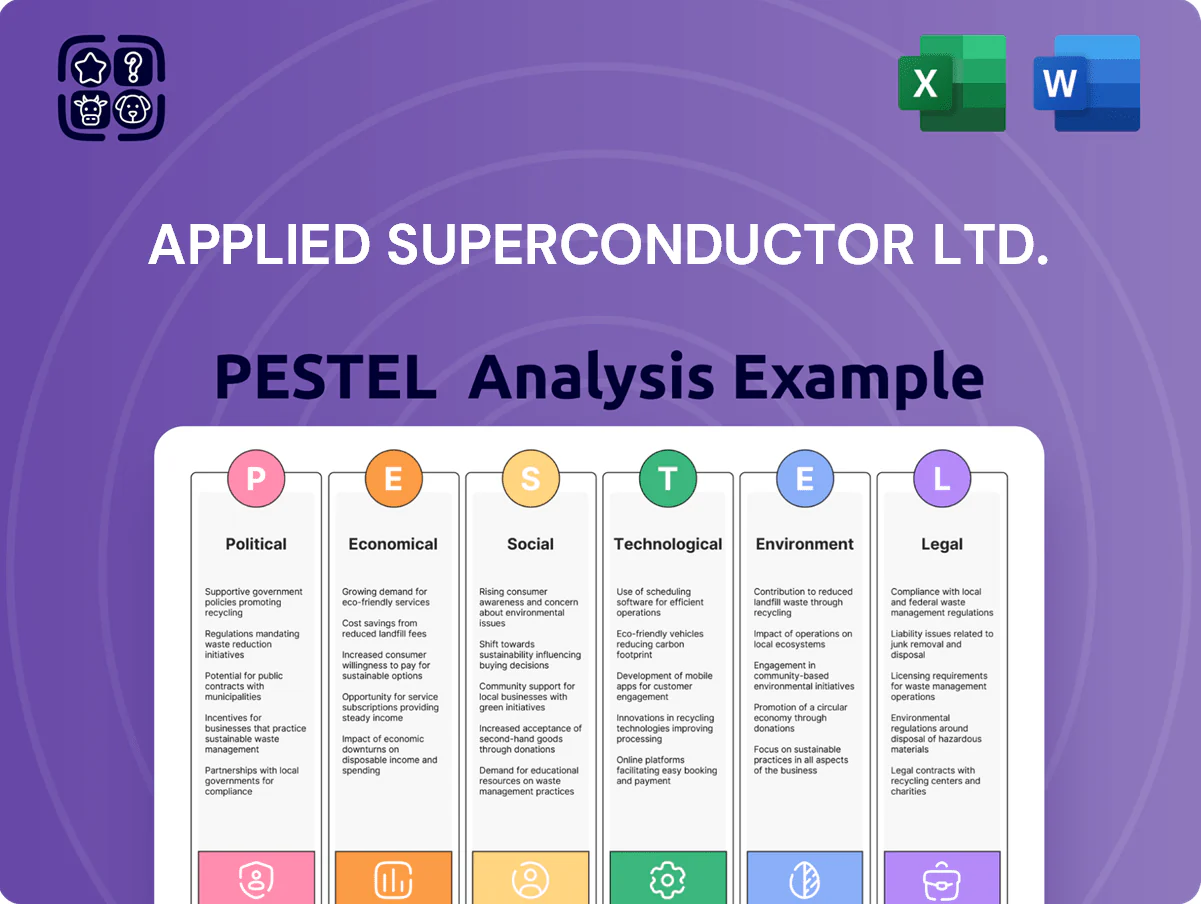

Applied Superconductor Ltd. PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and rapid tech advances are shaping Applied Superconductor Ltd.’s strategic outlook—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions; purchase the full analysis for the complete, editable report and actionable insights ready for immediate use.

Political factors

Federal Grid Modernization Grants

Federal grants under the Infrastructure Investment and Jobs Act and related programs continue funding grid resilience through 2025, with $65+ billion nationwide for grid upgrades; AMSC has secured multiple federal-backed awards enabling deployment of HTS cable solutions in urban corridors, targeting projects valued at $10–50M each and accelerating revenue recognition; bipartisan policy favoring a domestic advanced-materials supply chain positions AMSC as a strategic national asset for energy security.

