPS cash & defense spend reshape ADI: China exposure, capex & market gains

Political risks—US-China export controls (China ~22% of ADI FY2025 revenue ~$1.9B), CHIPS Act incentives (~$52B national fund) boosting ADI capex (FY2024 capex $1.6B), Taiwan/SE Asia supply sensitivity (Taiwan ~20–25% global fab capacity), and FY2025 DoD budget ~$842B—drive higher compliance costs, localized investment, and defense market opportunity.

| Metric | Value |

|---|---|

| China revenue share FY2025 | ~22% ($1.9B) |

| FY2024 capex | $1.6B |

| CHIPS Act funding | ~$52B |

| FY2025 DoD budget | $842B |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Analog Devices, linking each dimension to industry data and regional market dynamics to highlight risks and growth levers.

A concise, visually segmented PESTLE snapshot for Analog Devices that streamlines external risk assessment and market-position discussions during meetings or presentations.

Economic factors

Industrial Sector Cyclicality

The demand for Analog Devices analog ICs tracks global industrial activity; industrial electronics accounted for about 28% of ADI’s FY2025 revenue, so a 2023–24 manufacturing slowdown triggered inventory corrections and reduced order visibility, with industrial revenue down ~6% YoY in FY2024. Conversely, industrial capex recovery and investments in smart sensors and power management—projected 4–6% CAGR in industrial automation through 2026—drive strong upside.

Automotive Electrification Demand

Demand for EV-related systems drives Analog Devices, with automotive revenue up 12% in FY2025 to about $2.8B, supported by BMS and cabin-electronics content growth as EV global sales hit 14.1M units in 2024 (up ~40% y/y).

Higher interest rates and softer luxury EV purchases cooled 2024 US EV sales growth vs. 2023, risking near-term capital-spend delays in this high-ticket segment.

Long-term EV and autonomy forecasts—IEA projecting 400M EVs by 2040 under stated policies—create stable baseline semiconductor demand, benefiting ADI’s specialized analog/AD-conversion products.

Interest Rate Sensitivity

Higher global interest rates—US Fed funds at 5.25–5.50% in 2024—tighten capex for Analog Devices’ communications and industrial customers, with 2024 telecom capex growth forecast cut to ~2–3% vs prior double digits. Elevated borrowing costs can delay 5G rollouts and factory overhauls, reducing near-term demand for ADCs and RF ICs. ADI must preserve liquidity—cash and equivalents of $3.1B (FY2024)—and push high-value, fast-ROI solutions to sustain orders.

Currency Exchange Volatility

As a global firm with ~60% of revenue from outside the US, Analog Devices is exposed to USD/EUR/JPY swings; the dollar strengthened ~8% vs. euro and ~10% vs. yen in 2022–2024, pressuring international pricing and competitiveness.

Management employs hedging—forward contracts and currency swaps—to smooth FX impact, but ADI reported FX headwinds reducing FY2024 revenue growth by ~1–2 percentage points and compressing gross margin by ~30–60 basis points.

- ~60% revenue outside US

- USD up ~8% vs EUR, ~10% vs JPY (2022–24)

- Hedging used; FY2024 FX reduced revenue growth ~1–2 ppt

- Gross margin hit ~30–60 bps from FX

Inflationary Pressure on Inputs

- Input inflation ~8–10% y/y in 2024

- ADI FY2024 gross margin 64.2%

- Tech wage growth ~6–7% in 2024

- Mitigation: efficiency, pricing, yield

ADI gains from industrial & $2.8B automotive amid FX headwinds and 64.2% margin

Global industrial and automotive demand drives ADI—industrial was ~28% of FY2025 revenue; automotive ~$2.8B (FY2025). FX headwinds (USD up ~8% vs EUR, ~10% vs JPY, 2022–24) cut FY2024 revenue growth ~1–2ppt and gross margin ~30–60bps. Input inflation ~8–10% in 2024 pressured COGS; FY2024 gross margin 64.2%; cash $3.1B.

| Metric | Value |

|---|---|

| Industrial mix | ~28% |

| Automotive rev FY2025 | $2.8B |

| USD moves (22–24) | +8% vs EUR, +10% vs JPY |

| Input inflation 2024 | 8–10% |

| FY2024 gross margin | 64.2% |

| Cash (FY2024) | $3.1B |

What You See Is What You Get

Analog Devices PESTLE Analysis

The preview shown here is the exact Analog Devices PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.