Aptar Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

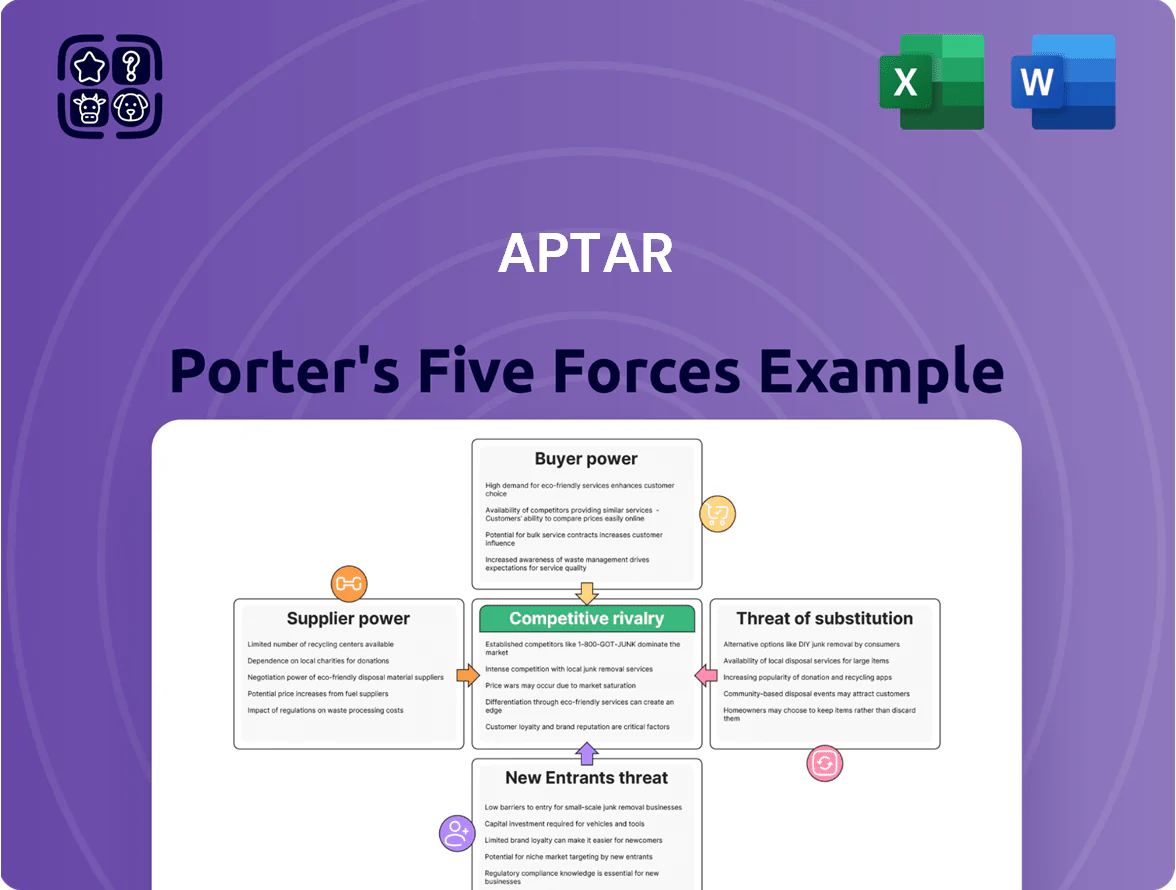

Aptar operates in a competitive packaging and dispensing market where supplier relationships, customer concentration, and innovation-driven substitutes shape margins and growth prospects; regulatory and scale barriers temper new entrants but competitive rivalry remains intense.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aptar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Aptar Group depends on plastic resins, aluminum and specialty rubber from global commodity markets; resin costs rose ~28% in 2021–2022 and crude oil jumped from $50/barrel (Jan 2021) to $120/barrel (Mar 2022), showing sensitivity to petroleum swings.

