Angang Steel Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

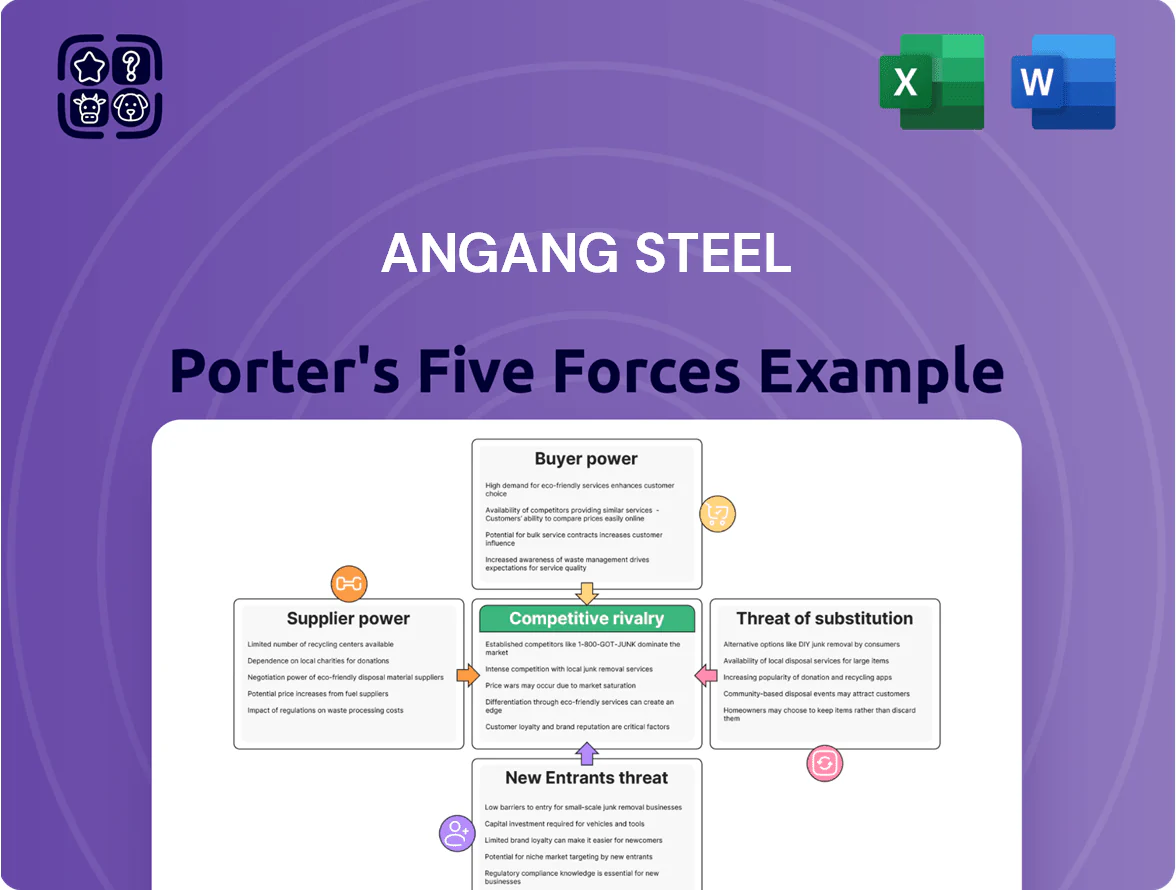

Angang Steel faces intense rivalry from domestic peers, moderate supplier leverage due to raw-material concentration, and persistent buyer pressure from large industrial customers, while barriers to entry remain high and substitutes pose limited short-term threat.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Angang Steel’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Concentration

The global iron ore market is concentrated: BHP, Rio Tinto, and Vale supplied about 57% of seaborne iron ore in 2024, giving them strong pricing power over Angang Steel (Anshan Iron & Steel Group).

Ansteel Group supplies part of Angang’s needs, but Angang still buys on the spot market and faces volatility—iron ore 62% Fe fines averaged 107 USD/t in 2024, up 18% from 2023.

High-grade ore demand rises with stricter emissions rules; meeting 2024 BF-BOF (blast furnace-basic oxygen furnace) standards increased Angang’s high-grade ore share to ~40%, raising cost exposure.

