Angang Steel Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

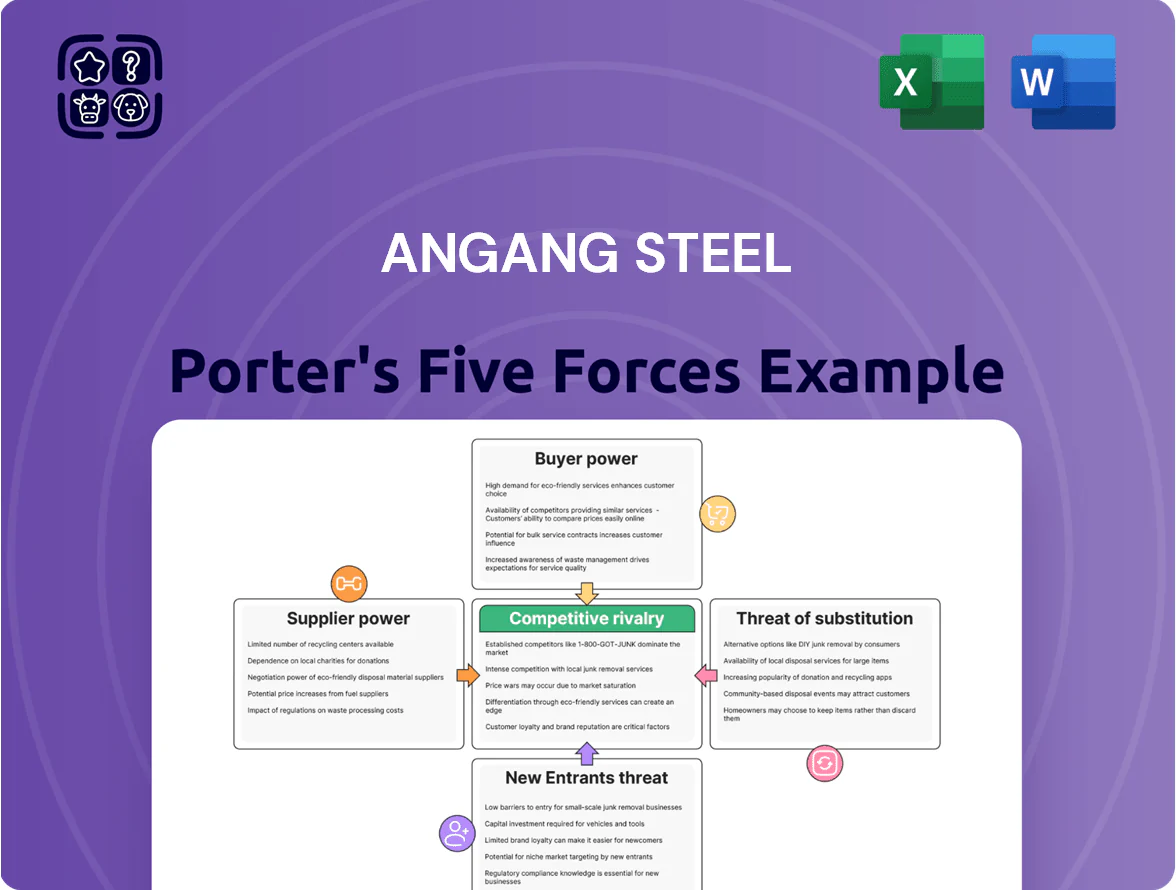

Angang Steel faces intense rivalry from domestic giants and price-sensitive buyers, while raw-material suppliers and cyclical demand limit margin flexibility; barriers to entry are moderate but scale and distribution advantages protect incumbents.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Angang Steel’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global Iron Ore Giants

The global iron-ore market is highly concentrated, with Vale, Rio Tinto and BHP supplying about 60% of seaborne iron ore in 2024–2025, giving them strong pricing power over Angang Steel. High-grade ore is critical for Angang’s blast furnaces, so shortages or premium pricing from these miners raise feedstock costs and squeeze margins. Despite Angang’s diversification efforts, late-2025 procurement still sources roughly 40–50% from majors, keeping supplier power high. This forces Angang to absorb market-driven price swings—iron ore fines 62% Fe index rose ~22% YoY in 2025—directly impacting EBITDA.

Energy and Coking Coal Volatility

Energy costs and coking coal availability strongly raise supplier power for Ansteel (Angang). In 2024 China coking coal prices averaged about 2,200 CNY/ton, up ~18% year-on-year, and fuel/energy makes ~20–25% of blast-furnace steel costs, so utilities/miners can push prices and terms.

Carbon rules since 2021 cut thermal-coal supply and strengthened premium coal suppliers, tightening contracts and raising spot volatility; suppliers win more leverage in negotiations.

Ansteel faces rising input costs and must shift to low-carbon energy—solar, hydrogen, or purchased green power—often via niche providers with higher margins and less bargaining pressure.

