Andrew Peller PESTLE Analysis

Skip the Research. Get the Strategy.

Explore how political shifts, consumer trends, and sustainability pressures shape Andrew Peller’s growth prospects in our concise PESTLE snapshot—then unlock the full, actionable report to inform investment and strategy decisions. Purchase the complete PESTLE analysis now for detailed, editable insights and practical recommendations tailored to Andrew Peller’s competitive landscape.

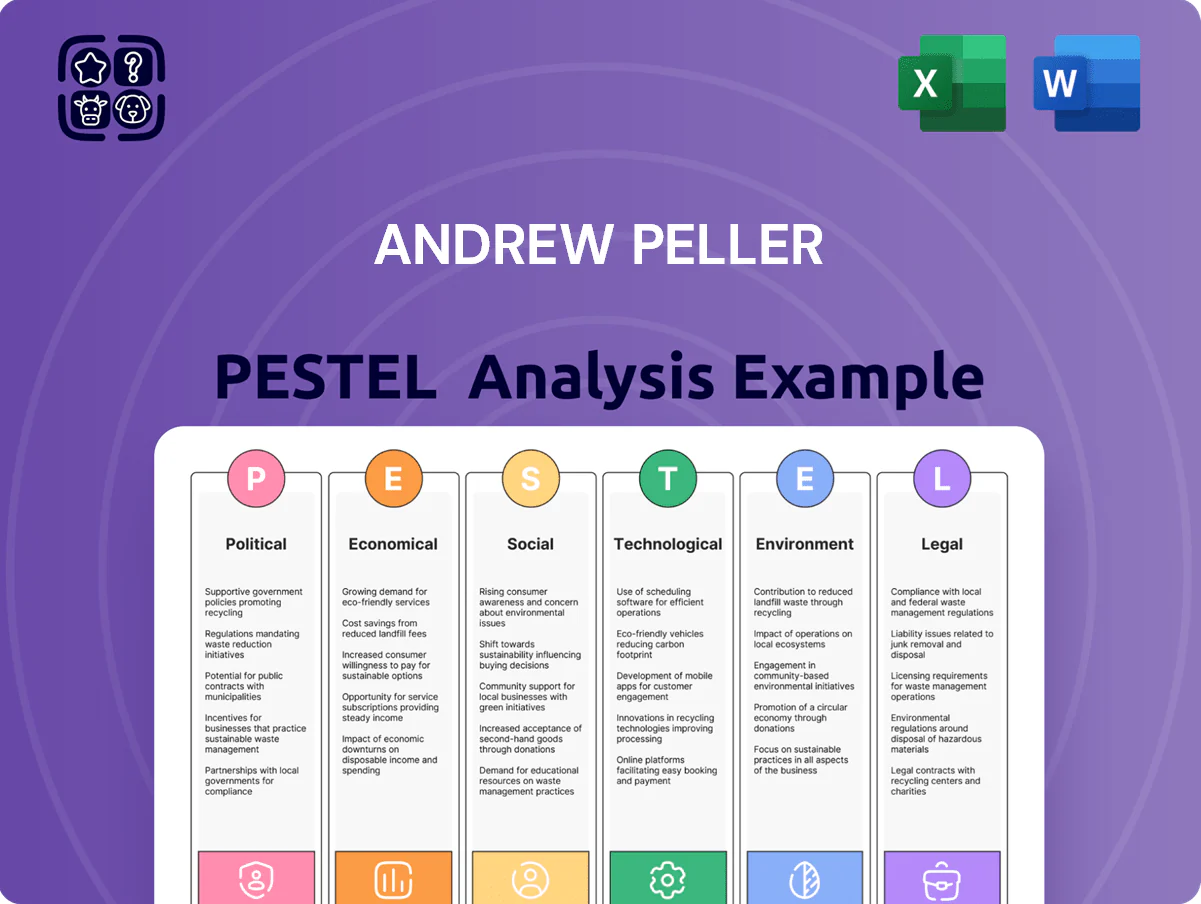

Political factors

Inter-provincial trade barriers

The movement of wine across Canadian provincial borders remains subject to complex regulatory frameworks that in 2024 still fragment distribution, contributing to added logistics costs—provincial differences can increase fulfilment expenses by an estimated 5–10% for national distributors like Andrew Peller. While incremental liberalization has occurred, provincial monopolies (e.g., LCBO, SAQ) continue strict controls that limit direct-to-consumer shipping and constrain margin expansion. Navigating these political hurdles is essential for Andrew Peller to maximize domestic market share and streamline a national logistics network amid a Canadian wine market valued at roughly CAD 7.8 billion in 2024.

