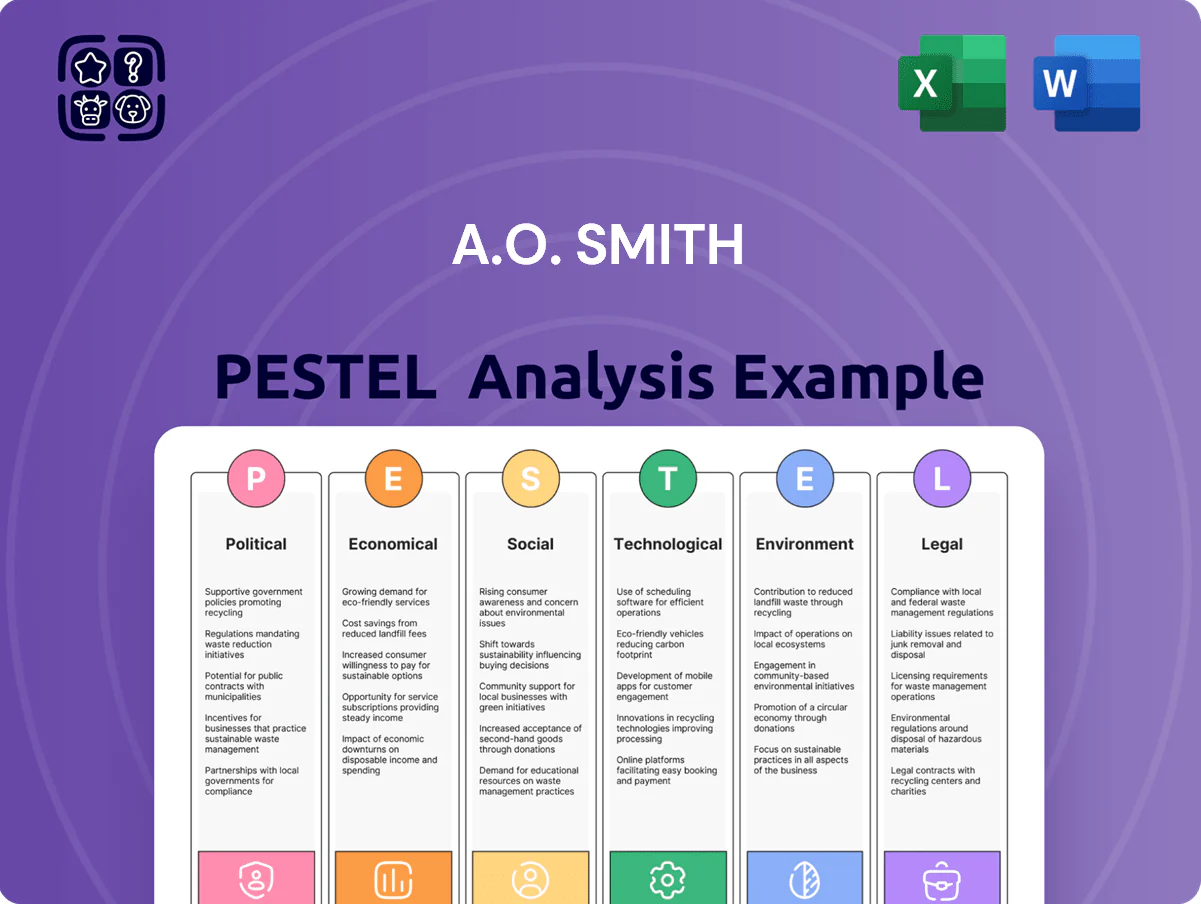

A.O. Smith PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Understand how political shifts, economic cycles, and rapid tech change shape A.O. Smith’s strategy and risks—our concise PESTLE highlights the external forces that matter most. Ideal for investors, consultants, and planners, the full report delivers actionable, editable insights to inform forecasts and boardroom decisions. Purchase the complete PESTLE now for instant access to the deep-dive analysis you need.

