Apollo Global Management SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Apollo Global Management combines scale, private markets expertise, and strong fee-generating platforms, yet faces cyclicality, regulatory scrutiny, and valuation risks in a competitive alternative-asset landscape. Discover the full SWOT analysis for actionable insights, financial context, and a downloadable Word + Excel package to support investment decisions, pitches, and strategic planning—purchase the complete report to move from snapshot to strategy.

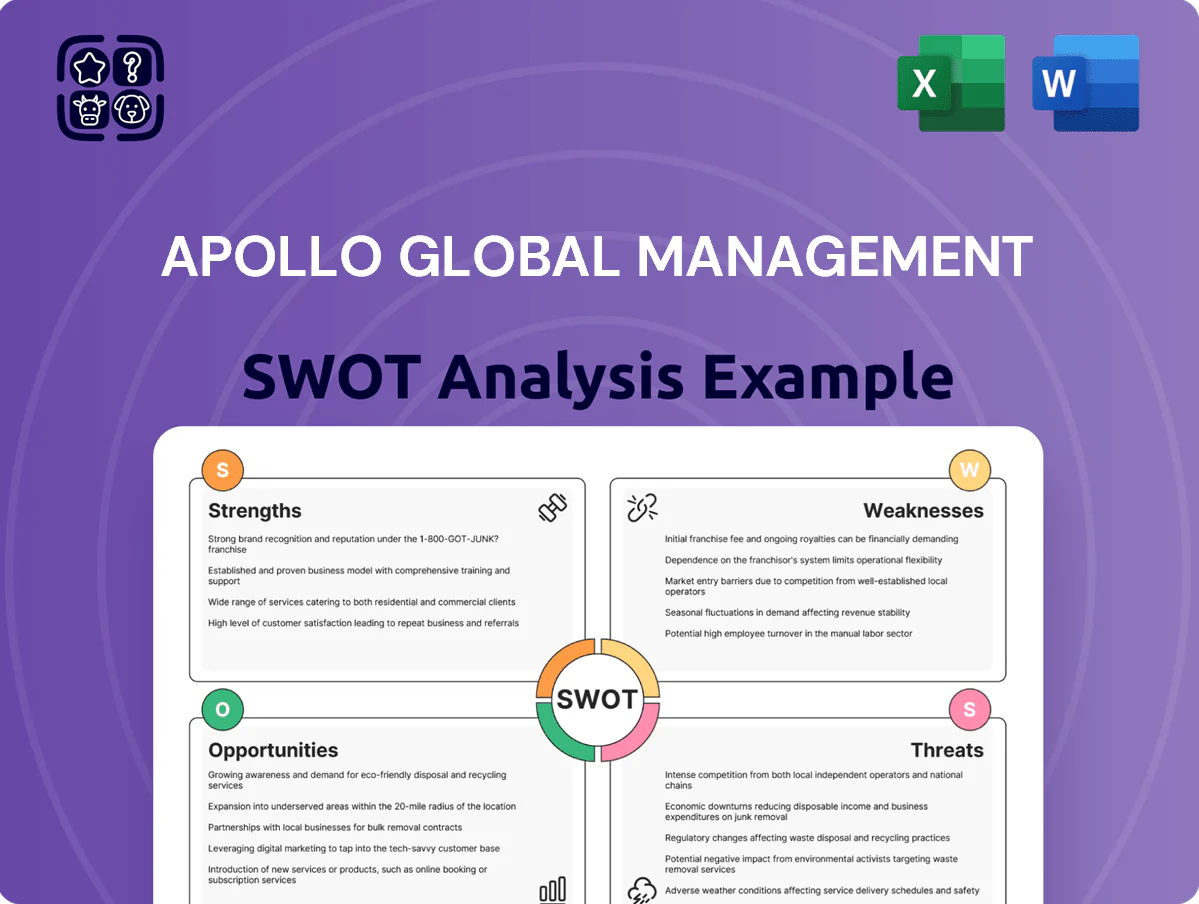

Strengths

Dominant Credit and Yield Platform

Apollo’s dominant private credit platform leverages $548 billion AUM (2025 firm report) to originate higher-quality debt at scale, generating a steady proprietary deal flow often closed to banks due to regulatory constraints. This ecosystem produced $18 billion of direct lending commitments in 2024, and its bespoke financing capability—stretching unitranche and structured solutions—remains a key competitive advantage in volatile markets through end-2025.

