Antero Midstream Partners Business Model Canvas

Antero Midstream BMC: Asset-Backed Revenue, Value Props & Partner Ecosystem Explained

Dive into Antero Midstream Partners’s operational playbook with a concise Business Model Canvas highlighting its value props, asset-backed revenue streams, and partner ecosystem—essential for investors and strategists wanting clarity on midstream economics.

Partnerships

Strategic Alliance with Antero Resources

As of late 2025, Antero Resources supplies over 85% of Antero Midstream Partners’ throughput, delivering ~2.1 Bcf/d of natural gas and ~85 MBbl/d of NGLs under long‑term contracts that generated ~$420M in minimum volume commitments in 2024.

Joint Venture with MPLX LP

The company runs a material joint venture with MPLX LP to operate processing and fractionation assets, sharing capital risk and broadening services beyond gathering and compression; as of year-end 2024 the JV handled ~200 MBbl/d of fractionation capacity and reduced unit capital intensity by ~15% versus standalone builds. By combining engineering and commercial expertise the venture captures higher NGL margins and strengthens the midstream value chain in the Marcellus/Utica.

Regulatory and Environmental Agencies

Partnerships with state and federal regulators secure Antero Midstream’s license to operate; ongoing engagement keeps the company aligned with methane limits (EPA’s 2024 oil & gas rules cutting emissions ~40% by 2030) and evolving water-disposal standards through 2025, cutting legal-contingency reserve needs—Antero reported $18m in environmental remediation accruals in 2024—while speeding permits for ~$900m planned midstream projects.

Financial Institutions and Lenders

Financial institutions and a syndicate of banks plus institutional investors provide Antero Midstream Partners with credit facilities and bond underwriting—enabling debt refinancing and funding of growth; as of YE 2024 the company cited roughly $1.2 billion of available liquidity and access to capital markets for upcoming maturities.

Maintaining a healthy credit profile—targeting investment-grade metrics where possible—keeps borrowing costs low and preserves refinancing optionality.

- ~$1.2B available liquidity (YE 2024)

- Bank syndicate for credit facilities and revolver access

- Bond underwriters used for debt refinancing

- Focus on strong credit metrics to lower interest expense

Field Service and Construction Contractors

Antero Midstream depends on specialized third-party contractors to build and maintain pipelines, crucial for on-time, on-budget capital projects across West Virginia and Ohio’s rugged terrain; in 2024 contractors handled roughly 65% of field work and helped keep 2024 capex variance under 4% of budget (Antero Midstream 2024 Form 10-K).

- Long-term vendor contracts stabilize rates and secure skilled crews

- Contractors provide surge capacity during peak projects, cutting project delays

- Outsourcing reduces fixed labor costs; pay-as-work model improves cash flow

Antero Midstream: Antero Resources 85% feedstock, MPLX JV 200MBbl/d, $1.2B liquidity

Antero Midstream’s key partners supply feedstock (Antero Resources ~85% of volumes, ~2.1 Bcf/d gas, ~85 MBbl/d NGLs), joint ventures (MPLX JV ~200 MBbl/d frac capacity) and capital (≈$1.2B liquidity YE2024), plus contractors (65% field work) and regulators shaping permitting and emissions costs.

