Antero Midstream Partners SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Antero Midstream’s stable cash flows and strategic Appalachian footprint contrast with commodity exposure and regulatory risks; our concise SWOT preview highlights key operational strengths, leverage concerns, and growth levers worth scrutinizing.

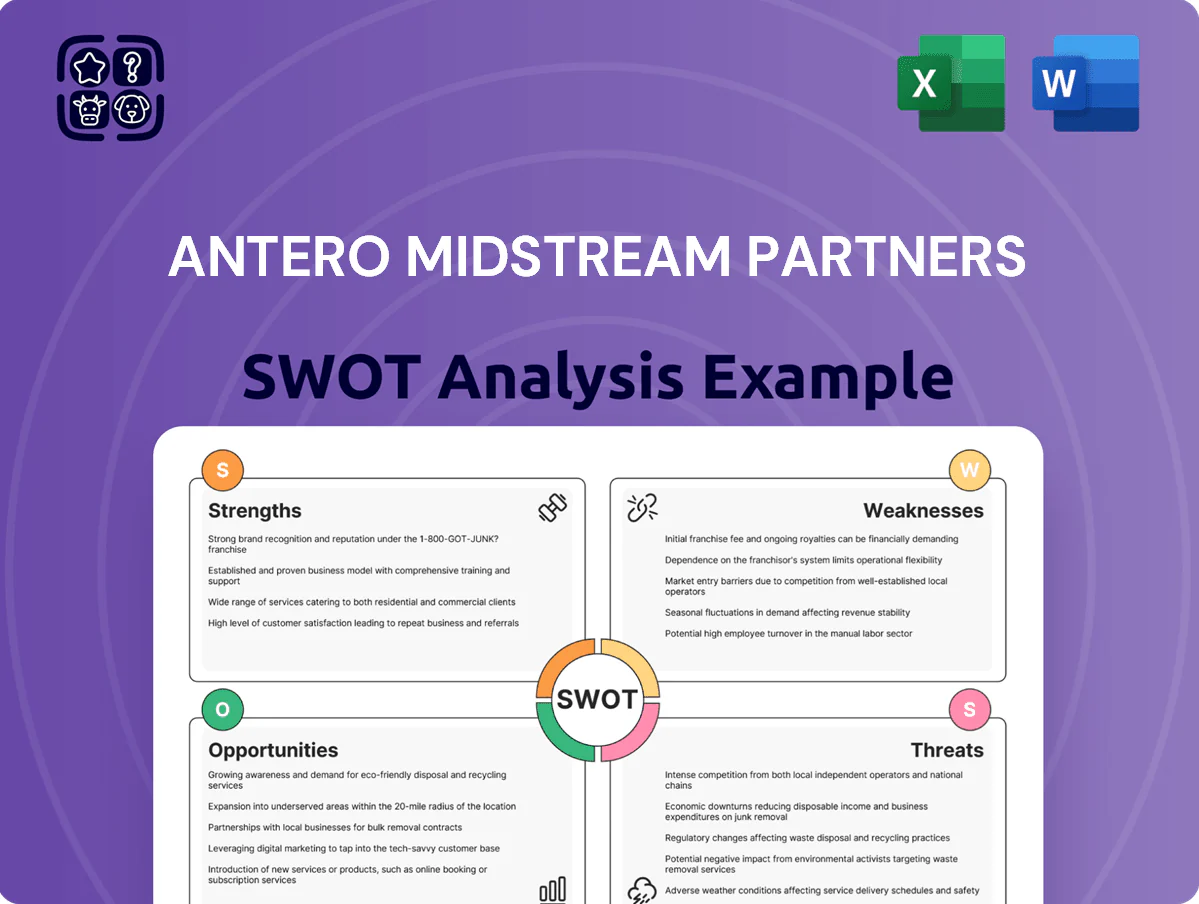

Strengths

Strategic Integration with Antero Resources

The company’s symbiotic tie to Antero Resources, its anchor customer, secured ~65% of volumes in 2024 and delivered predictable cash flow—Antero Resources produced ~3.1 Bcf/d in Appalachia in 2024, much of which flowed through Antero Midstream systems.

Joint development planning lets Antero Midstream time ~$350–400M annual midstream capex to match producer schedules, lowering idle capacity and boosting 2024 adjusted EBITDA margin stability.