Synergistic Athene Integration

The full integration of Athene gives Apollo Global Management a permanent capital base—Athene held $220 billion of invested assets and contributed about $1.9 billion in operating earnings in 2024—cutting reliance on periodic fundraises.

This insurance-led model supplies steady AUM inflows that Apollo can deploy into high-yield credit; Apollo reported $670 billion AUM total by Q4 2024, with credit a growing mix.

Predictable fee income and spread-based earnings from Athene helped Apollo stabilize revenue volatility, raising recurring revenue share and improving net income resilience versus pure-play PE peers.

Disciplined Value-Oriented Investing

Apollo Global Management keeps a disciplined, contrarian value approach, prioritizing strict purchase-price discipline and hands-on operational fixes; their $548bn AUM (end-2024) and 27% private equity realized IRR since 2019 show the payoff.

The firm’s deep restructuring and distressed-assets skillset—over $70bn invested in stressed transactions since 2015—lets Apollo generate alpha in downturns and protect downside while capturing upside in recoveries.

Scale and Capital Raising Prowess

As of late 2025, Apollo Global Management has scaled AUM to roughly $950 billion, nearing the $1 trillion mark after rapid fund launches and 2024–25 strategic partnerships that boosted private credit and real assets pools.

Its global distribution and long-standing ties with sovereign wealth funds and pension plans secure steady institutional inflows, letting Apollo lead and finance mega-deals worldwide.

- $950B AUM (late 2025)

- Top LPs: sovereign wealth & pension funds

- Enables largest, complex transactions

Expansion into Hybrid Value Solutions

Apollo pioneered hybrid value—securities between debt and equity—deploying about $24bn in flexible capital in 2024 to capture mid-stack opportunities and tailor structures to corporate needs.

These bespoke financings boost fee-bearing AUM and produced mid-teens net IRRs on recent deals, with returns showing low correlation to S&P 500, helping diversify the firm’s risk profile.

- Deployed ~24bn in 2024

- Targets mid-stack cashflows

- Mid-teens net IRRs on recent deals

- Low correlation to S&P 500

Apollo’s $950B AUM & Athene tie drive mid‑teens IRRs via scale in credit, real assets

Apollo’s $950B AUM (late-2025) anchors a leading private credit and real-assets franchise, with $18B direct lending in 2024 and ~$24B hybrid capital deployed that year, plus Athene’s $220B invested assets boosting recurring fee income and reducing fundraising reliance—deep distressed expertise ($70B since 2015) and sovereign/pension LPs enable large, bespoke financings and mid-teens net IRRs.

| Metric | Value |

|---|---|

| Total AUM (late-2025) | $950B |

| Direct lending (2024) | $18B |

| Hybrid capital deployed (2024) | $24B |

| Athene invested assets (2024) | $220B |

| Distressed investments since 2015 | $70B |

| Reported mid-teens net IRRs | ~15%+ |

What is included in the product

Provides a concise SWOT overview of Apollo Global Management, outlining its core strengths, operational weaknesses, strategic opportunities, and external threats to evaluate the firm’s competitive positioning and future prospects.

Delivers a focused SWOT snapshot of Apollo Global Management to speed executive alignment and decision-making.