Index‑linked supply contracts let Aptar pass part of input moves to customers, but sudden raw‑material spikes (e.g., a 30% resin surge) can compress gross margins—Aptar’s 2022 gross margin fell to 29.8% from 32.4% in 2021—before repricing.

Concentration of polymer producers

The supply of high-quality polymers and specialty resins is concentrated: the top 5 chemical firms (BASF, Dow, SABIC, LyondellBasell, and Covestro) held roughly 42% of global polyolefin/resin market share in 2024, giving suppliers pricing leverage due to low substitutability and technical specs.

Aptar depends on these inputs for closures and pumps, so suppliers can pressure prices; in 2024 resin price spikes added an estimated 3–4% to Aptar’s COGS in pockets of its 2023–2024 procurement cycle.

To reduce risk, Aptar keeps multi-sourcing agreements and strategic inventory; by end-2024 it reported supplier diversification across 4+ Tier-1 resin vendors per product line, limiting single-supplier exposure.

Transition to sustainable feedstocks

As of late 2025, demand for post-consumer recycled (PCR) resins outstrips supply—global PCR resin prices rose ~22% YoY and availability tightened, giving certified sustainable-material suppliers higher bargaining power over Aptar.

Aptar faces binding ESG targets and EU/US recycled-content rules, so it must lock long-term supply contracts; in 2024 Aptar reported 18% of plastics as recycled, pushing procurement toward multi-year deals to avoid production disruptions.

Energy and logistics dependencies

Manufacturing dispensing systems is energy-intensive, making Aptar vulnerable to regional utility price swings and carbon taxes; in 2024 European industrial power prices spiked ~40% vs 2020, raising COGS for plastics/assembly lines.

Logistics providers hold leverage as Aptar ships across North America, Europe, Asia and South America; global container freight rates averaged $2,000/FEU in 2024, and rising transport decarbonization mandates increase procurement costs.

- Energy cost sensitivity: ~40% price surge in EU power since 2020

- Carbon exposure: rising regional carbon taxes

- Freight pressure: ~$2,000/FEU avg 2024

- Decarbonization mandates raise carrier premiums

Specialized pharma components

In Aptar’s pharmaceutical business, suppliers of medical-grade, specialty components hold moderate bargaining power because replacing them triggers costly re-validation and regulatory approvals; Aptar reported 2024 pharma segment revenue of $1.2 billion, so supply disruption risks tangible.

Aptar mitigates this by forming deep technical partnerships and dual-sourcing where possible, cutting supplier-related downtime and meeting FDA/EMA standards.

- High switching cost: re-validation months to >1 year

- 2024 pharma revenue: $1.2B

- Mitigation: technical collaborations, dual-sourcing

Supplier shocks squeeze Aptar margins; multi-sourcing and PCR deals mitigate costs

Suppliers hold moderate-to-high power: concentrated resin suppliers (top5 ~42% share in 2024), PCR shortages (+22% price YoY 2024), energy/freight shocks (EU power +40% vs 2020; $2,000/FEU 2024) raised Aptar’s COGS (~3–4% pockets) and compressed margins (gross margin 29.8% 2022); Aptar offsets via index-linked contracts, multi-sourcing (4+ Tier‑1 vendors), long-term PCR deals and pharma technical partnerships.

| Metric | Value |

|---|---|

| Top5 resin share (2024) | ~42% |

| PCR price change (2024) | +22% YoY |

| EU industrial power (vs 2020) | +40% |

| Avg container rate (2024) | $2,000/FEU |

| Aptar gross margin (2022) | 29.8% |

What is included in the product

Tailored exclusively for Aptar, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats—supported by industry insights to inform pricing, profitability, and strategic positioning.

One-sheet Porter’s Five Forces for Aptar—instant visibility into supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic choices.

