Aptar PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and emerging technologies are shaping Aptar’s strategic outlook with our concise PESTLE snapshot—designed for investors and strategists who need insight fast. Buy the full PESTLE to unlock detailed risk assessments, regulatory implications, and actionable opportunities tailored to Aptar’s markets. Download now for a ready-to-use analysis that speeds decision-making and strengthens your competitive edge.

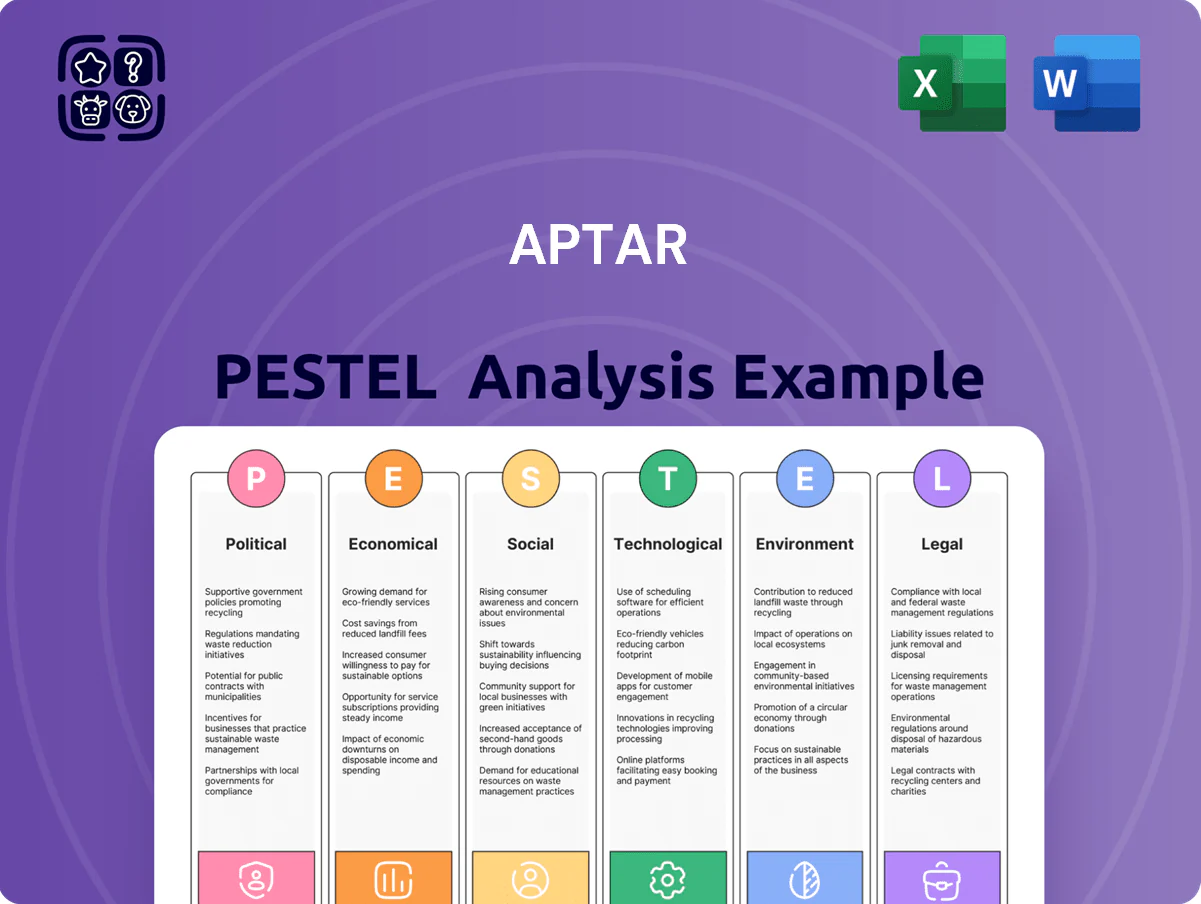

Political factors

Geopolitical Trade Tensions and Tariff Barriers

The global distribution network of Aptar is increasingly sensitive to shifting trade policies between the United States, China, and the European Union, with tariffs and non-tariff barriers raising landed costs by an estimated 3–7% in 2024–2025 for specialty components.

As of late 2025, rising protectionist measures and regional trade blocs push Aptar toward localized manufacturing; establishing regional plants can reduce import duties that otherwise add up to 8–12% on high-value packaging parts.

