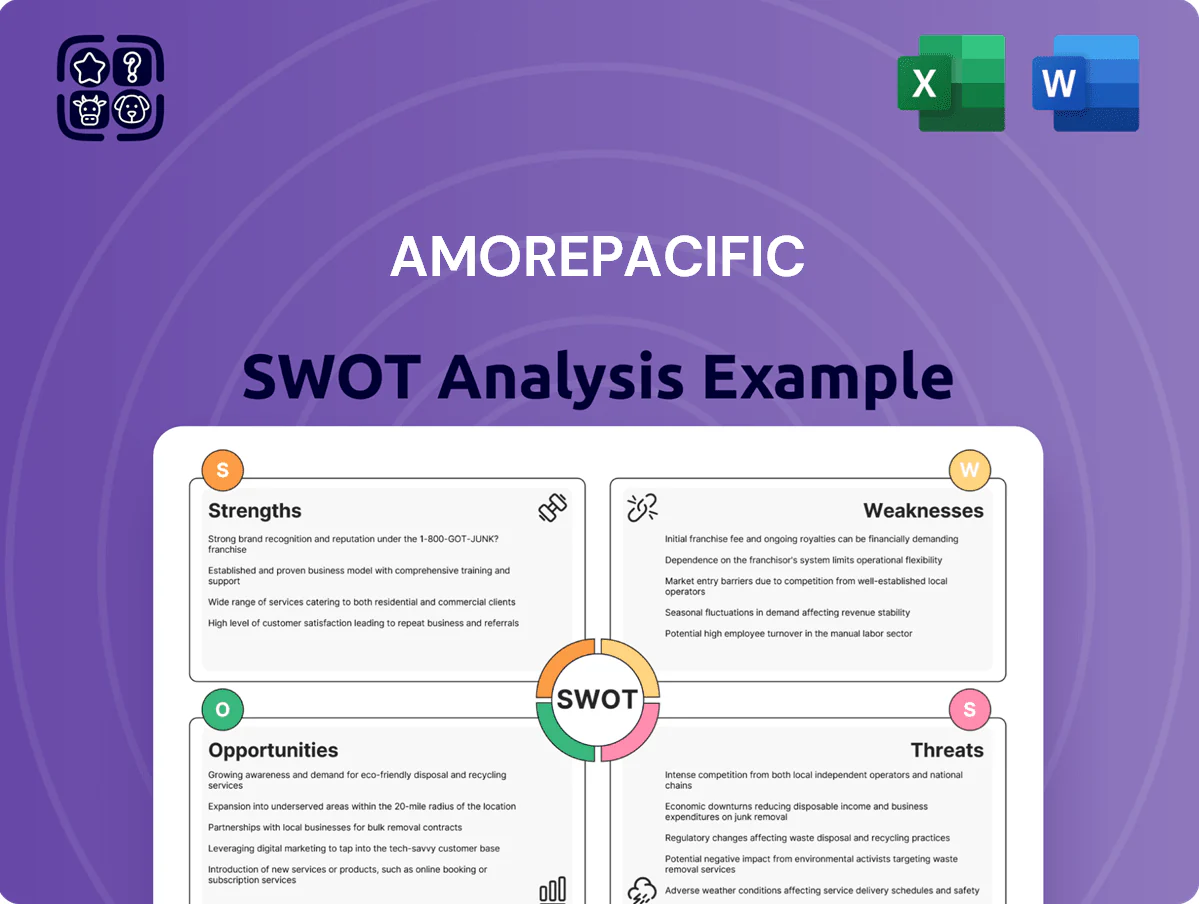

Amorepacific SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Amorepacific combines premium brand equity and a diversified Asian footprint with strong R&D in K-beauty, but faces margin pressure from intense competition and supply-chain risks; regulatory shifts and digital disruption are both threats and opportunities for expansion. Discover the full SWOT analysis for investor-ready insights, editable deliverables, and strategic recommendations to inform your next move—available for purchase.

Strengths

Leading R&D and Heritage Ingredient Integration

Amorepacific blends Asian botanicals like ginseng and green tea with molecular R&D, and by end-2025 its four proprietary research centers reported 28 patent families tied to efficacy claims, underpinning high-performance formulas.

This nature-plus-tech positioning drives premium SKU pricing—luxury brands grew 12% YoY in 2024—differentiating Amorepacific from many Western rivals lacking heritage-based narratives.

Robust Multi-Tier Brand Portfolio

Amorepacific runs a multi-tier portfolio from Sulwhasoo (luxury) to Innisfree (mass) letting it capture consumers across income bands and regions; beauty segment revenue mix was ~42% domestic, 58% international in FY2024 (KRW basis).

Brand diversification cut single-brand risk and boosted ASPs; premium lines lifted group gross margin by ~210 bps in 2024 versus 2022.

By late 2025 Laneige’s repositioning increased global millennial/Gen Z sales share to ~28% of brand revenue, strengthening growth in skincare and online channels.