Weaknesses

Significant Insurance Exposure Risks

Apollo’s heavy reliance on Athene (now part of Apollo since the 2022 merger) ties ~30% of assets under management to insurance-linked liabilities, making the firm sensitive to insurance regulation and capital-rule shifts like NAIC or Solvency II equivalents; a 100 bps rise in actuarial discount rates could cut earnings by an estimated mid-single digits. Unexpected claim spikes or adverse mortality/morbidity moves would pressure ROE and capital, and the insurance concentration creates sector-specific risk that more diversified managers avoid.

Operational Complexity and Scale

The rapid expansion of Apollo Global Management to $548 billion AUM as of 2025 has increased organizational complexity, straining governance and slowing decision cycles in parts of the firm. Managing ~3,400 employees across private equity, credit, and insurance demands advanced oversight and integrated tech; gaps could raise operational costs and error rates. As scale grows, inefficiencies and diluted culture pose risks to execution and retention.

Regulatory Scrutiny of Private Credit

As a dominant shadow-banking player, Apollo Global Management faces rising regulatory scrutiny after global regulators flagged private credit for systemic risk; in 2024 the Financial Stability Board noted private credit assets reached roughly $1.2 trillion, heightening oversight.

New reporting rules and possible capital buffers could constrain Apollo’s origination—private credit made up about 42% of Apollo’s $550bn AUM in 2024—reducing deal agility.

Navigating rules needs larger legal and compliance spend; if compliance costs rise 50–100 bps of fee income, margins could be meaningfully pressured.

Sensitivity to Interest Rate Volatility

Extreme interest-rate swings can hurt Apollo by revaluing fixed-income holdings and raising leverage costs even though higher rates boost yield strategies; in 2024 Apollo’s loan portfolio sensitivity showed mark-to-market swings up to 7% in stressed months.

Rapid rate moves can compress the spread between Athene’s funding cost and Apollo’s investment yields, forcing hedges that cut reported ROE; by Q4 2024 Athene funding costs rose to ~4.2%, narrowing spreads vs. target yields.

Managing this requires constant hedging and advanced risk systems, adding expense and execution risk that can destabilize earnings during volatile rate shifts.

- Marked asset revaluations: up to 7% swing

- Athene funding: ~4.2% by Q4 2024

- Higher hedging costs reduce ROE

Public Perception and ESG Challenges

Despite improved sustainability reporting, Apollo Global Management faces investor and public pressure over portfolio emissions; in 2024 critics cited carbon-intensive holdings after Apollo reported $548bn AUM in Q4 2024.

Stricter ESG mandates from pension funds and sovereigns—about 22% of large US institutional mandates tightened ESG screens in 2023—could restrict Apollo’s access to high-yield, carbon-heavy sectors.

Managing reputational risk is critical to keep broad capital access; a single large LP pullback could affect fundraising timing and fee generation.

- 2024 AUM: $548bn

- ~22% large institutions tightened ESG screens (2023)

- Risk: reduced access to carbon-heavy deals

Concentration Risk: $548B AUM, 30% Athene Link, 42% Private Credit—Rate Shocks Bite

Concentration in insurance (Athene) ties ~30% of AUM to insurance liabilities; a 100bps actuarial rate rise may cut earnings mid-single digits. $548bn AUM (2025) increases governance strain and ops costs; private credit (≈42% of AUM) faces regulatory pressure after private credit reached ~$1.2T (2024). Rate volatility caused mark-to-market swings ≈7% and Athene funding hit ~4.2% (Q4 2024).

| Metric | Value |

|---|---|

| AUM (2025) | $548bn |

| Athene-linked AUM | ~30% |

| Private credit share | ≈42% |

| Private credit market (2024) | $1.2T |

| Mark-to-market swing | ≈7% |

| Athene funding (Q4 2024) | ~4.2% |

Same Document Delivered

Apollo Global Management SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is not a sample but the real, editable analysis you'll download post-purchase. Buy now to unlock the complete, detailed version immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Apollo Global Management combines scale, private markets expertise, and strong fee-generating platforms, yet faces cyclicality, regulatory scrutiny, and valuation risks in a competitive alternative-asset landscape. Discover the full SWOT analysis for actionable insights, financial context, and a downloadable Word + Excel package to support investment decisions, pitches, and strategic planning—purchase the complete report to move from snapshot to strategy.