Analysts should monitor geopolitical shifts, since reconfigured supply chains could increase operating costs and capex—Aptar reported global cost-of-goods pressures of roughly 2–4% in 2024—and materially affect margins in pharmaceutical and beauty packaging.

Global Healthcare Reform and Drug Pricing Policies

Government efforts to curb healthcare spending in the US and EU—such as US IRA provisions affecting drug pricing and EU price-revision initiatives—put direct pressure on Aptar's Pharma segment by prompting pharma clients to seek lower-cost delivery solutions. Recent moves targeting single-drug price reductions of up to 20–30% in certain markets can compress pharma margins, increasing demand for cost-efficient dispensing technologies. Aptar must pivot its value proposition toward demonstrated cost-per-dose savings and adherence gains—studies show adherence-improving devices can cut total treatment costs by ~10–15%—to retain contracts and justify premium pricing.

Regional Political Stability in Emerging Markets

Aptar’s expansion into Southeast Asia and Latin America exposes it to political volatility; World Bank data show political stability scores vary from -0.5 to 0.3 across key markets in 2024, increasing disruption risk to plants and logistics hubs. Sudden leadership changes or unrest in 2023–24 caused average port delays of 12–18% in the region, threatening on‑time delivery and revenue. Diversified geographic footprint and dual-sourcing reduce single‑country operational risk and protect supply continuity.

Domestic Manufacturing Incentives and Reshoring

Many governments offered large reshoring incentives: the US CHIPS+ and Inflation Reduction Act enabled manufacturing tax credits and grants, while the EU pledged over €100 billion in industrial support for strategic supply chains in 2024–25, allowing Aptar to seek subsidies to modernize North American and European plants.

Political backing supports capital-heavy automation: US Federal programs and state-level grants can cover 20–40% of qualifying capex, lowering Aptar’s payback horizons for advanced filling and packaging lines and strengthening its role in secure medical and consumer supply chains.

- Leverage US/EU grants (€100B+ EU, multi‑billion US programs)

- Potential 20–40% capex offsets for automation

- Aligns Aptar investments with national supply‑security priorities

Governmental Sustainability Mandates

Political pressure has driven national targets for recycled content and packaging circularity by 2026, with the EU requiring 30% recycled plastic in PET bottles and several countries mandating similar thresholds, pressuring suppliers like Aptar to adapt.

Extended producer responsibility schemes now hold manufacturers accountable for end-of-life costs; global EPR expansion grew 18% in 2024, increasing compliance costs and shifting CAPEX toward recyclable and refillable dispensing designs.

Aptar’s ability to meet these mandates—reflected in its 2024 R&D investments of ~$120 million and rollout of bio-based and recyclable closures—will be critical to retain leadership in sustainable dispensing solutions.

- 2026 recycled-content targets (e.g., EU 30% PET)

- Global EPR expansion up 18% in 2024

- Aptar 2024 R&D ≈ $120M toward recyclable solutions

Geopolitics, pricing reform and circularity force localization, capex and R&D jumps

Political shifts—trade barriers (3–7% landed cost rise 2024–25), protectionism (8–12% duties on high‑value parts), and reshoring incentives (US/EU grants; 20–40% capex offsets)—heighten localization and capex needs; healthcare pricing reforms (potential 20–30% drug price cuts) push Pharma clients toward lower‑cost dispensing; EPR and recycled‑content mandates (EU 30% PET by 2026) raise compliance and R&D demands (Aptar 2024 R&D ≈ $120M).

| Metric | Value |

|---|---|

| Landed cost impact | 3–7% (2024–25) |

| Import duties on parts | 8–12% |

| Capex offsets | 20–40% |

| Drug price cuts risk | 20–30% |

| EU recycled PET target | 30% (2026) |

| Aptar R&D | ≈ $120M (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect Aptar across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section supported by current data and industry trends to surface actionable risks and opportunities.

A concise, visually segmented PESTLE summary of Aptar that highlights key external risks and opportunities, easily droppable into presentations or shared across teams for swift alignment and decision-making.

Economic factors

Currency Exchange Rate Volatility

Aptar generated about 72% of 2024 revenue from outside the US, exposing it to Euro, RMB and other FX swings; a 10% US dollar strength versus the euro reduced reported revenue by roughly 3–5% in past years.

