Anuvu Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

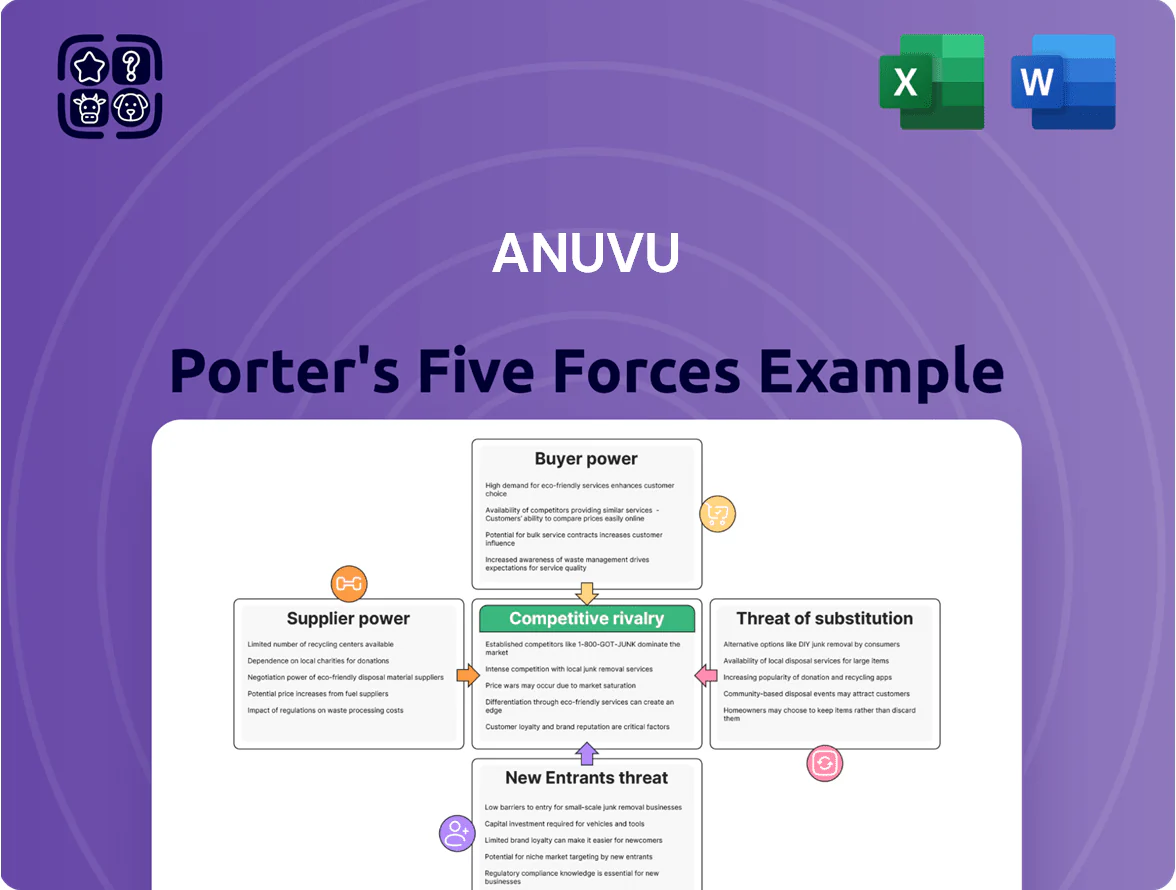

Anuvu faces a complex mix of competitive pressures—from concentrated supplier leverage in satellite capacity to rising substitute threats like terrestrial and LEO connectivity—creating both strategic risks and niche opportunities for differentiated services.

This brief snapshot highlights key dynamics but only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Anuvu’s market position.

Suppliers Bargaining Power

Satellite Capacity Providers

Anuvu depends on third-party satellite operators for bandwidth; with global high-throughput demand up 35% CAGR in 2021–25, suppliers gain pricing power and control over capacity allocation.

The market is concentrated: SES and Telesat control multi-Gbps fleets—SES reported €1.8B revenue in 2024—so Anuvu must keep strong contracts and reserves to avoid service disruption.

Hollywood Studios and Content Owners

The entertainment division relies on licensing from major studios (Disney, Warner Bros. Discovery, NBCUniversal), giving suppliers high bargaining power because premium titles are critical for competitive in-flight entertainment.

In 2024 top studio licensing fees rose ~12% year-over-year; restrictive windowing and territory clauses can raise content costs, squeezing Anuvu’s margins—Anuvu reported entertainment revenue of $38M in FY2024, so a 10% fee hike cuts ~ $3.8M.