Customers Bargaining Power

Consolidation of global CPG brands

Aptar serves massive CPG firms such as L'Oreal, Unilever, and Procter & Gamble, whose combined annual CPG spend exceeds tens of billions; a single global buyer can account for 5–10% of a supplier’s revenue, giving them strong leverage. These customers use scale to push for lower unit prices, faster lead times, and joint R&D on closures and dispensing tech. That concentration compresses Aptar’s margins unless it boosts operational efficiency—Aptar reported adjusted EBITDA margin of 16.4% in 2024, so cost improvements directly protect profitability. Suppliers must also invest in innovation to meet buyer demands or risk contract loss.

High switching costs in Pharma

In drug delivery, customers face high switching costs because FDA/EMA filings often name the exact dispensing device tied to a drug; changing suppliers can add 12–36 months and $5–50m in revalidation and clinical bridging, so manufacturers stick with proven partners. This technical lock-in strengthens Aptar’s moat in its highest-margin devices—Aptar reported 2024 device revenue of $1.1bn, keeping churn low and gross margins above 40% in that segment.

Demand for custom innovation

Customers now demand proprietary dispensing innovations to stand out and improve UX, giving them leverage to seek exclusivity; in 2024 Aptar reported R&D spend of $152M (≈3.8% of revenue) and must weigh custom projects that can lift ASPs against losing SKU scale; exclusive licensing can boost customer retention but may shrink addressable market—balancing bespoke work with scaling core platforms kept gross margin steady at 30.2% in FY2024.

Sustainability and circularity mandates

By end-2025, corporate customers face intense net-zero targets, pushing demand for fully recyclable or refillable packaging; 72% of CPG execs in a 2024 McKinsey survey said sustainability influenced supplier selection.

Buyers can switch to suppliers offering advanced eco-solutions, giving them leverage over Aptar unless Aptar scales sustainable-design R&D and circular offerings rapidly.

- 72% of CPG execs (2024) say sustainability shapes supplier choice

- Global refillable packaging market projected at $10.5B by 2025

- Aptar must increase sustainable SKUs and recyclability rates to keep contracts

Price sensitivity in Beauty and Home Care

Beauty and Home Care buyers show high price sensitivity: NielsenIQ reported in 2024 that 48% of U.S. shoppers switched brands after a 5%+ price rise, unlike Pharma where margins absorb hikes.

If Aptar increases prices aggressively, clients may shift to regional lower-cost converters or reduce pack complexity, risking share loss in a segment where average retail margins are 10–20%.

So Aptar must balance premium features with competitive pricing; in 2024 Aptar’s packaging solutions saw 3–5% volume decline when price gaps exceeded 7% versus rivals.

- 48% brand-switch at 5%+ price rise

- Retail margins 10–20% in Beauty/Home Care

- 3–5% volume drop if price gap >7%

- Risk: shift to regional low-cost suppliers

Aptar: Margin resilience vs. buyer pressure amid pharma lock‑in and sustainability shifts

Large CPG clients (5–10% of supplier rev) exert strong price and innovation pressure; Aptar’s FY2024 adjusted EBITDA margin 16.4% and device gross margin >40% show both vulnerability and strength. Pharma switching costs (12–36 months, $5–50m) protect high‑margin device revenue ($1.1bn in 2024). Sustainability demand (72% of CPG execs, 2024) and refillable market ($10.5B by 2025) raise leverage for buyers.

Same Document Delivered

Aptar Porter's Five Forces Analysis

This preview shows the exact Aptar Porter’s Five Forces analysis you will receive immediately after purchase—no placeholders or mockups.

The document displayed is the final, professionally formatted file, ready for download and use the moment you buy.

No samples or edits are missing: once payment is complete, you’ll have instant access to this exact, ready-to-use analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Aptar operates in a competitive packaging and dispensing market where supplier relationships, customer concentration, and innovation-driven substitutes shape margins and growth prospects; regulatory and scale barriers temper new entrants but competitive rivalry remains intense.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aptar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Aptar Group depends on plastic resins, aluminum and specialty rubber from global commodity markets; resin costs rose ~28% in 2021–2022 and crude oil jumped from $50/barrel (Jan 2021) to $120/barrel (Mar 2022), showing sensitivity to petroleum swings.