Energy Input Volatility

Energy input volatility: coking coal and power account for roughly 25–30% of Angang Steel’s production cost; coking coal prices surged ~40% in 2021–2022 and hit RMB 2,200/ton in Jan 2024, while industrial power tariffs rose 5–8% in 2023 after mine curbs. Suppliers hold leverage during geopolitical shocks or China mining restrictions, so Angang’s margins can swing quickly unless it secures long-term contracts or hedges.

Parent Company Integration

As a subsidiary of Ansteel Group (Anshan Iron & Steel, 2024 revenue RMB 281.5 billion), Angang Steel gains vertical-integration advantages—stable iron ore and coking coal flows and shared logistics that cut input volatility vs independents by an estimated 12–18% in 2023 procurement cost comparisons.

That said, Angang’s supply chain exposure ties to Ansteel’s strategy and balance sheet: Ansteel’s 2024 net debt/EBITDA ~2.1 can constrain raw-material capex and force centralized sourcing decisions affecting Angang’s operational flexibility.

Logistics and Transportation Costs

Suppliers of shipping and rail freight hold leverage because Angang ships massive tonnages—China’s steel logistics average 60–120 yuan/ton transport costs in 2024, and fuel-driven spikes can add 5–12% to expenses.

Infrastructure bottlenecks and congestion on key rail corridors raise lead times and demurrage risks, and Angang’s dependence on specific state-run rail lines creates localized supplier power over pricing and schedules.

Higher transport costs are hard to pass to downstream buyers amid China’s 2024 flat steel margins, squeezing Angang’s operating margins.

- Bulk volumes = high freight dependency

- 2024 avg transport 60–120 yuan/ton; fuel adds 5–12%

- State-run rail creates localized dependency

- Limited pass-through hurts margins

Decarbonization Technology Providers

Miner dominance, rising energy & tech costs squeeze steel margins; Ansteel ties Angang to leverage

Suppliers hold moderate-to-high power: three miners (BHP, Rio Tinto, Vale) supplied ~57% seaborne ore in 2024; 62% Fe ore averaged $107/t (2024). Energy/coking coal and freight (60–120 yuan/ton) drive 25–30% of costs; Ansteel Group vertical integration cuts procurement volatility ~12–18% but ties Angang to Ansteel’s net debt/EBITDA ~2.1 (2024). CCS/electrolyzer vendors add rising leverage.

| Metric | 2024 value |

|---|---|

| Seaborne ore share (top3) | 57% |

| 62% Fe price | $107/t |

| Transport cost | 60–120 yuan/t |

| Ansteel net debt/EBITDA | ~2.1 |

What is included in the product

Provides a focused Porter's Five Forces assessment for Angang Steel, uncovering competitive intensity, supplier/buyer power, substitute threats, and entry barriers with strategic insights tailored to the company.

Clear Porter's Five Forces snapshot for Angang Steel—quickly pinpoint supplier, buyer, and competitive pressures to guide strategic moves and investment decisions.

Customers Bargaining Power

Large Industrial Client Leverage

Low Switching Costs for Commodity Products

For standard steel like hot-rolled sheets, buyers can switch suppliers on price and delivery; global crude steel export competitiveness meant China’s slab export price gap averaged about 60–90 USD/ton in 2024, so a small price advantage wins contracts.

Because these products are undifferentiated, Angang (Ansteel Group Corporation Limited) must cut unit costs—its 2024 COGS-to-revenue was ~78%—or lose share to lower-cost mills.

Lack of brand loyalty raises buyer power: commodity customers negotiate aggressively, pushing margins down and forcing Angang to prioritize operational efficiency and logistics speed.

Price Transparency and Digital Platforms

The rise of digital trading platforms and live indices (e.g., SteelMint, Platts) has pushed steel price transparency up—global spot price feeds now update hourly, and 2024 data show online price discovery reduced bid-ask spreads by ~12% in hot-rolled coil markets. Buyers can instantly compare Angang Steel’s quotes with domestic rivals and Chinese exporters, cutting Angang’s ability to hold premium margins. This info symmetry lets procurement teams negotiate tougher terms at renewals; a 2023 survey found 68% of buyers used online indices to demand price concessions. Expect margin pressure unless Angang adds service or quality differentiation.