Hardware and Component Manufacturers

The specialized antennas and modems for aero/maritime SATCOM come from a handful of aerospace-grade suppliers (e.g., Cobham, Honeywell), concentrating >70% of certified units; in 2024 component lead times averaged 18–30 weeks, elevating installation delays and capex by ~12–20% for operators like Anuvu.

Cloud Infrastructure and Software Vendors

Operational efficiency for Anuvu relies on cloud services from leaders like Amazon Web Services (AWS) and Microsoft Azure; AWS reported $86.7B revenue in 2024, signaling scale that constrains bespoke deals for mid-sized vendors.

Standardized pricing and limited negotiation power raise supplier leverage, while deep tech integration creates high switching costs—migrations often exceed $2M and take 6–12 months.

- Major vendors: AWS, Azure

- AWS 2024 rev: $86.7B

- Limited price negotiation for mid-sized firms

- Switch cost estimate: $2M+, 6–12 months

Regulatory and Spectrum Licensing Bodies

Regulatory bodies control orbital slots and spectrum—resources essential for Anuvu’s satellite links—and can charge licensing fees or impose constraints that raise capex and delay rollouts; the ITU coordinates spectrum, and national regulators like the FCC issued $2.7B in space-related fees/auctions in 2023-2024, highlighting material cost exposure.

Anuvu faces complex cross-border approvals for GEO/LEO use, so regulators wield indirect supplier power by limiting coverage, adding compliance costs, and creating timing risk that can shift revenue recognition and unit economics.

- Regulatory fees: $2.7B (US auctions 2023–24)

- Key regulators: ITU, FCC, ESA, national telecom agencies

- Impact: higher capex, rollout delays, constrained service areas

Concentrated suppliers, rising fees and costly switches squeeze Anuvu margins

Suppliers hold high bargaining power: satellite capacity suppliers (SES, Telesat) and studio licensors (Disney, WBD) are concentrated; 2021–25 satcom demand rose ~35% CAGR and studio fees grew ~12% in 2024, squeezing Anuvu’s margins. Key hardware/cloud vendors (Cobham, Honeywell, AWS) create >70% certification concentration and switching costs >$2M, 6–12 months; regulators (FCC/ITU) add spectrum fees and rollout delays.

| Metric | Value |

|---|---|

| Satcom demand CAGR (2021–25) | ~35% |

| Studio fee rise (2024) | ~12% |

| AWS revenue (2024) | $86.7B |

| Switch cost | $2M+, 6–12m |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and rivalry specific to Anuvu, identifying disruptive threats and strategic levers to protect market share and pricing power.

A concise Porter's Five Forces one-sheet for Anuvu—instantly reveal competitive pressures and prioritize strategic responses.

Customers Bargaining Power

Major Commercial Airlines

Major commercial airlines account for roughly 40–55% of Anuvu’s revenue in recent years, giving them strong bargaining power; large carriers push for customized satcom and in-flight connectivity packages, strict SLAs, and steep discounts at renewal. Airlines often demand multi-year contracts with price resets, forcing Anuvu to absorb higher capex or margin compression—losing one top-5 airline client could cut revenue by >15% in a fiscal year.

Global Cruise Line Operators

Global cruise line operators, led by Carnival Corporation (2024 revenue $18.2B) and Royal Caribbean Group (2024 revenue $11.9B), run large fleets needing multi-Gbps passenger bandwidth, giving them strong buyer power to negotiate lower per-GB rates and prefer bundled services.

Their procurement cycles and ability to switch vendors at contract renewal force Anuvu to cut prices, innovate latency and coverage, and offer SLA credits—Cruise CAPEX per ship often exceeds $500M, so connectivity is negotiable.

Government and Defense Agencies

Government and defense agencies demand highly secure, mission‑critical connectivity, forcing Anuvu to meet strict certifications and bespoke specs; in 2024 US federal IT spending hit $123.3B, showing scale and bargaining clout. Procurement rules and long RFP cycles let buyers dictate technical terms and pricing, yet multi‑year contracts (often 3–10 years) deliver steady, low‑volatility revenue—Anuvu reported government segment growth of ~12% in 2023.

Commercial Shipping and Energy Fleets

- Numerous small accounts reduce single-account leverage

- Collective demand forces tiered pricing and bulk discounts

- 2024–25 LEO price drops ~15–25% increase price sensitivity

- Anuvu responds with flexible SLAs, bulk plans, and segmented bundles

Consolidation of Travel Industry Players

Consolidation in airlines and cruise lines—eg, IAG’s 2024 purchase moves and Carnival Group’s 2024 fleet scale—creates buyers controlling larger fleet pools and stronger negotiating leverage, enabling volume discounts and longer-term contracts that squeeze supplier margins.