Dollar moves cause translation gains/losses—Aptar reported a $21m negative FX impact in 2023—so hedging effectiveness is crucial to separate currency effects from organic growth.

Raw Material Price Fluctuations

Volatility in plastic resins and aluminum markets—resin prices rose ~18% year-over-year in 2024 while primary aluminum averaged $2,200/ton—directly pressures Aptar’s COGS and trimmed its 2024 gross margin by roughly 120 bps vs 2023.

A downturn or cost spike in petrochemicals rapidly feeds through input costs; petrochemical feedstock ethylene fell 7% in 2025 YTD, easing some margin pressure.

Aptar’s use of contractual pricing escalators and raw-material surcharges has enabled pass-through of about 60–80% of input cost increases historically, critical to preserving operating margins amid high inflation.

Global Interest Rate Environments

Central bank rate hikes push Aptar’s borrowing costs higher, raising its cost of debt and potentially reducing R&D or M&A firepower; US Fed funds at 5.25–5.50% and ECB depo at 3.25% in late 2025 squeeze yields on corporate bonds.

Higher rates in late 2025 suggest Aptar may favor conservative expansion and prioritize cash-flow optimization—free cash flow margin and net debt/EBITDA ratios will guide capex restraint.

Investors should monitor shifts in Aptar’s WACC—rising risk-free rates and credit spreads lower DCF valuations; track company guidance on interest expense and leverage for valuation impact.

Consumer Spending Power and Premiumization

The Beauty and Home Care segments are highly sensitive to discretionary spending; global cosmetics sales fell 3.5% in 2023 during tighter consumer budgets, risking lower demand for Aptar’s advanced dispensers as consumers trade down to value brands.

Conversely, emerging-market premiumization persists: middle-class households in Asia-Pacific grew by ~75 million annually (2021–2025), supporting higher-end personal care and food packaging, sustaining demand for premium dispensing systems.

- 2023 global cosmetics -3.5% vs 2022

- Asia-Pacific middle-class +~75M/year (2021–2025)

- Downtrading reduces premium dispenser demand

- Emerging-market premiumization supports long-term growth

Healthcare Spending Trends

The pharmaceutical segment shows resilience to economic cycles versus consumer-facing divisions, cushioning Aptar during slow growth; globally, healthcare spending reached about 10.3% of GDP in 2023 and is projected to hit $13.7 trillion by 2026, supporting demand for injectable and respiratory delivery systems.

This stability underpins Aptar’s financial health—pharma-related sales represented roughly 45% of Aptar’s 2024 revenue, reinforcing its investment appeal amid aging populations and rising chronic disease prevalence.

- Healthcare spending ~10.3% of global GDP (2023), $13.7T projected by 2026

- Injectable/respiratory demand grows with aging populations and chronic conditions

- Pharma ≈45% of Aptar 2024 revenue, providing economic stability

Aptar squeezed by FX, raw-materials and rising rates; pharma buffers volatility

Aptar faces FX exposure (72% 2024 revenue ex-US; a 10% USD/EUR move cut reported rev ~3–5%); 2023 FX hit $21m. Raw-material volatility raised resin +18% in 2024 and aluminum ~ $2,200/ton, shaving ~120bps gross margin; ethylene down 7% YTD 2025. Pharma (~45% 2024 rev) cushions cyclicality; rising rates (Fed 5.25–5.50%, ECB depo 3.25% late 2025) lift borrowing costs and WACC.

| Metric | Value |

|---|---|

| Revenue ex-US (2024) | ~72% |

| FX impact (2023) | $21m loss |

| Resin price change (2024) | +18% YoY |

| Aluminum (avg) | $2,200/ton |

| Pharma share (2024) | ~45% |

| Fed funds (late 2025) | 5.25–5.50% |

Preview the Actual Deliverable

Aptar PESTLE Analysis

The preview shown here is the exact Aptar PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible in this preview are precisely what you’ll download immediately after payment, with no placeholders or surprises.

Everything displayed is part of the final, professionally structured file—ready for analysis, presentation, or inclusion in your strategic workflow.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and emerging technologies are shaping Aptar’s strategic outlook with our concise PESTLE snapshot—designed for investors and strategists who need insight fast. Buy the full PESTLE to unlock detailed risk assessments, regulatory implications, and actionable opportunities tailored to Aptar’s markets. Download now for a ready-to-use analysis that speeds decision-making and strengthens your competitive edge.