Defense Procurement and Naval Contracts

The company maintains a critical relationship with the US Navy for delivery of Ship Protection Systems and advanced propulsion components, supplying AMSC with multi-year contracts valued at an estimated $150–250 million through 2026.

Defense budget allocations for 2025–2026 prioritize naval modernization and fleet electrification, with the Navy requesting $230.4 billion in FY2026 and highlighting power and propulsion upgrades as key investments.

Sustained political emphasis on maritime superiority drives a steady pipeline of long-term government contracts for AMSC's specialized hardware, supporting revenue visibility and multi-year backlog growth projected at 10–15% annually through 2026.

International Trade and Geopolitical Stability

As a global supplier, Applied Superconductor Ltd faces exposure to US trade relations with Asia and Europe; in 2024 US goods exports to the EU topped $736 billion and to China $179 billion, making market access vital for AMSC revenue streams.

Export controls on dual-use technologies require ongoing compliance with Commerce Department rules updated through 2025, affecting shipments of superconducting components classified under ECCN categories.

Geopolitical tensions risk raw-material disruptions—copper and niobium prices rose 18% and 12% in 2024 respectively—impacting production costs and competitiveness in foreign utility contracts.

Renewable Energy Policy Mandates

State and federal mandates targeting 100 percent clean electricity by 2050—over 30 states with 2030 interim targets—boost demand for AMSC’s wind turbine components and grid interconnection tech; US DOE projects wind capacity to reach 370–480 GW by 2050, increasing component markets.

Carbon pricing and emission penalties drive utilities toward high-efficiency superconducting cables; utilities facing potential compliance costs estimated in billions favor upgrades to reduce losses.

Political urgency to hit 2030 climate milestones shortens permitting timelines for large energy projects, accelerating deployment cycles and revenue recognition for AMSC’s infrastructure solutions.

- 100% clean by 2050 mandates; 30+ states with 2030 targets

- US wind capacity forecast 370–480 GW by 2050

- Carbon penalties raise utility capex for loss-reduction tech

- Faster permitting → quicker project timelines and revenues

Energy Security and Independence

The 2026 push for energy independence elevates grid efficiency as a policy priority; US federal funding for grid modernization reached about $20.5bn in 2023–25, boosting demand for AMSC’s REGAL and voltage management solutions.

REGAL systems are framed as critical for mitigating physical and cyber threats, aligning with DOE and FERC resilience standards and appealing to utilities planning 10–20 year upgrade cycles.

Bipartisan infrastructure hardening support—reflected in sustained appropriations and tax incentives—creates predictable investment horizons for AMSC’s long-term utility contracts.

- Federal grid modernization funding ~ $20.5bn (2023–25)

- Utilities target 10–20 year upgrade cycles

- REGAL positioned for cyber/physical resilience compliance

- Bipartisan support yields stable capital deployment

US funding and Navy spending boost clean-energy growth amid supply risks

Strong US federal funding (~$20.5B for grid modernization 2023–25) and FY2026 Navy request $230.4B drive multi-year contracts (AMSC defense backlog est. $150–250M through 2026), while export controls and 2024 commodity price rises (copper +18%, niobium +12%) pose supply risks; clean-energy mandates (30+ states, 100% by 2050) and DOE wind forecasts (370–480 GW by 2050) expand market demand.

| Metric | Value |

|---|---|

| Grid funding (2023–25) | $20.5B |

| Navy FY2026 request | $230.4B |

| Defense backlog | $150–250M |

| Copper/niobium 2024 | +18% / +12% |

| US wind by 2050 | 370–480 GW |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Applied Superconductor Ltd., combining current industry trends, regional regulatory context, and data-driven insights to reveal risks, opportunities, and strategic implications for executives, investors, and advisors.

A concise, visually segmented PESTLE snapshot of Applied Superconductor Ltd. that distills regulatory, technological, economic, social, and environmental risks into an easily shareable slide or note, enabling quick alignment, contextual annotations, and faster strategy discussions across teams.

