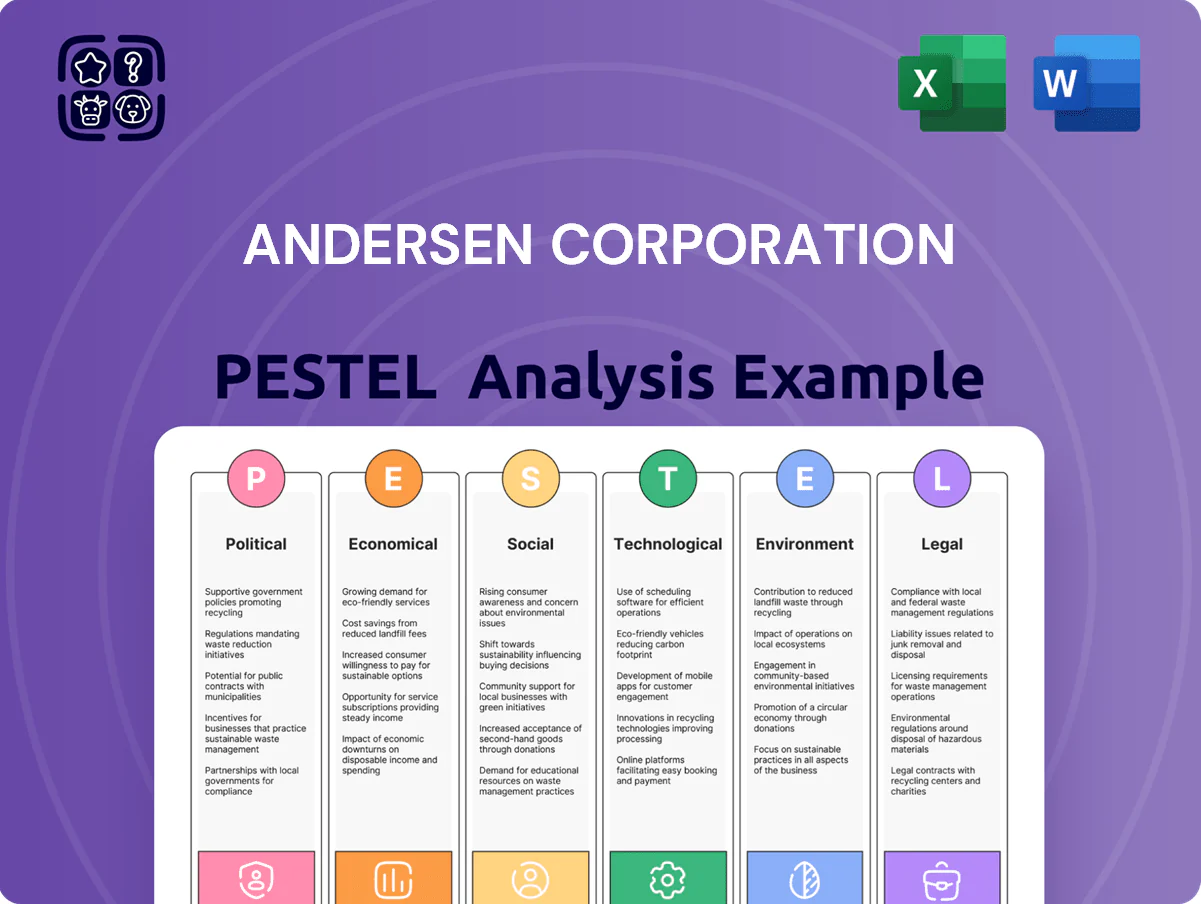

Andersen Corporation PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and evolving tech and environmental trends are reshaping Andersen Corporation’s market position—our concise PESTLE highlights immediate risks and opportunities to inform smarter strategy and investment calls; purchase the full analysis for a complete, editable report and actionable insights you can use right away.

Political factors

Trade Tariffs and Material Costs

Trade tariffs on imported glass and aluminum can raise Andersen Corporation's COGS materially; US tariffs added in 2024 increased aluminum import costs by about 12%, raising industry inputs; by late 2025 geopolitical shifts have caused spot aluminum prices to swing ~18% YoY and glass import premiums to widen, stressing margins; proactive sourcing and renegotiated supply contracts are vital to preserve competitive North American pricing.