Federal excise tax adjustments

The Canadian federal government raised the excise duty escalation rate in 2024, adding roughly CAD 0.10–0.20 per standard drink on spirits equivalents, which can push Andrew Peller’s retail prices up and erode margins given the company reported 2023 gross margin of ~40.2%.

Tax hikes historically reduce volume: alcohol excise increases correlated with a 1–3% annual drop in category volumes in prior years, risking lower sales for Andrew Peller.

Management needs active government relations—Andrew Peller’s advocacy and industry lobbying helped secure exemptions in past federal reviews—critical to maintain a stable tax environment and protect long-term viability of Canada’s CAD 6–7 billion wine market.

Government agricultural subsidies

International trade agreements

Trade deals like CUSMA and CPTPP shape import flows; Canada imported CAD 4.9B of wine in 2024, raising competition for Andrew Peller’s mid-tier brands.

Tariff cuts or protections can flood market with low-cost foreign labels, pressuring margins and market share given Andrew Peller’s domestic positioning.

The firm must track geopolitical shifts affecting tariffs and export windows for Canadian craft spirits—Canada’s wine exports were CAD 175M in 2024.

- CUSMA/CPTPP affect import competitiveness

- CAD 4.9B wine imports (2024) increase low-cost pressure

- CAD 175M Canada wine exports (2024) signal export potential

Provincial liquor board policies

The operational success of Andrew Peller Co. is tightly linked to provincial liquor boards like Ontario's LCBO and BC's BCLDB, which controlled roughly 60% of Canadian retail liquor sales in 2024 — LCBO alone reported C$7.1bn in sales (2024).

Political changes affecting shelf space, listing fees, and local promotion mandates can rapidly shift distribution; new provincial listing requirements in 2023 increased vendor compliance costs by an estimated 8–12% for suppliers.

Strong institutional relationships and active engagement with procurement processes are essential to secure consistent shelf presence and protect annual volume and revenue streams (Andrew Peller reported C$700–900m in annual revenue range, 2023–24 estimates).

- Dependence on LCBO/BCLDB: ~60% of market

- LCBO 2024 sales: C$7.1bn

- 2023 listing rule changes raised supplier costs ~8–12%

- Securing shelf space is critical to protect C$700–900m revenue range

Canadian wine: regulatory costs, import pressure and concentrated provincial retail grip

Provincial liquor controls and fragmented interprovincial rules add ~5–10% to national logistics costs; LCBO/BCLDB accounted for ~60% of retail sales (LCBO C$7.1bn, 2024). Federal excise rises (2024) added ≈CAD 0.10–0.20/standard drink, pressuring margins (Andrew Peller gross margin ~40.2%, 2023). CAD 4.9bn wine imports (2024) increase low‑cost competition; Canada wine exports CAD 175M (2024).

| Metric | 2024 |

|---|---|

| LCBO sales | C$7.1bn |

| Retail share (provincial boards) | ~60% |

| Wine imports | CAD 4.9bn |

| Wine exports | CAD 175M |

| Andrew Peller gross margin | ~40.2% (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely impact Andrew Peller, using data-driven trends and region-specific dynamics to identify risks and opportunities for executives, investors and strategists.

A concise, visually segmented PESTLE summary for Andrew Peller that’s easily dropped into presentations or shared across teams, enabling quick alignment on external risks, market positioning, and region-specific notes during strategy sessions.

Economic factors

Consumer discretionary spending levels

As a producer of premium and mid-market wines, Andrew Peller’s revenue is highly sensitive to Canadian household disposable income; Statistics Canada reported real disposable income growth of 0.3% in 2024 after a 1.1% fall in 2023, affecting premium wine demand.

