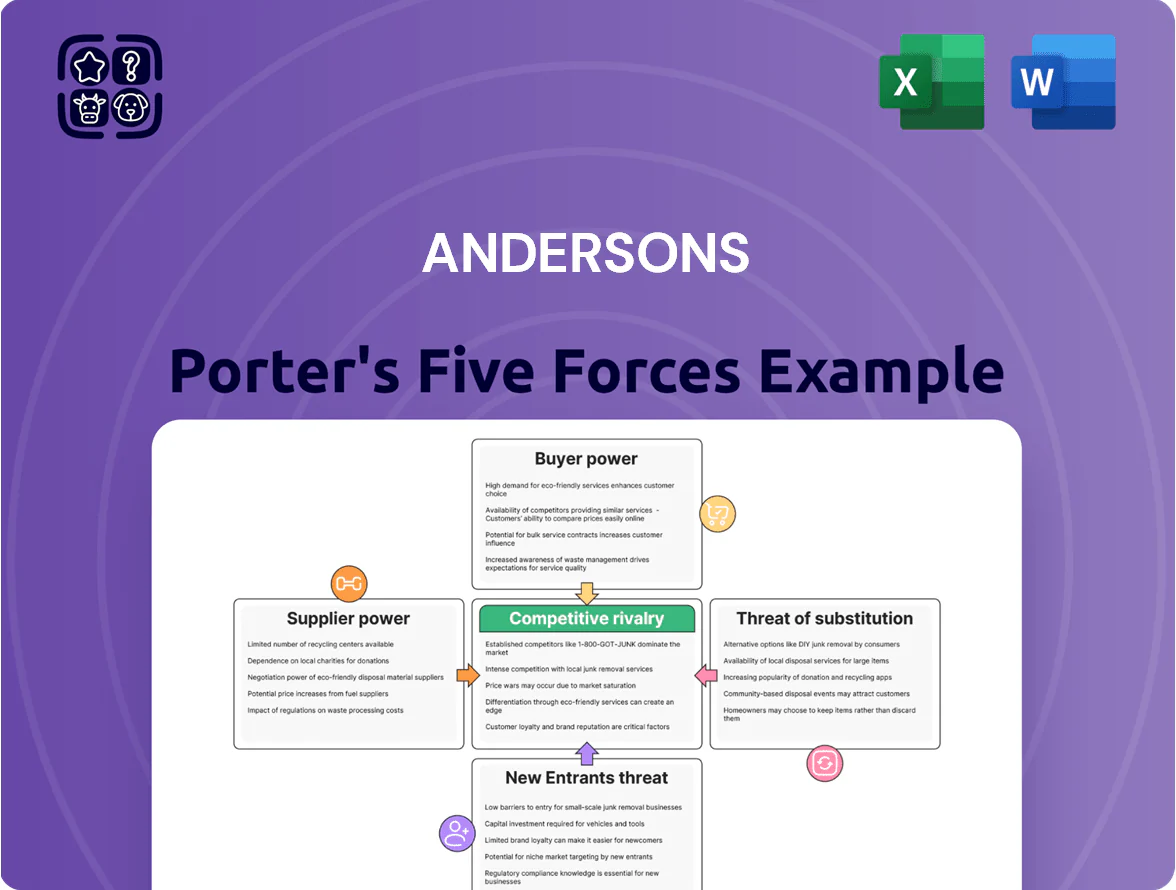

Andersons Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Andersons faces moderate supplier power and cyclical demand, while buyer negotiation and substitute threats hinge on commodity prices and technological shifts—keeper margins are under pressure and scale matters.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Andersons’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of Grain Producers

Thousands of independent grain farmers supply The Andersons, so no single producer holds much bargaining power; USDA reports 2024 US corn farms numbered ~190,000, underscoring fragmentation. Global corn futures (CBOT) set baseline prices that the company must match, with 2024 average corn price ~$5.40/bu. The Andersons reduces supplier price pressure by offering storage, merchandising, and risk-management services to lock in loyalty.

Concentration of Nutrient Manufacturers

The global potash market is dominated by three players—Belaruskali, Nutrien (Canada), and Uralkali—controlling about 70% of exports in 2024, and phosphate supply is similarly concentrated with Mosaic, OCP Group, and PhosAgro holding roughly 60% of seaborne trade; this concentration gives manufacturers strong price-setting power over distributors like The Andersons.

In 2024 potash spot prices averaged near 420 USD/ton, up 18% year-over-year, so The Andersons must use just-in-time inventory, multi-month forward purchase contracts, and fertilizer futures hedges to protect gross margins; a simple hedge covering 30% of expected volume would have cut 2024 price-exposure by roughly 5–8% based on volatility.