| Partner | Key metric | 2024 |

|---|---|---|

| Antero Resources | Share of throughput | ~85% |

| MPLX JV | Fractionation capacity | ~200 MBbl/d |

| Liquidity | Available | $1.2B |

| Contractors | Field work share | ~65% |

What is included in the product

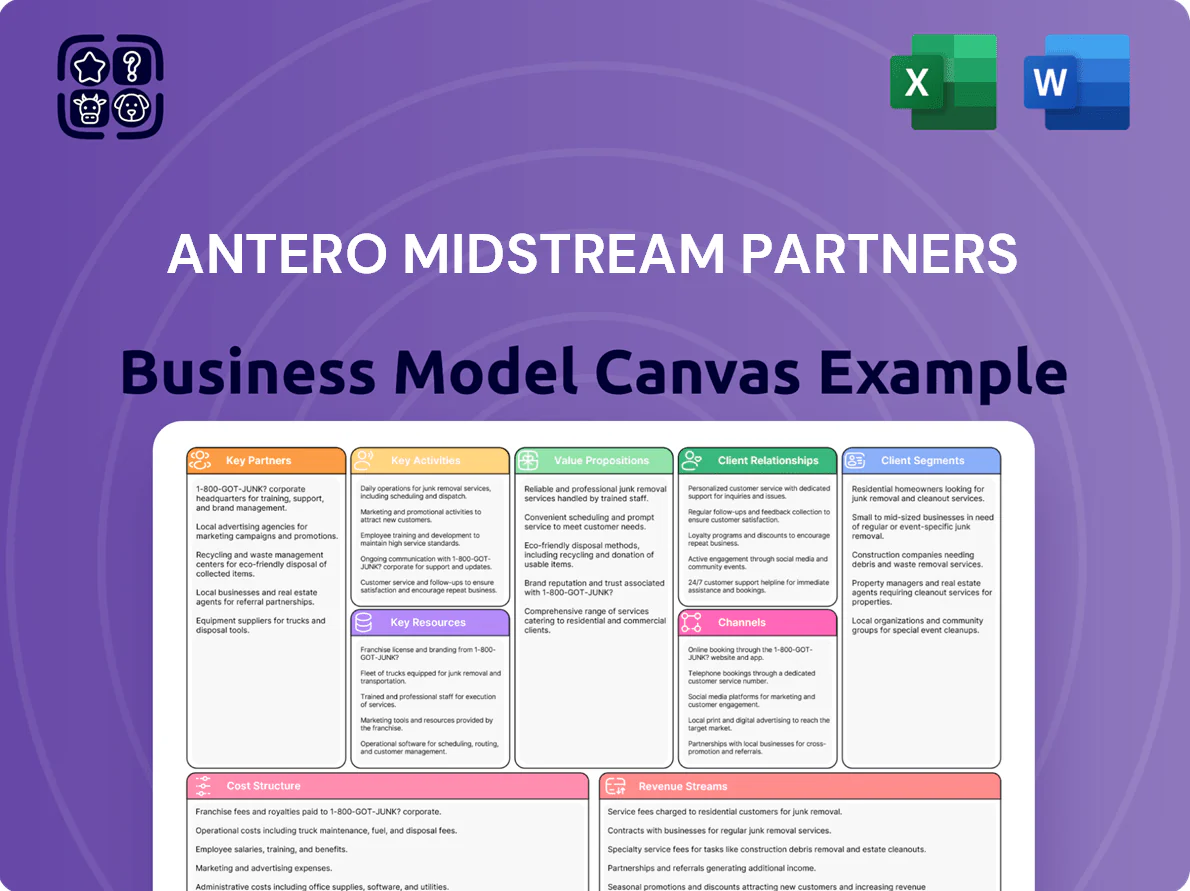

A concise Business Model Canvas for Antero Midstream Partners outlining its nine blocks—customer segments (E&P companies, utilities), value propositions (reliable midstream infrastructure, fee-based cash flows), channels (direct contracts, JV partnerships), customer relationships (long-term acreage & tolling agreements), revenue streams (take-or-pay, throughput fees), key resources (pipelines, processing plants, storage), key activities (gathering, processing, transportation), key partners (Antero Resources, NGL buyers, shippers), cost structure (maintenance, capital projects)—with strategic insights on competitive advantages, risks, and growth opportunities for investor presentations.

Condenses Antero Midstream Partners’ infrastructure and revenue model into a digestible one-page canvas, saving hours of formatting while enabling quick comparison, team collaboration, and boardroom-ready summaries.

Activities

Natural Gas Gathering and Compression

Natural gas gathering and compression moves raw gas from wellheads via ~10,000 miles of low- and high‑pressure pipelines into processing or interstate receipts; Antero Midstream reported 2024 throughput ~3.1 Bcf/d and compression horsepower ~1.2 million HP, making this activity the primary daily operational focus and capital allocation driver.

Integrated Water Management Services

By end-2025 Antero Midstream Partners provides full-cycle water services—freshwater delivery and produced-water gathering—operating >1,200 miles of pipelines that cut trucking needs ~70%, lowering transport costs and CO2e by ~60% versus truck haul; water handling now accounts for ~18% of midstream completions revenue and is essential to upstream well completion efficiency.

Infrastructure Expansion and Maintenance

Ongoing engineering and construction link new Marcellus and Utica well pads to Antero Midstream Partners’ gathering system, with capital spending of about $120–150 million annually in 2024–2025 for expansions and tie‑ins; maintenance teams perform scheduled inspections and inline integrity testing (ILI), reducing downtime by roughly 30% and helping keep spill incidents below industry median (0.02 incidents per 1,000 miles/year).

Processing and Fractionation Oversight

- JV oversight of processing plants

- Ensures pipeline-quality gas

- Recovers NGLs (~97% recovery)

- 2024 plant uptime ~95%

- Contributed to ~$1.1B revenue

Financial Strategy and Dividend Management

Antero Midstream manages its balance sheet to sustain and grow dividends, targeting free cash flow after capex sufficient to cover distributions while cutting leverage; as of 2025 guidance management aimed for distributable cash flow supporting a ~$0.50/share annualized payout and net debt/EBITDA trending toward 1.5x.