Federal Housing Incentives

Federal tax credits for energy-efficient renovations, bolstered by the Inflation Reduction Act, have increased demand for premium windows—residential retrofit spending rose 6.4% in 2024, supporting a US window market estimated at $24.8B. Andersen must ensure products meet evolving federal energy standards (e.g., DOE/ENERGY STAR criteria) to keep customers eligible for incentives. Policy stability of these subsidies directly influences remodeling activity and consumer purchasing power.

Labor Market Regulations

Rising federal/state minimums and union drives raise Andersen Corporation’s labor costs, with 2024 median US manufacturing hourly wages at about $25.50 and several states hiking minimums to $15–$16, increasing manufacturing overhead and unit labor cost pressure.

Operating across multiple states, Andersen must adapt HR policies and scheduling to diverse rules—over 20% of its workforce in union-prone regions—reducing operational flexibility.

Strict compliance with evolving standards is essential to avoid lawsuits and downtime; labor disputes in 2023–24 cost US manufacturers an estimated $3.5 billion in lost output, underscoring production risk.

International Market Access

Diplomatic relations between the United States and partners like Canada, Mexico and the EU influence Andersen Corporation’s export logistics and market entry; US goods exports to these regions totaled about $1.5 trillion in 2024, affecting cross-border construction supply chains.

Export regulations and foreign investment rules shape Andersen’s access to emerging markets—US outward FDI flows were $424 billion in 2024—impacting joint ventures and manufacturing footprint decisions.

Navigating geopolitical tensions, such as supply-chain disruptions that raised global shipping costs ~20% in 2023–24, is vital to secure long-term growth and reduce volatility risks.

- Dependence on US diplomatic ties with major partners

- Export rules and FDI policy constrain market entry

- Geopolitical risks increase shipping and supply-chain costs (~20% rise)

Infrastructure Development Policies

Local zoning laws and the $1.2 trillion 2021 Bipartisan Infrastructure Law funding and continued FY2025 federal infrastructure allocations shape demand for Andersen’s residential and commercial windows, favoring retrofit and new-build products in growth markets.

Rising political emphasis on sustainable urban development—cities targeting 50–70% emissions reductions by 2030—boosts demand for high-performance, high-density fenestration solutions with superior U-values and embodied carbon reductions.

Andersen must proactively engage policymakers and planning bodies to anticipate zoning changes, green building codes, and tax incentives that will drive product specs and procurement in the next 3–5 years.

- Federal infrastructure funding: $1.2T (BIL) plus FY2025 allocations

- Urban emissions targets: 50–70% reductions by 2030 in key metros

- Market shift: higher demand for low-U-value, low-carbon window systems

- Action: active policy engagement to influence codes and procurement

Tariffs, wages and $1.2T infrastructure fuel window retrofits amid 18% price swings

Political risks: tariffs raised aluminum costs ~12% (2024) and spot swings ~18% YoY (2025); federal energy-efficiency credits lifted retrofit demand (+6.4% in 2024; US window market $24.8B); labor cost pressure (median mfg wage $25.50/hr, min wages $15–16); infrastructure funding $1.2T (BIL) + FY2025 allocations driving retrofit/new-build demand.

| Metric | Value |

|---|---|

| Aluminum tariff impact | +12% (2024) |

| Spot price volatility | ~18% YoY (2025) |

| Retrofit growth | +6.4% (2024) |

| US window market | $24.8B (2024) |

| Median mfg wage | $25.50/hr (2024) |

| Infrastructure funding | $1.2T (BIL) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Andersen Corporation across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trend-based insights to identify threats and opportunities for executives and investors.

A concise Andersen Corporation PESTLE summary that’s visually segmented for quick reference, easing meeting prep and presentation use while enabling note additions for region- or business-specific context.

Economic factors

Interest Rate Fluctuations

High mortgage rates at the end of 2025—around 7.1% for a 30-year fixed mortgage—dampened new home starts by about 10% year-over-year, steering Andersen toward renovation demand where the company saw aftermarket sales grow roughly 6% in 2025.

