Apex Oil PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how geopolitical shifts, regulatory pressure, and energy transition trends are reshaping Apex Oil’s strategic landscape—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions. Purchase the full PESTLE analysis for a comprehensive, actionable report with data-driven insights ready for investment, strategic planning, or competitive analysis.

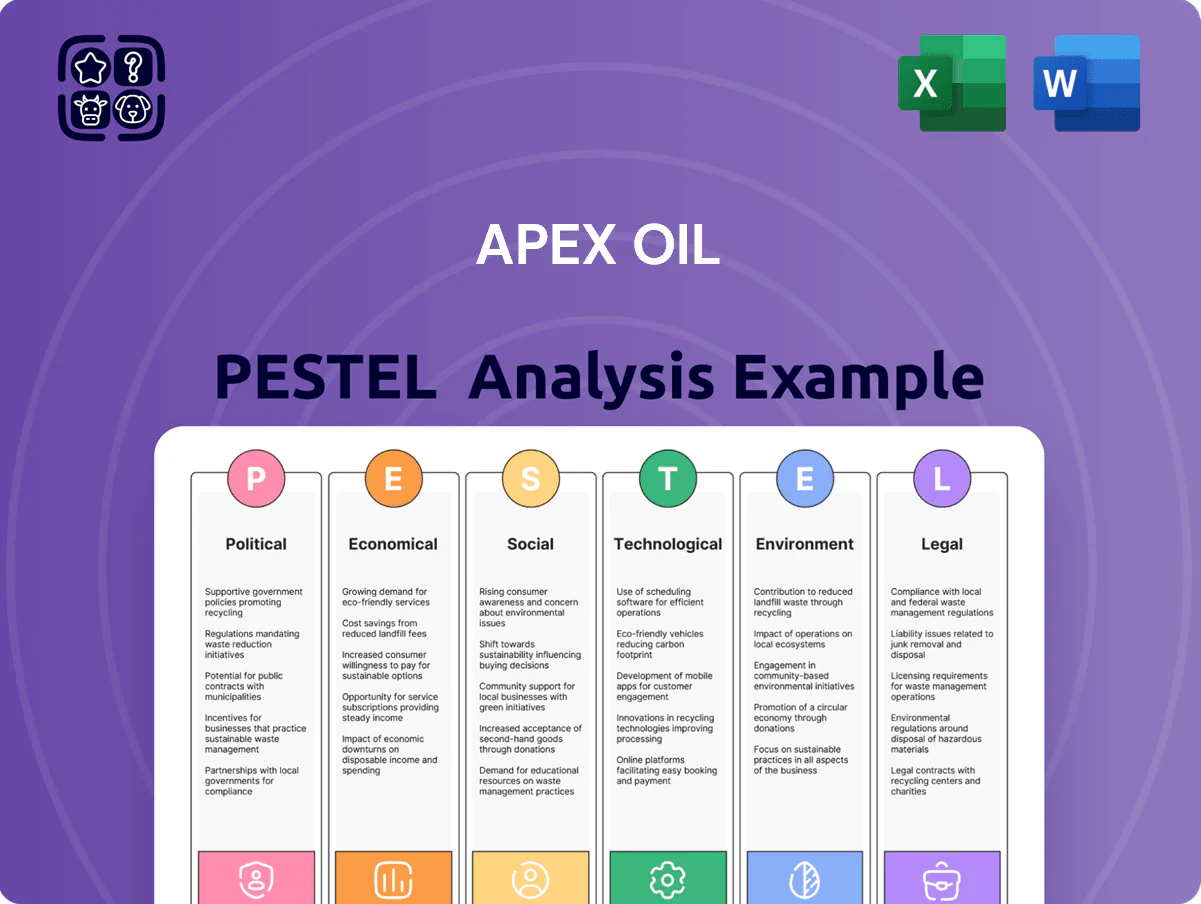

Political factors

Federal Energy Policy Shifts

The post-2024 administration priorities shape regulation through 2025, with federal mandates boosting domestic crude output targets by ~5% YoY and approving $12.5B for pipeline resilience, directly affecting refined volumes via Midwest–Gulf routes (~+3.8% throughput in 2024); Apex Oil must revise forecasts as subsidy caps fall by $4–6B and federal energy-security reserves target a 10% increase in available refined products.