Financial planning and analysis stress-tests cash flow against commodity swings and rate moves, using hedges and covenant-aware capex pacing to protect payouts and maintain liquidity.

- Target free cash flow after capex: cover ~$0.50/sh dividends

- Leverage goal: net debt/EBITDA ≈ 1.5x

- Controls: hedging, covenant monitoring, flexible capex

Midstream powerhouse: 3.1 Bcf/d throughput, $1.1B revenue, $0.50 div target

Gathering/compression (≈10,000 mi pipelines) moves ~3.1 Bcf/d with ~1.2M HP; water services (>1,200 mi) cut trucking ~70% and CO2e ~60%, contributing ~18% of completions revenue; JV processing/fractionation yields ~97% NGL recovery, ~95% uptime and helped drive ~$1.1B 2024 revenue; capex $120–150M/yr, target DCF cover ~$0.50/sh and net debt/EBITDA ≈1.5x.

| Metric | Value |

|---|---|

| Throughput | 3.1 Bcf/d |

| Compression HP | 1.2M HP |

| Water pipeline | 1,200+ mi |

| NGL recovery | 97% |

| Plant uptime | 95% |

| 2024 revenue | $1.1B |

| Annual capex | $120–150M |

| Dividend target | $0.50/sh |

| Leverage goal | Net debt/EBITDA ≈1.5x |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Antero Midstream Partners Business Model Canvas—not a mockup—and it reflects the exact structure, content, and formatting you will receive after purchase. When you complete your order, you will download this same professional, ready-to-edit file in Word and Excel formats, with all canvas sections, notes, and supporting details included. There are no placeholders or marketing samples—just the full deliverable as shown, instant and complete for presentation, analysis, or customization.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Antero Midstream BMC: Asset-Backed Revenue, Value Props & Partner Ecosystem Explained

Dive into Antero Midstream Partners’s operational playbook with a concise Business Model Canvas highlighting its value props, asset-backed revenue streams, and partner ecosystem—essential for investors and strategists wanting clarity on midstream economics.

Partnerships

Strategic Alliance with Antero Resources

As of late 2025, Antero Resources supplies over 85% of Antero Midstream Partners’ throughput, delivering ~2.1 Bcf/d of natural gas and ~85 MBbl/d of NGLs under long‑term contracts that generated ~$420M in minimum volume commitments in 2024.

Joint Venture with MPLX LP

The company runs a material joint venture with MPLX LP to operate processing and fractionation assets, sharing capital risk and broadening services beyond gathering and compression; as of year-end 2024 the JV handled ~200 MBbl/d of fractionation capacity and reduced unit capital intensity by ~15% versus standalone builds. By combining engineering and commercial expertise the venture captures higher NGL margins and strengthens the midstream value chain in the Marcellus/Utica.

Regulatory and Environmental Agencies

Partnerships with state and federal regulators secure Antero Midstream’s license to operate; ongoing engagement keeps the company aligned with methane limits (EPA’s 2024 oil & gas rules cutting emissions ~40% by 2030) and evolving water-disposal standards through 2025, cutting legal-contingency reserve needs—Antero reported $18m in environmental remediation accruals in 2024—while speeding permits for ~$900m planned midstream projects.

Financial Institutions and Lenders

Financial institutions and a syndicate of banks plus institutional investors provide Antero Midstream Partners with credit facilities and bond underwriting—enabling debt refinancing and funding of growth; as of YE 2024 the company cited roughly $1.2 billion of available liquidity and access to capital markets for upcoming maturities.

Maintaining a healthy credit profile—targeting investment-grade metrics where possible—keeps borrowing costs low and preserves refinancing optionality.

- ~$1.2B available liquidity (YE 2024)

- Bank syndicate for credit facilities and revolver access

- Bond underwriters used for debt refinancing

- Focus on strong credit metrics to lower interest expense

Field Service and Construction Contractors

Antero Midstream depends on specialized third-party contractors to build and maintain pipelines, crucial for on-time, on-budget capital projects across West Virginia and Ohio’s rugged terrain; in 2024 contractors handled roughly 65% of field work and helped keep 2024 capex variance under 4% of budget (Antero Midstream 2024 Form 10-K).