Index‑linked supply contracts let Aptar pass part of input moves to customers, but sudden raw‑material spikes (e.g., a 30% resin surge) can compress gross margins—Aptar’s 2022 gross margin fell to 29.8% from 32.4% in 2021—before repricing.

Concentration of polymer producers

The supply of high-quality polymers and specialty resins is concentrated: the top 5 chemical firms (BASF, Dow, SABIC, LyondellBasell, and Covestro) held roughly 42% of global polyolefin/resin market share in 2024, giving suppliers pricing leverage due to low substitutability and technical specs.

Aptar depends on these inputs for closures and pumps, so suppliers can pressure prices; in 2024 resin price spikes added an estimated 3–4% to Aptar’s COGS in pockets of its 2023–2024 procurement cycle.

To reduce risk, Aptar keeps multi-sourcing agreements and strategic inventory; by end-2024 it reported supplier diversification across 4+ Tier-1 resin vendors per product line, limiting single-supplier exposure.

Transition to sustainable feedstocks

As of late 2025, demand for post-consumer recycled (PCR) resins outstrips supply—global PCR resin prices rose ~22% YoY and availability tightened, giving certified sustainable-material suppliers higher bargaining power over Aptar.

Aptar faces binding ESG targets and EU/US recycled-content rules, so it must lock long-term supply contracts; in 2024 Aptar reported 18% of plastics as recycled, pushing procurement toward multi-year deals to avoid production disruptions.

Energy and logistics dependencies

Manufacturing dispensing systems is energy-intensive, making Aptar vulnerable to regional utility price swings and carbon taxes; in 2024 European industrial power prices spiked ~40% vs 2020, raising COGS for plastics/assembly lines.

Logistics providers hold leverage as Aptar ships across North America, Europe, Asia and South America; global container freight rates averaged $2,000/FEU in 2024, and rising transport decarbonization mandates increase procurement costs.

- Energy cost sensitivity: ~40% price surge in EU power since 2020

- Carbon exposure: rising regional carbon taxes

- Freight pressure: ~$2,000/FEU avg 2024

- Decarbonization mandates raise carrier premiums

Specialized pharma components

In Aptar’s pharmaceutical business, suppliers of medical-grade, specialty components hold moderate bargaining power because replacing them triggers costly re-validation and regulatory approvals; Aptar reported 2024 pharma segment revenue of $1.2 billion, so supply disruption risks tangible.

Aptar mitigates this by forming deep technical partnerships and dual-sourcing where possible, cutting supplier-related downtime and meeting FDA/EMA standards.

- High switching cost: re-validation months to >1 year

- 2024 pharma revenue: $1.2B

- Mitigation: technical collaborations, dual-sourcing

Supplier shocks squeeze Aptar margins; multi-sourcing and PCR deals mitigate costs

Suppliers hold moderate-to-high power: concentrated resin suppliers (top5 ~42% share in 2024), PCR shortages (+22% price YoY 2024), energy/freight shocks (EU power +40% vs 2020; $2,000/FEU 2024) raised Aptar’s COGS (~3–4% pockets) and compressed margins (gross margin 29.8% 2022); Aptar offsets via index-linked contracts, multi-sourcing (4+ Tier‑1 vendors), long-term PCR deals and pharma technical partnerships.

| Metric | Value |

|---|---|

| Top5 resin share (2024) | ~42% |

| PCR price change (2024) | +22% YoY |

| EU industrial power (vs 2020) | +40% |

| Avg container rate (2024) | $2,000/FEU |

| Aptar gross margin (2022) | 29.8% |

What is included in the product

Tailored exclusively for Aptar, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats—supported by industry insights to inform pricing, profitability, and strategic positioning.