High Percentage of Fee-Based Contracts

A significant majority of Antero Midstream Partners’ revenue comes from long-term, fixed-fee contracts—about 75% of cash flow was fee-based in 2024—giving high visibility into future cash flows.

These contracts include minimum volume commitments that shield EBITDA from short-term commodity-price swings and production dips; in 2024 minimums covered roughly 65% of contracted volumes.

This fee-based structure underpinned consistent distributions and funded $150m of 2024 capital projects without large external equity raises.

Robust Free Cash Flow Generation

Leading Appalachian Basin Infrastructure

Antero Midstream owns and operates an interconnected footprint across the Marcellus and Utica shales, the top US gas plays, with ~3,000 miles of gathering pipelines and ~500,000 horsepower of compression (2025 company filings), creating high entry barriers from land, permitting, and corridor constraints.

This physical dominance forms a durable moat, making the firm a critical regional supply chain link and supporting steady fee-based cash flow and volume capture.

- ~3,000 miles pipelines

- ~500,000 HP compression

- Marcellus/Utica = largest US gas production

- High geographic/regulatory entry barriers

Advanced Water Handling Capabilities

Antero Midstream operates a closed-loop water management system covering sourcing, treatment, reuse, and disposal for hydraulic fracturing, cutting truck hauls and emissions. In 2024 the system supported >1,200 well pads, reused ~70% of produced water, and lowered midstream logistics costs by an estimated $8–12 per barrel equivalent.

- Reuses ~70% of produced water

- Supports >1,200 well pads (2024)

- Cuts $8–12 per barrel logistics

High-visibility fee cash flows, $850–900M FCF and regional moat from 3,000-mi pipeline

Anchor customer tie to Antero Resources (≈65% volumes, ~3.1 Bcf/d in 2024) plus ~75% fee-based cash flow in 2024 provides high visibility; coordinated capex ($350–400M/year) stabilized adjusted EBITDA margins; 2025 free cash flow ≈$850–900M funded $300M buybacks, $150M extra dividends and ~$500M net-debt paydown; ~3,000 miles pipelines and ~500,000 HP compression create regional moat.

| Metric | 2024–25 |

|---|---|

| Anchor volumes | ~65% |

| Antero prod. | 3.1 Bcf/d (2024) |

| Fee-based cash | ~75% |

| FCF | $850–900M (2025) |

| Pipelines | ~3,000 miles |

What is included in the product

Provides a concise SWOT overview of Antero Midstream Partners, outlining its operational strengths and weaknesses alongside market opportunities and external threats to assess strategic positioning and future risks.

Delivers a concise SWOT snapshot of Antero Midstream Partners for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Severe Customer Concentration Risk

Antero Midstream Partners depends on Antero Resources for roughly 90% of consolidated revenue in 2024, creating a single-point-of-failure risk in its business model.

Any bankruptcy, production decline, or strategic pivot at Antero Resources would cut cash flows sharply and could breach midstream covenants almost immediately.

Despite a strong current contract portfolio, this extreme customer concentration deters risk-averse institutional investors and raises valuation and refinancing concerns.

Geographic Limitation to Appalachia

Antero Midstream’s operations are confined to the Appalachian Basin, exposing it to regional regulatory shifts, local pipeline bottlenecks, and Marcellus/Utica basis discounts that averaged about 1.80 $/MMBtu below Henry Hub in 2024; unlike peers with Permian or Gulf Coast exposure, it cannot reallocate volumes to higher-margin regions, raising sensitivity to northeastern US political and economic risks and concentrating cash flow volatility from basin-specific outages or takeaway constraints.

Sensitivity to Natural Gas Prices

Although Antero Midstream Partners uses fee-based contracts, its long-term growth links indirectly to Henry Hub natural gas prices; a 2024 average Henry Hub of about 2.70 USD/MMBtu tightened producer drilling budgets and cut completions. If prices stay depressed, Antero Resources may curtail completions, reducing volume growth versus projections and pressuring distributable cash flow. This indirect exposure drove valuation swings in 2022–2024, with shares showing ~40% peak-to-trough volatility.

Limited Non-Gas Revenue Streams

The company earns over 80% of revenues from natural gas gathering and water services (2024 Form 10-K), with negligible crude, refined products, or renewables exposure, concentrating earnings on gas price and demand cycles.