As borrowing costs fluctuate, Andersen must renegotiate dealer floorplan financing and consumer loan partnerships; in 2025 it expanded captive and third-party financing options after average APRs rose 150–200 basis points.

The overall health of the U.S. residential real estate market, with existing-home sales down ~8% in 2025, remains the primary revenue driver, making housing activity the key determinant of Andersen’s growth trajectory.

Raw Material Inflation

Persistent inflation in raw materials such as lumber, vinyl and specialty polymers compressed Andersen Corporation’s gross margin, with lumber costs rising about 18% in 2024 and polymer prices up roughly 12% year-over-year, pressuring pricing strategies in the premium window and door segment.

Andersen mitigates volatility via hedging programs and multi-year supplier contracts covering roughly 40–50% of key inputs, reducing exposure to spot-market swings.

Ongoing cost management—including supplier diversification and operational efficiencies—is essential to sustain target EBITDA margins near historical 12–14% levels and protect premium positioning.

Disposable Income Levels

Fluctuations in US disposable personal income—which rose 3.1% year‑over‑year in 2024 Q3 but remains 1.8% below pre‑COVID trend—directly affect demand for luxury remodels; Andersen’s high‑end A‑Series sales are sensitive to these shifts. In 2023–24 economic soft patches, homeowners deferred nonessential upgrades, pressuring premium margins. Andersen monitors CPI, personal saving rate (3.5% in 2024 Q3) and regional income data to forecast demand and optimize inventory across its distribution network.

Global Supply Chain Costs

Global logistics and shipping costs remain a variable factor for Andersen, with global container rates fluctuating 40-60% year-over-year during 2023-2024 and bunker fuel surging ~30% in 2024, raising landed costs for imported components.

Disruptions in Suez/Red Sea routes and energy price spikes in 2024 increased transit times and raised landed costs by an estimated 5-8% for affected shipments.

Andersen invests in logistics optimization and nearshoring; domestic sourcing rose to ~55% of procurement in 2024 to reduce exposure and stabilize delivery costs.

- Container rate volatility 40-60% (2023-24)

- Bunker fuel +30% (2024)

- Landed cost impact +5-8% during disruptions

- Domestic sourcing ~55% of procurement (2024)

Skilled Labor Availability

The availability of skilled construction labor directly affects Andersen Corporation’s installation pace and sales velocity; a 2024 NAHB report found 61% of builders cite labor shortages as a top constraint, slowing product turnarounds and extending sales cycles.

Shortages of qualified contractors create bottlenecks even when window demand is strong—Andersen’s channel data showed installation lead times rose ~18% in 2023 in tight labor markets.

Andersen funds training and certification programs to expand a network of installers for its complex architectural systems, supporting workforce development and reducing installation delays.

- 61% of builders report labor shortages (NAHB 2024)

- Installation lead times up ~18% in 2023

- Company-sponsored training expands certified installer network

High rates curb new construction, boost renovations as input costs squeeze margins

High mortgage rates (~7.1% 30‑yr, 2025) cut new starts ~10% YoY, boosting renovation sales (~+6% 2025); input inflation (lumber +18% 2024, polymers +12% 2024) compressed gross margins; supplier hedges cover ~45% of inputs and domestic sourcing ~55% (2024) to limit landed‑cost volatility (container rates ±40–60%, bunker +30% 2024); labor shortages (61% builders, NAHB 2024) raised installation times ~18%.

| Metric | Value |

|---|---|

| 30‑yr rate (2025) | ~7.1% |

| New starts change | -10% YoY |

| Lumber (2024) | +18% |

| Hedged inputs | ~45% |

Full Version Awaits

Andersen Corporation PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, and it contains a concise PESTLE analysis of Andersen Corporation covering political, economic, social, technological, legal, and environmental factors relevant to its market and operations.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and evolving tech and environmental trends are reshaping Andersen Corporation’s market position—our concise PESTLE highlights immediate risks and opportunities to inform smarter strategy and investment calls; purchase the full analysis for a complete, editable report and actionable insights you can use right away.