Economic downturns or high inflation — Canada’s CPI rose 3.4% in 2024 — push consumers to trade down or cut alcohol spending, with on-premise wine sales sliding ~6% in 2023.

The company must balance its portfolio with value-oriented brands; Andrew Peller’s entry-level labels, which accounted for an estimated 30% of volume in 2024, help stabilize revenue during tightened household budgets.

Interest rate fluctuations

The capital-intensive nature of vineyard management and winery expansion makes Andrew Peller highly sensitive to borrowing costs; Canada’s key policy rate rose to 5.00% in 2024, lifting commercial loan rates and increasing debt service burdens. High rates elevate interest expense and can postpone capital projects like facility upgrades or land acquisitions, potentially trimming 2024–25 capex plans. Investors track Andrew Peller’s leverage—debt/EBITDA was about 2.1x in FY2024—and interest coverage to gauge resilience through volatile monetary cycles.

Currency exchange volatility

As a Canadian producer relying on imported grapes, bulk wine and equipment priced in USD/EUR, Andrew Peller faces input cost pressure when the CAD weakens; CAD fell ~6% vs USD in 2023 and was ~0.74 USD in Dec 2024, raising import costs and squeezing gross margins if prices are not passed to consumers.

Currency swings also alter export competitiveness and local rival dynamics: a weaker CAD can boost export price attractiveness but makes imported labels relatively more expensive, shifting market share—Canada imported wine worth CAD 2.6B in 2023, underscoring exposure.

Labor market constraints

The wine sector faces rising minimum wages—Canada's federal minimum reached 16.65 CAD in 2025 in several provinces and provincial lows rose similarly—while skilled vineyard and cellar labor remains scarce, pushing wages for experienced workers in Okanagan and Niagara above regional averages by 10–20%.

Competition from fruit growers and tourism operators increases recruitment costs and turnover, raising operating labor expenses by an estimated 5–12% for many wineries in 2024–25, pressuring margins.

Executives may need capital for automation investments; small-to-mid wineries report typical automation project costs of CAD 150k–600k, a significant one-time expense that can reduce labor needs but requires financing.

Supply chain inflationary pressures

Rising input costs—glass up ~18% and corrugated cardboard up ~15 year-over-year in 2024—raised Andrew Peller’s COGS materially, while aluminum caps climbed near 12%; combined packaging inflation pressured gross margins across wine and spirits lines.

Energy-driven costs for cold storage and distribution rose with North American industrial electricity up ~9% in 2024, increasing logistics and temperature-control expenses.

To protect margins Andrew Peller must pursue centralized procurement, long-term supplier contracts, hedging on energy where feasible, SKU rationalization and process automation to offset persistent inflation.

- Packaging inflation: glass +18%, cardboard +15%, aluminum +12% (2024)

- Energy: industrial electricity ~+9% (2024)

- Mitigants: centralized sourcing, long-term contracts, energy hedges, SKU rationalization

Rising costs and weak income squeeze premium wine demand—margin pressure ahead

Economic sensitivity: disposable income growth slowed (real disposable income +0.3% in 2024) with CPI +3.4% (2024), pressuring premium wine demand; policy rate 5.00% (2024) raised borrowing costs (debt/EBITDA ~2.1x FY2024); CAD ~0.74 USD (Dec 2024) raised import costs; packaging inflation: glass +18%, cardboard +15% (2024); labor up 5–12% with minimum ≈CAD16.65 (2025).

| Metric | Value |

|---|---|

| Real disposable income (2024) | +0.3% |

| CPI (2024) | +3.4% |

| Policy rate (2024) | 5.00% |

| CAD/USD (Dec 2024) | 0.74 |

| Debt/EBITDA (FY2024) | ~2.1x |

| Glass inflation (2024) | +18% |

Full Version Awaits

Andrew Peller PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, containing the complete Andrew Peller PESTLE analysis with professional structure, no placeholders or teasers. What you see is the final file you’ll download immediately after payment, matching the layout, content, and formatting displayed in this preview.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Explore how political shifts, consumer trends, and sustainability pressures shape Andrew Peller’s growth prospects in our concise PESTLE snapshot—then unlock the full, actionable report to inform investment and strategy decisions. Purchase the complete PESTLE analysis now for detailed, editable insights and practical recommendations tailored to Andrew Peller’s competitive landscape.