One-sheet Porter’s Five Forces for Aptar—instant visibility into supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic choices.

Customers Bargaining Power

Consolidation of global CPG brands

Aptar serves massive CPG firms such as L'Oreal, Unilever, and Procter & Gamble, whose combined annual CPG spend exceeds tens of billions; a single global buyer can account for 5–10% of a supplier’s revenue, giving them strong leverage. These customers use scale to push for lower unit prices, faster lead times, and joint R&D on closures and dispensing tech. That concentration compresses Aptar’s margins unless it boosts operational efficiency—Aptar reported adjusted EBITDA margin of 16.4% in 2024, so cost improvements directly protect profitability. Suppliers must also invest in innovation to meet buyer demands or risk contract loss.

High switching costs in Pharma

In drug delivery, customers face high switching costs because FDA/EMA filings often name the exact dispensing device tied to a drug; changing suppliers can add 12–36 months and $5–50m in revalidation and clinical bridging, so manufacturers stick with proven partners. This technical lock-in strengthens Aptar’s moat in its highest-margin devices—Aptar reported 2024 device revenue of $1.1bn, keeping churn low and gross margins above 40% in that segment.

Demand for custom innovation

Customers now demand proprietary dispensing innovations to stand out and improve UX, giving them leverage to seek exclusivity; in 2024 Aptar reported R&D spend of $152M (≈3.8% of revenue) and must weigh custom projects that can lift ASPs against losing SKU scale; exclusive licensing can boost customer retention but may shrink addressable market—balancing bespoke work with scaling core platforms kept gross margin steady at 30.2% in FY2024.

Sustainability and circularity mandates

By end-2025, corporate customers face intense net-zero targets, pushing demand for fully recyclable or refillable packaging; 72% of CPG execs in a 2024 McKinsey survey said sustainability influenced supplier selection.

Buyers can switch to suppliers offering advanced eco-solutions, giving them leverage over Aptar unless Aptar scales sustainable-design R&D and circular offerings rapidly.

- 72% of CPG execs (2024) say sustainability shapes supplier choice

- Global refillable packaging market projected at $10.5B by 2025

- Aptar must increase sustainable SKUs and recyclability rates to keep contracts

Price sensitivity in Beauty and Home Care

Beauty and Home Care buyers show high price sensitivity: NielsenIQ reported in 2024 that 48% of U.S. shoppers switched brands after a 5%+ price rise, unlike Pharma where margins absorb hikes.

If Aptar increases prices aggressively, clients may shift to regional lower-cost converters or reduce pack complexity, risking share loss in a segment where average retail margins are 10–20%.

So Aptar must balance premium features with competitive pricing; in 2024 Aptar’s packaging solutions saw 3–5% volume decline when price gaps exceeded 7% versus rivals.

- 48% brand-switch at 5%+ price rise

- Retail margins 10–20% in Beauty/Home Care

- 3–5% volume drop if price gap >7%

- Risk: shift to regional low-cost suppliers

Aptar: Margin resilience vs. buyer pressure amid pharma lock‑in and sustainability shifts

Large CPG clients (5–10% of supplier rev) exert strong price and innovation pressure; Aptar’s FY2024 adjusted EBITDA margin 16.4% and device gross margin >40% show both vulnerability and strength. Pharma switching costs (12–36 months, $5–50m) protect high‑margin device revenue ($1.1bn in 2024). Sustainability demand (72% of CPG execs, 2024) and refillable market ($10.5B by 2025) raise leverage for buyers.

Same Document Delivered

Aptar Porter's Five Forces Analysis

This preview shows the exact Aptar Porter’s Five Forces analysis you will receive immediately after purchase—no placeholders or mockups.

The document displayed is the final, professionally formatted file, ready for download and use the moment you buy.

No samples or edits are missing: once payment is complete, you’ll have instant access to this exact, ready-to-use analysis.