Political factors

Trade Tariffs and Material Costs

Trade tariffs on imported glass and aluminum can raise Andersen Corporation's COGS materially; US tariffs added in 2024 increased aluminum import costs by about 12%, raising industry inputs; by late 2025 geopolitical shifts have caused spot aluminum prices to swing ~18% YoY and glass import premiums to widen, stressing margins; proactive sourcing and renegotiated supply contracts are vital to preserve competitive North American pricing.

Federal Housing Incentives

Federal tax credits for energy-efficient renovations, bolstered by the Inflation Reduction Act, have increased demand for premium windows—residential retrofit spending rose 6.4% in 2024, supporting a US window market estimated at $24.8B. Andersen must ensure products meet evolving federal energy standards (e.g., DOE/ENERGY STAR criteria) to keep customers eligible for incentives. Policy stability of these subsidies directly influences remodeling activity and consumer purchasing power.

Labor Market Regulations

Rising federal/state minimums and union drives raise Andersen Corporation’s labor costs, with 2024 median US manufacturing hourly wages at about $25.50 and several states hiking minimums to $15–$16, increasing manufacturing overhead and unit labor cost pressure.

Operating across multiple states, Andersen must adapt HR policies and scheduling to diverse rules—over 20% of its workforce in union-prone regions—reducing operational flexibility.

Strict compliance with evolving standards is essential to avoid lawsuits and downtime; labor disputes in 2023–24 cost US manufacturers an estimated $3.5 billion in lost output, underscoring production risk.

International Market Access

Diplomatic relations between the United States and partners like Canada, Mexico and the EU influence Andersen Corporation’s export logistics and market entry; US goods exports to these regions totaled about $1.5 trillion in 2024, affecting cross-border construction supply chains.

Export regulations and foreign investment rules shape Andersen’s access to emerging markets—US outward FDI flows were $424 billion in 2024—impacting joint ventures and manufacturing footprint decisions.

Navigating geopolitical tensions, such as supply-chain disruptions that raised global shipping costs ~20% in 2023–24, is vital to secure long-term growth and reduce volatility risks.

- Dependence on US diplomatic ties with major partners

- Export rules and FDI policy constrain market entry

- Geopolitical risks increase shipping and supply-chain costs (~20% rise)

Infrastructure Development Policies

Local zoning laws and the $1.2 trillion 2021 Bipartisan Infrastructure Law funding and continued FY2025 federal infrastructure allocations shape demand for Andersen’s residential and commercial windows, favoring retrofit and new-build products in growth markets.

Rising political emphasis on sustainable urban development—cities targeting 50–70% emissions reductions by 2030—boosts demand for high-performance, high-density fenestration solutions with superior U-values and embodied carbon reductions.

Andersen must proactively engage policymakers and planning bodies to anticipate zoning changes, green building codes, and tax incentives that will drive product specs and procurement in the next 3–5 years.

- Federal infrastructure funding: $1.2T (BIL) plus FY2025 allocations

- Urban emissions targets: 50–70% reductions by 2030 in key metros

- Market shift: higher demand for low-U-value, low-carbon window systems

- Action: active policy engagement to influence codes and procurement

Tariffs, wages and $1.2T infrastructure fuel window retrofits amid 18% price swings

Political risks: tariffs raised aluminum costs ~12% (2024) and spot swings ~18% YoY (2025); federal energy-efficiency credits lifted retrofit demand (+6.4% in 2024; US window market $24.8B); labor cost pressure (median mfg wage $25.50/hr, min wages $15–16); infrastructure funding $1.2T (BIL) + FY2025 allocations driving retrofit/new-build demand.

| Metric | Value |

|---|---|

| Aluminum tariff impact | +12% (2024) |

| Spot price volatility | ~18% YoY (2025) |

| Retrofit growth | +6.4% (2024) |

| US window market | $24.8B (2024) |

| Median mfg wage | $25.50/hr (2024) |

| Infrastructure funding | $1.2T (BIL) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Andersen Corporation across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trend-based insights to identify threats and opportunities for executives and investors.

A concise Andersen Corporation PESTLE summary that’s visually segmented for quick reference, easing meeting prep and presentation use while enabling note additions for region- or business-specific context.