Political factors

US-China Trade Relations

Ongoing US-China tensions affect A.O. Smith, which generated about 53% of 2024 revenues from Greater China, exposing it to tariffs and policy shifts that can raise input costs and compress margins; a 10% tariff on imported components could add materially to COGS. Tariff-driven supply disruptions risk higher inventory and logistics expenses, seen in 2023 China operations where operating margin dipped versus US. Political stability is critical to sustain its dual-market strategy and 2024 capex plans of roughly $150–200 million in China.

Government Infrastructure Spending

Federal and state infrastructure bills in the US and Canada—including US bipartisan Infrastructure Investment and Jobs Act allocations ($550B for water and power-related projects through 2026) and Canada’s Investing in Canada Plan—support steady demand for A. O. Smith’s commercial boilers and large-scale water heaters; modernization of public buildings, schools, and hospitals (public construction up 6.8% y/y in US 2024) boosts its commercial segment revenue; shifts in administration can reprioritize funds and alter the institutional project pipeline.

Energy Efficiency Mandates

Political pressure to cut carbon emissions has tightened appliance efficiency standards, prompting A.O. Smith to accelerate R&D into heat pump water heaters; US DOE proposed 2025 efficiency rules could raise minimum SEER/EF targets by ~10-15%, affecting product specs and costs.

Federal and state incentives—IRA tax credits up to $2,000 and Inflation Reduction Act funding that helped boost heat pump water heater shipments by ~30% in 2023—support consumer uptake and higher ASPs for A.O. Smith.

Conversely, a political shift reducing green subsidies or delaying standards would likely slow migration to premium, high-margin units and pressure near-term revenue growth tied to electrification trends.

India Market Expansion Policies

India's push for clean water and urban development, including the Jal Jeevan Mission targeting 100% household tap connections by 2024, creates a large addressable market for A.O. Smith's water treatment products; Jal Jeevan Mission had reached over 90% household coverage by end-2024, indicating strong demand potential.

Political stability and continued ease-of-doing-business reforms—India ranked 63rd in World Bank's 2024 Doing Business indicators—support A.O. Smith's Rest of World expansion and investment confidence.

- Jal Jeevan Mission ~90%+ coverage by 2024

- Urbanization: 35%+ urban population (2024)

- India Doing Business rank 63 (2024)

Global Supply Chain Sovereignty

Rising global emphasis on supply chain sovereignty is prompting A.O. Smith to rethink sourcing of steel and electronic controllers; the U.S. CHIPS and Inflation Reduction Act and EU reshoring incentives have driven a 12-18% rise in domestic procurement costs for many manufacturers in 2024.

Policies favoring near-shoring may force A.O. Smith to reconfigure its logistics network, potentially increasing CAPEX for regional sourcing hubs and raising unit costs if import tariffs and duties are avoided.

Navigating protectionist trends is critical to prevent punitive duties and maintain steady component flow—A.O. Smith reported 2024 supply-chain related margin pressure of ~60-120 bps in comparable peers, highlighting the financial stakes.

- Domestic procurement costs up ~12-18% (2024)

- Supply-chain margin pressure ~60-120 bps (peer benchmark 2024)

- Near-shoring may increase CAPEX for regional hubs

Geopolitics, US infra and IRA spur heat-pump, water-treatment growth amid China risks

US-China tensions (53% of 2024 revenue from Greater China) raise tariff and margin risk; US infrastructure spending ($550B to 2026) boosts commercial demand; tighter efficiency rules (DOE proposed +10–15% targets) accelerate heat pump R&D and raise costs; IRA incentives (up to $2,000) lifted heat pump shipments ~30% in 2023; India Jal Jeevan Mission >90% by 2024 expands water-treatment market.

| Factor | Key metric |

|---|---|

| China revenue | 53% (2024) |

| US infra | $550B to 2026 |

| DOE target rise | +10–15% (proposed 2025) |

| IRA credit | up to $2,000 |

| India coverage | >90% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect A.O. Smith, using region- and industry-specific data to identify risks and opportunities for strategy and investment.

Condenses A.O. Smith's PESTLE into a clear, presentation-ready summary that teams can quickly reference during strategy sessions or client briefings.