This narrow mix raises transition risk as U.S. gas demand could shift; limited capital spent on renewables or midstream diversification through 2023–2025 keeps appeal low for energy-transition funds.

High Capital Intensity for Expansion

Maintaining and expanding midstream assets needs continuous, large capital outlays that can strain liquidity; Antero Midstream reported $295 million capital expenditures in 2024, down from $410 million in 2023 but still sizable vs free cash flow.

Free cash flow improved to $230 million in 2024, yet pipeline construction and regulatory compliance costs keep pressure on leverage and payout capacity.

Any major cost overruns would threaten leverage targets (net debt/EBITDA 2.8x in 2024) and could force dividend cuts or delayed growth.

- 2024 capex $295M; 2023 $410M

- 2024 free cash flow $230M

- Net debt/EBITDA 2.8x in 2024

- Cost overruns risk dividends and leverage

Concentration Risk: Antero Midstream's 90% Tied to Antero Resources, Tight Leverage

Antero Midstream is highly concentrated: ~90% revenue from Antero Resources (2024), ~80% from gas/water, regional Appalachian exposure, and limited oil/renewables diversification; this raises single-counterparty, basis-discount, and transition risks. Capex $295M, FCF $230M, net debt/EBITDA 2.8x (2024) leave limited buffer for overruns that could force dividend cuts.

| Metric | 2024 |

|---|---|

| Revenue from Antero Resources | ~90% |

| Gas/water revenue | ~80% |

| Henry Hub avg | $2.70/MMBtu |

| Appalachian basis discount | $1.80/MMBtu |

| Capex | $295M |

| Free cash flow | $230M |

| Net debt / EBITDA | 2.8x |

Full Version Awaits

Antero Midstream Partners SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. You’re previewing the real analysis document; buy now to unlock the complete, detailed version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Antero Midstream’s stable cash flows and strategic Appalachian footprint contrast with commodity exposure and regulatory risks; our concise SWOT preview highlights key operational strengths, leverage concerns, and growth levers worth scrutinizing.

Strengths

Strategic Integration with Antero Resources

The company’s symbiotic tie to Antero Resources, its anchor customer, secured ~65% of volumes in 2024 and delivered predictable cash flow—Antero Resources produced ~3.1 Bcf/d in Appalachia in 2024, much of which flowed through Antero Midstream systems.

Joint development planning lets Antero Midstream time ~$350–400M annual midstream capex to match producer schedules, lowering idle capacity and boosting 2024 adjusted EBITDA margin stability.

High Percentage of Fee-Based Contracts

A significant majority of Antero Midstream Partners’ revenue comes from long-term, fixed-fee contracts—about 75% of cash flow was fee-based in 2024—giving high visibility into future cash flows.

These contracts include minimum volume commitments that shield EBITDA from short-term commodity-price swings and production dips; in 2024 minimums covered roughly 65% of contracted volumes.

This fee-based structure underpinned consistent distributions and funded $150m of 2024 capital projects without large external equity raises.

Robust Free Cash Flow Generation

Leading Appalachian Basin Infrastructure

Antero Midstream owns and operates an interconnected footprint across the Marcellus and Utica shales, the top US gas plays, with ~3,000 miles of gathering pipelines and ~500,000 horsepower of compression (2025 company filings), creating high entry barriers from land, permitting, and corridor constraints.

This physical dominance forms a durable moat, making the firm a critical regional supply chain link and supporting steady fee-based cash flow and volume capture.

- ~3,000 miles pipelines

- ~500,000 HP compression

- Marcellus/Utica = largest US gas production

- High geographic/regulatory entry barriers

Advanced Water Handling Capabilities

Antero Midstream operates a closed-loop water management system covering sourcing, treatment, reuse, and disposal for hydraulic fracturing, cutting truck hauls and emissions. In 2024 the system supported >1,200 well pads, reused ~70% of produced water, and lowered midstream logistics costs by an estimated $8–12 per barrel equivalent.