Energy and Utility Provider Influence

Energy use in ethanol making is high, so The Andersons depends on natural gas and grid electricity; in 2024 U.S. industrial natural gas average was about $5.20/MMBtu and industrial electricity ~$0.078/kWh, which limits cost control.

Utilities are often state-regulated or regional monopolies, giving the company little bargaining power on tariffs and capacity charges, so rate shifts pass straight to Renewables margins.

Spot natural gas volatility rose 48% in 2023–24, so price swings can change Renewables segment EBITDA by several million dollars annually on modest feedstock and fuel shifts.

Specialized Railcar Equipment Suppliers

The Andersons depends on a small set of specialized railcar manufacturers for new cars and premium components; procurement concentration gives suppliers notable pricing leverage over expansion and modernization projects.

In 2024 the North American new-railcar backlog rose ~15% vs 2023, pushing lead times to 12–18 months and unit prices up ~8%, so steel or parts shortages can delay fleet growth and raise maintenance costs.

- Few suppliers → higher price leverage

- Lead times 12–18 months (2024)

- Unit prices +8% (2024)

- Steel/parts disruption → delayed expansion, higher maintenance

Volatility of Raw Commodity Markets

Andersons: Fragmented corn supply vs concentrated fertilizer & energy risks — margins held ~3pts

Suppliers vary: fragmented US grain base (~190,000 corn farms in 2024) gives The Andersons low supplier power, while concentrated fertilizer (Nutrien, Belaruskali, Uralkali ≈70% exports) and railcar/energy suppliers give high leverage; 2024 potash ~$420/ton, corn ~$5.40/bu, nat gas ~$5.20/MMBtu. Hedging, storage, and diversified sourcing limited 2024 gross-margin swing to ~3 pts.

| Item | 2024 value |

|---|---|

| US corn farms | ~190,000 |

| Corn price (CBOT) | $5.40/bu |

| Potash spot | $420/ton |

| Nat gas (industrial) | $5.20/MMBtu |

| Fertilizer export conc. | ~70% |

| Gross-margin swing cut | ~3 pts |

What is included in the product

Concise Porter’s Five Forces assessment of The Andersons, highlighting competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers—identifying strategic risks and opportunities shaping its industry positioning.

Fast, one-sheet Porter's Five Forces for The Andersons—clarify competitive pressures and spot relief strategies in seconds for confident, board-ready decisions.

Customers Bargaining Power

Consolidation of Food and Feed Processors

Large-scale buyers like Tyson Foods and Cargill, and US livestock integrators purchasing millions of bushels, wield strong bargaining power over The Andersons because they buy high volumes—US feed demand was 144 million tons in 2024. These customers force competitive pricing and can switch suppliers quickly due to advanced logistics and rail/truck networks. The Andersons must keep gross margin intact by improving operational efficiency and meeting 98%+ on-time delivery for key accounts to retain them.

Price Sensitivity in Agricultural Nutrients

Farmers and retail dealers buying plant nutrients show high price sensitivity: USDA data show fertilizer price volatility rose 18% in 2023, and when corn futures fell 22% in 2024 average margins tightened, boosting switching to local co-ops. If The Andersons' pricing looks uncompetitive, buyers can pivot quickly to cooperatives or regional distributors, squeezing The Andersons’ market share. This limits the firm’s ability to pass manufacturer cost increases to end users without risking volume loss.

Regulatory Influence on Ethanol Buyers

The Andersons faces concentrated buyer power from fuel blenders whose volumes hinge on mandates like the US Renewable Fuel Standard (RFS) — 2024 RFS implied blending rose to ~15.0 billion gallons renewable fuel equivalent, so a policy cut could reduce ethanol demand rapidly, boosting blender leverage; Andersons mitigates this by producing low‑carbon‑intensity ethanol (CI <40 gCO2e/MJ), which retained a price premium of ~$0.10–0.20/gal in 2025 under stricter state programs.

Market Dynamics in Railcar Leasing

Customers in railcar leasing can switch between road, barge, or truck and several large lessors, or buy cars outright, giving them strong bargaining power—US rail carloadings fell 7.7% y/y in 2024 through Q3, boosting lessee leverage.

During slowdowns lessees push for lower rates or shorter terms; spot lease rates dropped ~12% in 2024 vs 2023, per industry trackers, pressuring margins.

The Andersons offsets this by bundling repair and maintenance—its rail services reduced downtime 18% in 2023, creating stickiness and premium pricing ability.

- Customers have modal alternatives and ownership option

- Rail demand down 7.7% y/y (2024 Q1–Q3)

- Spot lease rates fell ~12% in 2024

- The Andersons’ maintenance cut downtime 18% (2023)

Increased Access to Real Time Market Data

Modern buyers use platforms like CME Group and GrainTrade for real-time commodity prices, cutting the merchandiser information edge and enabling spot purchases when prices dip; 2024 trade-platform use rose ~22% among US grain buyers.