Sensitivity to Downstream Economic Cycles

Demand for steel is cyclical and tied to construction and manufacturing, which contracted in China by 1.2% and 0.8% respectively in 2024–25, making buyers far more price-sensitive and aggressive in negotiations.

During these slowdowns Angang often concedes margins or absorbs raw-material cost increases to keep blast furnaces and rolling mills running, contributing to a 2024 gross margin drop of ~220 basis points year-on-year.

- Construction/manuf. decline: China −1.2%/−0.8% (2024–25)

- Buyers sharpen price demands; spot discounts widen

- Angang absorbs costs; gross margin fell ~220 bps in 2024

Demand for Specialized High-End Specs

High-end aerospace and precision machinery buyers prioritize technical specs over price, forcing Angang Steel to fund custom R&D and dedicated runs; in 2024 Angang reported ~RMB 1.2bn R&D spend, reflecting this pressure.

If Angang misses strict quality or certification targets, these clients—often sourcing from specialized global mills in Japan and Germany—can switch, risking multi-million-dollar contracts.

- High specs > price sensitivity

- RMB 1.2bn R&D (2024)

- Dedicated runs raise unit costs

- Losses: multi‑million contracts to foreign specialists

Concentrated buyers squeeze margins—24.6Mt sales, receivables surge, R&D offsets

| Metric | 2024 |

|---|---|

| Sales | 24.6 Mt |

| Top‑5 share | 42% |

| Receivables | RMB 21.4bn |

| Gross margin change | −220 bps |

| R&D | RMB 1.2bn |

Full Version Awaits

Angang Steel Porter's Five Forces Analysis

This preview shows the exact Angang Steel Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the final deliverable: the same complete file available to you instantly after payment. No mockups or samples—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Angang Steel faces intense rivalry from domestic peers, moderate supplier leverage due to raw-material concentration, and persistent buyer pressure from large industrial customers, while barriers to entry remain high and substitutes pose limited short-term threat.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Angang Steel’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Concentration

The global iron ore market is concentrated: BHP, Rio Tinto, and Vale supplied about 57% of seaborne iron ore in 2024, giving them strong pricing power over Angang Steel (Anshan Iron & Steel Group).

Ansteel Group supplies part of Angang’s needs, but Angang still buys on the spot market and faces volatility—iron ore 62% Fe fines averaged 107 USD/t in 2024, up 18% from 2023.

High-grade ore demand rises with stricter emissions rules; meeting 2024 BF-BOF (blast furnace-basic oxygen furnace) standards increased Angang’s high-grade ore share to ~40%, raising cost exposure.

Energy Input Volatility

Energy input volatility: coking coal and power account for roughly 25–30% of Angang Steel’s production cost; coking coal prices surged ~40% in 2021–2022 and hit RMB 2,200/ton in Jan 2024, while industrial power tariffs rose 5–8% in 2023 after mine curbs. Suppliers hold leverage during geopolitical shocks or China mining restrictions, so Angang’s margins can swing quickly unless it secures long-term contracts or hedges.

Parent Company Integration

As a subsidiary of Ansteel Group (Anshan Iron & Steel, 2024 revenue RMB 281.5 billion), Angang Steel gains vertical-integration advantages—stable iron ore and coking coal flows and shared logistics that cut input volatility vs independents by an estimated 12–18% in 2023 procurement cost comparisons.

That said, Angang’s supply chain exposure ties to Ansteel’s strategy and balance sheet: Ansteel’s 2024 net debt/EBITDA ~2.1 can constrain raw-material capex and force centralized sourcing decisions affecting Angang’s operational flexibility.

Logistics and Transportation Costs

Suppliers of shipping and rail freight hold leverage because Angang ships massive tonnages—China’s steel logistics average 60–120 yuan/ton transport costs in 2024, and fuel-driven spikes can add 5–12% to expenses.

Infrastructure bottlenecks and congestion on key rail corridors raise lead times and demurrage risks, and Angang’s dependence on specific state-run rail lines creates localized supplier power over pricing and schedules.

Higher transport costs are hard to pass to downstream buyers amid China’s 2024 flat steel margins, squeezing Angang’s operating margins.