- Reuses ~70% of produced water

- Supports >1,200 well pads (2024)

- Cuts $8–12 per barrel logistics

High-visibility fee cash flows, $850–900M FCF and regional moat from 3,000-mi pipeline

Anchor customer tie to Antero Resources (≈65% volumes, ~3.1 Bcf/d in 2024) plus ~75% fee-based cash flow in 2024 provides high visibility; coordinated capex ($350–400M/year) stabilized adjusted EBITDA margins; 2025 free cash flow ≈$850–900M funded $300M buybacks, $150M extra dividends and ~$500M net-debt paydown; ~3,000 miles pipelines and ~500,000 HP compression create regional moat.

| Metric | 2024–25 |

|---|---|

| Anchor volumes | ~65% |

| Antero prod. | 3.1 Bcf/d (2024) |

| Fee-based cash | ~75% |

| FCF | $850–900M (2025) |

| Pipelines | ~3,000 miles |

What is included in the product

Provides a concise SWOT overview of Antero Midstream Partners, outlining its operational strengths and weaknesses alongside market opportunities and external threats to assess strategic positioning and future risks.

Delivers a concise SWOT snapshot of Antero Midstream Partners for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Severe Customer Concentration Risk

Antero Midstream Partners depends on Antero Resources for roughly 90% of consolidated revenue in 2024, creating a single-point-of-failure risk in its business model.

Any bankruptcy, production decline, or strategic pivot at Antero Resources would cut cash flows sharply and could breach midstream covenants almost immediately.

Despite a strong current contract portfolio, this extreme customer concentration deters risk-averse institutional investors and raises valuation and refinancing concerns.

Geographic Limitation to Appalachia

Antero Midstream’s operations are confined to the Appalachian Basin, exposing it to regional regulatory shifts, local pipeline bottlenecks, and Marcellus/Utica basis discounts that averaged about 1.80 $/MMBtu below Henry Hub in 2024; unlike peers with Permian or Gulf Coast exposure, it cannot reallocate volumes to higher-margin regions, raising sensitivity to northeastern US political and economic risks and concentrating cash flow volatility from basin-specific outages or takeaway constraints.

Sensitivity to Natural Gas Prices

Although Antero Midstream Partners uses fee-based contracts, its long-term growth links indirectly to Henry Hub natural gas prices; a 2024 average Henry Hub of about 2.70 USD/MMBtu tightened producer drilling budgets and cut completions. If prices stay depressed, Antero Resources may curtail completions, reducing volume growth versus projections and pressuring distributable cash flow. This indirect exposure drove valuation swings in 2022–2024, with shares showing ~40% peak-to-trough volatility.

Limited Non-Gas Revenue Streams

The company earns over 80% of revenues from natural gas gathering and water services (2024 Form 10-K), with negligible crude, refined products, or renewables exposure, concentrating earnings on gas price and demand cycles.

This narrow mix raises transition risk as U.S. gas demand could shift; limited capital spent on renewables or midstream diversification through 2023–2025 keeps appeal low for energy-transition funds.

High Capital Intensity for Expansion

Maintaining and expanding midstream assets needs continuous, large capital outlays that can strain liquidity; Antero Midstream reported $295 million capital expenditures in 2024, down from $410 million in 2023 but still sizable vs free cash flow.

Free cash flow improved to $230 million in 2024, yet pipeline construction and regulatory compliance costs keep pressure on leverage and payout capacity.

Any major cost overruns would threaten leverage targets (net debt/EBITDA 2.8x in 2024) and could force dividend cuts or delayed growth.

- 2024 capex $295M; 2023 $410M

- 2024 free cash flow $230M

- Net debt/EBITDA 2.8x in 2024

- Cost overruns risk dividends and leverage

Concentration Risk: Antero Midstream's 90% Tied to Antero Resources, Tight Leverage

Antero Midstream is highly concentrated: ~90% revenue from Antero Resources (2024), ~80% from gas/water, regional Appalachian exposure, and limited oil/renewables diversification; this raises single-counterparty, basis-discount, and transition risks. Capex $295M, FCF $230M, net debt/EBITDA 2.8x (2024) leave limited buffer for overruns that could force dividend cuts.

| Metric | 2024 |

|---|---|

| Revenue from Antero Resources | ~90% |

| Gas/water revenue | ~80% |

| Henry Hub avg | $2.70/MMBtu |

| Appalachian basis discount | $1.80/MMBtu |

| Capex | $295M |

| Free cash flow | $230M |

| Net debt / EBITDA | 2.8x |

Full Version Awaits

Antero Midstream Partners SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. You’re previewing the real analysis document; buy now to unlock the complete, detailed version immediately after checkout.