Transparency lets buyers challenge quotes and time buys—cash basis volatility fell 12% in 2023 as more buyers hedged with market data.

The Andersons counters with its own digital tools and client portals launched 2022–2024, offering live pricing, weather signals, and basis analytics to retain margins and advisory revenue.

- Real-time platforms up ~22% usage (2024)

- Cash-basis volatility down 12% (2023)

- Andersons digital tools launched 2022–2024

Buyers’ clout sinks rail rates; Andersons boosts margins with downtime cuts & ethanol premium

Buyers hold strong leverage: large integrators and fuel blenders buy huge volumes (US feed 144M tons, 2024) and can switch suppliers; rail lessees faced 7.7% lower demand (2024 Q1–Q3) and pushed spot lease rates down ~12% in 2024. The Andersons defends margins via 18% downtime reduction in rail services (2023), low‑CI ethanol premium ~$0.10–0.20/gal (2025), and digital pricing tools (launched 2022–2024).

| Metric | Value |

|---|---|

| US feed demand (2024) | 144M tons |

| Rail demand change (2024 Q1–Q3) | -7.7% |

| Spot lease rates change (2024) | -12% |

| Rail downtime reduced (Andersons, 2023) | -18% |

| Low‑CI ethanol premium (2025) | $0.10–0.20/gal |

Preview Before You Purchase

Andersons Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for The Andersons you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted file—ready to download and use the moment you buy.

What you see is the actual deliverable; once payment is complete you’ll have instant access to this exact analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Andersons faces moderate supplier power and cyclical demand, while buyer negotiation and substitute threats hinge on commodity prices and technological shifts—keeper margins are under pressure and scale matters.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Andersons’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of Grain Producers

Thousands of independent grain farmers supply The Andersons, so no single producer holds much bargaining power; USDA reports 2024 US corn farms numbered ~190,000, underscoring fragmentation. Global corn futures (CBOT) set baseline prices that the company must match, with 2024 average corn price ~$5.40/bu. The Andersons reduces supplier price pressure by offering storage, merchandising, and risk-management services to lock in loyalty.

Concentration of Nutrient Manufacturers

The global potash market is dominated by three players—Belaruskali, Nutrien (Canada), and Uralkali—controlling about 70% of exports in 2024, and phosphate supply is similarly concentrated with Mosaic, OCP Group, and PhosAgro holding roughly 60% of seaborne trade; this concentration gives manufacturers strong price-setting power over distributors like The Andersons.

In 2024 potash spot prices averaged near 420 USD/ton, up 18% year-over-year, so The Andersons must use just-in-time inventory, multi-month forward purchase contracts, and fertilizer futures hedges to protect gross margins; a simple hedge covering 30% of expected volume would have cut 2024 price-exposure by roughly 5–8% based on volatility.

Energy and Utility Provider Influence

Energy use in ethanol making is high, so The Andersons depends on natural gas and grid electricity; in 2024 U.S. industrial natural gas average was about $5.20/MMBtu and industrial electricity ~$0.078/kWh, which limits cost control.

Utilities are often state-regulated or regional monopolies, giving the company little bargaining power on tariffs and capacity charges, so rate shifts pass straight to Renewables margins.

Spot natural gas volatility rose 48% in 2023–24, so price swings can change Renewables segment EBITDA by several million dollars annually on modest feedstock and fuel shifts.

Specialized Railcar Equipment Suppliers

The Andersons depends on a small set of specialized railcar manufacturers for new cars and premium components; procurement concentration gives suppliers notable pricing leverage over expansion and modernization projects.

In 2024 the North American new-railcar backlog rose ~15% vs 2023, pushing lead times to 12–18 months and unit prices up ~8%, so steel or parts shortages can delay fleet growth and raise maintenance costs.

- Few suppliers → higher price leverage

- Lead times 12–18 months (2024)

- Unit prices +8% (2024)

- Steel/parts disruption → delayed expansion, higher maintenance

Volatility of Raw Commodity Markets

Andersons: Fragmented corn supply vs concentrated fertilizer & energy risks — margins held ~3pts

Suppliers vary: fragmented US grain base (~190,000 corn farms in 2024) gives The Andersons low supplier power, while concentrated fertilizer (Nutrien, Belaruskali, Uralkali ≈70% exports) and railcar/energy suppliers give high leverage; 2024 potash ~$420/ton, corn ~$5.40/bu, nat gas ~$5.20/MMBtu. Hedging, storage, and diversified sourcing limited 2024 gross-margin swing to ~3 pts.

| Item | 2024 value |

|---|---|

| US corn farms | ~190,000 |

| Corn price (CBOT) | $5.40/bu |

| Potash spot | $420/ton |

| Nat gas (industrial) | $5.20/MMBtu |

| Fertilizer export conc. | ~70% |

| Gross-margin swing cut | ~3 pts |

What is included in the product

Concise Porter’s Five Forces assessment of The Andersons, highlighting competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers—identifying strategic risks and opportunities shaping its industry positioning.