Political factors

Inter-provincial trade barriers

The movement of wine across Canadian provincial borders remains subject to complex regulatory frameworks that in 2024 still fragment distribution, contributing to added logistics costs—provincial differences can increase fulfilment expenses by an estimated 5–10% for national distributors like Andrew Peller. While incremental liberalization has occurred, provincial monopolies (e.g., LCBO, SAQ) continue strict controls that limit direct-to-consumer shipping and constrain margin expansion. Navigating these political hurdles is essential for Andrew Peller to maximize domestic market share and streamline a national logistics network amid a Canadian wine market valued at roughly CAD 7.8 billion in 2024.

Federal excise tax adjustments

The Canadian federal government raised the excise duty escalation rate in 2024, adding roughly CAD 0.10–0.20 per standard drink on spirits equivalents, which can push Andrew Peller’s retail prices up and erode margins given the company reported 2023 gross margin of ~40.2%.

Tax hikes historically reduce volume: alcohol excise increases correlated with a 1–3% annual drop in category volumes in prior years, risking lower sales for Andrew Peller.

Management needs active government relations—Andrew Peller’s advocacy and industry lobbying helped secure exemptions in past federal reviews—critical to maintain a stable tax environment and protect long-term viability of Canada’s CAD 6–7 billion wine market.

Government agricultural subsidies

International trade agreements

Trade deals like CUSMA and CPTPP shape import flows; Canada imported CAD 4.9B of wine in 2024, raising competition for Andrew Peller’s mid-tier brands.

Tariff cuts or protections can flood market with low-cost foreign labels, pressuring margins and market share given Andrew Peller’s domestic positioning.

The firm must track geopolitical shifts affecting tariffs and export windows for Canadian craft spirits—Canada’s wine exports were CAD 175M in 2024.

- CUSMA/CPTPP affect import competitiveness

- CAD 4.9B wine imports (2024) increase low-cost pressure

- CAD 175M Canada wine exports (2024) signal export potential

Provincial liquor board policies

The operational success of Andrew Peller Co. is tightly linked to provincial liquor boards like Ontario's LCBO and BC's BCLDB, which controlled roughly 60% of Canadian retail liquor sales in 2024 — LCBO alone reported C$7.1bn in sales (2024).

Political changes affecting shelf space, listing fees, and local promotion mandates can rapidly shift distribution; new provincial listing requirements in 2023 increased vendor compliance costs by an estimated 8–12% for suppliers.

Strong institutional relationships and active engagement with procurement processes are essential to secure consistent shelf presence and protect annual volume and revenue streams (Andrew Peller reported C$700–900m in annual revenue range, 2023–24 estimates).

- Dependence on LCBO/BCLDB: ~60% of market

- LCBO 2024 sales: C$7.1bn

- 2023 listing rule changes raised supplier costs ~8–12%

- Securing shelf space is critical to protect C$700–900m revenue range

Canadian wine: regulatory costs, import pressure and concentrated provincial retail grip

Provincial liquor controls and fragmented interprovincial rules add ~5–10% to national logistics costs; LCBO/BCLDB accounted for ~60% of retail sales (LCBO C$7.1bn, 2024). Federal excise rises (2024) added ≈CAD 0.10–0.20/standard drink, pressuring margins (Andrew Peller gross margin ~40.2%, 2023). CAD 4.9bn wine imports (2024) increase low‑cost competition; Canada wine exports CAD 175M (2024).

| Metric | 2024 |

|---|---|

| LCBO sales | C$7.1bn |

| Retail share (provincial boards) | ~60% |

| Wine imports | CAD 4.9bn |

| Wine exports | CAD 175M |

| Andrew Peller gross margin | ~40.2% (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely impact Andrew Peller, using data-driven trends and region-specific dynamics to identify risks and opportunities for executives, investors and strategists.

A concise, visually segmented PESTLE summary for Andrew Peller that’s easily dropped into presentations or shared across teams, enabling quick alignment on external risks, market positioning, and region-specific notes during strategy sessions.