Geopolitical Influence on Supply Chains

Ongoing tensions in Middle East and Eastern Europe drove Brent crude volatility to a 2025 YTD range of 68–102 USD/bbl, forcing Apex to bolster diversified sourcing—imports from 6 supplier regions rose 22% in H1 2025—and maintain terminal inventories equivalent to 45 days of throughput to buffer shocks.

Government Procurement and Defense Contracts

As a major supplier to federal and state agencies, Apex Oil’s revenues are sensitive to budget shifts: US federal defense fuel procurement was about $12.5 billion in 2024, and a 5% cut in military fuel buys could reduce Apex’s diesel/jet volume materially. State transit fuel allocations (roughly $3.2 billion nationwide in 2024) similarly affect demand for wholesale diesel. Rigorous compliance with FAR bidding rules and political vetting is essential to retaining high-volume contracts.

Regional Regulatory Variations

Operating across the Midwest and Gulf Coast exposes Apex Oil to a patchwork of state policies that can diverge from federal rules; in 2024, 7 Midwestern states enacted biofuel mandates increasing ethanol blending targets by up to 2 percentage points while Texas and Louisiana continued incentives for refinery investment totaling $1.1 billion.

Apex must balance regions pushing accelerated biofuel adoption—projected to raise regional biodiesel demand by 12% by 2025—against states preserving petroleum jobs, adjusting terminal allocations and transport routes to avoid capacity bottlenecks and comply with varying permitting timelines.

Trade Policy and Import Export Tariffs

Trade relations between the United States and energy partners shape costs for refined products and blending components; in 2024 US petroleum product imports averaged about 6.2 million barrels per month, influencing feedstock pricing for Apex Oil.

Tariff changes or revised trade agreements can shift margins for barge operations and terminal storage—US Gulf Coast barge rates swung 12% in 2024 when import duties and fuel costs shifted.

Apex tracks political developments and adjusts pricing models; by Q3 2025 the company targeted a 3–5% margin protection through dynamic tariff-linked pricing and storage optimization.

- US petroleum imports ~6.2M bbl/month (2024)

- Barge rates volatility ~12% in 2024

- Margin protection target 3–5% via pricing adjustments (Q3 2025)

Apex must flex logistics as policy, biofuel demand lift crude and squeeze 3–5% margins

Federal energy policy through 2025 raised domestic crude targets ~5% YoY and approved $12.5B for pipeline resilience; Brent ranged 68–102 USD/bbl (2025 YTD), US petroleum imports ~6.2M bbl/mo (2024), Midwestern biofuel mandates tightened in 7 states (2024) boosting regional biodiesel demand ~+12% by 2025; Apex must flex terminals/logistics and protect 3–5% margins via dynamic pricing.

| Metric | Value |

|---|---|

| Pipeline resilience funding | 12.5B USD |

| Domestic crude target change | +5% YoY |

| Brent 2025 YTD range | 68–102 USD/bbl |

| US petroleum imports (2024) | 6.2M bbl/mo |

| States tightening biofuel mandates (2024) | 7 |

| Regional biodiesel demand change | +12% by 2025 |

| Targeted margin protection (Q3 2025) | 3–5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Apex Oil across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary of Apex Oil that’s editable for local context, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Volatility in Global Commodity Pricing

Fluctuations in crude oil—Brent dropped from ~US$95/bbl in Jan 2025 to ~US$72/bbl by Dec 2025—directly compressed Apex Oil’s wholesale margins and forced inventory write-downs, reducing 2025 gross margin by an estimated 180–220 basis points. Rapid swings require sophisticated hedging: industry data show 60% of global downstream firms increased derivatives coverage in 2025 to mitigate price shocks. Capital for terminal expansions depends on energy market health; oil sector free cash flow fell ~15% y/y in 2025, tightening expansion funding.