Advanced Digital Transformation and Direct-to-Consumer Growth

Strong Cultural Capital via K-Beauty Influence

- Global K‑beauty market $50.6B (2024)

- US sales +12% (Amorepacific, 2024)

- ASEAN e‑commerce +20% YoY (2024)

- Lowered CAC via organic cultural reach

Commitment to ESG and Sustainable Innovation

- 42% emissions cut target vs 2019

- 70% recycled-content packaging in core SKUs

- 6% revenue uplift in 2024 from eco lines

Amorepacific: Botanical patents, premium pricing drive luxury +12% and 48% online

Amorepacific pairs Asian botanicals and 28 patent families (end‑2025) with premium pricing; luxury SKU growth +12% YoY (2024) and group gross margin +210 bps vs 2022.

Multi‑brand portfolio (Sulwhasoo–Innisfree) split 42% domestic/58% international (FY2024); online sales 48% of revenue (FY2024).

| Metric | Value |

|---|---|

| Patents (2025) | 28 families |

| Luxury growth (2024) | +12% YoY |

| Online sales (FY2024) | 48% |

| Revenue mix (FY2024) | 42% KR / 58% Intl |

What is included in the product

Provides a concise SWOT overview of Amorepacific, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic positioning and growth prospects.

Delivers a concise Amorepacific SWOT matrix for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Concentration Risk in Specific Geographic Regions

High Operating Costs for Brand Maintenance

Maintaining Amorepacific’s global position demands heavy marketing and celebrity deals; the company spent ₩522.4 billion on selling and administrative expenses in 2024, squeezing operating margin to about 6.8% in FY2024 when global demand slowed.

R&D and product innovation add pressure: Amorepacific invested ₩72.3 billion in R&D in 2024, costs that need multi-year horizons to pay off and reduce near-term profitability risk.

Vulnerability to Travel Retail Fluctuations

Amorepacific depends heavily on duty-free channels—these accounted for about 18% of group sales in 2023—so fluctuations in international travel hit revenue fast; for example, Korea duty-free sales fell 40% in 2020 and bounced unevenly, leaving FY2022 duty-free recovery still ~15% below 2019 levels. Any health crisis or geopolitics can thus cause immediate, sharp shortfalls, reducing resilience to travel-sector shocks.

Complex Organizational Structure and Brand Overlap

The vast Amorepacific portfolio — 30+ brands and 2024 consolidated revenue KRW 6.4 trillion — creates internal cannibalization and consumer confusion, especially in the crowded mid-range segment where Mamonde and Etude overlap.

Overlapping SKUs dilute brand identity and marketing ROI; administrative overhead for governance and 2024 operating margin 8.7% can slow agile launches and decisions.

- 30+ brands (2024)

- KRW 6.4T revenue (2024)

- Operating margin 8.7% (2024)

- Mid-range SKU overlap hurts brand clarity

- Higher admin cost slows decisions

Slower Market Penetration in Western Mass Retail

Amorepacific excels in prestige channels but lags in securing shelf space in high-volume Western drugstores and supermarkets, limiting access to price-sensitive shoppers.

The brand prioritized specialty retailers like Sephora in North America and Europe, so mass-market penetration remains under 10% of its Western retail footprint as of 2025.

This restricted presence reduces revenue upside versus local mass brands that capture large volume—e.g., U.S. drugstore chains generated over $40B in beauty sales in 2024.

- Prestige-focused distribution

- Mass-market share <10% in West (2025)

- Missed access to $40B+ U.S. drugstore beauty market

Amorepacific: East‑Asia concentration and high costs fuel volatile, margin‑pressed growth

| Metric | Value |

|---|---|

| East Asia rev share (FY2025) | 62% |

| China share | 41% |

| S. Korea share | 21% |

| Duty-free sales (2023) | 18% |

| SG&A (2024) | ₩522.4B |

| R&D (2024) | ₩72.3B |

| Operating margin (2024) | 8.7% |

| Brands (2024) | 30+ |

| Mass-market West share (2025) | <10% |

Full Version Awaits

Amorepacific SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the same editable file delivered after checkout. You’re viewing a live excerpt of the complete, structured Amorepacific SWOT analysis; buy now to unlock the full, detailed report.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Amorepacific combines premium brand equity and a diversified Asian footprint with strong R&D in K-beauty, but faces margin pressure from intense competition and supply-chain risks; regulatory shifts and digital disruption are both threats and opportunities for expansion. Discover the full SWOT analysis for investor-ready insights, editable deliverables, and strategic recommendations to inform your next move—available for purchase.

Strengths

Leading R&D and Heritage Ingredient Integration

Amorepacific blends Asian botanicals like ginseng and green tea with molecular R&D, and by end-2025 its four proprietary research centers reported 28 patent families tied to efficacy claims, underpinning high-performance formulas.