- Bulk volumes = high freight dependency

- 2024 avg transport 60–120 yuan/ton; fuel adds 5–12%

- State-run rail creates localized dependency

- Limited pass-through hurts margins

Decarbonization Technology Providers

Miner dominance, rising energy & tech costs squeeze steel margins; Ansteel ties Angang to leverage

Suppliers hold moderate-to-high power: three miners (BHP, Rio Tinto, Vale) supplied ~57% seaborne ore in 2024; 62% Fe ore averaged $107/t (2024). Energy/coking coal and freight (60–120 yuan/ton) drive 25–30% of costs; Ansteel Group vertical integration cuts procurement volatility ~12–18% but ties Angang to Ansteel’s net debt/EBITDA ~2.1 (2024). CCS/electrolyzer vendors add rising leverage.

| Metric | 2024 value |

|---|---|

| Seaborne ore share (top3) | 57% |

| 62% Fe price | $107/t |

| Transport cost | 60–120 yuan/t |

| Ansteel net debt/EBITDA | ~2.1 |

What is included in the product

Provides a focused Porter's Five Forces assessment for Angang Steel, uncovering competitive intensity, supplier/buyer power, substitute threats, and entry barriers with strategic insights tailored to the company.

Clear Porter's Five Forces snapshot for Angang Steel—quickly pinpoint supplier, buyer, and competitive pressures to guide strategic moves and investment decisions.

Customers Bargaining Power

Large Industrial Client Leverage

Low Switching Costs for Commodity Products

For standard steel like hot-rolled sheets, buyers can switch suppliers on price and delivery; global crude steel export competitiveness meant China’s slab export price gap averaged about 60–90 USD/ton in 2024, so a small price advantage wins contracts.

Because these products are undifferentiated, Angang (Ansteel Group Corporation Limited) must cut unit costs—its 2024 COGS-to-revenue was ~78%—or lose share to lower-cost mills.

Lack of brand loyalty raises buyer power: commodity customers negotiate aggressively, pushing margins down and forcing Angang to prioritize operational efficiency and logistics speed.

Price Transparency and Digital Platforms

The rise of digital trading platforms and live indices (e.g., SteelMint, Platts) has pushed steel price transparency up—global spot price feeds now update hourly, and 2024 data show online price discovery reduced bid-ask spreads by ~12% in hot-rolled coil markets. Buyers can instantly compare Angang Steel’s quotes with domestic rivals and Chinese exporters, cutting Angang’s ability to hold premium margins. This info symmetry lets procurement teams negotiate tougher terms at renewals; a 2023 survey found 68% of buyers used online indices to demand price concessions. Expect margin pressure unless Angang adds service or quality differentiation.

Sensitivity to Downstream Economic Cycles

Demand for steel is cyclical and tied to construction and manufacturing, which contracted in China by 1.2% and 0.8% respectively in 2024–25, making buyers far more price-sensitive and aggressive in negotiations.

During these slowdowns Angang often concedes margins or absorbs raw-material cost increases to keep blast furnaces and rolling mills running, contributing to a 2024 gross margin drop of ~220 basis points year-on-year.

- Construction/manuf. decline: China −1.2%/−0.8% (2024–25)

- Buyers sharpen price demands; spot discounts widen

- Angang absorbs costs; gross margin fell ~220 bps in 2024

Demand for Specialized High-End Specs

High-end aerospace and precision machinery buyers prioritize technical specs over price, forcing Angang Steel to fund custom R&D and dedicated runs; in 2024 Angang reported ~RMB 1.2bn R&D spend, reflecting this pressure.

If Angang misses strict quality or certification targets, these clients—often sourcing from specialized global mills in Japan and Germany—can switch, risking multi-million-dollar contracts.

- High specs > price sensitivity

- RMB 1.2bn R&D (2024)

- Dedicated runs raise unit costs

- Losses: multi‑million contracts to foreign specialists

Concentrated buyers squeeze margins—24.6Mt sales, receivables surge, R&D offsets

| Metric | 2024 |

|---|---|

| Sales | 24.6 Mt |

| Top‑5 share | 42% |

| Receivables | RMB 21.4bn |

| Gross margin change | −220 bps |

| R&D | RMB 1.2bn |

Full Version Awaits

Angang Steel Porter's Five Forces Analysis

This preview shows the exact Angang Steel Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the final deliverable: the same complete file available to you instantly after payment. No mockups or samples—what you see is what you get.