Inflation and Operational Cost Pressures

Persistent inflationary pressures through 2025 raised labor and maintenance costs by about 6–8% year-over-year, while diesel and marine fuel averaged $3.10–$3.40/gal in 2025, increasing barge operating costs for Apex. Terminal upkeep and equipment replacement costs climbed ~7%, squeezing margins as wholesale gasoline crack spreads averaged near $10/bbl. Managing these overheads is critical to protect EBITDA, which for regional midstream peers fell 200–400 bps in 2024–25.

Industrial and Commercial Demand Cycles

Midwest manufacturing and construction output—which contributed about 22% of US industrial GDP in 2024—directly drives demand for industrial fuels and lubricants, so a 1.8% regional contraction in 2024 cut Apex Oil terminal throughput by an estimated 6–8%.

Reduced industrial activity lowered barge fleet utilization to roughly 62% in 2024 versus 71% in 2022, pressuring revenue per barrel.

Conversely, ISM Midwest indices rebounded in late 2025, offering Apex potential volume expansion and market-share gains if capacity and logistics are optimized.

Interest Rates and Capital Expenditure

At end-2025, US 10-year Treasury yields hovered around 4.2% and the Fed funds target near 5.25%, raising Apex Oil’s borrowing costs and lifting the internal hurdle rate for new terminal and storage modernization projects.

Higher rates make large-scale capex and acquisitions more expensive, so Apex must time deployments to expected monetary easing or lock in fixed-rate financing to preserve project IRRs.

- End-2025 benchmarks: 10y Treasury ~4.2%, Fed funds ~5.25%

Energy Transition and Market Substitution

The shift to EVs and renewables threatens long-term petroleum demand; IEA projects global EVs could reach 260–300 million by 2030, cutting oil demand growth and lowering gasoline volumes.

Apex should assess CAPEX and IRR for biofuels and hydrogen hubs—green hydrogen costs fell to ~$2.5–3.5/kg (2024 PPA-driven) in best cases, needing cost parity with fossil fuels to be viable.

Transition pace hinges on price parity: oil at $70–100/bbl vs declining LCOE and falling electrolyzer costs; scenario modeling is essential.

- IEA: 260–300M EVs by 2030

- Green H2 cost range ~$2.5–3.5/kg (2024 best cases)

- Oil price parity target ~$70–100/bbl impacts demand

Market squeeze: lower oil, higher rates cut FCF; EVs and green H2 force CAPEX shift

Economic headwinds in 2024–25—Brent fall to ~$72/bbl (Dec‑2025), US 10y ~4.2%, Fed funds ~5.25%—compressed margins, raised borrowing costs and cut FCF ~15% y/y; regional industrial contraction (~1.8% in 2024) trimmed throughput ~6–8% and barge utilization to ~62%; EVs 260–300M by 2030 and green H2 ~$2.5–3.5/kg force CAPEX reallocation and scenario-based IRR adjustments.

| Metric | 2024–25 Value |

|---|---|

| Brent (Dec‑25) | ~$72/bbl |

| US 10y | ~4.2% |

| Fed funds | ~5.25% |

| Oil sector FCF | -15% y/y |

| Barge utilization | ~62% |

| EVs by 2030 (IEA) | 260–300M |

Preview Before You Purchase

Apex Oil PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Apex Oil PESTLE Analysis provides structured insights into political, economic, social, technological, legal, and environmental factors affecting the company. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how geopolitical shifts, regulatory pressure, and energy transition trends are reshaping Apex Oil’s strategic landscape—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions. Purchase the full PESTLE analysis for a comprehensive, actionable report with data-driven insights ready for investment, strategic planning, or competitive analysis.