Because steelmaking is highly energy intensive, suppliers remain a dominant cost driver: a 1% fuel price rise can cut hot-rolled coil margins by ~0.3–0.5 percentage points, so supplier leverage stays high.

Vertical Integration with Parent Group

As a subsidiary of Anshan Iron and Steel Group, Angang gains internal supply security: in 2024 roughly 35–40% of its iron ore and 30% of logistics needs were sourced within the group, reducing reliance on external vendors. This vertical integration cuts supplier bargaining power by ensuring stable feedstock and transport rates, lowering raw-material cost volatility versus smaller rivals. Group sourcing also supports faster procurement during disruptions, improving operational resilience.

Technological and Equipment Dependency

The transition to smart manufacturing and green steel at Angang relies on specialized machinery and proprietary software from a few global engineering firms, giving suppliers strong leverage; global green-steel equipment market was valued at about $12.4B in 2024, concentrating vendors and tech.

These suppliers lock value via long-term maintenance and service contracts—typical 7–10 year SLAs—and switching would require billions in capex and risk operational downtime, so vendors hold negotiating power during modernization.

- 2024 green-steel equipment market: $12.4B

- Typical supplier SLAs: 7–10 years

- Switching capex: potentially hundreds of millions to >$1B per major plant

- High vendor concentration: few global OEMs dominate

Logistics and Infrastructure Constraints

State-controlled rail and major shipping lines dominate bulk transport for Angang Steel, giving suppliers high bargaining power since alternatives for heavy volumes are limited; China Railway carried 3.8bn tonnes in 2024, showing scale concentration.

Freight rate swings and port fees shift landed costs materially—dry bulk freight index rose ~22% in 2024, affecting export pricing and margins.

Angang’s location forces reliance on stable contracts with rail and ports to meet deliveries across northeastern and southern industrial hubs; any disruption raises stock and logistics costs.

- High dependency: state rail + major shippers dominate

- Scale: China Railway 3.8bn tonnes (2024)

- Cost risk: Baltic Dry-like index +22% in 2024

- Operational need: stable contracts to avoid delays

Suppliers Hold Sway: Top Miners ≈60%, Angang Still 40–50% External; Costs Up

Suppliers exert high power: top miners (Vale, Rio Tinto, BHP) supply ~60% seaborne ore (2024–25), Angang still sources ~40–50% externally (late‑2025), coking coal avg ~2,200 CNY/ton in 2024 (+18% YoY), fuel ~20–25% of costs; group internal sourcing (35–40% ore, 30% logistics in 2024) reduces but does not eliminate supplier leverage.

| Metric | 2024–25 |

|---|---|

| Top miners share | ~60% |

| Angang external ore | 40–50% |

| Coking coal price | ~2,200 CNY/ton |

| Internal ore logistics | 35–40% / 30% |

What is included in the product

Tailored Porter's Five Forces analysis of Angang Steel that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—supporting strategic decisions and investor materials.

Concise Porter's Five Forces snapshot for Angang Steel—helps executives quickly gauge competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Consolidation of Major Industrial Buyers

Low Switching Costs for Standardized Products

For many construction and manufacturing uses, hot-rolled sheets are commodities, so buyers choose on price and lead time, not brand. With 2024 Chinese crude steel output at 1.01 billion tonnes and domestic mill utilisation near 75%, oversupply lets buyers pit Angang (Anshan Iron & Steel Group) against rivals to cut prices. Market transparency—online spot indices showing weekly price swings of 30–70 CNY/tonne—keeps switching costs low and boosts customer bargaining power.

Global Price Transparency and Benchmarking

Real-time global steel price indices (Platts, CRU) and platforms (Metalshub) give buyers transparent benchmarks; spot HRC (hot-rolled coil) averaged 880 USD/ton in 2025 Q1, so customers quickly spot Angang price gaps.

Well-informed buyers track iron ore and coking coal swings—iron ore seaborne fell 18% in 2024—letting them credibly challenge Angang’s increases.

This parity forces Angang to forgo premiums on commodity grades unless a specialised alloy is offered, keeping EBITDA margins on standard slabs near industry median ~6–8%.

Growth of Green Steel Demand

As regulations tighten, major buyers (automotive, construction) now demand certified green steel—global green-steel demand grew ~42% in 2024, with corporate procurement targets pushing suppliers to near-zero CO2 standards.

This lets customers set new environmental specs and certifications; Angang must spend heavily on low-carbon tech or lose preferred-supplier status and share to greener rivals.

Customers gain leverage, forcing environmental accountability plus competitive pricing.

- 2024 green-steel demand +42%

- Buyers set certification standards

- Angang needs capex for low-carbon tech

- Customer power rises: price + sustainability

Sensitivity to Economic Cycles

The demand for Angang Steel (Anshan Iron & Steel Group) closely follows China’s real estate and infrastructure cycles; residential investment fell 8.6% year-on-year in 2024, raising project delays and cutting steel orders.