Political factors

Geopolitical Trade Tensions and Tariff Barriers

The global distribution network of Aptar is increasingly sensitive to shifting trade policies between the United States, China, and the European Union, with tariffs and non-tariff barriers raising landed costs by an estimated 3–7% in 2024–2025 for specialty components.

As of late 2025, rising protectionist measures and regional trade blocs push Aptar toward localized manufacturing; establishing regional plants can reduce import duties that otherwise add up to 8–12% on high-value packaging parts.

Analysts should monitor geopolitical shifts, since reconfigured supply chains could increase operating costs and capex—Aptar reported global cost-of-goods pressures of roughly 2–4% in 2024—and materially affect margins in pharmaceutical and beauty packaging.

Global Healthcare Reform and Drug Pricing Policies

Government efforts to curb healthcare spending in the US and EU—such as US IRA provisions affecting drug pricing and EU price-revision initiatives—put direct pressure on Aptar's Pharma segment by prompting pharma clients to seek lower-cost delivery solutions. Recent moves targeting single-drug price reductions of up to 20–30% in certain markets can compress pharma margins, increasing demand for cost-efficient dispensing technologies. Aptar must pivot its value proposition toward demonstrated cost-per-dose savings and adherence gains—studies show adherence-improving devices can cut total treatment costs by ~10–15%—to retain contracts and justify premium pricing.

Regional Political Stability in Emerging Markets

Aptar’s expansion into Southeast Asia and Latin America exposes it to political volatility; World Bank data show political stability scores vary from -0.5 to 0.3 across key markets in 2024, increasing disruption risk to plants and logistics hubs. Sudden leadership changes or unrest in 2023–24 caused average port delays of 12–18% in the region, threatening on‑time delivery and revenue. Diversified geographic footprint and dual-sourcing reduce single‑country operational risk and protect supply continuity.

Domestic Manufacturing Incentives and Reshoring

Many governments offered large reshoring incentives: the US CHIPS+ and Inflation Reduction Act enabled manufacturing tax credits and grants, while the EU pledged over €100 billion in industrial support for strategic supply chains in 2024–25, allowing Aptar to seek subsidies to modernize North American and European plants.

Political backing supports capital-heavy automation: US Federal programs and state-level grants can cover 20–40% of qualifying capex, lowering Aptar’s payback horizons for advanced filling and packaging lines and strengthening its role in secure medical and consumer supply chains.

- Leverage US/EU grants (€100B+ EU, multi‑billion US programs)

- Potential 20–40% capex offsets for automation

- Aligns Aptar investments with national supply‑security priorities

Governmental Sustainability Mandates

Political pressure has driven national targets for recycled content and packaging circularity by 2026, with the EU requiring 30% recycled plastic in PET bottles and several countries mandating similar thresholds, pressuring suppliers like Aptar to adapt.

Extended producer responsibility schemes now hold manufacturers accountable for end-of-life costs; global EPR expansion grew 18% in 2024, increasing compliance costs and shifting CAPEX toward recyclable and refillable dispensing designs.

Aptar’s ability to meet these mandates—reflected in its 2024 R&D investments of ~$120 million and rollout of bio-based and recyclable closures—will be critical to retain leadership in sustainable dispensing solutions.

- 2026 recycled-content targets (e.g., EU 30% PET)

- Global EPR expansion up 18% in 2024

- Aptar 2024 R&D ≈ $120M toward recyclable solutions

Geopolitics, pricing reform and circularity force localization, capex and R&D jumps

Political shifts—trade barriers (3–7% landed cost rise 2024–25), protectionism (8–12% duties on high‑value parts), and reshoring incentives (US/EU grants; 20–40% capex offsets)—heighten localization and capex needs; healthcare pricing reforms (potential 20–30% drug price cuts) push Pharma clients toward lower‑cost dispensing; EPR and recycled‑content mandates (EU 30% PET by 2026) raise compliance and R&D demands (Aptar 2024 R&D ≈ $120M).

| Metric | Value |

|---|---|

| Landed cost impact | 3–7% (2024–25) |

| Import duties on parts | 8–12% |

| Capex offsets | 20–40% |

| Drug price cuts risk | 20–30% |

| EU recycled PET target | 30% (2026) |

| Aptar R&D | ≈ $120M (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect Aptar across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section supported by current data and industry trends to surface actionable risks and opportunities.

A concise, visually segmented PESTLE summary of Aptar that highlights key external risks and opportunities, easily droppable into presentations or shared across teams for swift alignment and decision-making.