Political factors

Federal Energy Policy Shifts

The post-2024 administration priorities shape regulation through 2025, with federal mandates boosting domestic crude output targets by ~5% YoY and approving $12.5B for pipeline resilience, directly affecting refined volumes via Midwest–Gulf routes (~+3.8% throughput in 2024); Apex Oil must revise forecasts as subsidy caps fall by $4–6B and federal energy-security reserves target a 10% increase in available refined products.

Geopolitical Influence on Supply Chains

Ongoing tensions in Middle East and Eastern Europe drove Brent crude volatility to a 2025 YTD range of 68–102 USD/bbl, forcing Apex to bolster diversified sourcing—imports from 6 supplier regions rose 22% in H1 2025—and maintain terminal inventories equivalent to 45 days of throughput to buffer shocks.

Government Procurement and Defense Contracts

As a major supplier to federal and state agencies, Apex Oil’s revenues are sensitive to budget shifts: US federal defense fuel procurement was about $12.5 billion in 2024, and a 5% cut in military fuel buys could reduce Apex’s diesel/jet volume materially. State transit fuel allocations (roughly $3.2 billion nationwide in 2024) similarly affect demand for wholesale diesel. Rigorous compliance with FAR bidding rules and political vetting is essential to retaining high-volume contracts.

Regional Regulatory Variations

Operating across the Midwest and Gulf Coast exposes Apex Oil to a patchwork of state policies that can diverge from federal rules; in 2024, 7 Midwestern states enacted biofuel mandates increasing ethanol blending targets by up to 2 percentage points while Texas and Louisiana continued incentives for refinery investment totaling $1.1 billion.

Apex must balance regions pushing accelerated biofuel adoption—projected to raise regional biodiesel demand by 12% by 2025—against states preserving petroleum jobs, adjusting terminal allocations and transport routes to avoid capacity bottlenecks and comply with varying permitting timelines.

Trade Policy and Import Export Tariffs

Trade relations between the United States and energy partners shape costs for refined products and blending components; in 2024 US petroleum product imports averaged about 6.2 million barrels per month, influencing feedstock pricing for Apex Oil.

Tariff changes or revised trade agreements can shift margins for barge operations and terminal storage—US Gulf Coast barge rates swung 12% in 2024 when import duties and fuel costs shifted.

Apex tracks political developments and adjusts pricing models; by Q3 2025 the company targeted a 3–5% margin protection through dynamic tariff-linked pricing and storage optimization.

- US petroleum imports ~6.2M bbl/month (2024)

- Barge rates volatility ~12% in 2024

- Margin protection target 3–5% via pricing adjustments (Q3 2025)

Apex must flex logistics as policy, biofuel demand lift crude and squeeze 3–5% margins

Federal energy policy through 2025 raised domestic crude targets ~5% YoY and approved $12.5B for pipeline resilience; Brent ranged 68–102 USD/bbl (2025 YTD), US petroleum imports ~6.2M bbl/mo (2024), Midwestern biofuel mandates tightened in 7 states (2024) boosting regional biodiesel demand ~+12% by 2025; Apex must flex terminals/logistics and protect 3–5% margins via dynamic pricing.

| Metric | Value |

|---|---|

| Pipeline resilience funding | 12.5B USD |

| Domestic crude target change | +5% YoY |

| Brent 2025 YTD range | 68–102 USD/bbl |

| US petroleum imports (2024) | 6.2M bbl/mo |

| States tightening biofuel mandates (2024) | 7 |

| Regional biodiesel demand change | +12% by 2025 |

| Targeted margin protection (Q3 2025) | 3–5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Apex Oil across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary of Apex Oil that’s editable for local context, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Volatility in Global Commodity Pricing

Fluctuations in crude oil—Brent dropped from ~US$95/bbl in Jan 2025 to ~US$72/bbl by Dec 2025—directly compressed Apex Oil’s wholesale margins and forced inventory write-downs, reducing 2025 gross margin by an estimated 180–220 basis points. Rapid swings require sophisticated hedging: industry data show 60% of global downstream firms increased derivatives coverage in 2025 to mitigate price shocks. Capital for terminal expansions depends on energy market health; oil sector free cash flow fell ~15% y/y in 2025, tightening expansion funding.