Economic factors

Capital Investment Trends in Utilities

At end-2025, rising global cost of capital—US 10-year Treasury ~4.5% and average utility borrowing costs near 5.5%—dampened uptake of high-CAPEX HTS upgrades despite projected 20–30% lifetime O&M savings; utilities require lower rates or rate-case approval to justify upfront spend. AMSC tracks utility investment cycles and US state rate-case timelines to time offers and financing support, aligning sales with recently approved capital plans totaling ~$45–60B in transmission upgrades through 2026.

Raw Material Price Volatility

The production of high-temperature superconducting wire depends on rare earths and metals like yttrium, barium, and silver, whose prices swung 18–27% annually in 2023–2024; such volatility directly pressures AMSC gross margins. By late 2025 AMSC is optimizing supplier contracts and localizing inputs to curb inflation-driven cost rises after US PPI for metals rose ~11% in 2021–2024. Mining/refining disruptions can therefore move wire margins several percentage points.

Global Energy Demand Growth

Rising global electricity use—projected to grow about 2.1% annually to 2040 with data-center demand up ~8% yearly and EV fleet energy needs rising 20%+ by 2030—drives demand for high-capacity transmission where AMSC superconducting cables fit.

AMSC targets congested grids: many OECD urban networks face capacity limits, with transmission upgrade backlogs worth an estimated $300–500 billion globally.

Emerging-market GDP growth (IMF 2024: EM growth ~4.4%) and rapid electrification in Asia/Africa expand export opportunities for superconducting systems into high-growth regions.

Inflationary Pressure on Manufacturing

Persistent inflation through 2025 led Applied Materials and Systems Company to tighten manufacturing costs, with input inflation averaging 5.8% YoY in 2024 and energy costs up ~12% in 2024–25, prompting efficiency drives across facilities to protect margins.

Rising labor expenses—wage growth ~4–6% in key US and EU sites—plus higher industrial energy bills risk compressing gross margins unless offset by yield improvements and automation.

AMSC selectively raised product prices by ~3–7% in 2024 while monitoring competitiveness versus copper components, where price parity remains critical for market adoption.

- Input inflation ~5.8% (2024)

- Energy costs +12% (2024–25)

- Wage growth 4–6%

- Price hikes 3–7% (2024)

Currency Exchange Rate Risks

With ~65% of Applied Superconductor Ltd revenue tied to international wind OEMs and utilities, currency volatility poses material risk to margins and sales volumes.

A stronger US dollar vs euro or yuan in 2024–2025 reduced competitiveness in Europe/China, potentially lowering order intake by an estimated 5–10% per 10% FX move.

As of end-2025, disciplined use of forwards/options and a targeted hedge ratio near 70% is essential to stabilize earnings and protect cashflow.

- ~65% revenue international exposure

- 5–10% order sensitivity per 10% USD move

- target hedge ratio ~70% by end-2025

Macro tightening, FX risk and input swings slow HTS adoption despite O&M savings

Macro tightening and higher utility borrowing costs (US 10y ~4.5% end-2025) slow high-CAPEX HTS adoption despite 20–30% O&M savings; input cost swings (yttrium/silver ±18–27% 2023–24) and energy +12% (2024–25) pressure margins; demand growth from electricity use ~2.1%/yr and EV/data-center loads boosts addressable market; FX exposure (~65% international revenue) creates 5–10% order sensitivity per 10% USD move, prompting ~70% hedge target.

| Metric | Value |

|---|---|

| US 10y (end‑2025) | ~4.5% |

| Input price volatility (2023–24) | ±18–27% |

| Energy cost change (2024–25) | +12% |

| Revenue intl. exposure | ~65% |

| Order sensitivity per 10% USD move | 5–10% |

| Target hedge ratio | ~70% |

Full Version Awaits

Applied Superconductor Ltd. PESTLE Analysis

The preview shown here is the exact Applied Superconductor Ltd. PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and rapid tech advances are shaping Applied Superconductor Ltd.’s strategic outlook—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions; purchase the full analysis for the complete, editable report and actionable insights ready for immediate use.