- Long-term vendor contracts stabilize rates and secure skilled crews

- Contractors provide surge capacity during peak projects, cutting project delays

- Outsourcing reduces fixed labor costs; pay-as-work model improves cash flow

Antero Midstream: Antero Resources 85% feedstock, MPLX JV 200MBbl/d, $1.2B liquidity

Antero Midstream’s key partners supply feedstock (Antero Resources ~85% of volumes, ~2.1 Bcf/d gas, ~85 MBbl/d NGLs), joint ventures (MPLX JV ~200 MBbl/d frac capacity) and capital (≈$1.2B liquidity YE2024), plus contractors (65% field work) and regulators shaping permitting and emissions costs.

| Partner | Key metric | 2024 |

|---|---|---|

| Antero Resources | Share of throughput | ~85% |

| MPLX JV | Fractionation capacity | ~200 MBbl/d |

| Liquidity | Available | $1.2B |

| Contractors | Field work share | ~65% |

What is included in the product

A concise Business Model Canvas for Antero Midstream Partners outlining its nine blocks—customer segments (E&P companies, utilities), value propositions (reliable midstream infrastructure, fee-based cash flows), channels (direct contracts, JV partnerships), customer relationships (long-term acreage & tolling agreements), revenue streams (take-or-pay, throughput fees), key resources (pipelines, processing plants, storage), key activities (gathering, processing, transportation), key partners (Antero Resources, NGL buyers, shippers), cost structure (maintenance, capital projects)—with strategic insights on competitive advantages, risks, and growth opportunities for investor presentations.

Condenses Antero Midstream Partners’ infrastructure and revenue model into a digestible one-page canvas, saving hours of formatting while enabling quick comparison, team collaboration, and boardroom-ready summaries.

Activities

Natural Gas Gathering and Compression

Natural gas gathering and compression moves raw gas from wellheads via ~10,000 miles of low- and high‑pressure pipelines into processing or interstate receipts; Antero Midstream reported 2024 throughput ~3.1 Bcf/d and compression horsepower ~1.2 million HP, making this activity the primary daily operational focus and capital allocation driver.

Integrated Water Management Services

By end-2025 Antero Midstream Partners provides full-cycle water services—freshwater delivery and produced-water gathering—operating >1,200 miles of pipelines that cut trucking needs ~70%, lowering transport costs and CO2e by ~60% versus truck haul; water handling now accounts for ~18% of midstream completions revenue and is essential to upstream well completion efficiency.

Infrastructure Expansion and Maintenance

Ongoing engineering and construction link new Marcellus and Utica well pads to Antero Midstream Partners’ gathering system, with capital spending of about $120–150 million annually in 2024–2025 for expansions and tie‑ins; maintenance teams perform scheduled inspections and inline integrity testing (ILI), reducing downtime by roughly 30% and helping keep spill incidents below industry median (0.02 incidents per 1,000 miles/year).

Processing and Fractionation Oversight

- JV oversight of processing plants

- Ensures pipeline-quality gas

- Recovers NGLs (~97% recovery)

- 2024 plant uptime ~95%

- Contributed to ~$1.1B revenue

Financial Strategy and Dividend Management

Antero Midstream manages its balance sheet to sustain and grow dividends, targeting free cash flow after capex sufficient to cover distributions while cutting leverage; as of 2025 guidance management aimed for distributable cash flow supporting a ~$0.50/share annualized payout and net debt/EBITDA trending toward 1.5x.

Financial planning and analysis stress-tests cash flow against commodity swings and rate moves, using hedges and covenant-aware capex pacing to protect payouts and maintain liquidity.

- Target free cash flow after capex: cover ~$0.50/sh dividends

- Leverage goal: net debt/EBITDA ≈ 1.5x

- Controls: hedging, covenant monitoring, flexible capex

Midstream powerhouse: 3.1 Bcf/d throughput, $1.1B revenue, $0.50 div target

Gathering/compression (≈10,000 mi pipelines) moves ~3.1 Bcf/d with ~1.2M HP; water services (>1,200 mi) cut trucking ~70% and CO2e ~60%, contributing ~18% of completions revenue; JV processing/fractionation yields ~97% NGL recovery, ~95% uptime and helped drive ~$1.1B 2024 revenue; capex $120–150M/yr, target DCF cover ~$0.50/sh and net debt/EBITDA ≈1.5x.

| Metric | Value |

|---|---|

| Throughput | 3.1 Bcf/d |

| Compression HP | 1.2M HP |

| Water pipeline | 1,200+ mi |

| NGL recovery | 97% |

| Plant uptime | 95% |

| 2024 revenue | $1.1B |

| Annual capex | $120–150M |

| Dividend target | $0.50/sh |

| Leverage goal | Net debt/EBITDA ≈1.5x |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Antero Midstream Partners Business Model Canvas—not a mockup—and it reflects the exact structure, content, and formatting you will receive after purchase. When you complete your order, you will download this same professional, ready-to-edit file in Word and Excel formats, with all canvas sections, notes, and supporting details included. There are no placeholders or marketing samples—just the full deliverable as shown, instant and complete for presentation, analysis, or customization.