Inflation and Operational Cost Pressures

Persistent inflationary pressures through 2025 raised labor and maintenance costs by about 6–8% year-over-year, while diesel and marine fuel averaged $3.10–$3.40/gal in 2025, increasing barge operating costs for Apex. Terminal upkeep and equipment replacement costs climbed ~7%, squeezing margins as wholesale gasoline crack spreads averaged near $10/bbl. Managing these overheads is critical to protect EBITDA, which for regional midstream peers fell 200–400 bps in 2024–25.

Industrial and Commercial Demand Cycles

Midwest manufacturing and construction output—which contributed about 22% of US industrial GDP in 2024—directly drives demand for industrial fuels and lubricants, so a 1.8% regional contraction in 2024 cut Apex Oil terminal throughput by an estimated 6–8%.

Reduced industrial activity lowered barge fleet utilization to roughly 62% in 2024 versus 71% in 2022, pressuring revenue per barrel.

Conversely, ISM Midwest indices rebounded in late 2025, offering Apex potential volume expansion and market-share gains if capacity and logistics are optimized.

Interest Rates and Capital Expenditure

At end-2025, US 10-year Treasury yields hovered around 4.2% and the Fed funds target near 5.25%, raising Apex Oil’s borrowing costs and lifting the internal hurdle rate for new terminal and storage modernization projects.

Higher rates make large-scale capex and acquisitions more expensive, so Apex must time deployments to expected monetary easing or lock in fixed-rate financing to preserve project IRRs.

- End-2025 benchmarks: 10y Treasury ~4.2%, Fed funds ~5.25%

Energy Transition and Market Substitution

The shift to EVs and renewables threatens long-term petroleum demand; IEA projects global EVs could reach 260–300 million by 2030, cutting oil demand growth and lowering gasoline volumes.

Apex should assess CAPEX and IRR for biofuels and hydrogen hubs—green hydrogen costs fell to ~$2.5–3.5/kg (2024 PPA-driven) in best cases, needing cost parity with fossil fuels to be viable.

Transition pace hinges on price parity: oil at $70–100/bbl vs declining LCOE and falling electrolyzer costs; scenario modeling is essential.

- IEA: 260–300M EVs by 2030

- Green H2 cost range ~$2.5–3.5/kg (2024 best cases)

- Oil price parity target ~$70–100/bbl impacts demand

Market squeeze: lower oil, higher rates cut FCF; EVs and green H2 force CAPEX shift

Economic headwinds in 2024–25—Brent fall to ~$72/bbl (Dec‑2025), US 10y ~4.2%, Fed funds ~5.25%—compressed margins, raised borrowing costs and cut FCF ~15% y/y; regional industrial contraction (~1.8% in 2024) trimmed throughput ~6–8% and barge utilization to ~62%; EVs 260–300M by 2030 and green H2 ~$2.5–3.5/kg force CAPEX reallocation and scenario-based IRR adjustments.

| Metric | 2024–25 Value |

|---|---|

| Brent (Dec‑25) | ~$72/bbl |

| US 10y | ~4.2% |

| Fed funds | ~5.25% |

| Oil sector FCF | -15% y/y |

| Barge utilization | ~62% |

| EVs by 2030 (IEA) | 260–300M |

Preview Before You Purchase

Apex Oil PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Apex Oil PESTLE Analysis provides structured insights into political, economic, social, technological, legal, and environmental factors affecting the company. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.