Anuvu must shift to enterprise sales, offer fleet-level pricing tiers, and pursue joint-value metrics (revenue per seat, uptime guarantees) to retain deals with consolidated buyers.

- Major buyers grew share: top 5 cruise lines ~60% global capacity (2024)

- Airline M&A raised fleet concentration ~+8% top-10 share (2023–24)

- Action: fleet pricing, SLAs, joint KPIs

Buyers Wield Power: Airlines, Cruise & LEO Price Drops Force Discounts and Rigid SLAs

Buyers hold high bargaining power: top airlines (40–55% revenue) and cruise lines (top 5 ≈60% capacity in 2024) force discounts, SLAs, and multi‑year terms—losing a top‑5 airline can cut revenue >15%. LEO price falls (~15–25% in 2024–25) raised price sensitivity; government contracts (US federal IT $123.3B in 2024) add strict specs but steady revenue.

| Buyer | 2024 stat | Impact |

|---|---|---|

| Airlines | 40–55% revenue | High leverage |

| Cruise | Top5 ≈60% cap | Volume discounts |

| LEO trend | Price −15–25% | Higher sensitivity |

| Government | US IT $123.3B | Strict specs |

Preview the Actual Deliverable

Anuvu Porter's Five Forces Analysis

This preview shows the exact Anuvu Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the professionally formatted final file and will be available for instant download the moment you complete your purchase.

No mockups or samples: what you see is the full, ready-to-use analysis you’ll get upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Anuvu faces a complex mix of competitive pressures—from concentrated supplier leverage in satellite capacity to rising substitute threats like terrestrial and LEO connectivity—creating both strategic risks and niche opportunities for differentiated services.

This brief snapshot highlights key dynamics but only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Anuvu’s market position.

Suppliers Bargaining Power

Satellite Capacity Providers

Anuvu depends on third-party satellite operators for bandwidth; with global high-throughput demand up 35% CAGR in 2021–25, suppliers gain pricing power and control over capacity allocation.

The market is concentrated: SES and Telesat control multi-Gbps fleets—SES reported €1.8B revenue in 2024—so Anuvu must keep strong contracts and reserves to avoid service disruption.

Hollywood Studios and Content Owners

The entertainment division relies on licensing from major studios (Disney, Warner Bros. Discovery, NBCUniversal), giving suppliers high bargaining power because premium titles are critical for competitive in-flight entertainment.

In 2024 top studio licensing fees rose ~12% year-over-year; restrictive windowing and territory clauses can raise content costs, squeezing Anuvu’s margins—Anuvu reported entertainment revenue of $38M in FY2024, so a 10% fee hike cuts ~ $3.8M.

Hardware and Component Manufacturers

The specialized antennas and modems for aero/maritime SATCOM come from a handful of aerospace-grade suppliers (e.g., Cobham, Honeywell), concentrating >70% of certified units; in 2024 component lead times averaged 18–30 weeks, elevating installation delays and capex by ~12–20% for operators like Anuvu.

Cloud Infrastructure and Software Vendors

Operational efficiency for Anuvu relies on cloud services from leaders like Amazon Web Services (AWS) and Microsoft Azure; AWS reported $86.7B revenue in 2024, signaling scale that constrains bespoke deals for mid-sized vendors.

Standardized pricing and limited negotiation power raise supplier leverage, while deep tech integration creates high switching costs—migrations often exceed $2M and take 6–12 months.

- Major vendors: AWS, Azure

- AWS 2024 rev: $86.7B

- Limited price negotiation for mid-sized firms

- Switch cost estimate: $2M+, 6–12 months

Regulatory and Spectrum Licensing Bodies

Regulatory bodies control orbital slots and spectrum—resources essential for Anuvu’s satellite links—and can charge licensing fees or impose constraints that raise capex and delay rollouts; the ITU coordinates spectrum, and national regulators like the FCC issued $2.7B in space-related fees/auctions in 2023-2024, highlighting material cost exposure.

Anuvu faces complex cross-border approvals for GEO/LEO use, so regulators wield indirect supplier power by limiting coverage, adding compliance costs, and creating timing risk that can shift revenue recognition and unit economics.