In slowdowns buyers slash inventories and push for lower prices and extended payment terms, forcing Angang to offer discounts to keep blast furnaces and rolling mills at high utilization.

Customer bargaining power peaks during weak demand and policy uncertainty, evidenced by spot-price discounts of up to 12% in late-2023/2024 construction slowdowns.

- Real estate decline: -8.6% residential investment 2024

- Spot discounts: up to 12% in 2023–24

- Buyers seek longer payments, lower inventory

Top buyers drive rebates, low switching costs and capex strain as green-steel demand surges

Large buyers (top 10 ~28% of demand in 2024) wield strong price and spec leverage; OEMs secured 3–7% rebates in 2025, and shifting a ≥200 ktpa contract can cut a mill’s regional sales 2–5%. Commodity HRC pricing (2025 Q1 spot ~880 USD/t) and online indices (weekly swings 30–70 CNY/t) keep switching costs low. Green-steel demand rose ~42% in 2024, forcing buyers to demand low‑carbon specs and raising supplier capex pressure.

| Metric | 2024–25 |

|---|---|

| Top‑10 buyer share | ~28% |

| OEM rebates | 3–7% |

| Spot HRC | ~880 USD/t (2025 Q1) |

| Green‑steel demand | +42% (2024) |

Same Document Delivered

Angang Steel Porter's Five Forces Analysis

This preview shows the exact Angang Steel Porter’s Five Forces analysis you’ll receive—no placeholders or excerpts; the full, professionally formatted document is ready for instant download and use after purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Angang Steel faces intense rivalry from domestic giants and price-sensitive buyers, while raw-material suppliers and cyclical demand limit margin flexibility; barriers to entry are moderate but scale and distribution advantages protect incumbents.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Angang Steel’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global Iron Ore Giants

The global iron-ore market is highly concentrated, with Vale, Rio Tinto and BHP supplying about 60% of seaborne iron ore in 2024–2025, giving them strong pricing power over Angang Steel. High-grade ore is critical for Angang’s blast furnaces, so shortages or premium pricing from these miners raise feedstock costs and squeeze margins. Despite Angang’s diversification efforts, late-2025 procurement still sources roughly 40–50% from majors, keeping supplier power high. This forces Angang to absorb market-driven price swings—iron ore fines 62% Fe index rose ~22% YoY in 2025—directly impacting EBITDA.

Energy and Coking Coal Volatility

Energy costs and coking coal availability strongly raise supplier power for Ansteel (Angang). In 2024 China coking coal prices averaged about 2,200 CNY/ton, up ~18% year-on-year, and fuel/energy makes ~20–25% of blast-furnace steel costs, so utilities/miners can push prices and terms.

Carbon rules since 2021 cut thermal-coal supply and strengthened premium coal suppliers, tightening contracts and raising spot volatility; suppliers win more leverage in negotiations.

Ansteel faces rising input costs and must shift to low-carbon energy—solar, hydrogen, or purchased green power—often via niche providers with higher margins and less bargaining pressure.

Because steelmaking is highly energy intensive, suppliers remain a dominant cost driver: a 1% fuel price rise can cut hot-rolled coil margins by ~0.3–0.5 percentage points, so supplier leverage stays high.

Vertical Integration with Parent Group

As a subsidiary of Anshan Iron and Steel Group, Angang gains internal supply security: in 2024 roughly 35–40% of its iron ore and 30% of logistics needs were sourced within the group, reducing reliance on external vendors. This vertical integration cuts supplier bargaining power by ensuring stable feedstock and transport rates, lowering raw-material cost volatility versus smaller rivals. Group sourcing also supports faster procurement during disruptions, improving operational resilience.

Technological and Equipment Dependency

The transition to smart manufacturing and green steel at Angang relies on specialized machinery and proprietary software from a few global engineering firms, giving suppliers strong leverage; global green-steel equipment market was valued at about $12.4B in 2024, concentrating vendors and tech.

These suppliers lock value via long-term maintenance and service contracts—typical 7–10 year SLAs—and switching would require billions in capex and risk operational downtime, so vendors hold negotiating power during modernization.

- 2024 green-steel equipment market: $12.4B

- Typical supplier SLAs: 7–10 years

- Switching capex: potentially hundreds of millions to >$1B per major plant

- High vendor concentration: few global OEMs dominate

Logistics and Infrastructure Constraints

State-controlled rail and major shipping lines dominate bulk transport for Angang Steel, giving suppliers high bargaining power since alternatives for heavy volumes are limited; China Railway carried 3.8bn tonnes in 2024, showing scale concentration.