Economic factors

Currency Exchange Rate Volatility

Aptar generated about 72% of 2024 revenue from outside the US, exposing it to Euro, RMB and other FX swings; a 10% US dollar strength versus the euro reduced reported revenue by roughly 3–5% in past years.

Dollar moves cause translation gains/losses—Aptar reported a $21m negative FX impact in 2023—so hedging effectiveness is crucial to separate currency effects from organic growth.

Raw Material Price Fluctuations

Volatility in plastic resins and aluminum markets—resin prices rose ~18% year-over-year in 2024 while primary aluminum averaged $2,200/ton—directly pressures Aptar’s COGS and trimmed its 2024 gross margin by roughly 120 bps vs 2023.

A downturn or cost spike in petrochemicals rapidly feeds through input costs; petrochemical feedstock ethylene fell 7% in 2025 YTD, easing some margin pressure.

Aptar’s use of contractual pricing escalators and raw-material surcharges has enabled pass-through of about 60–80% of input cost increases historically, critical to preserving operating margins amid high inflation.

Global Interest Rate Environments

Central bank rate hikes push Aptar’s borrowing costs higher, raising its cost of debt and potentially reducing R&D or M&A firepower; US Fed funds at 5.25–5.50% and ECB depo at 3.25% in late 2025 squeeze yields on corporate bonds.

Higher rates in late 2025 suggest Aptar may favor conservative expansion and prioritize cash-flow optimization—free cash flow margin and net debt/EBITDA ratios will guide capex restraint.

Investors should monitor shifts in Aptar’s WACC—rising risk-free rates and credit spreads lower DCF valuations; track company guidance on interest expense and leverage for valuation impact.

Consumer Spending Power and Premiumization

The Beauty and Home Care segments are highly sensitive to discretionary spending; global cosmetics sales fell 3.5% in 2023 during tighter consumer budgets, risking lower demand for Aptar’s advanced dispensers as consumers trade down to value brands.

Conversely, emerging-market premiumization persists: middle-class households in Asia-Pacific grew by ~75 million annually (2021–2025), supporting higher-end personal care and food packaging, sustaining demand for premium dispensing systems.

- 2023 global cosmetics -3.5% vs 2022

- Asia-Pacific middle-class +~75M/year (2021–2025)

- Downtrading reduces premium dispenser demand

- Emerging-market premiumization supports long-term growth

Healthcare Spending Trends

The pharmaceutical segment shows resilience to economic cycles versus consumer-facing divisions, cushioning Aptar during slow growth; globally, healthcare spending reached about 10.3% of GDP in 2023 and is projected to hit $13.7 trillion by 2026, supporting demand for injectable and respiratory delivery systems.

This stability underpins Aptar’s financial health—pharma-related sales represented roughly 45% of Aptar’s 2024 revenue, reinforcing its investment appeal amid aging populations and rising chronic disease prevalence.

- Healthcare spending ~10.3% of global GDP (2023), $13.7T projected by 2026

- Injectable/respiratory demand grows with aging populations and chronic conditions

- Pharma ≈45% of Aptar 2024 revenue, providing economic stability

Aptar squeezed by FX, raw-materials and rising rates; pharma buffers volatility

Aptar faces FX exposure (72% 2024 revenue ex-US; a 10% USD/EUR move cut reported rev ~3–5%); 2023 FX hit $21m. Raw-material volatility raised resin +18% in 2024 and aluminum ~ $2,200/ton, shaving ~120bps gross margin; ethylene down 7% YTD 2025. Pharma (~45% 2024 rev) cushions cyclicality; rising rates (Fed 5.25–5.50%, ECB depo 3.25% late 2025) lift borrowing costs and WACC.

| Metric | Value |

|---|---|

| Revenue ex-US (2024) | ~72% |

| FX impact (2023) | $21m loss |

| Resin price change (2024) | +18% YoY |

| Aluminum (avg) | $2,200/ton |

| Pharma share (2024) | ~45% |

| Fed funds (late 2025) | 5.25–5.50% |

Preview the Actual Deliverable

Aptar PESTLE Analysis

The preview shown here is the exact Aptar PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible in this preview are precisely what you’ll download immediately after payment, with no placeholders or surprises.

Everything displayed is part of the final, professionally structured file—ready for analysis, presentation, or inclusion in your strategic workflow.