Political factors

Federal Grid Modernization Grants

Federal grants under the Infrastructure Investment and Jobs Act and related programs continue funding grid resilience through 2025, with $65+ billion nationwide for grid upgrades; AMSC has secured multiple federal-backed awards enabling deployment of HTS cable solutions in urban corridors, targeting projects valued at $10–50M each and accelerating revenue recognition; bipartisan policy favoring a domestic advanced-materials supply chain positions AMSC as a strategic national asset for energy security.

Defense Procurement and Naval Contracts

The company maintains a critical relationship with the US Navy for delivery of Ship Protection Systems and advanced propulsion components, supplying AMSC with multi-year contracts valued at an estimated $150–250 million through 2026.

Defense budget allocations for 2025–2026 prioritize naval modernization and fleet electrification, with the Navy requesting $230.4 billion in FY2026 and highlighting power and propulsion upgrades as key investments.

Sustained political emphasis on maritime superiority drives a steady pipeline of long-term government contracts for AMSC's specialized hardware, supporting revenue visibility and multi-year backlog growth projected at 10–15% annually through 2026.

International Trade and Geopolitical Stability

As a global supplier, Applied Superconductor Ltd faces exposure to US trade relations with Asia and Europe; in 2024 US goods exports to the EU topped $736 billion and to China $179 billion, making market access vital for AMSC revenue streams.

Export controls on dual-use technologies require ongoing compliance with Commerce Department rules updated through 2025, affecting shipments of superconducting components classified under ECCN categories.

Geopolitical tensions risk raw-material disruptions—copper and niobium prices rose 18% and 12% in 2024 respectively—impacting production costs and competitiveness in foreign utility contracts.

Renewable Energy Policy Mandates

State and federal mandates targeting 100 percent clean electricity by 2050—over 30 states with 2030 interim targets—boost demand for AMSC’s wind turbine components and grid interconnection tech; US DOE projects wind capacity to reach 370–480 GW by 2050, increasing component markets.

Carbon pricing and emission penalties drive utilities toward high-efficiency superconducting cables; utilities facing potential compliance costs estimated in billions favor upgrades to reduce losses.

Political urgency to hit 2030 climate milestones shortens permitting timelines for large energy projects, accelerating deployment cycles and revenue recognition for AMSC’s infrastructure solutions.

- 100% clean by 2050 mandates; 30+ states with 2030 targets

- US wind capacity forecast 370–480 GW by 2050

- Carbon penalties raise utility capex for loss-reduction tech

- Faster permitting → quicker project timelines and revenues

Energy Security and Independence

The 2026 push for energy independence elevates grid efficiency as a policy priority; US federal funding for grid modernization reached about $20.5bn in 2023–25, boosting demand for AMSC’s REGAL and voltage management solutions.

REGAL systems are framed as critical for mitigating physical and cyber threats, aligning with DOE and FERC resilience standards and appealing to utilities planning 10–20 year upgrade cycles.

Bipartisan infrastructure hardening support—reflected in sustained appropriations and tax incentives—creates predictable investment horizons for AMSC’s long-term utility contracts.

- Federal grid modernization funding ~ $20.5bn (2023–25)

- Utilities target 10–20 year upgrade cycles

- REGAL positioned for cyber/physical resilience compliance

- Bipartisan support yields stable capital deployment

US funding and Navy spending boost clean-energy growth amid supply risks

Strong US federal funding (~$20.5B for grid modernization 2023–25) and FY2026 Navy request $230.4B drive multi-year contracts (AMSC defense backlog est. $150–250M through 2026), while export controls and 2024 commodity price rises (copper +18%, niobium +12%) pose supply risks; clean-energy mandates (30+ states, 100% by 2050) and DOE wind forecasts (370–480 GW by 2050) expand market demand.

| Metric | Value |

|---|---|

| Grid funding (2023–25) | $20.5B |

| Navy FY2026 request | $230.4B |

| Defense backlog | $150–250M |

| Copper/niobium 2024 | +18% / +12% |

| US wind by 2050 | 370–480 GW |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Applied Superconductor Ltd., combining current industry trends, regional regulatory context, and data-driven insights to reveal risks, opportunities, and strategic implications for executives, investors, and advisors.