This nature-plus-tech positioning drives premium SKU pricing—luxury brands grew 12% YoY in 2024—differentiating Amorepacific from many Western rivals lacking heritage-based narratives.

Robust Multi-Tier Brand Portfolio

Amorepacific runs a multi-tier portfolio from Sulwhasoo (luxury) to Innisfree (mass) letting it capture consumers across income bands and regions; beauty segment revenue mix was ~42% domestic, 58% international in FY2024 (KRW basis).

Brand diversification cut single-brand risk and boosted ASPs; premium lines lifted group gross margin by ~210 bps in 2024 versus 2022.

By late 2025 Laneige’s repositioning increased global millennial/Gen Z sales share to ~28% of brand revenue, strengthening growth in skincare and online channels.

Advanced Digital Transformation and Direct-to-Consumer Growth

Strong Cultural Capital via K-Beauty Influence

- Global K‑beauty market $50.6B (2024)

- US sales +12% (Amorepacific, 2024)

- ASEAN e‑commerce +20% YoY (2024)

- Lowered CAC via organic cultural reach

Commitment to ESG and Sustainable Innovation

- 42% emissions cut target vs 2019

- 70% recycled-content packaging in core SKUs

- 6% revenue uplift in 2024 from eco lines

Amorepacific: Botanical patents, premium pricing drive luxury +12% and 48% online

Amorepacific pairs Asian botanicals and 28 patent families (end‑2025) with premium pricing; luxury SKU growth +12% YoY (2024) and group gross margin +210 bps vs 2022.

Multi‑brand portfolio (Sulwhasoo–Innisfree) split 42% domestic/58% international (FY2024); online sales 48% of revenue (FY2024).

| Metric | Value |

|---|---|

| Patents (2025) | 28 families |

| Luxury growth (2024) | +12% YoY |

| Online sales (FY2024) | 48% |

| Revenue mix (FY2024) | 42% KR / 58% Intl |

What is included in the product

Provides a concise SWOT overview of Amorepacific, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic positioning and growth prospects.

Delivers a concise Amorepacific SWOT matrix for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Concentration Risk in Specific Geographic Regions

High Operating Costs for Brand Maintenance

Maintaining Amorepacific’s global position demands heavy marketing and celebrity deals; the company spent ₩522.4 billion on selling and administrative expenses in 2024, squeezing operating margin to about 6.8% in FY2024 when global demand slowed.

R&D and product innovation add pressure: Amorepacific invested ₩72.3 billion in R&D in 2024, costs that need multi-year horizons to pay off and reduce near-term profitability risk.

Vulnerability to Travel Retail Fluctuations

Amorepacific depends heavily on duty-free channels—these accounted for about 18% of group sales in 2023—so fluctuations in international travel hit revenue fast; for example, Korea duty-free sales fell 40% in 2020 and bounced unevenly, leaving FY2022 duty-free recovery still ~15% below 2019 levels. Any health crisis or geopolitics can thus cause immediate, sharp shortfalls, reducing resilience to travel-sector shocks.

Complex Organizational Structure and Brand Overlap

The vast Amorepacific portfolio — 30+ brands and 2024 consolidated revenue KRW 6.4 trillion — creates internal cannibalization and consumer confusion, especially in the crowded mid-range segment where Mamonde and Etude overlap.

Overlapping SKUs dilute brand identity and marketing ROI; administrative overhead for governance and 2024 operating margin 8.7% can slow agile launches and decisions.

- 30+ brands (2024)

- KRW 6.4T revenue (2024)

- Operating margin 8.7% (2024)

- Mid-range SKU overlap hurts brand clarity

- Higher admin cost slows decisions

Slower Market Penetration in Western Mass Retail

Amorepacific excels in prestige channels but lags in securing shelf space in high-volume Western drugstores and supermarkets, limiting access to price-sensitive shoppers.

The brand prioritized specialty retailers like Sephora in North America and Europe, so mass-market penetration remains under 10% of its Western retail footprint as of 2025.

This restricted presence reduces revenue upside versus local mass brands that capture large volume—e.g., U.S. drugstore chains generated over $40B in beauty sales in 2024.

- Prestige-focused distribution

- Mass-market share <10% in West (2025)

- Missed access to $40B+ U.S. drugstore beauty market

Amorepacific: East‑Asia concentration and high costs fuel volatile, margin‑pressed growth

| Metric | Value |

|---|---|

| East Asia rev share (FY2025) | 62% |

| China share | 41% |

| S. Korea share | 21% |

| Duty-free sales (2023) | 18% |

| SG&A (2024) | ₩522.4B |

| R&D (2024) | ₩72.3B |

| Operating margin (2024) | 8.7% |

| Brands (2024) | 30+ |

| Mass-market West share (2025) | <10% |

Full Version Awaits

Amorepacific SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the same editable file delivered after checkout. You’re viewing a live excerpt of the complete, structured Amorepacific SWOT analysis; buy now to unlock the full, detailed report.