- Regulatory fees: $2.7B (US auctions 2023–24)

- Key regulators: ITU, FCC, ESA, national telecom agencies

- Impact: higher capex, rollout delays, constrained service areas

Concentrated suppliers, rising fees and costly switches squeeze Anuvu margins

Suppliers hold high bargaining power: satellite capacity suppliers (SES, Telesat) and studio licensors (Disney, WBD) are concentrated; 2021–25 satcom demand rose ~35% CAGR and studio fees grew ~12% in 2024, squeezing Anuvu’s margins. Key hardware/cloud vendors (Cobham, Honeywell, AWS) create >70% certification concentration and switching costs >$2M, 6–12 months; regulators (FCC/ITU) add spectrum fees and rollout delays.

| Metric | Value |

|---|---|

| Satcom demand CAGR (2021–25) | ~35% |

| Studio fee rise (2024) | ~12% |

| AWS revenue (2024) | $86.7B |

| Switch cost | $2M+, 6–12m |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and rivalry specific to Anuvu, identifying disruptive threats and strategic levers to protect market share and pricing power.

A concise Porter's Five Forces one-sheet for Anuvu—instantly reveal competitive pressures and prioritize strategic responses.

Customers Bargaining Power

Major Commercial Airlines

Major commercial airlines account for roughly 40–55% of Anuvu’s revenue in recent years, giving them strong bargaining power; large carriers push for customized satcom and in-flight connectivity packages, strict SLAs, and steep discounts at renewal. Airlines often demand multi-year contracts with price resets, forcing Anuvu to absorb higher capex or margin compression—losing one top-5 airline client could cut revenue by >15% in a fiscal year.

Global Cruise Line Operators

Global cruise line operators, led by Carnival Corporation (2024 revenue $18.2B) and Royal Caribbean Group (2024 revenue $11.9B), run large fleets needing multi-Gbps passenger bandwidth, giving them strong buyer power to negotiate lower per-GB rates and prefer bundled services.

Their procurement cycles and ability to switch vendors at contract renewal force Anuvu to cut prices, innovate latency and coverage, and offer SLA credits—Cruise CAPEX per ship often exceeds $500M, so connectivity is negotiable.

Government and Defense Agencies

Government and defense agencies demand highly secure, mission‑critical connectivity, forcing Anuvu to meet strict certifications and bespoke specs; in 2024 US federal IT spending hit $123.3B, showing scale and bargaining clout. Procurement rules and long RFP cycles let buyers dictate technical terms and pricing, yet multi‑year contracts (often 3–10 years) deliver steady, low‑volatility revenue—Anuvu reported government segment growth of ~12% in 2023.

Commercial Shipping and Energy Fleets

- Numerous small accounts reduce single-account leverage

- Collective demand forces tiered pricing and bulk discounts

- 2024–25 LEO price drops ~15–25% increase price sensitivity

- Anuvu responds with flexible SLAs, bulk plans, and segmented bundles

Consolidation of Travel Industry Players

Consolidation in airlines and cruise lines—eg, IAG’s 2024 purchase moves and Carnival Group’s 2024 fleet scale—creates buyers controlling larger fleet pools and stronger negotiating leverage, enabling volume discounts and longer-term contracts that squeeze supplier margins.

Anuvu must shift to enterprise sales, offer fleet-level pricing tiers, and pursue joint-value metrics (revenue per seat, uptime guarantees) to retain deals with consolidated buyers.

- Major buyers grew share: top 5 cruise lines ~60% global capacity (2024)

- Airline M&A raised fleet concentration ~+8% top-10 share (2023–24)

- Action: fleet pricing, SLAs, joint KPIs

Buyers Wield Power: Airlines, Cruise & LEO Price Drops Force Discounts and Rigid SLAs

Buyers hold high bargaining power: top airlines (40–55% revenue) and cruise lines (top 5 ≈60% capacity in 2024) force discounts, SLAs, and multi‑year terms—losing a top‑5 airline can cut revenue >15%. LEO price falls (~15–25% in 2024–25) raised price sensitivity; government contracts (US federal IT $123.3B in 2024) add strict specs but steady revenue.

| Buyer | 2024 stat | Impact |

|---|---|---|

| Airlines | 40–55% revenue | High leverage |

| Cruise | Top5 ≈60% cap | Volume discounts |

| LEO trend | Price −15–25% | Higher sensitivity |

| Government | US IT $123.3B | Strict specs |

Preview the Actual Deliverable

Anuvu Porter's Five Forces Analysis

This preview shows the exact Anuvu Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the professionally formatted final file and will be available for instant download the moment you complete your purchase.

No mockups or samples: what you see is the full, ready-to-use analysis you’ll get upon payment.