Economic factors

Interest Rate Fluctuations

Interest rate fluctuations directly affect borrowing costs and the mortgage market, shaping new home construction and residential replacement cycles; the US 30-year fixed mortgage rose from ~3.0% in Jan 2021 to ~7.0% in Oct 2023 before easing to ~6.3% by Dec 2025, which suppressed new home starts (single‑family starts fell ~20% peak-to-trough in 2022–2023). High rates deter upgrades to premium water heaters and delay projects, while stabilization/declines correlate with increased A.O. Smith residential demand—company revenue from North American residential products grew ~5% year-over-year in 2024 as rates eased.

Raw Material Commodity Pricing

Fluctuations in steel, copper and specialized plastics directly affect A.O. Smith’s COGS—steel rose about 12% in 2024 while copper averaged $8,450/ton in 2025, increasing input costs for its water heater and motor segments.

As a major commodity consumer, A.O. Smith uses procurement hedges and supplier contracts; in FY2024 raw material inflation contributed to a 150–200 basis-point pressure on gross margin.

Failure to pass costs to consumers amid industrial-material inflation can compress margins; A.O. Smith raised prices in late 2024, helping stabilize operating margin to roughly 11% in FY2025.

Consumer Discretionary Spending

Economic cycles shape homeowner spend on A.O. Smith products: in 2024 US real disposable personal income rose 1.2% YoY and housing starts climbed 7%, supporting demand for premium tankless heaters and advanced filtration, which can lift ASPs by 5–8%; conversely the 2023–24 softening in consumer sentiment (Conference Board index down ~6%) pushed buyers toward lower-cost replacements, compressing ASPs and margins.

Currency Exchange Rate Volatility

As a global manufacturer, A.O. Smith faces currency volatility across USD, CNY and INR; in 2024 about 18% of revenue came from China and India, so FX swings materially affect results.

A stronger USD in 2024 reduced reported international earnings and pressured export pricing versus local competitors, compressing margins in APAC.

The firm uses hedging, local sourcing and pricing adjustments; as of FY2024 management reported increased forward contracts and natural hedges to limit FX exposure.

- ~18% revenue from China/India (2024)

- USD strength lowered reported international earnings in 2024

- Mitigations: forward contracts, natural hedges, local pricing

Labor Market Dynamics

- 2024 U.S. wage growth ~4.5% and China ~6%

- U.S. manufacturing openings ~700,000 (2024)

- A.O. Smith capex $228M (2024) targeting automation

- Automation reduces variable labor cost exposure

Mortgage dips, raw-material inflation and wages squeeze margins; automation capex rises

Interest-rate-driven housing trends and real disposable income shifts materially affect residential demand; mortgage rates peaked ~7.0% in Oct 2023 then eased to ~6.3% by Dec 2025, supporting a 5% YoY North American residential revenue rise in 2024. Raw-material inflation (steel +12% in 2024; copper ~$8,450/ton in 2025) trimmed gross margins ~150–200 bps in FY2024; price increases stabilized operating margin ~11% in FY2025. FX exposure (≈18% revenue China/India in 2024) and rising wages (US +4.5%, China +6% in 2024) pushed automation capex $228M in 2024 to protect margins.

| Metric | Value |

|---|---|

| 30y mortgage (Oct 2023) | ~7.0% |

| 30y mortgage (Dec 2025) | ~6.3% |

| North Am residential rev change (2024) | +5% YoY |

| Steel price change (2024) | +12% |

| Copper price (2025) | $8,450/ton |

| Gross margin headwind (FY2024) | 150–200 bps |

| Operating margin (FY2025) | ~11% |

| Revenue from China/India (2024) | ~18% |

| Wage growth (2024) | US +4.5%, China +6% |

| Capex (2024) | $228M |

Preview Before You Purchase

A.O. Smith PESTLE Analysis

The preview shown here is the exact A.O. Smith PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Understand how political shifts, economic cycles, and rapid tech change shape A.O. Smith’s strategy and risks—our concise PESTLE highlights the external forces that matter most. Ideal for investors, consultants, and planners, the full report delivers actionable, editable insights to inform forecasts and boardroom decisions. Purchase the complete PESTLE now for instant access to the deep-dive analysis you need.