Fast, one-sheet Porter's Five Forces for The Andersons—clarify competitive pressures and spot relief strategies in seconds for confident, board-ready decisions.

Customers Bargaining Power

Consolidation of Food and Feed Processors

Large-scale buyers like Tyson Foods and Cargill, and US livestock integrators purchasing millions of bushels, wield strong bargaining power over The Andersons because they buy high volumes—US feed demand was 144 million tons in 2024. These customers force competitive pricing and can switch suppliers quickly due to advanced logistics and rail/truck networks. The Andersons must keep gross margin intact by improving operational efficiency and meeting 98%+ on-time delivery for key accounts to retain them.

Price Sensitivity in Agricultural Nutrients

Farmers and retail dealers buying plant nutrients show high price sensitivity: USDA data show fertilizer price volatility rose 18% in 2023, and when corn futures fell 22% in 2024 average margins tightened, boosting switching to local co-ops. If The Andersons' pricing looks uncompetitive, buyers can pivot quickly to cooperatives or regional distributors, squeezing The Andersons’ market share. This limits the firm’s ability to pass manufacturer cost increases to end users without risking volume loss.

Regulatory Influence on Ethanol Buyers

The Andersons faces concentrated buyer power from fuel blenders whose volumes hinge on mandates like the US Renewable Fuel Standard (RFS) — 2024 RFS implied blending rose to ~15.0 billion gallons renewable fuel equivalent, so a policy cut could reduce ethanol demand rapidly, boosting blender leverage; Andersons mitigates this by producing low‑carbon‑intensity ethanol (CI <40 gCO2e/MJ), which retained a price premium of ~$0.10–0.20/gal in 2025 under stricter state programs.

Market Dynamics in Railcar Leasing

Customers in railcar leasing can switch between road, barge, or truck and several large lessors, or buy cars outright, giving them strong bargaining power—US rail carloadings fell 7.7% y/y in 2024 through Q3, boosting lessee leverage.

During slowdowns lessees push for lower rates or shorter terms; spot lease rates dropped ~12% in 2024 vs 2023, per industry trackers, pressuring margins.

The Andersons offsets this by bundling repair and maintenance—its rail services reduced downtime 18% in 2023, creating stickiness and premium pricing ability.

- Customers have modal alternatives and ownership option

- Rail demand down 7.7% y/y (2024 Q1–Q3)

- Spot lease rates fell ~12% in 2024

- The Andersons’ maintenance cut downtime 18% (2023)

Increased Access to Real Time Market Data

Modern buyers use platforms like CME Group and GrainTrade for real-time commodity prices, cutting the merchandiser information edge and enabling spot purchases when prices dip; 2024 trade-platform use rose ~22% among US grain buyers.

Transparency lets buyers challenge quotes and time buys—cash basis volatility fell 12% in 2023 as more buyers hedged with market data.

The Andersons counters with its own digital tools and client portals launched 2022–2024, offering live pricing, weather signals, and basis analytics to retain margins and advisory revenue.

- Real-time platforms up ~22% usage (2024)

- Cash-basis volatility down 12% (2023)

- Andersons digital tools launched 2022–2024

Buyers’ clout sinks rail rates; Andersons boosts margins with downtime cuts & ethanol premium

Buyers hold strong leverage: large integrators and fuel blenders buy huge volumes (US feed 144M tons, 2024) and can switch suppliers; rail lessees faced 7.7% lower demand (2024 Q1–Q3) and pushed spot lease rates down ~12% in 2024. The Andersons defends margins via 18% downtime reduction in rail services (2023), low‑CI ethanol premium ~$0.10–0.20/gal (2025), and digital pricing tools (launched 2022–2024).

| Metric | Value |

|---|---|

| US feed demand (2024) | 144M tons |

| Rail demand change (2024 Q1–Q3) | -7.7% |

| Spot lease rates change (2024) | -12% |

| Rail downtime reduced (Andersons, 2023) | -18% |

| Low‑CI ethanol premium (2025) | $0.10–0.20/gal |

Preview Before You Purchase

Andersons Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for The Andersons you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted file—ready to download and use the moment you buy.

What you see is the actual deliverable; once payment is complete you’ll have instant access to this exact analysis.