Economic factors

Interest Rate Fluctuations

High mortgage rates at the end of 2025—around 7.1% for a 30-year fixed mortgage—dampened new home starts by about 10% year-over-year, steering Andersen toward renovation demand where the company saw aftermarket sales grow roughly 6% in 2025.

As borrowing costs fluctuate, Andersen must renegotiate dealer floorplan financing and consumer loan partnerships; in 2025 it expanded captive and third-party financing options after average APRs rose 150–200 basis points.

The overall health of the U.S. residential real estate market, with existing-home sales down ~8% in 2025, remains the primary revenue driver, making housing activity the key determinant of Andersen’s growth trajectory.

Raw Material Inflation

Persistent inflation in raw materials such as lumber, vinyl and specialty polymers compressed Andersen Corporation’s gross margin, with lumber costs rising about 18% in 2024 and polymer prices up roughly 12% year-over-year, pressuring pricing strategies in the premium window and door segment.

Andersen mitigates volatility via hedging programs and multi-year supplier contracts covering roughly 40–50% of key inputs, reducing exposure to spot-market swings.

Ongoing cost management—including supplier diversification and operational efficiencies—is essential to sustain target EBITDA margins near historical 12–14% levels and protect premium positioning.

Disposable Income Levels

Fluctuations in US disposable personal income—which rose 3.1% year‑over‑year in 2024 Q3 but remains 1.8% below pre‑COVID trend—directly affect demand for luxury remodels; Andersen’s high‑end A‑Series sales are sensitive to these shifts. In 2023–24 economic soft patches, homeowners deferred nonessential upgrades, pressuring premium margins. Andersen monitors CPI, personal saving rate (3.5% in 2024 Q3) and regional income data to forecast demand and optimize inventory across its distribution network.

Global Supply Chain Costs

Global logistics and shipping costs remain a variable factor for Andersen, with global container rates fluctuating 40-60% year-over-year during 2023-2024 and bunker fuel surging ~30% in 2024, raising landed costs for imported components.

Disruptions in Suez/Red Sea routes and energy price spikes in 2024 increased transit times and raised landed costs by an estimated 5-8% for affected shipments.

Andersen invests in logistics optimization and nearshoring; domestic sourcing rose to ~55% of procurement in 2024 to reduce exposure and stabilize delivery costs.

- Container rate volatility 40-60% (2023-24)

- Bunker fuel +30% (2024)

- Landed cost impact +5-8% during disruptions

- Domestic sourcing ~55% of procurement (2024)

Skilled Labor Availability

The availability of skilled construction labor directly affects Andersen Corporation’s installation pace and sales velocity; a 2024 NAHB report found 61% of builders cite labor shortages as a top constraint, slowing product turnarounds and extending sales cycles.

Shortages of qualified contractors create bottlenecks even when window demand is strong—Andersen’s channel data showed installation lead times rose ~18% in 2023 in tight labor markets.

Andersen funds training and certification programs to expand a network of installers for its complex architectural systems, supporting workforce development and reducing installation delays.

- 61% of builders report labor shortages (NAHB 2024)

- Installation lead times up ~18% in 2023

- Company-sponsored training expands certified installer network

High rates curb new construction, boost renovations as input costs squeeze margins

High mortgage rates (~7.1% 30‑yr, 2025) cut new starts ~10% YoY, boosting renovation sales (~+6% 2025); input inflation (lumber +18% 2024, polymers +12% 2024) compressed gross margins; supplier hedges cover ~45% of inputs and domestic sourcing ~55% (2024) to limit landed‑cost volatility (container rates ±40–60%, bunker +30% 2024); labor shortages (61% builders, NAHB 2024) raised installation times ~18%.

| Metric | Value |

|---|---|

| 30‑yr rate (2025) | ~7.1% |

| New starts change | -10% YoY |

| Lumber (2024) | +18% |

| Hedged inputs | ~45% |

Full Version Awaits

Andersen Corporation PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, and it contains a concise PESTLE analysis of Andersen Corporation covering political, economic, social, technological, legal, and environmental factors relevant to its market and operations.