A concise, visually segmented PESTLE snapshot of Applied Superconductor Ltd. that distills regulatory, technological, economic, social, and environmental risks into an easily shareable slide or note, enabling quick alignment, contextual annotations, and faster strategy discussions across teams.

Economic factors

Capital Investment Trends in Utilities

At end-2025, rising global cost of capital—US 10-year Treasury ~4.5% and average utility borrowing costs near 5.5%—dampened uptake of high-CAPEX HTS upgrades despite projected 20–30% lifetime O&M savings; utilities require lower rates or rate-case approval to justify upfront spend. AMSC tracks utility investment cycles and US state rate-case timelines to time offers and financing support, aligning sales with recently approved capital plans totaling ~$45–60B in transmission upgrades through 2026.

Raw Material Price Volatility

The production of high-temperature superconducting wire depends on rare earths and metals like yttrium, barium, and silver, whose prices swung 18–27% annually in 2023–2024; such volatility directly pressures AMSC gross margins. By late 2025 AMSC is optimizing supplier contracts and localizing inputs to curb inflation-driven cost rises after US PPI for metals rose ~11% in 2021–2024. Mining/refining disruptions can therefore move wire margins several percentage points.

Global Energy Demand Growth

Rising global electricity use—projected to grow about 2.1% annually to 2040 with data-center demand up ~8% yearly and EV fleet energy needs rising 20%+ by 2030—drives demand for high-capacity transmission where AMSC superconducting cables fit.

AMSC targets congested grids: many OECD urban networks face capacity limits, with transmission upgrade backlogs worth an estimated $300–500 billion globally.

Emerging-market GDP growth (IMF 2024: EM growth ~4.4%) and rapid electrification in Asia/Africa expand export opportunities for superconducting systems into high-growth regions.

Inflationary Pressure on Manufacturing

Persistent inflation through 2025 led Applied Materials and Systems Company to tighten manufacturing costs, with input inflation averaging 5.8% YoY in 2024 and energy costs up ~12% in 2024–25, prompting efficiency drives across facilities to protect margins.

Rising labor expenses—wage growth ~4–6% in key US and EU sites—plus higher industrial energy bills risk compressing gross margins unless offset by yield improvements and automation.

AMSC selectively raised product prices by ~3–7% in 2024 while monitoring competitiveness versus copper components, where price parity remains critical for market adoption.

- Input inflation ~5.8% (2024)

- Energy costs +12% (2024–25)

- Wage growth 4–6%

- Price hikes 3–7% (2024)

Currency Exchange Rate Risks

With ~65% of Applied Superconductor Ltd revenue tied to international wind OEMs and utilities, currency volatility poses material risk to margins and sales volumes.

A stronger US dollar vs euro or yuan in 2024–2025 reduced competitiveness in Europe/China, potentially lowering order intake by an estimated 5–10% per 10% FX move.

As of end-2025, disciplined use of forwards/options and a targeted hedge ratio near 70% is essential to stabilize earnings and protect cashflow.

- ~65% revenue international exposure

- 5–10% order sensitivity per 10% USD move

- target hedge ratio ~70% by end-2025

Macro tightening, FX risk and input swings slow HTS adoption despite O&M savings

Macro tightening and higher utility borrowing costs (US 10y ~4.5% end-2025) slow high-CAPEX HTS adoption despite 20–30% O&M savings; input cost swings (yttrium/silver ±18–27% 2023–24) and energy +12% (2024–25) pressure margins; demand growth from electricity use ~2.1%/yr and EV/data-center loads boosts addressable market; FX exposure (~65% international revenue) creates 5–10% order sensitivity per 10% USD move, prompting ~70% hedge target.

| Metric | Value |

|---|---|

| US 10y (end‑2025) | ~4.5% |

| Input price volatility (2023–24) | ±18–27% |

| Energy cost change (2024–25) | +12% |

| Revenue intl. exposure | ~65% |

| Order sensitivity per 10% USD move | 5–10% |

| Target hedge ratio | ~70% |

Full Version Awaits

Applied Superconductor Ltd. PESTLE Analysis

The preview shown here is the exact Applied Superconductor Ltd. PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and investment decisions.