Political factors

US-China Trade Relations

Ongoing US-China tensions affect A.O. Smith, which generated about 53% of 2024 revenues from Greater China, exposing it to tariffs and policy shifts that can raise input costs and compress margins; a 10% tariff on imported components could add materially to COGS. Tariff-driven supply disruptions risk higher inventory and logistics expenses, seen in 2023 China operations where operating margin dipped versus US. Political stability is critical to sustain its dual-market strategy and 2024 capex plans of roughly $150–200 million in China.

Government Infrastructure Spending

Federal and state infrastructure bills in the US and Canada—including US bipartisan Infrastructure Investment and Jobs Act allocations ($550B for water and power-related projects through 2026) and Canada’s Investing in Canada Plan—support steady demand for A. O. Smith’s commercial boilers and large-scale water heaters; modernization of public buildings, schools, and hospitals (public construction up 6.8% y/y in US 2024) boosts its commercial segment revenue; shifts in administration can reprioritize funds and alter the institutional project pipeline.

Energy Efficiency Mandates

Political pressure to cut carbon emissions has tightened appliance efficiency standards, prompting A.O. Smith to accelerate R&D into heat pump water heaters; US DOE proposed 2025 efficiency rules could raise minimum SEER/EF targets by ~10-15%, affecting product specs and costs.

Federal and state incentives—IRA tax credits up to $2,000 and Inflation Reduction Act funding that helped boost heat pump water heater shipments by ~30% in 2023—support consumer uptake and higher ASPs for A.O. Smith.

Conversely, a political shift reducing green subsidies or delaying standards would likely slow migration to premium, high-margin units and pressure near-term revenue growth tied to electrification trends.

India Market Expansion Policies

India's push for clean water and urban development, including the Jal Jeevan Mission targeting 100% household tap connections by 2024, creates a large addressable market for A.O. Smith's water treatment products; Jal Jeevan Mission had reached over 90% household coverage by end-2024, indicating strong demand potential.

Political stability and continued ease-of-doing-business reforms—India ranked 63rd in World Bank's 2024 Doing Business indicators—support A.O. Smith's Rest of World expansion and investment confidence.

- Jal Jeevan Mission ~90%+ coverage by 2024

- Urbanization: 35%+ urban population (2024)

- India Doing Business rank 63 (2024)

Global Supply Chain Sovereignty

Rising global emphasis on supply chain sovereignty is prompting A.O. Smith to rethink sourcing of steel and electronic controllers; the U.S. CHIPS and Inflation Reduction Act and EU reshoring incentives have driven a 12-18% rise in domestic procurement costs for many manufacturers in 2024.

Policies favoring near-shoring may force A.O. Smith to reconfigure its logistics network, potentially increasing CAPEX for regional sourcing hubs and raising unit costs if import tariffs and duties are avoided.

Navigating protectionist trends is critical to prevent punitive duties and maintain steady component flow—A.O. Smith reported 2024 supply-chain related margin pressure of ~60-120 bps in comparable peers, highlighting the financial stakes.

- Domestic procurement costs up ~12-18% (2024)

- Supply-chain margin pressure ~60-120 bps (peer benchmark 2024)

- Near-shoring may increase CAPEX for regional hubs

Geopolitics, US infra and IRA spur heat-pump, water-treatment growth amid China risks

US-China tensions (53% of 2024 revenue from Greater China) raise tariff and margin risk; US infrastructure spending ($550B to 2026) boosts commercial demand; tighter efficiency rules (DOE proposed +10–15% targets) accelerate heat pump R&D and raise costs; IRA incentives (up to $2,000) lifted heat pump shipments ~30% in 2023; India Jal Jeevan Mission >90% by 2024 expands water-treatment market.

| Factor | Key metric |

|---|---|

| China revenue | 53% (2024) |

| US infra | $550B to 2026 |

| DOE target rise | +10–15% (proposed 2025) |

| IRA credit | up to $2,000 |

| India coverage | >90% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect A.O. Smith, using region- and industry-specific data to identify risks and opportunities for strategy and investment.