Strengths

Dominant Credit and Yield Platform

Apollo’s dominant private credit platform leverages $548 billion AUM (2025 firm report) to originate higher-quality debt at scale, generating a steady proprietary deal flow often closed to banks due to regulatory constraints. This ecosystem produced $18 billion of direct lending commitments in 2024, and its bespoke financing capability—stretching unitranche and structured solutions—remains a key competitive advantage in volatile markets through end-2025.

Synergistic Athene Integration

The full integration of Athene gives Apollo Global Management a permanent capital base—Athene held $220 billion of invested assets and contributed about $1.9 billion in operating earnings in 2024—cutting reliance on periodic fundraises.

This insurance-led model supplies steady AUM inflows that Apollo can deploy into high-yield credit; Apollo reported $670 billion AUM total by Q4 2024, with credit a growing mix.

Predictable fee income and spread-based earnings from Athene helped Apollo stabilize revenue volatility, raising recurring revenue share and improving net income resilience versus pure-play PE peers.

Disciplined Value-Oriented Investing

Apollo Global Management keeps a disciplined, contrarian value approach, prioritizing strict purchase-price discipline and hands-on operational fixes; their $548bn AUM (end-2024) and 27% private equity realized IRR since 2019 show the payoff.

The firm’s deep restructuring and distressed-assets skillset—over $70bn invested in stressed transactions since 2015—lets Apollo generate alpha in downturns and protect downside while capturing upside in recoveries.

Scale and Capital Raising Prowess

As of late 2025, Apollo Global Management has scaled AUM to roughly $950 billion, nearing the $1 trillion mark after rapid fund launches and 2024–25 strategic partnerships that boosted private credit and real assets pools.

Its global distribution and long-standing ties with sovereign wealth funds and pension plans secure steady institutional inflows, letting Apollo lead and finance mega-deals worldwide.

- $950B AUM (late 2025)

- Top LPs: sovereign wealth & pension funds

- Enables largest, complex transactions

Expansion into Hybrid Value Solutions

Apollo pioneered hybrid value—securities between debt and equity—deploying about $24bn in flexible capital in 2024 to capture mid-stack opportunities and tailor structures to corporate needs.

These bespoke financings boost fee-bearing AUM and produced mid-teens net IRRs on recent deals, with returns showing low correlation to S&P 500, helping diversify the firm’s risk profile.

- Deployed ~24bn in 2024

- Targets mid-stack cashflows

- Mid-teens net IRRs on recent deals

- Low correlation to S&P 500

Apollo’s $950B AUM & Athene tie drive mid‑teens IRRs via scale in credit, real assets

Apollo’s $950B AUM (late-2025) anchors a leading private credit and real-assets franchise, with $18B direct lending in 2024 and ~$24B hybrid capital deployed that year, plus Athene’s $220B invested assets boosting recurring fee income and reducing fundraising reliance—deep distressed expertise ($70B since 2015) and sovereign/pension LPs enable large, bespoke financings and mid-teens net IRRs.

| Metric | Value |

|---|---|

| Total AUM (late-2025) | $950B |

| Direct lending (2024) | $18B |

| Hybrid capital deployed (2024) | $24B |

| Athene invested assets (2024) | $220B |

| Distressed investments since 2015 | $70B |

| Reported mid-teens net IRRs | ~15%+ |

What is included in the product

Provides a concise SWOT overview of Apollo Global Management, outlining its core strengths, operational weaknesses, strategic opportunities, and external threats to evaluate the firm’s competitive positioning and future prospects.

Delivers a focused SWOT snapshot of Apollo Global Management to speed executive alignment and decision-making.