Freight rate swings and port fees shift landed costs materially—dry bulk freight index rose ~22% in 2024, affecting export pricing and margins.

Angang’s location forces reliance on stable contracts with rail and ports to meet deliveries across northeastern and southern industrial hubs; any disruption raises stock and logistics costs.

- High dependency: state rail + major shippers dominate

- Scale: China Railway 3.8bn tonnes (2024)

- Cost risk: Baltic Dry-like index +22% in 2024

- Operational need: stable contracts to avoid delays

Suppliers Hold Sway: Top Miners ≈60%, Angang Still 40–50% External; Costs Up

Suppliers exert high power: top miners (Vale, Rio Tinto, BHP) supply ~60% seaborne ore (2024–25), Angang still sources ~40–50% externally (late‑2025), coking coal avg ~2,200 CNY/ton in 2024 (+18% YoY), fuel ~20–25% of costs; group internal sourcing (35–40% ore, 30% logistics in 2024) reduces but does not eliminate supplier leverage.

| Metric | 2024–25 |

|---|---|

| Top miners share | ~60% |

| Angang external ore | 40–50% |

| Coking coal price | ~2,200 CNY/ton |

| Internal ore logistics | 35–40% / 30% |

What is included in the product

Tailored Porter's Five Forces analysis of Angang Steel that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—supporting strategic decisions and investor materials.

Concise Porter's Five Forces snapshot for Angang Steel—helps executives quickly gauge competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Consolidation of Major Industrial Buyers

Low Switching Costs for Standardized Products

For many construction and manufacturing uses, hot-rolled sheets are commodities, so buyers choose on price and lead time, not brand. With 2024 Chinese crude steel output at 1.01 billion tonnes and domestic mill utilisation near 75%, oversupply lets buyers pit Angang (Anshan Iron & Steel Group) against rivals to cut prices. Market transparency—online spot indices showing weekly price swings of 30–70 CNY/tonne—keeps switching costs low and boosts customer bargaining power.

Global Price Transparency and Benchmarking

Real-time global steel price indices (Platts, CRU) and platforms (Metalshub) give buyers transparent benchmarks; spot HRC (hot-rolled coil) averaged 880 USD/ton in 2025 Q1, so customers quickly spot Angang price gaps.

Well-informed buyers track iron ore and coking coal swings—iron ore seaborne fell 18% in 2024—letting them credibly challenge Angang’s increases.

This parity forces Angang to forgo premiums on commodity grades unless a specialised alloy is offered, keeping EBITDA margins on standard slabs near industry median ~6–8%.

Growth of Green Steel Demand

As regulations tighten, major buyers (automotive, construction) now demand certified green steel—global green-steel demand grew ~42% in 2024, with corporate procurement targets pushing suppliers to near-zero CO2 standards.

This lets customers set new environmental specs and certifications; Angang must spend heavily on low-carbon tech or lose preferred-supplier status and share to greener rivals.

Customers gain leverage, forcing environmental accountability plus competitive pricing.

- 2024 green-steel demand +42%

- Buyers set certification standards

- Angang needs capex for low-carbon tech

- Customer power rises: price + sustainability

Sensitivity to Economic Cycles

The demand for Angang Steel (Anshan Iron & Steel Group) closely follows China’s real estate and infrastructure cycles; residential investment fell 8.6% year-on-year in 2024, raising project delays and cutting steel orders.

In slowdowns buyers slash inventories and push for lower prices and extended payment terms, forcing Angang to offer discounts to keep blast furnaces and rolling mills at high utilization.

Customer bargaining power peaks during weak demand and policy uncertainty, evidenced by spot-price discounts of up to 12% in late-2023/2024 construction slowdowns.

- Real estate decline: -8.6% residential investment 2024

- Spot discounts: up to 12% in 2023–24

- Buyers seek longer payments, lower inventory

Top buyers drive rebates, low switching costs and capex strain as green-steel demand surges

Large buyers (top 10 ~28% of demand in 2024) wield strong price and spec leverage; OEMs secured 3–7% rebates in 2025, and shifting a ≥200 ktpa contract can cut a mill’s regional sales 2–5%. Commodity HRC pricing (2025 Q1 spot ~880 USD/t) and online indices (weekly swings 30–70 CNY/t) keep switching costs low. Green-steel demand rose ~42% in 2024, forcing buyers to demand low‑carbon specs and raising supplier capex pressure.

| Metric | 2024–25 |

|---|---|

| Top‑10 buyer share | ~28% |

| OEM rebates | 3–7% |

| Spot HRC | ~880 USD/t (2025 Q1) |

| Green‑steel demand | +42% (2024) |

Same Document Delivered

Angang Steel Porter's Five Forces Analysis

This preview shows the exact Angang Steel Porter’s Five Forces analysis you’ll receive—no placeholders or excerpts; the full, professionally formatted document is ready for instant download and use after purchase.