Condenses A.O. Smith's PESTLE into a clear, presentation-ready summary that teams can quickly reference during strategy sessions or client briefings.

Economic factors

Interest Rate Fluctuations

Interest rate fluctuations directly affect borrowing costs and the mortgage market, shaping new home construction and residential replacement cycles; the US 30-year fixed mortgage rose from ~3.0% in Jan 2021 to ~7.0% in Oct 2023 before easing to ~6.3% by Dec 2025, which suppressed new home starts (single‑family starts fell ~20% peak-to-trough in 2022–2023). High rates deter upgrades to premium water heaters and delay projects, while stabilization/declines correlate with increased A.O. Smith residential demand—company revenue from North American residential products grew ~5% year-over-year in 2024 as rates eased.

Raw Material Commodity Pricing

Fluctuations in steel, copper and specialized plastics directly affect A.O. Smith’s COGS—steel rose about 12% in 2024 while copper averaged $8,450/ton in 2025, increasing input costs for its water heater and motor segments.

As a major commodity consumer, A.O. Smith uses procurement hedges and supplier contracts; in FY2024 raw material inflation contributed to a 150–200 basis-point pressure on gross margin.

Failure to pass costs to consumers amid industrial-material inflation can compress margins; A.O. Smith raised prices in late 2024, helping stabilize operating margin to roughly 11% in FY2025.

Consumer Discretionary Spending

Economic cycles shape homeowner spend on A.O. Smith products: in 2024 US real disposable personal income rose 1.2% YoY and housing starts climbed 7%, supporting demand for premium tankless heaters and advanced filtration, which can lift ASPs by 5–8%; conversely the 2023–24 softening in consumer sentiment (Conference Board index down ~6%) pushed buyers toward lower-cost replacements, compressing ASPs and margins.

Currency Exchange Rate Volatility

As a global manufacturer, A.O. Smith faces currency volatility across USD, CNY and INR; in 2024 about 18% of revenue came from China and India, so FX swings materially affect results.

A stronger USD in 2024 reduced reported international earnings and pressured export pricing versus local competitors, compressing margins in APAC.

The firm uses hedging, local sourcing and pricing adjustments; as of FY2024 management reported increased forward contracts and natural hedges to limit FX exposure.

- ~18% revenue from China/India (2024)

- USD strength lowered reported international earnings in 2024

- Mitigations: forward contracts, natural hedges, local pricing

Labor Market Dynamics

- 2024 U.S. wage growth ~4.5% and China ~6%

- U.S. manufacturing openings ~700,000 (2024)

- A.O. Smith capex $228M (2024) targeting automation

- Automation reduces variable labor cost exposure

Mortgage dips, raw-material inflation and wages squeeze margins; automation capex rises

Interest-rate-driven housing trends and real disposable income shifts materially affect residential demand; mortgage rates peaked ~7.0% in Oct 2023 then eased to ~6.3% by Dec 2025, supporting a 5% YoY North American residential revenue rise in 2024. Raw-material inflation (steel +12% in 2024; copper ~$8,450/ton in 2025) trimmed gross margins ~150–200 bps in FY2024; price increases stabilized operating margin ~11% in FY2025. FX exposure (≈18% revenue China/India in 2024) and rising wages (US +4.5%, China +6% in 2024) pushed automation capex $228M in 2024 to protect margins.

| Metric | Value |

|---|---|

| 30y mortgage (Oct 2023) | ~7.0% |

| 30y mortgage (Dec 2025) | ~6.3% |

| North Am residential rev change (2024) | +5% YoY |

| Steel price change (2024) | +12% |

| Copper price (2025) | $8,450/ton |

| Gross margin headwind (FY2024) | 150–200 bps |

| Operating margin (FY2025) | ~11% |

| Revenue from China/India (2024) | ~18% |

| Wage growth (2024) | US +4.5%, China +6% |

| Capex (2024) | $228M |

Preview Before You Purchase

A.O. Smith PESTLE Analysis

The preview shown here is the exact A.O. Smith PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.