Weaknesses

Significant Insurance Exposure Risks

Apollo’s heavy reliance on Athene (now part of Apollo since the 2022 merger) ties ~30% of assets under management to insurance-linked liabilities, making the firm sensitive to insurance regulation and capital-rule shifts like NAIC or Solvency II equivalents; a 100 bps rise in actuarial discount rates could cut earnings by an estimated mid-single digits. Unexpected claim spikes or adverse mortality/morbidity moves would pressure ROE and capital, and the insurance concentration creates sector-specific risk that more diversified managers avoid.

Operational Complexity and Scale

The rapid expansion of Apollo Global Management to $548 billion AUM as of 2025 has increased organizational complexity, straining governance and slowing decision cycles in parts of the firm. Managing ~3,400 employees across private equity, credit, and insurance demands advanced oversight and integrated tech; gaps could raise operational costs and error rates. As scale grows, inefficiencies and diluted culture pose risks to execution and retention.

Regulatory Scrutiny of Private Credit

As a dominant shadow-banking player, Apollo Global Management faces rising regulatory scrutiny after global regulators flagged private credit for systemic risk; in 2024 the Financial Stability Board noted private credit assets reached roughly $1.2 trillion, heightening oversight.

New reporting rules and possible capital buffers could constrain Apollo’s origination—private credit made up about 42% of Apollo’s $550bn AUM in 2024—reducing deal agility.

Navigating rules needs larger legal and compliance spend; if compliance costs rise 50–100 bps of fee income, margins could be meaningfully pressured.

Sensitivity to Interest Rate Volatility

Extreme interest-rate swings can hurt Apollo by revaluing fixed-income holdings and raising leverage costs even though higher rates boost yield strategies; in 2024 Apollo’s loan portfolio sensitivity showed mark-to-market swings up to 7% in stressed months.

Rapid rate moves can compress the spread between Athene’s funding cost and Apollo’s investment yields, forcing hedges that cut reported ROE; by Q4 2024 Athene funding costs rose to ~4.2%, narrowing spreads vs. target yields.

Managing this requires constant hedging and advanced risk systems, adding expense and execution risk that can destabilize earnings during volatile rate shifts.

- Marked asset revaluations: up to 7% swing

- Athene funding: ~4.2% by Q4 2024

- Higher hedging costs reduce ROE

Public Perception and ESG Challenges

Despite improved sustainability reporting, Apollo Global Management faces investor and public pressure over portfolio emissions; in 2024 critics cited carbon-intensive holdings after Apollo reported $548bn AUM in Q4 2024.

Stricter ESG mandates from pension funds and sovereigns—about 22% of large US institutional mandates tightened ESG screens in 2023—could restrict Apollo’s access to high-yield, carbon-heavy sectors.

Managing reputational risk is critical to keep broad capital access; a single large LP pullback could affect fundraising timing and fee generation.

- 2024 AUM: $548bn

- ~22% large institutions tightened ESG screens (2023)

- Risk: reduced access to carbon-heavy deals

Concentration Risk: $548B AUM, 30% Athene Link, 42% Private Credit—Rate Shocks Bite

Concentration in insurance (Athene) ties ~30% of AUM to insurance liabilities; a 100bps actuarial rate rise may cut earnings mid-single digits. $548bn AUM (2025) increases governance strain and ops costs; private credit (≈42% of AUM) faces regulatory pressure after private credit reached ~$1.2T (2024). Rate volatility caused mark-to-market swings ≈7% and Athene funding hit ~4.2% (Q4 2024).

| Metric | Value |

|---|---|

| AUM (2025) | $548bn |

| Athene-linked AUM | ~30% |

| Private credit share | ≈42% |

| Private credit market (2024) | $1.2T |

| Mark-to-market swing | ≈7% |

| Athene funding (Q4 2024) | ~4.2% |

Same Document Delivered

Apollo Global Management SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is not a sample but the real, editable analysis you'll download post-purchase. Buy now to unlock the complete, detailed version immediately after checkout.