Economic factors

Consumer discretionary spending levels

As a producer of premium and mid-market wines, Andrew Peller’s revenue is highly sensitive to Canadian household disposable income; Statistics Canada reported real disposable income growth of 0.3% in 2024 after a 1.1% fall in 2023, affecting premium wine demand.

Economic downturns or high inflation — Canada’s CPI rose 3.4% in 2024 — push consumers to trade down or cut alcohol spending, with on-premise wine sales sliding ~6% in 2023.

The company must balance its portfolio with value-oriented brands; Andrew Peller’s entry-level labels, which accounted for an estimated 30% of volume in 2024, help stabilize revenue during tightened household budgets.

Interest rate fluctuations

The capital-intensive nature of vineyard management and winery expansion makes Andrew Peller highly sensitive to borrowing costs; Canada’s key policy rate rose to 5.00% in 2024, lifting commercial loan rates and increasing debt service burdens. High rates elevate interest expense and can postpone capital projects like facility upgrades or land acquisitions, potentially trimming 2024–25 capex plans. Investors track Andrew Peller’s leverage—debt/EBITDA was about 2.1x in FY2024—and interest coverage to gauge resilience through volatile monetary cycles.

Currency exchange volatility

As a Canadian producer relying on imported grapes, bulk wine and equipment priced in USD/EUR, Andrew Peller faces input cost pressure when the CAD weakens; CAD fell ~6% vs USD in 2023 and was ~0.74 USD in Dec 2024, raising import costs and squeezing gross margins if prices are not passed to consumers.

Currency swings also alter export competitiveness and local rival dynamics: a weaker CAD can boost export price attractiveness but makes imported labels relatively more expensive, shifting market share—Canada imported wine worth CAD 2.6B in 2023, underscoring exposure.

Labor market constraints

The wine sector faces rising minimum wages—Canada's federal minimum reached 16.65 CAD in 2025 in several provinces and provincial lows rose similarly—while skilled vineyard and cellar labor remains scarce, pushing wages for experienced workers in Okanagan and Niagara above regional averages by 10–20%.

Competition from fruit growers and tourism operators increases recruitment costs and turnover, raising operating labor expenses by an estimated 5–12% for many wineries in 2024–25, pressuring margins.

Executives may need capital for automation investments; small-to-mid wineries report typical automation project costs of CAD 150k–600k, a significant one-time expense that can reduce labor needs but requires financing.

Supply chain inflationary pressures

Rising input costs—glass up ~18% and corrugated cardboard up ~15 year-over-year in 2024—raised Andrew Peller’s COGS materially, while aluminum caps climbed near 12%; combined packaging inflation pressured gross margins across wine and spirits lines.

Energy-driven costs for cold storage and distribution rose with North American industrial electricity up ~9% in 2024, increasing logistics and temperature-control expenses.

To protect margins Andrew Peller must pursue centralized procurement, long-term supplier contracts, hedging on energy where feasible, SKU rationalization and process automation to offset persistent inflation.

- Packaging inflation: glass +18%, cardboard +15%, aluminum +12% (2024)

- Energy: industrial electricity ~+9% (2024)

- Mitigants: centralized sourcing, long-term contracts, energy hedges, SKU rationalization

Rising costs and weak income squeeze premium wine demand—margin pressure ahead

Economic sensitivity: disposable income growth slowed (real disposable income +0.3% in 2024) with CPI +3.4% (2024), pressuring premium wine demand; policy rate 5.00% (2024) raised borrowing costs (debt/EBITDA ~2.1x FY2024); CAD ~0.74 USD (Dec 2024) raised import costs; packaging inflation: glass +18%, cardboard +15% (2024); labor up 5–12% with minimum ≈CAD16.65 (2025).

| Metric | Value |

|---|---|

| Real disposable income (2024) | +0.3% |

| CPI (2024) | +3.4% |

| Policy rate (2024) | 5.00% |

| CAD/USD (Dec 2024) | 0.74 |

| Debt/EBITDA (FY2024) | ~2.1x |

| Glass inflation (2024) | +18% |

Full Version Awaits

Andrew Peller PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, containing the complete Andrew Peller PESTLE analysis with professional structure, no placeholders or teasers. What you see is the final file you’ll download immediately after payment, matching the layout, content, and formatting displayed in this preview.